Tag: optimization

-

Uber’s Orbit Full Bayesian Time Series Forecasting & Inference

This article introduces Orbit, an open-source Python framework by Uber for full Bayesian time series forecasting and inference. It supports models like Exponential Smoothing, Local Global Trend, and Kernel Time-based Regression, along with methods like Markov-Chain Monte Carlo and Variational Inference. Orbit captures uncertainty in time-series data, allowing credible probabilistic forecasts with confidence intervals. The…

-

100 Basic Python Codes

Source: PYPL Popularity of Programming Language, Feb 2024. Table of Contents Setting Up Your Environment Download Datasets Initial Pandas Data QC Displaying Pandas Data Types Showing Descriptive Statistics Exploring the Dataset Email Slicer User Input & Type Conversion Working with Lists Practicing Loops Calculator Temperature Conversion ADC Temperature Sensor Sorting Numpy Arrays Story Generator Display…

-

A Market-Neutral Strategy

The work aims to solve the problem of Markowitz portfolio optimization for a one-year investment horizon through the pairs trading cointegrated strategy. Market-neutral trading strategies seek to generate returns independent of market swings to achieve a zero beta against its relevant market index. Statistical arbitrage (SA), pairs trading, and APO signals are analyzed. The study…

-

Health Insurance Cross Sell Prediction with ML Model Tuning & Validation

The content discusses the use of AI and Machine Learning (ML) for insurance cross-selling. It covers topics such as data preparation, model training with different algorithms, parameter optimization, and model evaluation. The study showcases the ability of ML models (HGBM, XGBoost, Random Forest) to predict cross-sell customers in the insurance sector, providing potential for improved…

-

A Balanced Mix-and-Match Time Series Forecasting: ThymeBoost, Prophet, and AutoARIMA

The post evaluates the performance of popular Time Series Forecasting (TSF) methods, namely AutoARIMA, Facebook Prophet, and ThymeBoost on four real-world time series datasets: Air Passengers, U.S. Wholesale Price Index (WPI), BTC-USD price, and Peyton Manning. Each TSF model uses historical data to identify trends and make future predictions. Studies indicate that ThymeBoost, which combines…

-

Dividend-NG-BTC Diversify Big Tech

SEO Title: Can Dividends, Natural Gas and Crypto Diversify Big Techs? Ultimately, we need to answer the following fundamental question: Can Dividend Kings, NGUSD and BTC-USD Diversify Growth Tech assets? Dividends are very popular among investors, especially those who want a steady stream of income from their investments. Some companies choose to share their profits…

-

Oracle Monte Carlo Stock Simulations

Oracle Corporation’s significant developments in Generative AI have led to lucrative partnerships with Nvidia and Elon Musk’s xAI. Having secured contracts exceeding $4 billion for its Generation 2 Cloud designed for AI model training, Oracle’s earnings doubled in Q4 2023. Monte Carlo simulations align with Zacks Rank 3-Hold for ORCL, implying bullish potential with projected…

-

Machine Learning-Based Crop Yield Prediction, Classification, and Recommendations

We have implemented a Machine Learning-Based decision support tool for crop yield prediction, including supporting decisions on what crops to grow and what to do during the growing season of the crops.

-

Multiple-Criteria Technical Analysis of Blue Chips in Python

Blue chip stocks are the stocks of well-known, high-quality companies. We demonstrate that the proposed approach can help optimize the blue-chip portfolios comprehensively.

-

WA House Price Prediction: EDA-ML-HPO

A predictive model of house sale prices in King County, Washington, was developed using multiple supervised machine learning (ML) regression models, including LinearRegression, SGDRegressor, RandomForestRegressor, XGBRegressor, and AdaBoostRegressor. The best-performing model, XGBRegressor, explained 90.6% of the price variance, with a RMSE of $18472.7. These results, valuable to local realtors, indicate houses with a waterfront are…

-

ML Prediction of High/Low Video Game Hits with Data Resampling and Model Tuning

The post outlines a ML-based approach to forecast video game sales, using several techniques to enhance training, accuracy, and prediction. The Kaggle’s VGChartz dataset, containing sales data and other game-specific information, was used to build and refine the model. Several ML techniques including RandomForestClassifier and Logistic Regression yielded top predictors, with the critic’s score deemed…

-

Risk-Aware Strategies for DCA Investors

Dollar-Cost Averaging (DCA) is an investment approach that involves investing a fixed amount regularly, regardless of market price. It offers benefits such as risk reduction and market downturn resilience. It’s useful for beginners and can be combined with other strategies for a disciplined investment approach. References include Investopedia and Yahoo Finance.

-

Joint Analysis of Bitcoin, Gold and Crude Oil Prices

The content discusses a comprehensive analysis on a joint time-series analysis of Bitcoin, Gold and Crude Oil prices from 2021 to 2023. It explores data processing, exploratory data analysis before running a range of statistical tests, ARIMA models fitting, and finally, using the Markowitz portfolio optimization method. It then presents a detailed analysis, including data…

-

Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

The post discusses applying Guillen’s algorithm for risk-aware portfolio rebalancing, using Python. It incorporates five different stocks with specific weight allocations within an initial portfolio of $1,000,000. The post demonstrates setting the parameters for portfolio, importing required libraries, downloading input data, setting algorithmic rules for rebalancing, calculation of shares and portfolio values, and plotting visualizations.…

-

Post-SVB Risk Aware Investing

The recent collapse of Silicon Valley Bank and its repercussions have prompted a reevaluation of risk-aware investing in the US financial sector. The crisis has exposed the vulnerability of banks invested in long-term fixed income assets, highlighting the importance of diversification and risk management. Market indicators suggest continued volatility and uncertainty, urging investors to exercise…

-

Portfolio Optimization of 20 Dividend Growth Stocks

The post discusses implementing a stochastic optimization algorithm to create a balanced portfolio of 20 dividend growth stocks for maximum return within defined risk tolerance. By analyzing daily stock and benchmark data, the algorithm optimizes the portfolio to outperform the benchmark index and achieve desired risk-reward outcomes. The results facilitate spreading investment capital across diverse…

-

Towards Max(ROI/Risk) Trading

This post compares 1-year ROI/Risk of selected stocks vs ETF using stock analyzer functions. It includes comparing prices, visualizing annual risk and return, and examining correlation matrix of stock returns. It provides insights for selecting CPB stock for trading based on low correlation with ^GSPC, high return (~20%), and low risk (~23%).

-

Risk/Return POA – Dr. Dividend’s Positions

Based upon the Portfolio Optimization Algorithm (POA) discussed earlier and the relevant POA QC analysis and comparisons, let’s look at the current stock positions suggested by Dr. Dividend (DD). Let’s define the following POA parameters: benchmark_ = [“^GSPC”,]portfolio_ = [‘AAPL’, ‘GOOG’, ‘COST’, ‘SBUX’, ‘DE’,’SOFI’,’APD’,’UNH’,’SHW’,’NVDA’] start_date_ = “2021-01-01”end_date_ = “2022-10-05”number_of_scenarios = 10000 trade_days_per_year = 252 delta_risk…

-

HealthTech ML/AI Q3 ’22 Round-Up

Featured Photo by Andy Kelly on Unsplash This blog presents a Q3 ’22 summary of current healthtech ML/AI innovation methods, trends and challenges. Virtual reality, artificial intelligence, augmented reality, and machine learning are all healthcare technology trends that are going to play a vital role across the entire healthcare system. Let’s take a look at…

-

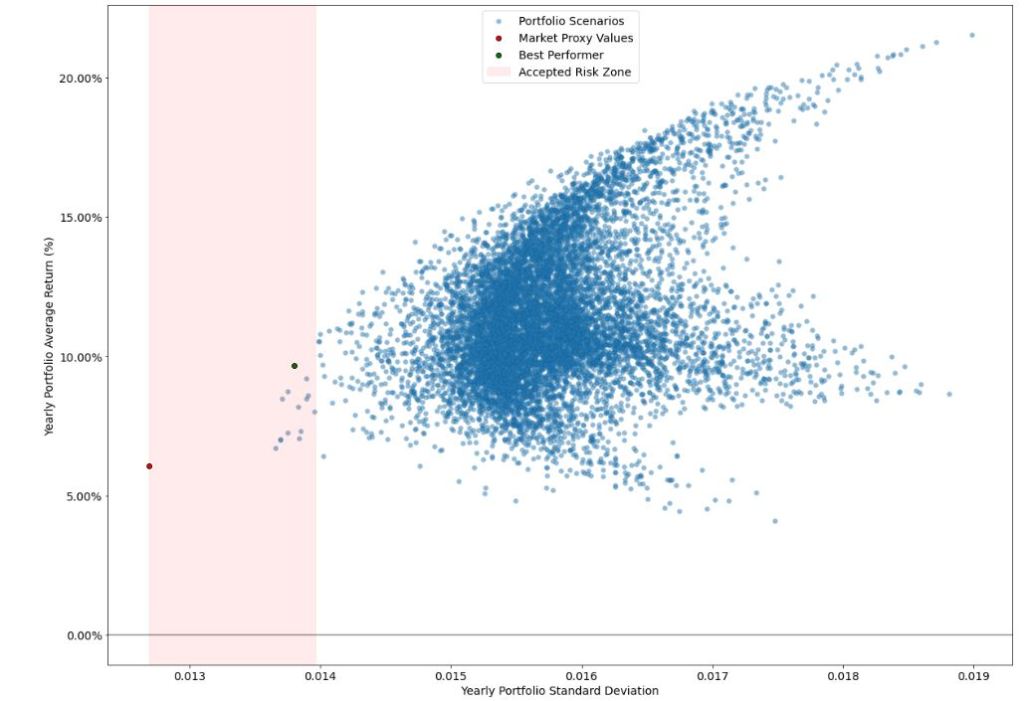

Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

The Portfolio Optimization Algorithm (POA) is used for comparing the top five stock positions of Humble Div (HD) and Dividend Glenn (DG) from 2017 to 2022. The Risk/Return Ratio (RRR) shows HD portfolio as a better performer than DG portfolio and the market. Both portfolios and market are within risk boundaries.