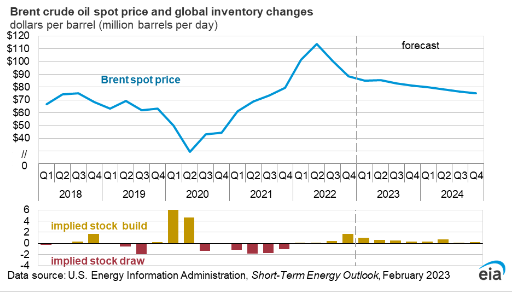

Based on our previous study, our today’s focus is on SARIMAX time-series X-validation of the Brent crude oil spot price USD: viz. the goal is to verify the following EIA energy forecast in 2023

According to EIA, the Brent spot price will average $83.63/b in 2023.

Table of Contents

- Prerequisites

- Libraries

- Input Data

- ETS Decomposition

- ADF Test

- SARIMAX

- Predictions

- Residuals

- Summary

- Explore More

- Embed Socials

Prerequisites

In this study we will be installing Anaconda, managing relevant Python-3 packages, creating individual conda environments and sharing them via conda YAML file. One can install multiple packages at the same time.

Libraries

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and import/install the following libraries

!pip install statsmodels !pip install yfinance

import yfinance as yf

import numpy as np

import pandas as pd

from matplotlib import pyplot as plt

from statsmodels.tsa.stattools import adfuller

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.arima_model import ARIMA

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

from pmdarima import auto_arima

import warnings

warnings.filterwarnings(“ignore”)

!pip install pmdarima

Additional libraries can be imported on the “if-needed” basis.

Input Data

let’s load the input data

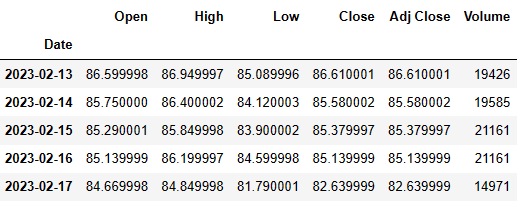

df = yf.download(‘BZ=F’, ‘2022-02-03’)

[*********************100%***********************] 1 of 1 completed

Let’s explore the data structure

df.shape

(264, 6)

df.info()

<class 'pandas.core.frame.DataFrame'> DatetimeIndex: 264 entries, 2022-02-03 to 2023-02-17 Data columns (total 6 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Open 264 non-null float64 1 High 264 non-null float64 2 Low 264 non-null float64 3 Close 264 non-null float64 4 Adj Close 264 non-null float64 5 Volume 264 non-null int64 dtypes: float64(5), int64(1) memory usage: 14.4 KB

df.describe()

df.tail()

Let’s drop the following columns

df=df.drop([‘Open’, ‘High’, ‘Low’, ‘Close’,’Volume’], axis=1)

to get the single-column table with the time index

df.tail()

Let’s check the null values

df.isnull().sum()

df.isnull().sum()

Adj Close 0 dtype: int64

ETS Decomposition

Let’s perform the seasonal decomposition of our data with model=’multiplicative’ and period=30 (i.e. 1 month)

result = seasonal_decompose(df, model=’multiplicative’,period=30)

result.plot()

ADF Test

Let’s perform the Augmented Dickey-Fuller (ADF) test

adfuller(df[‘Adj Close’])

(-0.8702493547662872,

0.7976118156481764,

10,

253,

{'1%': -3.4564641849494113,

'5%': -2.873032730098417,

'10%': -2.572894516864816},

1257.2890699767)

Here’s how to interpret the most important values in the output:

- Test statistic: -0.870249

- P-value: 0.79761

Since the p-value is not less than .05, we fail to reject the null hypothesis.

This means the time series is non-stationary in that it has some time-dependent structure and does not have constant variance over time.

SARIMAX

Let’s fit auto_arima function to our input dataset

stepwise_fit = auto_arima(df[‘Adj Close’], start_p = 1, start_q = 1,

max_p = 3, max_q = 3, m = 12,

start_P = 0, seasonal = True,

d = None, D = 1, trace = True,

error_action =’ignore’,

suppress_warnings = True,

stepwise = True)

stepwise_fit.summary()

Performing stepwise search to minimize aic ARIMA(1,0,1)(0,1,1)[12] intercept : AIC=inf, Time=1.00 sec ARIMA(0,0,0)(0,1,0)[12] intercept : AIC=1755.936, Time=0.02 sec ARIMA(1,0,0)(1,1,0)[12] intercept : AIC=1388.994, Time=0.28 sec ARIMA(0,0,1)(0,1,1)[12] intercept : AIC=1574.287, Time=0.28 sec ARIMA(0,0,0)(0,1,0)[12] : AIC=1754.679, Time=0.03 sec ARIMA(1,0,0)(0,1,0)[12] intercept : AIC=1438.019, Time=0.05 sec ARIMA(1,0,0)(2,1,0)[12] intercept : AIC=1357.220, Time=1.05 sec ARIMA(1,0,0)(2,1,1)[12] intercept : AIC=inf, Time=3.20 sec ARIMA(1,0,0)(1,1,1)[12] intercept : AIC=inf, Time=0.87 sec ARIMA(0,0,0)(2,1,0)[12] intercept : AIC=1738.787, Time=0.72 sec ARIMA(2,0,0)(2,1,0)[12] intercept : AIC=1358.635, Time=1.18 sec ARIMA(1,0,1)(2,1,0)[12] intercept : AIC=1358.655, Time=1.28 sec ARIMA(0,0,1)(2,1,0)[12] intercept : AIC=1570.019, Time=0.87 sec ARIMA(2,0,1)(2,1,0)[12] intercept : AIC=1360.622, Time=2.68 sec ARIMA(1,0,0)(2,1,0)[12] : AIC=1355.364, Time=0.30 sec ARIMA(1,0,0)(1,1,0)[12] : AIC=1387.045, Time=0.09 sec ARIMA(1,0,0)(2,1,1)[12] : AIC=inf, Time=1.39 sec ARIMA(1,0,0)(1,1,1)[12] : AIC=inf, Time=0.78 sec ARIMA(0,0,0)(2,1,0)[12] : AIC=1740.760, Time=0.18 sec ARIMA(2,0,0)(2,1,0)[12] : AIC=1356.815, Time=0.38 sec ARIMA(1,0,1)(2,1,0)[12] : AIC=1356.832, Time=0.36 sec ARIMA(0,0,1)(2,1,0)[12] : AIC=1572.157, Time=0.30 sec ARIMA(2,0,1)(2,1,0)[12] : AIC=1358.807, Time=0.81 sec Best model: ARIMA(1,0,0)(2,1,0)[12] Total fit time: 18.091 seconds

SARIMAX Results:

| Dep. Variable: | y | No. Observations: | 264 |

|---|---|---|---|

| Model: | SARIMAX(1, 0, 0)x(2, 1, 0, 12) | Log Likelihood | -673.682 |

| Date: | Fri, 17 Feb 2023 | AIC | 1355.364 |

| Time: | 10:36:45 | BIC | 1369.482 |

| Sample: | 0 | HQIC | 1361.045 |

| – 264 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ar.L1 | 0.9165 | 0.019 | 47.894 | 0.000 | 0.879 | 0.954 |

| ar.S.L12 | -0.6100 | 0.049 | -12.357 | 0.000 | -0.707 | -0.513 |

| ar.S.L24 | -0.4017 | 0.052 | -7.708 | 0.000 | -0.504 | -0.300 |

| sigma2 | 11.9008 | 0.874 | 13.617 | 0.000 | 10.188 | 13.614 |

| Ljung-Box (L1) (Q): | 0.61 | Jarque-Bera (JB): | 14.30 |

|---|---|---|---|

| Prob(Q): | 0.44 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 0.24 | Skew: | -0.01 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 4.17 |

let’s split the data into train / test sets

train = df.iloc[:len(df)-12]

test = df.iloc[len(df)-12:] # set one year(12 months) for testing

and fit the SARIMAX(1, 0, 0)x(2, 1, 0, 12) model to the training set

from statsmodels.tsa.statespace.sarimax import SARIMAX

model = SARIMAX(train[‘Adj Close’],

order = (0, 1, 0),

seasonal_order =(2, 1, 0, 12))

result = model.fit()

result.summary()

SARIMAX Results:

| Dep. Variable: | Adj Close | No. Observations: | 252 |

|---|---|---|---|

| Model: | SARIMAX(0, 1, 0)x(2, 1, 0, 12) | Log Likelihood | -647.761 |

| Date: | Fri, 17 Feb 2023 | AIC | 1301.521 |

| Time: | 10:37:05 | BIC | 1311.951 |

| Sample: | 0 | HQIC | 1305.724 |

| – 252 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ar.S.L12 | -0.6397 | 0.047 | -13.476 | 0.000 | -0.733 | -0.547 |

| ar.S.L24 | -0.4151 | 0.048 | -8.736 | 0.000 | -0.508 | -0.322 |

| sigma2 | 12.8359 | 0.969 | 13.246 | 0.000 | 10.937 | 14.735 |

| Ljung-Box (L1) (Q): | 0.01 | Jarque-Bera (JB): | 19.35 |

|---|---|---|---|

| Prob(Q): | 0.92 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 0.25 | Skew: | -0.40 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 4.14 |

- Goodness of fit test, The Jarque-Bera test is a goodness-of-fit test that measures if sample data has skewness and kurtosis that are similar to a normal distribution. The JB test statistic is always positive, and if it is not close to zero, it shows that the sample data do not have a normal distribution.

- Negative skew refers to a longer or fatter tail on the left side of the distribution.

- Positive excess values of kurtosis (>3) indicate that a distribution is peaked and possess thick tails. Leptokurtic distributions have positive kurtosis values.

- A leptokurtic distribution has a higher peak (thin bell) and taller (i.e. fatter and heavy) tails than a normal distribution.

Predictions

Let’s print our test data and 1Y predictions

print(test[‘Adj Close’],predictions)

Date 2023-02-02 82.169998 2023-02-03 79.940002 2023-02-06 80.989998 2023-02-07 83.690002 2023-02-08 85.089996 2023-02-09 84.500000 2023-02-10 86.389999 2023-02-13 86.610001 2023-02-14 85.580002 2023-02-15 85.379997 2023-02-16 85.139999 2023-02-17 83.680000 Name: Adj Close, dtype: float64 252 84.005361 253 85.602957 254 86.011120 255 84.965660 256 84.457512 257 84.003784 258 84.321574 259 85.826474 260 85.605278 261 86.496948 262 86.800109 263 85.527856 Name: Predictions, dtype: float64

Let’s plot test data vs predictions

x=test[‘Adj Close’]

y=predictions

plt.plot(x,y, ‘o’, color=’green’)

get m (slope) and b(intercept) of a linear regression line

m, b = np.polyfit(x, y, 1)

use red as a color for the linear regression line

plt.plot(x, m*x+b, color=’red’)

plt.xlabel(‘Adj Close Test’)

plt.ylabel(‘Predictions’)

Train the model on the full dataset

model = model = SARIMAX(df[‘Adj Close’],

order = (0, 1, 1),

seasonal_order =(2, 1, 1, 12))

result = model.fit()

Forecast for 1Y

forecast = result.predict(start = len(df),

end = (len(df)-1) + 1 * 12,

typ = ‘levels’).rename(‘Forecast’)

Plot the forecast values vs train data

df[‘Adj Close’].plot(figsize = (2, 5), legend = True)

forecast.plot(legend = True)

Let’s plot the forecast

print(forecast)

264 82.930292 265 82.569673 266 82.759312 267 81.629149 268 82.420565 269 82.121951 270 82.551539 271 82.931898 272 82.737850 273 82.810189 274 83.249728 275 83.419509 Name: Forecast, dtype: float64

a = np.array([‘Jan’, ‘Feb’, ‘Mar’,’Apr’,’May’,’Jun’,’Jul’,’Aug’,’Sept’,’Oct’,’Nov’,’Dec’])

plt.plot(a,forecast)

plt.xlabel(“Month 2023”);

plt.ylabel(“Predicted Brent Oil Price $”);

Overall, this plot supports the EIA energy forecast in 2023 within the confidence intervals defined below.

Residuals

Let’s evaluate our predictions by using the following sklearn error metrics

from sklearn.metrics import mean_squared_error

from statsmodels.tools.eval_measures import rmse

rmse(test[“Adj Close”], predictions)

2.5038953839620026

mean_squared_error(test[“Adj Close”], predictions)

6.2694920938262255

Summary

- The ADF test show that our time series dataset is non-stationary. In other words, it has some time-dependent structure and does not have constant variance over time.

- The seasonal decomposition of our dataset reveals the distinct trend curve and the prominent seasonal effect.

- Our train/test dataset does not have a normal distribution – negative skew refers to a longer or fatter tail on the left side of the distribution; positive excess value of kurtosis (>3) indicates that our distribution is peaked and possess thick tails (Leptokurtic distribution).

- Our predictions ca. $83.4 (Dec 2023) are generally consistent with the EIA energy forecast in 2023 (ca. $83.63/b).

- Remaining discrepancies are well within the predicted confidence intervals +/- $6.

Explore More

SARIMAX X-Validation of EIA Crude Oil Prices Forecast in 2023 – 1. WTI

OXY Stock Analysis, Thursday, 23 June 2022

Energy E&P: XOM Technical Analysis Nov ’22

Embed Socials

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment