Photo by Carl Heyerdahl on Unsplash

- Referring to the recent review of best stock screeners, let’s focus on the Datapane stock screener API.

- This API is built around the concept of Blocks, which are Python objects that represent an individual unit that can be processed, composed, and viewed.

Let’s install Datapane

!pip install datapane_components

and import standard libraries

import datapane as dp

import altair as alt

import pandas as pd

import plotly.express as px

import yfinance as yf

from datetime import datetime

import threading

from time import sleep

Let’s set the stock ticker

ticker=’MSFT’

and download the stock Adj Close price in USD

df = pd.DataFrame(yf.download(ticker, period=”1d”, interval=”5m”)[“Adj Close”]).reset_index()

df.columns = [“time”, “adjusted_close”]

[*********************100%***********************] 1 of 1 completed

df.tail()

“””

Stock Portfolio Analysis

A Datapane app that analyses stock portfolio data.

“””

from datetime import date, timedelta

import pandas as pd

import numpy as np

import plotly.figure_factory as ff

import plotly.graph_objs as go

import plotly.express as px

import plotly.io as pio

import datapane as dp

import datapane_components as dc

import yfinance as yf

pio.templates.default = “ggplot2”

dp.enable_logging()

def process(ticker1: str, ticker2: str = “GOOG”) -> dp.View:

print(f”Downloading datasets for {ticker1} vs {ticker2}”)

start = date.today() – timedelta(365)

end = date.today() + timedelta(2)

# get the data

df1 = yf.download(ticker1, start=start, end=end, interval=”1d”).reset_index() # [“Adj Close”]).reset_index()

df2 = yf.download(ticker2, start=start, end=end, interval=”1d”).reset_index() # [“Adj Close”]).reset_index()

df1[“Date”] = pd.to_datetime(df1[“Date”], format=”%d/%m/%Y”)

df2[“Date”] = pd.to_datetime(df2[“Date”], format=”%d/%m/%Y”)

orig_df1 = df1.copy(deep=True)

# Build all the visualizations

print("Creating plots...")

trace0 = go.Scatter(x=df1.Date, y=df1.Close, name=ticker1)

fig0 = go.Figure([trace0])

fig0.update_layout(title={"text": f"{ticker1} Stock Price", "x": 0.5, "xanchor": "center"})

df1["10-day MA"] = df1["Close"].rolling(window=10).mean()

df1["20-day MA"] = df1["Close"].rolling(window=20).mean()

df1["50-day MA"] = df1["Close"].rolling(window=50).mean()

trace0 = go.Scatter(x=df1.Date, y=df1.Close, name=ticker1)

trace1 = go.Scatter(x=df1.Date, y=df1["10-day MA"], name="10-day MA")

trace2 = go.Scatter(x=df1.Date, y=df1["20-day MA"], name="20-day MA")

fig1 = go.Figure([trace0, trace1, trace2])

fig1.update_layout(title={"text": f"{ticker1} Stock Price (Rolling Average)", "x": 0.5, "xanchor": "center"})

fig2 = go.Figure(go.Candlestick(x=df1.Date, open=df1.Open, high=df1.High, low=df1.Low, close=df1.Close))

fig2.update_layout(title={"text": f"{ticker1} Stock Price (Candle Stick)", "x": 0.5, "xanchor": "center"})

df1["Daily return (%)"] = round(df1["Close"].pct_change() * 100, 2)

fig3 = px.bar(df1, x="Date", y="Daily return (%)")

fig3.update_layout(title={"text": f"{ticker1} Stock Daily Return", "x": 0.5, "xanchor": "center"})

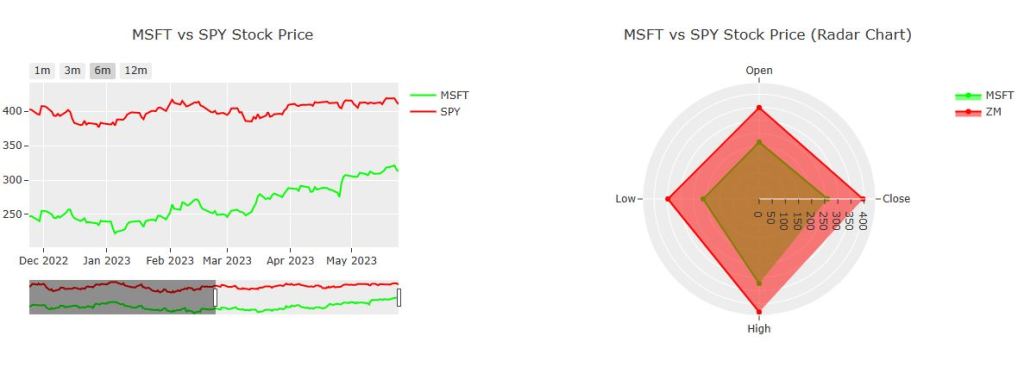

trace0 = go.Scatter(x=df1.Date, y=df1.Close, name=ticker1, line=dict(color="lime"))

trace1 = go.Scatter(x=df2.Date, y=df2.Close, name=ticker2, line=dict(color="red"))

fig4 = go.Figure([trace0, trace1])

fig4.update_layout(

dict(

title=dict({"text": f"{ticker1} vs {ticker2} Stock Price", "x": 0.5, "xanchor": "center"}),

xaxis=dict(

rangeselector=dict(

buttons=list(

[

dict(count=1, label="1m", step="month", stepmode="backward"),

dict(count=3, label="3m", step="month", stepmode="backward"),

dict(count=6, label="6m", step="month", stepmode="backward"),

dict(count=12, label="12m", step="month", stepmode="backward"),

]

)

),

rangeslider=dict(visible=True),

type="date",

),

)

)

trace0 = go.Scatterpolar(

r=[df1["Close"].mean(), df1["Open"].min(), df1["Low"].min(), df1["High"].max()],

theta=["Close", "Open", "Low", "High"],

line=dict(color="lime"),

name=ticker1,

fill="toself",

)

trace1 = go.Scatterpolar(

r=[df2["Close"].mean(), df2["Open"].min(), df2["Low"].min(), df2["High"].max()],

theta=["Close", "Open", "Low", "High"],

line=dict(color="red"),

name="ZM",

fill="toself",

)

fig5 = go.Figure([trace0, trace1])

fig5.update_layout(

go.Layout(

polar=dict(radialaxis=dict(visible=True)),

title=dict({"text": f"{ticker1} vs {ticker2} Stock Price (Radar Chart)", "x": 0.5, "xanchor": "center"}),

)

)

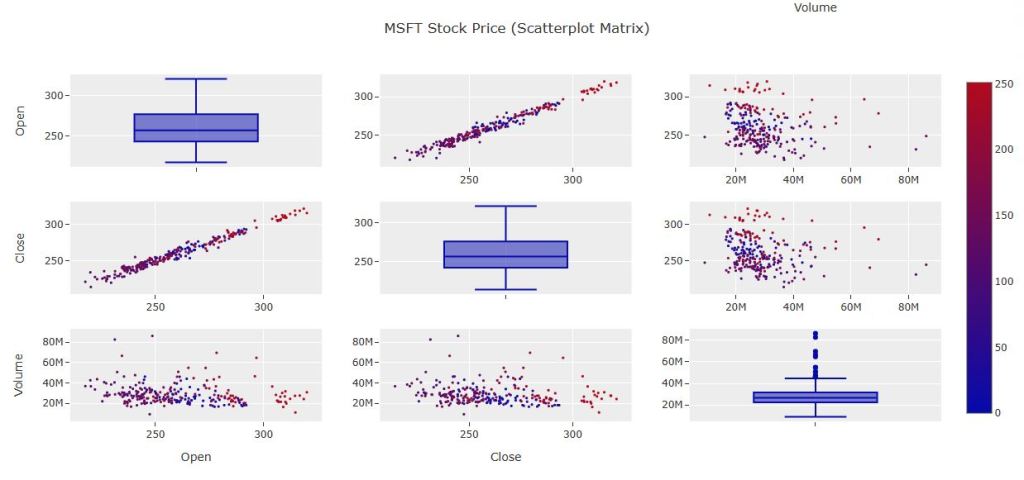

df1 = df1[["Open", "Close", "Volume"]]

df1["index"] = np.arange(len(df1))

fig7 = go.Figure(

ff.create_scatterplotmatrix(

df1,

diag="box",

index="index",

size=3,

height=600,

width=1150,

colormap="RdBu",

title={"text": f"{ticker1} Stock Price (Scatterplot Matrix)", "x": 0.5, "xanchor": "center"},

)

)

# Building the output Datapane View

# Now that we have a series of plots, we can construct our custom View.

# In addition to the visualizations, this View includes Datapane's `BigNumber` component to

# display today's stock prices, and our `DataTable` component to allow our viewers to filter,

# explore, and download the data themselves.

# We can build a more powerful report by using Datapane's layout components.

# e.g. using `Group` to place the `BigNumber` blocks in two columns, and `Select` block to add multiple tabs.

ticker1_today = df1.iloc[-1]

ticker2_today = df2.iloc[-1]

return dp.View(

dp.Group(

f"""## {ticker1} analysis (against {ticker2})""",

dp.Group(

dp.BigNumber(

heading=f"{ticker1} Day Performance",

value="${:,.2f}".format(ticker1_today.Close),

prev_value="${:,.2f}".format(ticker1_today.Open),

),

dp.BigNumber(

heading=f"{ticker2} Day Performance",

value="${:,.2f}".format(ticker2_today.Close),

prev_value="${:,.2f}".format(ticker2_today.Open),

),

columns=2,

),

dp.Group(fig0, fig1, fig2, fig3, fig4, fig5, columns=2),

dp.Plot(fig7),

# datasets

*dc.section(

"""

# Datasets

_These datasets are pulled live_.

"""

),

dp.Select(dp.DataTable(orig_df1, label=ticker1), dp.DataTable(df2, label=ticker2)),

label=f"{ticker1} vs {ticker2}",

),

)

controls = dp.Controls(

ticker1=dp.TextBox(label=”Ticker”, initial=”MSFT”),

ticker2=dp.TextBox(label=”(Optional) Comparison Ticker”, initial=”GOOG”, allow_empty=True),

)

v = dp.View(

dp.Compute(

function=process, controls=controls, label=”Choose Ticker”, cache=True, target=”results”, swap=dp.Swap.APPEND

),

dp.Select(name=”results”),

)

dp.serve_app(v)

Summary

This is A Quick Guide for Value Investors Who Can Use Datapane to Build Their Own Value Investing Stock Screener API in 10 Minutes.

Explore More

An Interactive GPT Index and DeepLake Interface – 1. Amazon Financial Statements

Working with FRED API in Python: U.S. Recession Forecast & Beyond

Advanced Integrated Data Visualization (AIDV) in Python – 1. Stock Technical Indicators

The Donchian Channel vs Buy-and-Hold Breakout Trading Systems – $MO Use-Case

A Comparative Analysis of The 3 Best U.S. Growth Stocks in Q1’23 – 1. WMT

Python Technical Analysis for BioTech – Get Buy Alerts on ABBV in 2023

Basic Stock Price Analysis in Python

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment