- The objective of this study is to evaluate sales and demand forecasting methods to help retail businesses make sense of market trends and provide the best possible offering to their customers. In fact, for sales forecasting is a large part of supply chain planning, as the chains only provide what retailers think the customers will want.

- Time-series analysis (TSA) is an effective statistical approach for predicting sales based on historical data, allowing retailers to make data-driven decisions and enhance operational efficiency.

- Referring to the multiple TSA case study and the corresponding algorithm, we train and evaluate the FB Prophet models with cross-validation and hyper-parameter optimization (Part 1). We will examine the impact of adding change points, seasonality, and events to these TSA models.

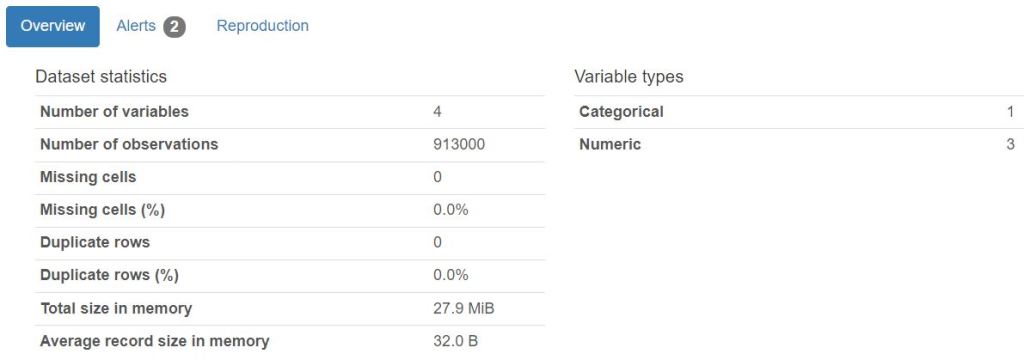

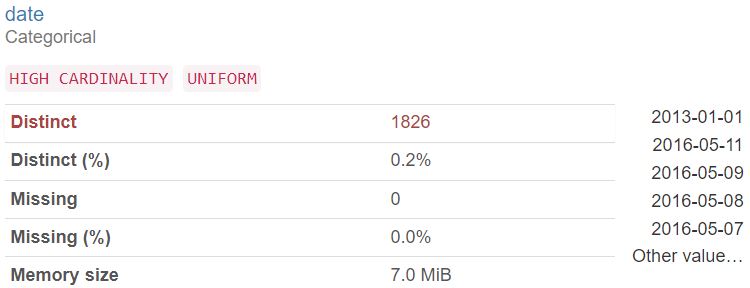

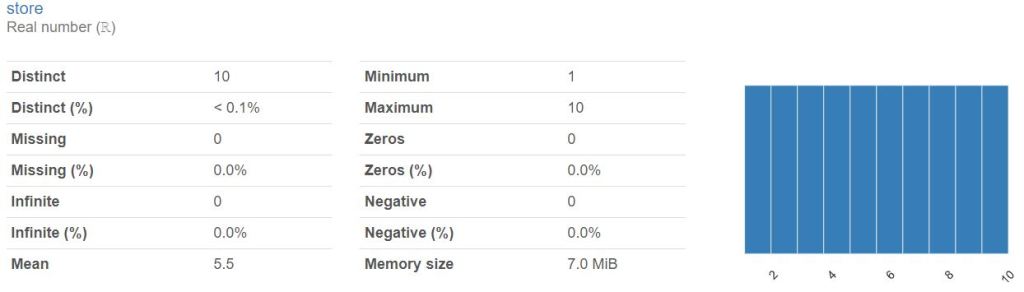

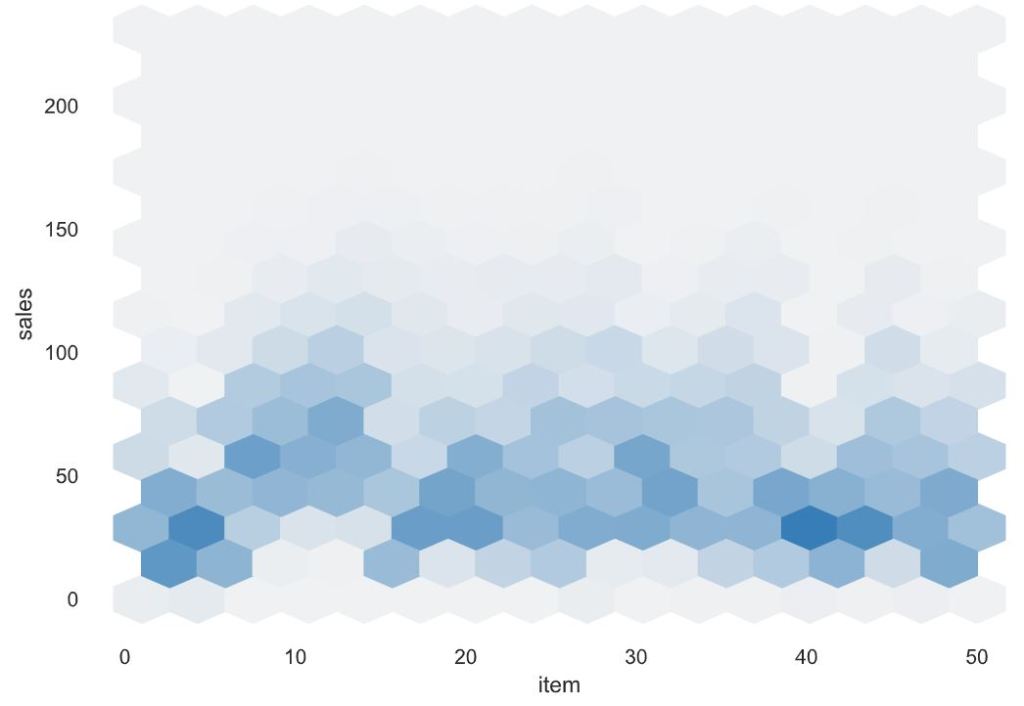

- We download the first input Kaggle dataset that has 10 different stores and each store has 50 items, i.e. total of 500 daily level time series data for 5 years. We analyze and investigate this dataset using the Pandas Profiling and SWEETVIZ AutoEDA HTML reports.

- In the second part of the post, the focus is on ARIMA models and their variants SARIMA and SARIMAX. These are widely recognized and extensively utilized TSA models.

- The aim is to unlock the power of the SARIMAX TSA in comparison with the FB Prophet, ARIMA and SARIMA predictions. In this example, we use a part of the input data that can be found here.

- To help us understand the accuracy of TSA, we compare predicted sales to real sales of the time series.

- FB Prophet X-validation plots consist of the trend, seasonal components, MAE and MAPE between expected and predicted values.

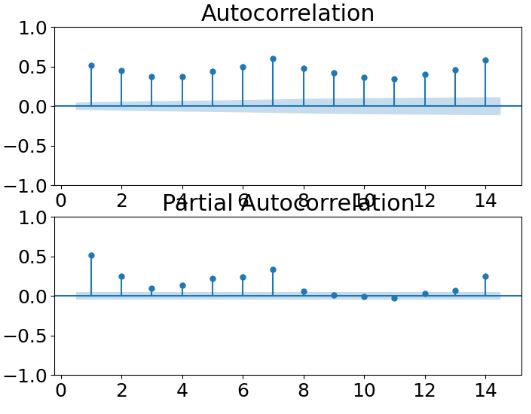

- The autocorrelation analysis (ACF and PACF) helps detect patterns and check for randomness.

- In addition to correlograms, ARIMA diagnostics plots contain standardized residuals, normal Q-Q, and histogram + estimated density.

- Points on the Normal Q-Q plot provide an indication of univariate normality of the dataset. Read more here.

- The Statsmodels’ SARIMAX QC tables can help you determine whether our SARIMAX model can actually yield meaningful information. These tables contain the following statistical metrics: Log Likelihood, AIC, BIC, HQIC, Ljung-Box, JB, H, Prob, Skew, and Kurtosis.

Table of Contents

AutoEDA

- Let’s set the working directory ARL and import the basic libraries

import os

os.chdir('ARL') # Set working directory

os. getcwd()

%matplotlib inline

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

- Reading the input data

data = pd.read_csv("trainretail.csv", index_col=0)

data = data.reset_index()

data.head()

date store item sales

0 2013-01-01 1 1 13

1 2013-01-02 1 1 11

2 2013-01-03 1 1 14

3 2013-01-04 1 1 13

4 2013-01-05 1 1 10

print(f"The dataset has {data.shape[0]} rows and {data.shape[1]} columns")

The dataset has 913000 rows and 4 columns

- Generating the Pandas Profiling Report

import pandas as pd

from pandas_profiling import ProfileReport

profile = ProfileReport(data, title="Pandas Profiling Report")

profile.to_file("reportretail.html")

Variables:

Interactions:

Correlations: store item sales

| store | 1.000 | 0.000 | -0.007 |

|---|---|---|---|

| item | 0.000 | 1.000 | -0.054 |

| sales | -0.007 | -0.054 | 1.000 |

Alerts:

date has a high cardinality: 1826 distinct values | High cardinality |

date is uniformly distributed |

- Generating the sweetviz report

import sweetviz as sv

import pandas as pd

# Create an analysis report for your data

report = sv.analyze(data)

# Display the report

report.show_html()

Variables

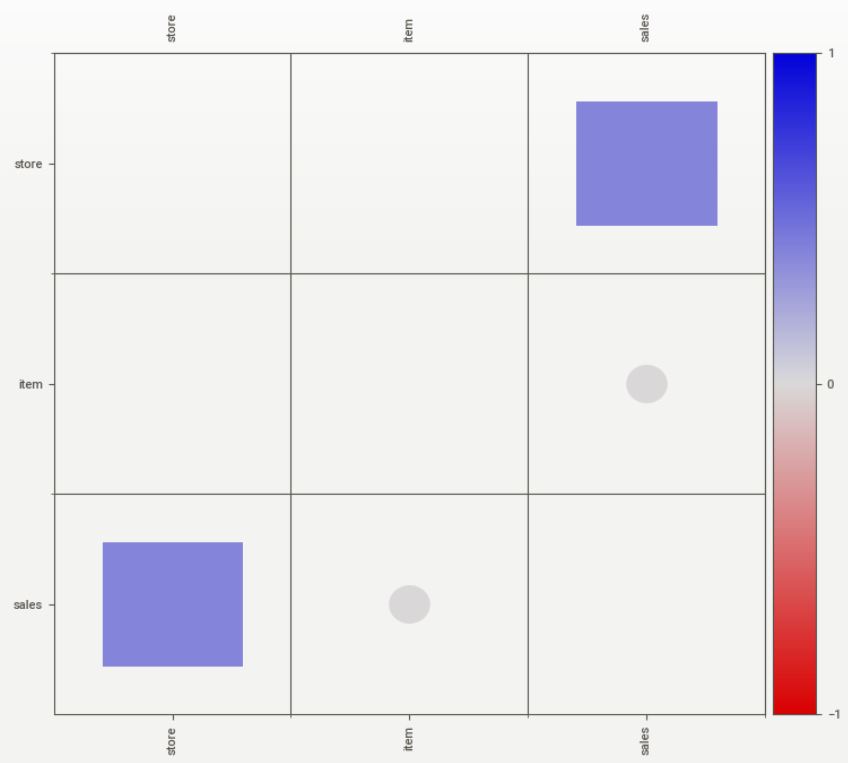

Associations

[Only including dataset “DataFrame”]

■ Squares are categorical associations (uncertainty coefficient & correlation ratio) from 0 to 1. The uncertainty coefficient is assymmetrical, (i.e. ROW LABEL values indicate how much they PROVIDE INFORMATION to each LABEL at the TOP).

• Circles are the symmetrical numerical correlations (Pearson’s) from -1 to 1. The trivial diagonal is intentionally left blank for clarity.

FB Prophet

- Preparing the input data for TSA

import itertools

multiindex = list(zip(item_sales_per_date["date"], item_sales_per_date["store_item"]))

multiindex = pd.MultiIndex.from_tuples(multiindex, names=('index_1', 'index_2'))

dataset = item_sales_per_date.copy()

dataset.index = multiindex

idx_dates = list(pd.date_range(min(item_sales_per_date["date"]), max(item_sales_per_date["date"])))

idx_ids = list(dataset["store_item"].unique())

idx = list(itertools.product(idx_dates, idx_ids))

dataset = dataset.reindex(idx)

dataset = dataset.reset_index()

dataset.head()

index_1 index_2 date store_item sales

0 2013-01-01 1_1 2013-01-01 1_1 13

1 2013-01-01 2_3 2013-01-01 2_3 19

2 2013-01-01 2_29 2013-01-01 2_29 50

3 2013-01-01 2_28 2013-01-01 2_28 45

4 2013-01-01 2_27 2013-01-01 2_27 17

dataset["date"] = dataset["date"].fillna(dataset["index_1"])

dataset["store_item"] = dataset["store_item"].fillna(dataset["index_2"])

dataset["sales"] = dataset["sales"].fillna(0)

dataset = dataset.drop(columns=["index_1", "index_2"])

dataset = dataset.set_index("date")

dataset.index.name = "date"

dataset.head()

store_item sales

date

2013-01-01 1_1 13

2013-01-01 2_3 19

2013-01-01 2_29 50

2013-01-01 2_28 45

2013-01-01 2_27 17

- Renaming the columns as follows

# The 'store_item' becomes 'unique_id' representing the unique identifier of the time series

# The 'date' becomes 'ds' representing the time stamp of the data points

# The 'sales' becomes 'y' representing the target variable we want to forecast

# Y_df = dataset.query('unique_id.str.startswith("6_46")').copy()

Y_df = dataset.copy()

Y_df = Y_df.reset_index()

Y_df = Y_df.rename(columns={

'store_item': 'unique_id',

'date': 'ds',

'sales': 'y'

})

Y_df['y'] = Y_df['y'].astype(int)

# Convert the 'ds' column to datetime format to ensure proper handling of date-related operations in subsequent steps

Y_df['ds'] = pd.to_datetime(Y_df['ds'])

Y_df['unique_id'] = Y_df['unique_id'].astype(str)

Y_df.tail()

ds unique_id y

182595 2017-12-31 1_36 71

182596 2017-12-31 1_35 55

182597 2017-12-31 1_34 32

182598 2017-12-31 1_33 61

182599 2017-12-31 1_42 27

- Running the FB Prophet TSA with 95% confidence

# Import Prophet

from prophet import Prophet

## Creating model parameters

model_param ={

"daily_seasonality": False,

"weekly_seasonality":False,

"yearly_seasonality":True,

"seasonality_mode": "multiplicative",

"growth": "logistic"

}

Y_df['cap']= Y_df["y"].max() + Y_df["y"].std() * 0.05

# Setting a cap or upper limit for the forecast as we are using logistics growth

# The cap will be maximum value of target variable plus 5% of std.

model = Prophet(**model_param)

model.fit(Y_df)

# Create future dataframe

future= model.make_future_dataframe(periods=365)

future['cap'] = Y_df['cap'].max()

forecast= model.predict(future)

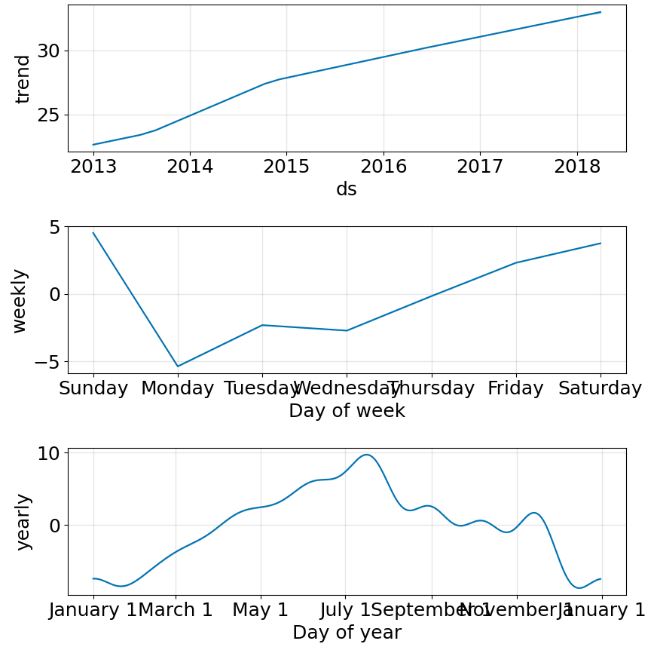

- Plotting the FB Prophet components and the forecast output

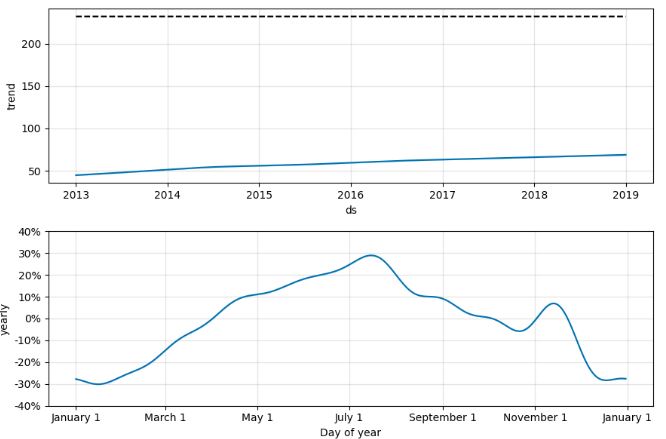

model.plot_components(forecast);

model.plot(forecast);# black dots are actual values and blue dots are forecast

- Adding extra parameters related to seasonality and events

## Adding parameters and seasonality and events

model = Prophet(**model_param)

model= model.add_seasonality(name="monthly", period=30, fourier_order=10)

model= model.add_seasonality(name="quarterly", period=92.25, fourier_order=10)

model.add_country_holidays("US")

model.fit(Y_df)

# Create future dataframe

future= model.make_future_dataframe(periods=365)

future['cap'] = Y_df['cap'].max()

forecast= model.predict(future)

- Selecting store 2 and item 28 subset of the input data

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import statsmodels.api as sm

from sklearn.metrics import mean_absolute_error, mean_absolute_percentage_error

from prophet import Prophet

import warnings

warnings.filterwarnings('ignore')

pd.set_option('display.width', None)

pd.set_option('display.max_rows', None)

df_store_2_item_28 = pd.read_csv("sales_store_2_item_28.csv")

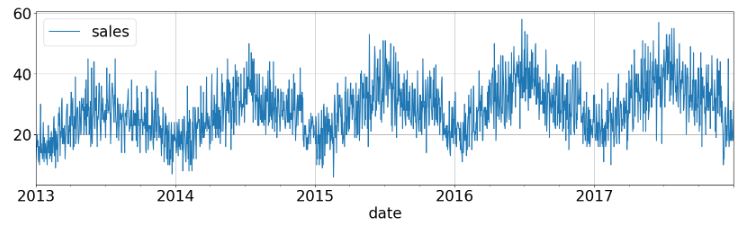

- Plotting the time-series data

import matplotlib

plt.figure(figsize=(15, 6))

matplotlib.rcParams.update({'font.size': 24})

df_store_2_item_28['date']=pd.to_datetime(df_store_2_item_28['date'])

df_store_2_item_28_time = df_store_2_item_28.set_index('date')

# Plot the entire time series data

df_store_2_item_28_time.plot(grid=True,figsize=(20,5))

plt.show()

- Plotting the monthly resampled data

df_store_2_item_28_time.resample('M').sum().plot(grid=True,figsize=(20,5))

plt.show()

- Plotting the yearly resampled data

df_store_2_item_28_time.resample('A').sum().plot(grid=True,figsize=(20,5))

plt.show()

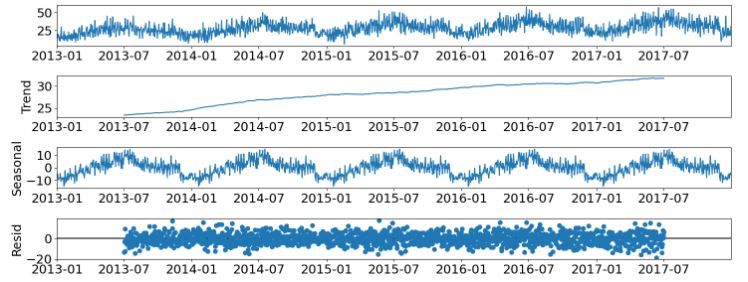

- Performing the statsmodels seasonal additive decomposition of original and resampled data

from pylab import rcParams

matplotlib.rcParams.update({'font.size': 18})

rcParams['figure.figsize'] = 15, 6

decomposition = sm.tsa.seasonal_decompose(df_store_2_item_28_time,

model = 'additive',

period=365)

fig = decomposition.plot()

plt.show()

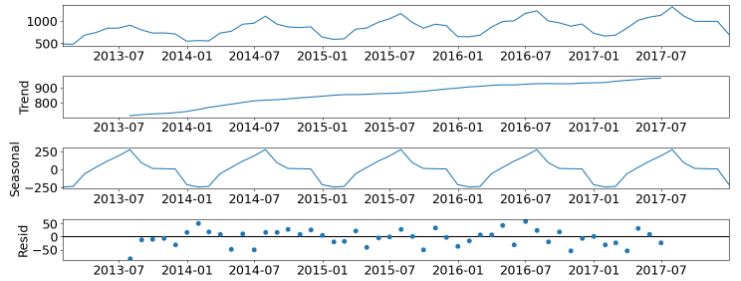

decomposition = sm.tsa.seasonal_decompose(df_store_2_item_28_time.resample('M').sum(),

model = 'additive',

period=12)

fig = decomposition.plot()

plt.show()

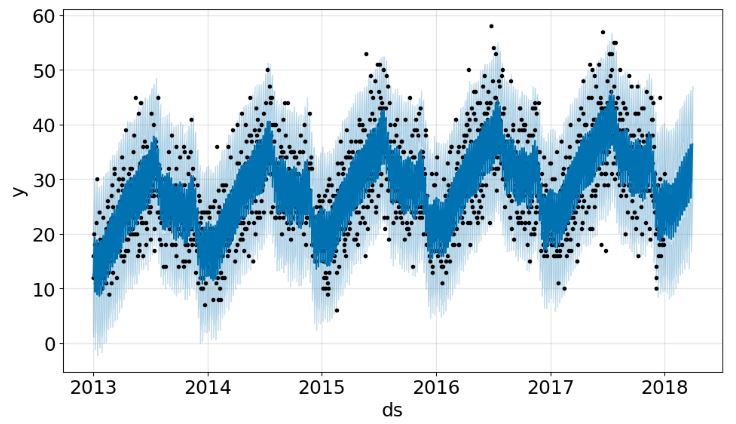

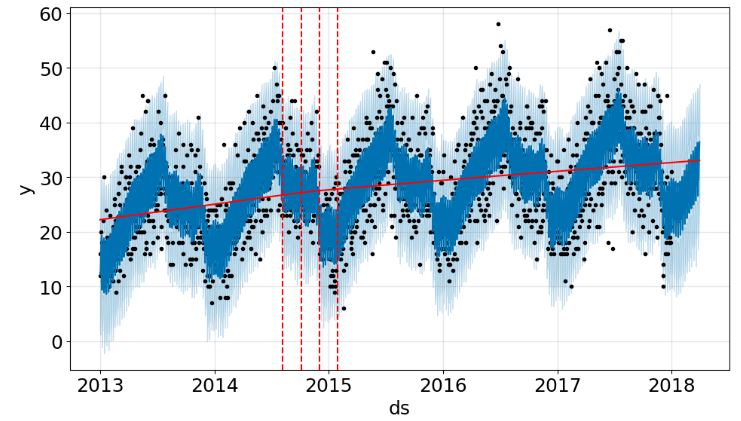

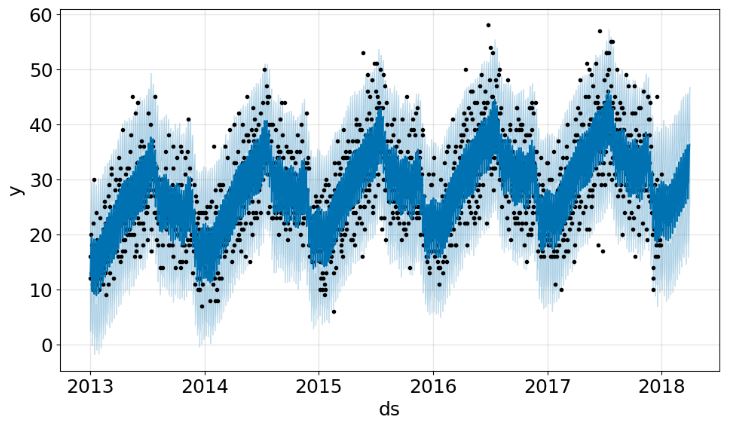

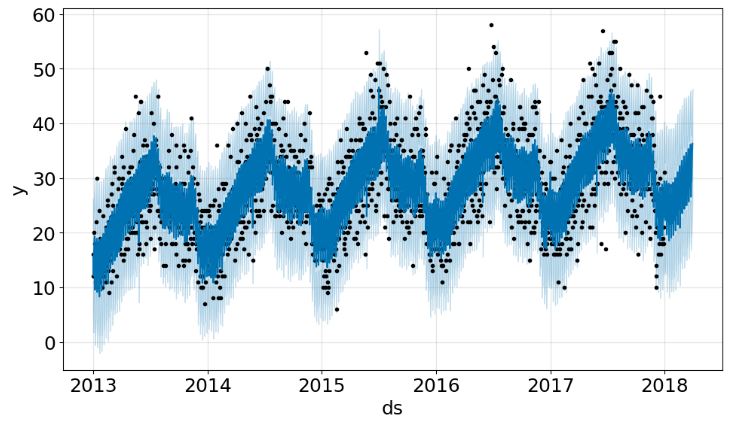

- Forecasting with FB Prophet (periods=90 and interval_width=0.95)

# rename date and sales, respectively ds and y

df_store_2_item_28.columns = ['ds','y']

m = Prophet(interval_width=0.95) #by default is 80%

model = m.fit(df_store_2_item_28)

future = m.make_future_dataframe(periods=90)

forecast = m.predict(future)

plot1 = m.plot(forecast)

- Adding change points to the above plot

from prophet.plot import add_changepoints_to_plot

plot1 = m.plot(forecast)

a = add_changepoints_to_plot(plot1.gca(),m,forecast)

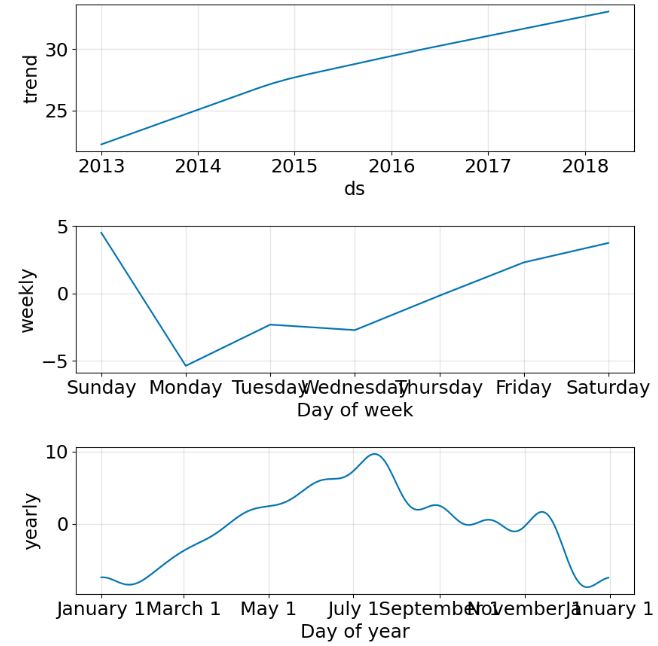

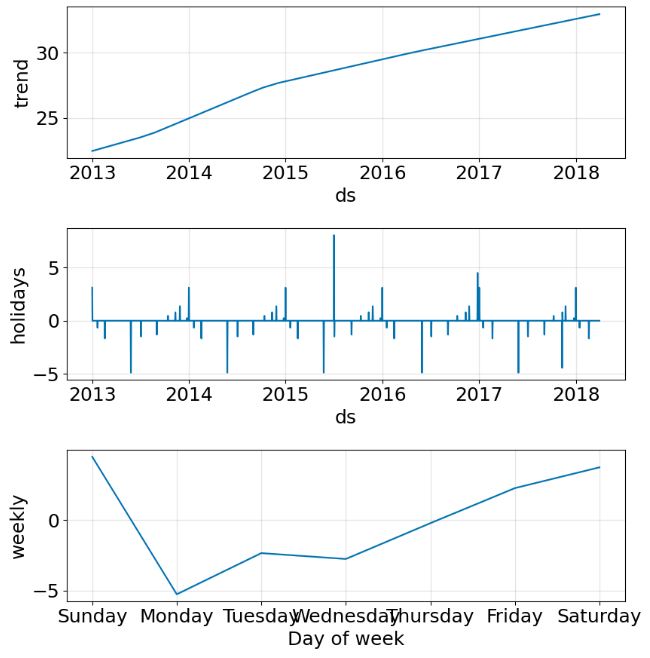

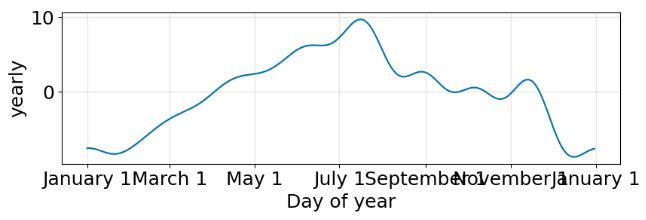

- Plotting the subset components

plot2 = m.plot_components(forecast)

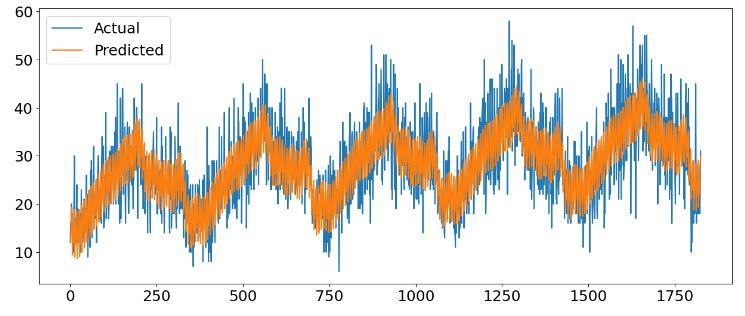

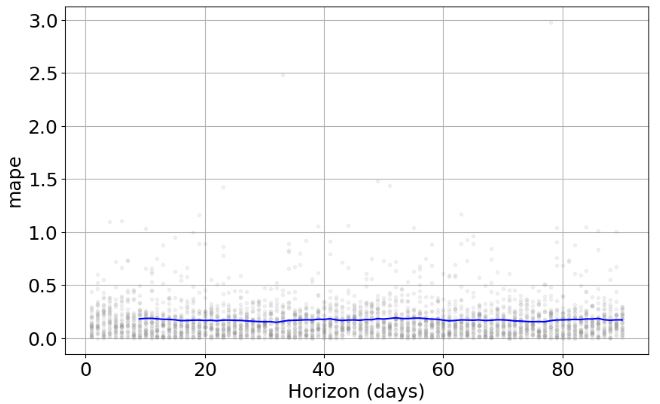

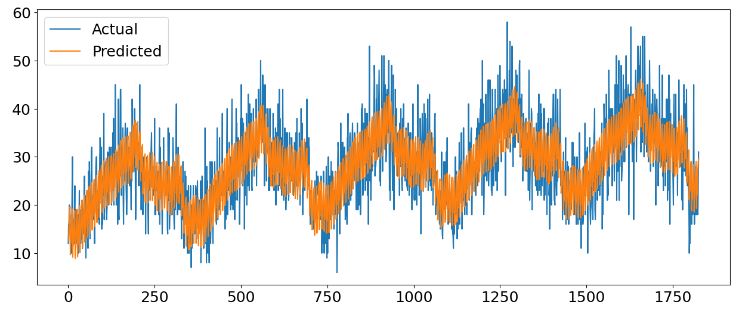

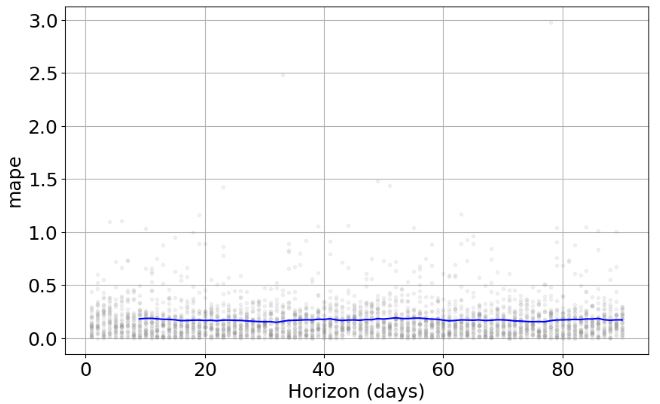

- Plotting the key FB Prophet (model 1) X-validation diagnostics – yhat, MAE, and MAPE

df_merge = pd.merge(df_store_2_item_28, forecast[['ds','yhat_lower','yhat_upper','yhat']],on='ds')

df_merge = df_merge[['ds','yhat_lower','yhat_upper','yhat','y']]

# calculate MAE between observed and predicted values

y_true = df_merge['y'].values

y_pred = df_merge['yhat'].values

mae_01 = mean_absolute_error(y_true, y_pred)

print('MAE: %.3f' % mae_01)

MAE: 4.275

# plot expected vs actual

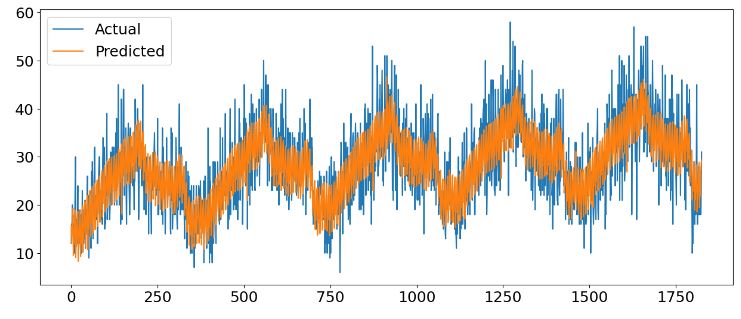

plt.plot(y_true, label='Actual')

plt.plot(y_pred, label='Predicted')

plt.legend()

plt.show()

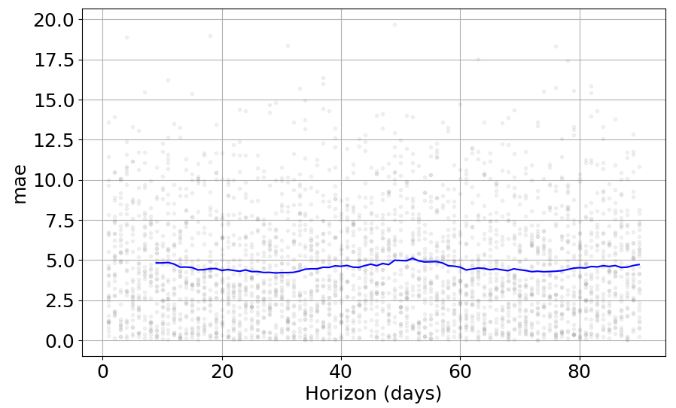

- FB Prophet X-validation

from prophet.diagnostics import cross_validation

df_cv = cross_validation(m, horizon='90 days')

INFO:prophet:Making 31 forecasts with cutoffs between 2014-01-21 00:00:00 and 2017-10-02 00:00:00

- Calculating the key performance metrics

from prophet.diagnostics import performance_metrics

df_p = performance_metrics(df_cv)

- Plotting MAE

from prophet.plot import plot_cross_validation_metric

plot3 = plot_cross_validation_metric(df_cv, metric='mae')

- Plotting MAPE

plot4 = plot_cross_validation_metric(df_cv, metric='mape')

- Storing the calculated metrics (model 1) in metrics_prophet_01

y_true = df_merge['y'].values

y_pred = df_merge['yhat'].values

mae_01 = mean_absolute_error(y_true, y_pred)

print('MAE: %.3f' % mae_01)

MAE: 4.252

mape_01 = mean_absolute_percentage_error(y_true, y_pred)

print('MAPE: %.3f' % mape_01)

MAPE: 0.168

metrics_prophet_01 = [round(mae_01,3),

round(mape_01,3)]

- Fine tuning hyperparameters by generating all combinations of parameters while minimizing MAE and MAPE

import itertools

param_grid = {

'changepoint_prior_scale': [0.001, 0.01, 0.1, 0.5],

'seasonality_prior_scale': [0.01, 0.1, 1.0, 10.0],

}

# Generate all combinations of parameters

all_params = [dict(zip(param_grid.keys(), v)) for v in itertools.product(*param_grid.values())]

maes = [] # Store the MAE for each params here

mapes = [] # Store the MAPE for each params here

# Use cross validation to evaluate all parameters

for params in all_params:

m = Prophet(**params).fit(df_store_2_item_28) # Fit model with given params

df_cv = cross_validation(m, horizon='90 days', parallel="processes")

df_p = performance_metrics(df_cv, rolling_window=1)

maes.append(df_p['mae'].values[0])

mapes.append(df_p['mape'].values[0])

# Find the best parameters

tuning_results = pd.DataFrame(all_params)

tuning_results['mae'] = maes

tuning_results['mape'] = mapes

tuning_results_df = pd.DataFrame(tuning_results)

tuning_results_df.sort_values(['mae','mape'])

- Finding the best parameters and generating TSA model 2

best_params = all_params[np.argmin(mapes)]

print(best_params)

{'changepoint_prior_scale': 0.1, 'seasonality_prior_scale': 10.0}

m = Prophet(interval_width=0.95, weekly_seasonality=True,

changepoint_prior_scale=best_params['changepoint_prior_scale'],

seasonality_prior_scale=best_params['seasonality_prior_scale'])

model = m.fit(df_store_2_item_28)

future = m.make_future_dataframe(periods=90) #to predict 90 days in the future

forecast = m.predict(future)

- Plotting the TSA forecast and key components of model 2

plot5 = m.plot(forecast)

plot6 = m.plot_components(forecast)

- Calculating the key performance metrics and storing them in metrics_prophet_02, running X-validation and plotting time-series comparisons (model 2)

df_merge = pd.merge(df_store_2_item_28, forecast[['ds','yhat_lower','yhat_upper','yhat']],on='ds')

df_merge = df_merge[['ds','yhat_lower','yhat_upper','yhat','y']]

y_true = df_merge['y'].values

y_pred = df_merge['yhat'].values

mae_02 = mean_absolute_error(y_true, y_pred)

print('MAE: %.3f' % mae_02)

MAE: 4.269

mape_02 = mean_absolute_percentage_error(y_true, y_pred)

print('MAPE: %.3f' % mape_02)

MAPE: 0.168

# plot expected vs actual

plt.plot(y_true, label='Actual')

plt.plot(y_pred, label='Predicted')

plt.legend()

plt.show()

df_cv = cross_validation(m, horizon='90 days')

df_p = performance_metrics(df_cv)

plot7 = plot_cross_validation_metric(df_cv, metric='mape')

- Adding the US holidays as events to the tuned model (model 3)

m = Prophet(interval_width=0.95, weekly_seasonality=True,

changepoint_prior_scale=best_params['changepoint_prior_scale'],

seasonality_prior_scale=best_params['seasonality_prior_scale'])

m.add_country_holidays(country_name='US')

model = m.fit(df_store_2_item_28)

# holidays included

m.train_holiday_names

0 New Year's Day

1 Martin Luther King Jr. Day

2 Washington's Birthday

3 Memorial Day

4 Independence Day

5 Labor Day

6 Columbus Day

7 Veterans Day

8 Thanksgiving

9 Christmas Day

10 Christmas Day (Observed)

11 New Year's Day (Observed)

12 Veterans Day (Observed)

13 Independence Day (Observed)

dtype: object

future = m.make_future_dataframe(periods=90)

forecast = m.predict(future)

- Plotting the TSA forecast and key components of model 3

plot5 = m.plot(forecast)

plot6 = m.plot_components(forecast)

- Calculating the key performance metrics and storing them in metrics_prophet_03, running X-validation and plotting time-series comparisons (model 3)

df_merge = pd.merge(df_store_2_item_28, forecast[['ds','yhat_lower','yhat_upper','yhat']],on='ds')

df_merge = df_merge[['ds','yhat_lower','yhat_upper','yhat','y']]

# calculate MAE between expected and predicted values

y_true = df_merge['y'].values

y_pred = df_merge['yhat'].values

mae_03 = mean_absolute_error(y_true, y_pred)

print('MAE: %.3f' % mae_03)

MAE: 4.252

mape_03 = mean_absolute_percentage_error(y_true, y_pred)

print('MAPE: %.3f' % mape_03)

MAPE: 0.168

# plot expected vs actual

plt.plot(y_true, label='Actual')

plt.plot(y_pred, label='Predicted')

plt.legend()

plt.show()

df_cv = cross_validation(m, horizon='90 days')

metrics_prophet_03 = [round(mae_03,3),

round(mape_03,3)]

- Printing the final FB Prophet TSA summary for models 1-3

pd.DataFrame({'metrics':['MAE','MAPE'],

'Prophet_01':metrics_prophet_01,

'Prophet_02':metrics_prophet_02,

'Prophet_03':metrics_prophet_03,

})

metrics Prophet_01 Prophet_02 Prophet_03

0 MAE 4.252 4.269 4.252

1 MAPE 0.168 0.168 0.168

- It is clear that neither model tuning nor adding extra events provides significantly better prediction accuracy. Which approach should we follow to minimize MAE and MAPE?

SARIMAX

- Defining the input dataset and searching for optimal SARIMAX order parameters p and q using AIC and BIC

df_store_2_item_28 = pd.read_csv("sales_store_2_item_28.csv")

# set date as index

df_store_2_item_28_time = df_store_2_item_28.set_index('date')

df_store_2_item_28_time.index = pd.DatetimeIndex(df_store_2_item_28_time.index.values)

# Create empty list to store search results

order_aic_bic=[]

# Loop over p values from 0-6

for p in range(7):

# Loop over q values from 0-6

for q in range(7):

# create and fit ARMA(p,q) model

model = SARIMAX(df_store_2_item_28_time, order=(p,1,q), freq="D") #because adf test showed that d=1

results = model.fit()

# Append order and results tuple

order_aic_bic.append((p,q,results.aic, results.bic))

# Construct DataFrame from order_aic_bic

order_df = pd.DataFrame(order_aic_bic,

columns=['p','q','AIC','BIC'])

# Print order_df in order of increasing AIC

order_df.sort_values('AIC')

p q AIC BIC

33 4 5 11671.554531 11726.647884

40 5 5 11672.383126 11732.985814

34 4 6 11683.272060 11743.874748

48 6 6 11708.930745 11780.552103

41 5 6 11719.959572 11786.071595

26 3 5 11723.712296 11773.296313

32 4 4 11725.330619 11774.914637

47 6 5 11726.087503 11792.199526

27 3 6 11729.544932 11784.638285

# Print order_df in order of increasing BIC

order_df.sort_values('BIC')

p q AIC BIC

33 4 5 11671.554531 11726.647884

40 5 5 11672.383126 11732.985814

34 4 6 11683.272060 11743.874748

18 2 4 11729.819753 11768.385100

24 3 3 11731.213716 11769.779063

26 3 5 11723.712296 11773.296313

32 4 4 11725.330619 11774.914637

25 3 4 11730.958579 11775.033261

48 6 6 11708.930745 11780.552103

20 2 6 11733.878491 11783.462508

19 2 5 11739.689796 11783.764478

27 3 6 11729.544932 11784.638285

41 5 6 11719.959572 11786.071595

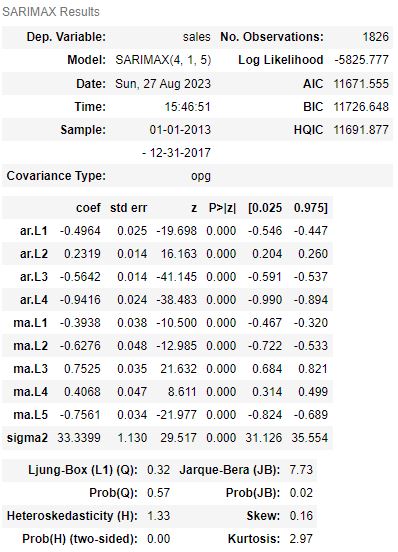

- Fitting the optimized model, calculating MAE and printing the summary diagnostics

arima_model = SARIMAX(df_store_2_item_28_time, order=(4,1,5))

# fit model

arima_results = arima_model.fit()

# Calculate the mean absolute error from residuals

mae = np.mean(np.abs(arima_results.resid))

# Print mean absolute error

print('MAE: %.3f' % mae)

MAE: 4.737

arima_results.summary()

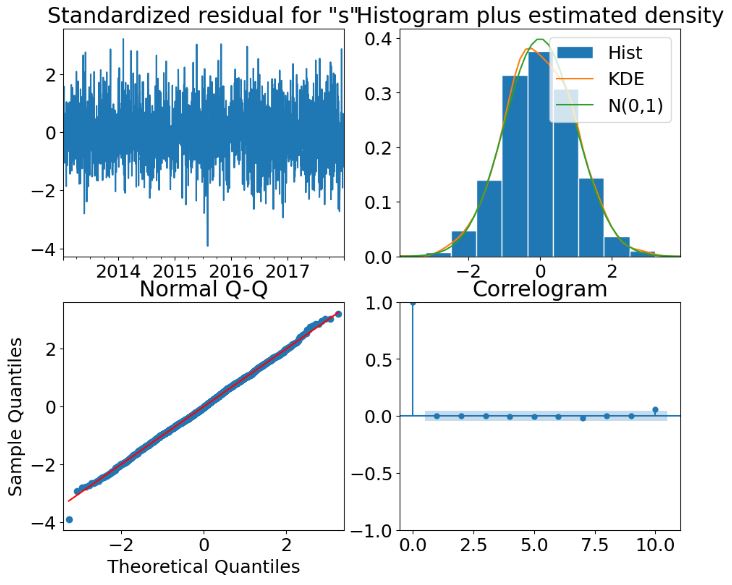

- Creating the 4 diagnostics plots using plot_diagnostics for the above model

- Computing ACF and PACF for the SARIMAX(4,1,5) model

# Create the figure

fig, (ax1, ax2) = plt.subplots(2,1,figsize=(8,6))

# Plot the ACF on ax1

plot_acf(df_store_2_item_28_time, lags=14, zero=False, ax=ax1)

# Plot the PACF on ax2

plot_pacf(df_store_2_item_28_time, lags=14, zero=False, ax=ax2)

plt.show()

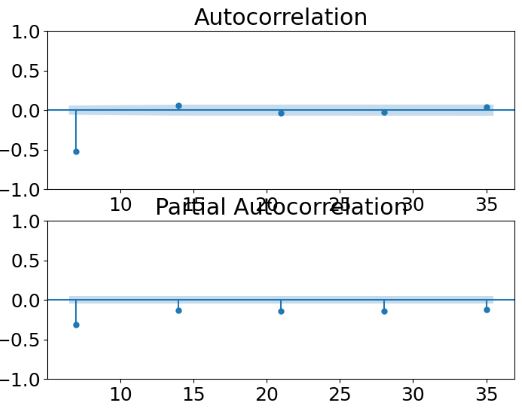

- Transformation to stationary data by taking the first and seasonal differences (S=7) and dropping Nan’s

df_store_2_item_28_time_diff = df_store_2_item_28_time.diff().diff(7).dropna()

# Make list of lags

lags = [7, 14, 21, 28, 35]

# Create the figure

fig, (ax1, ax2) = plt.subplots(2,1,figsize=(8,6))

# Plot the ACF on ax1

plot_acf(df_store_2_item_28_time_diff, lags=lags, zero=False, ax=ax1)

# Plot the PACF on ax2

plot_pacf(df_store_2_item_28_time_diff, lags=lags, zero=False, ax=ax2)

plt.show()

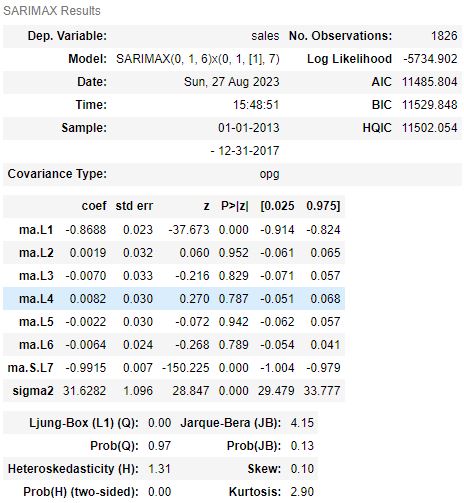

- Creating the 2nd SARIMAX model with order=(0,1,6), seasonal_order=(0,1,1,7)

sarima_01_model = SARIMAX(df_store_2_item_28_time, order=(0,1,6), seasonal_order=(0,1,1,7))

sarima_01_results = sarima_01_model.fit()

# Calculate the mean absolute error from residuals

mae = np.mean(np.abs(sarima_01_results.resid))

# Print mean absolute error

print('MAE: %.3f' % mae)

MAE: 4.555

- Printing the SARIMAX summary for the above model

sarima_01_results.summary()

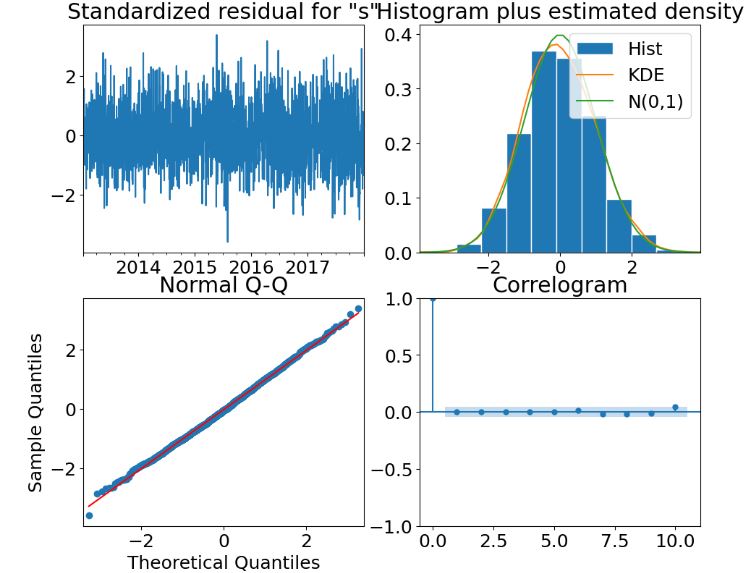

- Creating the 4 diagnostics plots using plot_diagnostics for the 2nd SARIMAX model

- Creating the Auto ARIMA model by performing stepwise search to minimize AIC

import pmdarima as pm

# Create auto_arima model

model1 = pm.auto_arima(df_store_2_item_28_time, #time series

seasonal=True, # is the time series seasonal

m=7, # the seasonal period - one week?

d=1, # non-seasonal difference order

D=1, # seasonal difference order

max_p=6, # max value of p to test

max_q=6, # max value of p to test

max_P=6, # max value of P to test

max_Q=6, # max value of Q to test

information_criterion='aic', # used to select best mode

trace=True, # prints the information_criterion for each model it fits

error_action='ignore', # ignore orders that don't work

stepwise=True, # apply an intelligent order search

suppress_warnings=True)

# Print model summary

print(model1.summary())

Performing stepwise search to minimize aic

ARIMA(2,1,2)(1,1,1)[7] : AIC=inf, Time=3.88 sec

ARIMA(0,1,0)(0,1,0)[7] : AIC=13739.527, Time=0.03 sec

ARIMA(1,1,0)(1,1,0)[7] : AIC=12650.572, Time=0.17 sec

ARIMA(0,1,1)(0,1,1)[7] : AIC=inf, Time=0.64 sec

ARIMA(1,1,0)(0,1,0)[7] : AIC=13229.902, Time=0.06 sec

ARIMA(1,1,0)(2,1,0)[7] : AIC=12480.179, Time=0.31 sec

ARIMA(1,1,0)(3,1,0)[7] : AIC=12344.238, Time=0.71 sec

ARIMA(1,1,0)(4,1,0)[7] : AIC=12270.400, Time=1.12 sec

ARIMA(1,1,0)(5,1,0)[7] : AIC=12224.430, Time=1.57 sec

ARIMA(1,1,0)(6,1,0)[7] : AIC=12196.670, Time=2.79 sec

ARIMA(1,1,0)(6,1,1)[7] : AIC=inf, Time=22.80 sec

ARIMA(1,1,0)(5,1,1)[7] : AIC=inf, Time=16.60 sec

ARIMA(0,1,0)(6,1,0)[7] : AIC=12702.277, Time=2.00 sec

ARIMA(2,1,0)(6,1,0)[7] : AIC=11998.566, Time=2.86 sec

ARIMA(2,1,0)(5,1,0)[7] : AIC=12027.447, Time=2.37 sec

ARIMA(2,1,0)(6,1,1)[7] : AIC=inf, Time=24.39 sec

ARIMA(2,1,0)(5,1,1)[7] : AIC=inf, Time=18.97 sec

ARIMA(3,1,0)(6,1,0)[7] : AIC=11888.959, Time=4.14 sec

ARIMA(3,1,0)(5,1,0)[7] : AIC=11915.280, Time=2.62 sec

ARIMA(3,1,0)(6,1,1)[7] : AIC=inf, Time=32.36 sec

ARIMA(3,1,0)(5,1,1)[7] : AIC=inf, Time=21.27 sec

ARIMA(4,1,0)(6,1,0)[7] : AIC=11829.853, Time=3.99 sec

ARIMA(4,1,0)(5,1,0)[7] : AIC=11855.759, Time=3.71 sec

ARIMA(4,1,0)(6,1,1)[7] : AIC=inf, Time=36.03 sec

ARIMA(4,1,0)(5,1,1)[7] : AIC=inf, Time=21.41 sec

ARIMA(5,1,0)(6,1,0)[7] : AIC=11787.764, Time=4.93 sec

ARIMA(5,1,0)(5,1,0)[7] : AIC=11813.941, Time=2.94 sec

ARIMA(5,1,0)(6,1,1)[7] : AIC=inf, Time=46.20 sec

ARIMA(5,1,0)(5,1,1)[7] : AIC=inf, Time=25.65 sec

ARIMA(6,1,0)(6,1,0)[7] : AIC=11723.670, Time=6.75 sec

ARIMA(6,1,0)(5,1,0)[7] : AIC=11754.653, Time=4.73 sec

ARIMA(6,1,0)(6,1,1)[7] : AIC=inf, Time=52.06 sec

ARIMA(6,1,0)(5,1,1)[7] : AIC=inf, Time=33.75 sec

ARIMA(6,1,1)(6,1,0)[7] : AIC=11680.726, Time=15.66 sec

ARIMA(6,1,1)(5,1,0)[7] : AIC=11700.932, Time=10.98 sec

ARIMA(6,1,1)(6,1,1)[7] : AIC=inf, Time=69.93 sec

ARIMA(6,1,1)(5,1,1)[7] : AIC=inf, Time=40.65 sec

ARIMA(5,1,1)(6,1,0)[7] : AIC=11681.051, Time=11.06 sec

ARIMA(6,1,2)(6,1,0)[7] : AIC=11681.423, Time=10.89 sec

ARIMA(5,1,2)(6,1,0)[7] : AIC=11683.639, Time=21.40 sec

ARIMA(6,1,1)(6,1,0)[7] intercept : AIC=11682.576, Time=79.21 sec

Best model: ARIMA(6,1,1)(6,1,0)[7]

Total fit time: 663.675 seconds

SARIMAX Results

==========================================================================================

Dep. Variable: y No. Observations: 1826

Model: SARIMAX(6, 1, 1)x(6, 1, [], 7) Log Likelihood -5826.363

Date: Sun, 27 Aug 2023 AIC 11680.726

Time: 16:00:26 BIC 11757.803

Sample: 01-01-2013 HQIC 11709.164

- 12-31-2017

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.0671 0.026 2.595 0.009 0.016 0.118

ar.L2 0.0575 0.027 2.118 0.034 0.004 0.111

ar.L3 0.0467 0.026 1.800 0.072 -0.004 0.098

ar.L4 0.0486 0.026 1.905 0.057 -0.001 0.099

ar.L5 0.0363 0.026 1.390 0.164 -0.015 0.087

ar.L6 0.0410 0.025 1.613 0.107 -0.009 0.091

ma.L1 -0.9464 0.014 -69.687 0.000 -0.973 -0.920

ar.S.L7 -0.8558 0.024 -36.375 0.000 -0.902 -0.810

ar.S.L14 -0.6815 0.032 -21.632 0.000 -0.743 -0.620

ar.S.L21 -0.5757 0.035 -16.429 0.000 -0.644 -0.507

ar.S.L28 -0.4127 0.033 -12.481 0.000 -0.478 -0.348

ar.S.L35 -0.2411 0.031 -7.798 0.000 -0.302 -0.181

ar.S.L42 -0.1133 0.024 -4.677 0.000 -0.161 -0.066

sigma2 35.3666 1.202 29.416 0.000 33.010 37.723

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 0.04

Prob(Q): 1.00 Prob(JB): 0.98

Heteroskedasticity (H): 1.31 Skew: 0.01

Prob(H) (two-sided): 0.00 Kurtosis: 3.00

===================================================================================

- Creating the mean forecast

# Create ARIMA mean forecast

arima_pred = arima_results.get_prediction(start=-90, dynamic=True)

arima_mean = arima_pred.predicted_mean

# Create SARIMA mean forecast

sarima_01_pred = sarima_01_results.get_prediction(start=-90, dynamic=True)

sarima_01_mean = sarima_01_pred.predicted_mean

# Create SARIMA mean forecast

sarima_02_pred = sarima_02_results.get_prediction(start=-90, dynamic=True)

sarima_02_mean = sarima_02_pred.predicted_mean

- Calculating the MAE and MAPE metrics and printing the summary

from sklearn.metrics import mean_absolute_error, mean_absolute_percentage_error

metrics_arima = [round(mean_absolute_error(df_store_2_item_28_time[-90:],arima_mean),3),

round(mean_absolute_percentage_error(df_store_2_item_28_time[-90:],arima_mean),3)]

metrics_sarima_01 = [round(mean_absolute_error(df_store_2_item_28_time[-90:],sarima_01_mean),3),

round(mean_absolute_percentage_error(df_store_2_item_28_time[-90:],sarima_01_mean),3)]

metrics_sarima_02 = [round(mean_absolute_error(df_store_2_item_28_time[-90:],sarima_02_mean),3),

round(mean_absolute_percentage_error(df_store_2_item_28_time[-90:],sarima_02_mean),3)]

df_arima_results = pd.DataFrame({'metrics':['MAE','MAPE'],

'ARIMA(4,1,5)':metrics_arima,

'SARIMA(0,1,6)(0,1,1)7':metrics_sarima_01,

'SARIMA(6,1,1)(6,1,0)7':metrics_sarima_02,

})

df_arima_results

metrics ARIMA(4,1,5) SARIMA(0,1,6)(0,1,1)7 SARIMA(6,1,1)(6,1,0)7

0 MAE 6.855 6.910 6.285

1 MAPE 0.294 0.301 0.213

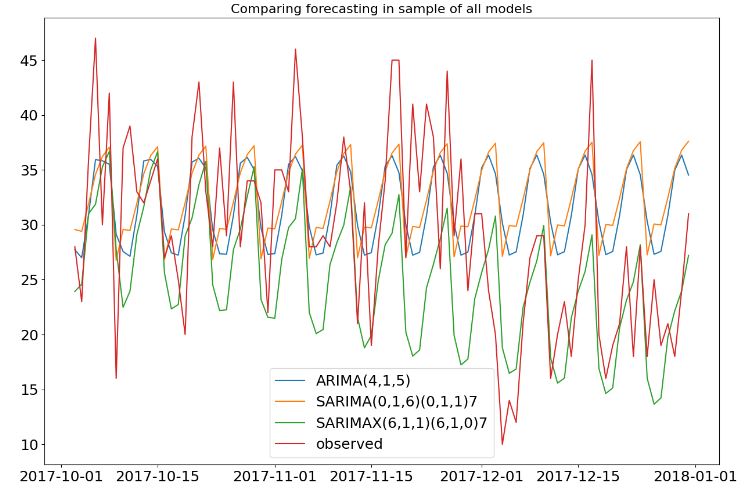

- Comparing forecasting in sample of all models

dates = df_store_2_item_28_time.index

# Plot mean ARIMA and SARIMA predictions and observed

plt.figure(figsize=(15,10))

plt.title('Comparing forecasting in sample of all models', size = 16)

plt.plot(arima_mean.index, arima_mean, label='ARIMA(4,1,5)')

plt.plot(sarima_01_mean.index, sarima_01_mean, label='SARIMA(0,1,6)(0,1,1)7')

plt.plot(sarima_02_mean.index, sarima_02_mean, label='SARIMAX(6,1,1)(6,1,0)7')

plt.plot(df_store_2_item_28_time[-90:], label='observed')

plt.legend()

plt.show()

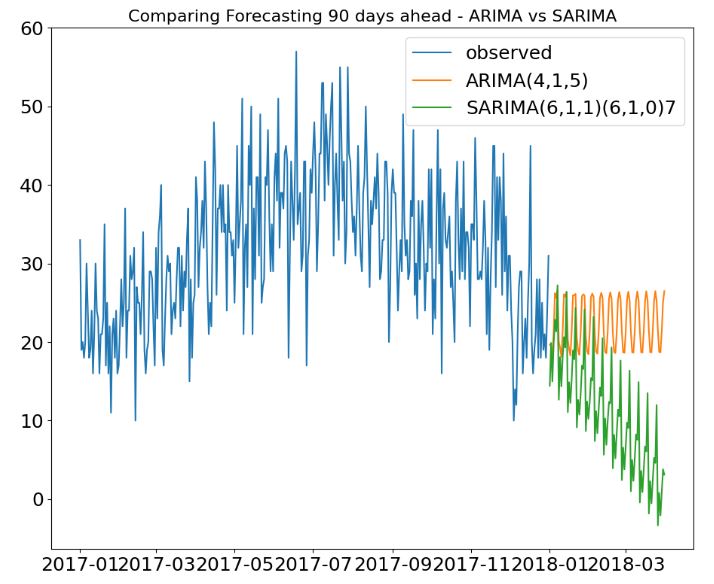

- Comparing Forecasting 90 days ahead – ARIMA vs SARIMA

#Forecast Out of Sample

# Create ARIMA mean forecast

arima_pred = arima_results.get_forecast(steps=90)

arima_mean = arima_pred.predicted_mean

# Create SARIMA mean forecast

sarima_02_pred = sarima_02_results.get_forecast(steps=90)

sarima_02_mean = sarima_02_pred.predicted_mean

dates = df_store_2_item_28_time.index

# Plot mean ARIMA and SARIMA predictions and observed

plt.title("Comparing Forecasting 90 days ahead - ARIMA vs SARIMA", size =16)

plt.plot(df_store_2_item_28_time['2017':], label='observed')

plt.plot(arima_mean.index, arima_mean, label='ARIMA(4,1,5)')

plt.plot(sarima_02_mean.index, sarima_02_mean, label='SARIMA(6,1,1)(6,1,0)7')

plt.legend()

plt.show()

Summary

- We compared 3 optimized FB Prophet models to forecast sales at the store level with high seasonality effects. The final model Prophet_03 yields MAE=4.252 and MAPE=0.168.

- Referring to these models, our observations support the following 2 aspects of previous case studies: (1) a native handling of trend and seasonality features, that makes FB Prophet a good baseline model if the time series follows sales cycles; (2) if your signal is noisy, fine-tuning the model’s performance can be a hassle.

- We also considered various autoregressive (AR) models. Specifically, SARIMAX models are among the most widely used AR models for forecasting, with good forecasting performance. In the SARIMAX model notation, the parameters p , d , and q represent the autoregressive, differencing, and moving-average components, respectively.

- We studied possible combinations of AR models for different values of (p , d , q). As a result of hyperparameter optimization, we calculated MAE and MAPE for the following 3 AR models: AR1=ARIMA(4,1,5), AR2=SARIMA(0,1,6)(0,1,1)7, and AR3=SARIMA(6,1,1)(6,1,0)7. AR3 is the the final AR model with MAE=6.285 and MAPE=0.213.

- If we look at the residual time-series plot, there is no trend or seasonal pattern, so it can be assumed that the residuals are normally distributed. This is also supported by the model residual histogram, which is bell-shaped, meaning the residuals are normally distributed.

- Event though SARIMA models allow for differencing data by seasonal frequency, FB Prophet provides an interpretable model with the best (short-time) performance.

- This data can also be applied to more complex forecasting models or by combining other forecasting methods to increase the accuracy of forecasting results.

- Business impact: if there is a significant decline in sales, then we can identify promotional strategies that have least impact on sales and further boost profitable promotional strategies.

Explore More

- Leveraging Predictive Uncertainties of Time Series Forecasting Models

- Evaluation of ML Sales Forecasting: tslearn, Random Walk, Holt-Winters, SARIMAX, GARCH, Prophet, and LSTM

- A Balanced Mix-and-Match Time Series Forecasting: ThymeBoost, Prophet, and AutoARIMA

- Low-Code AutoEDA of Dutch eHealth Data in Python

- A Comparison of Automated EDA Tools in Python: Pandas-Profiling vs SweetViz

- Time Series Forecasting of Hourly U.S.A. Energy Consumption – PJM East Electricity Grid

- SARIMAX Cross-Validation of EIA Crude Oil Prices Forecast in 2023 – 2. Brent

- SARIMAX-TSA Forecasting, QC and Visualization of Online Food Delivery Sales

- BTC-USD Freefall vs FB/Meta Prophet 2022-23 Predictions

- Stock Forecasting with FBProphet

- Brazilian E-Commerce Showcase

- Unsupervised ML Clustering, Customer Segmentation, Cohort, Market Basket, Bank Churn, CRM, ABC & RFM Analysis – A Comprehensive Guide in Python

References

- Time Series Part 3: Forecasting with Facebook Prophet: An Intro

- Time Series Part 2: Forecasting with SARIMAX models: An Intro

- Prophet vs SARIMA — Time Series Forecasting

- MKB-DataLab

- Time Series Model (SARIMAX Vs LSTM Vs fbprophet)

- An End-to-End Project on Time Series Analysis and Forecasting with Python

- ARIMA for Time-Series Forecasting: Retail Sales Predictions

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment