In this post, we will compare 1Y ROI/Risk of selected stocks vs ETF using a set of basic stock analyzer functions. The posts consists of the following three parts:

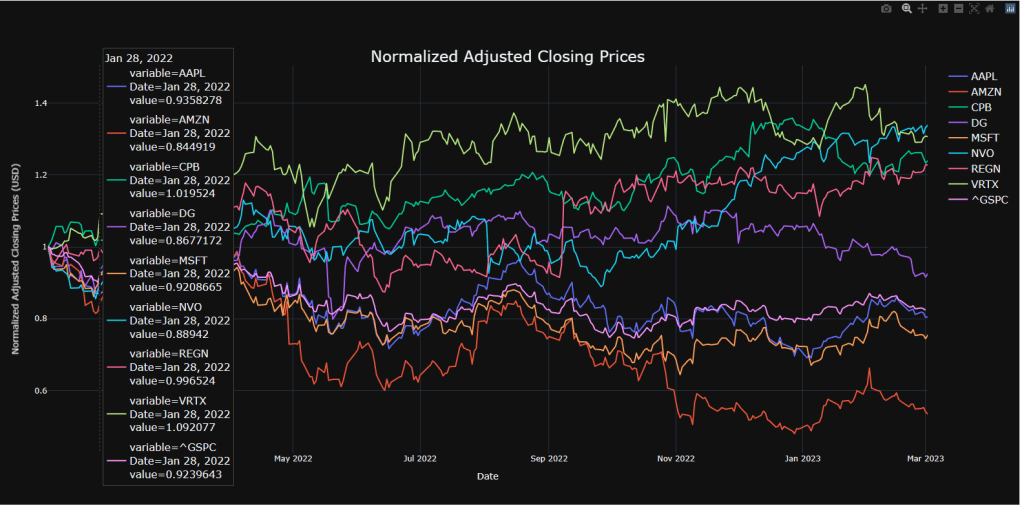

- Comparing normalized prices of selected stocks

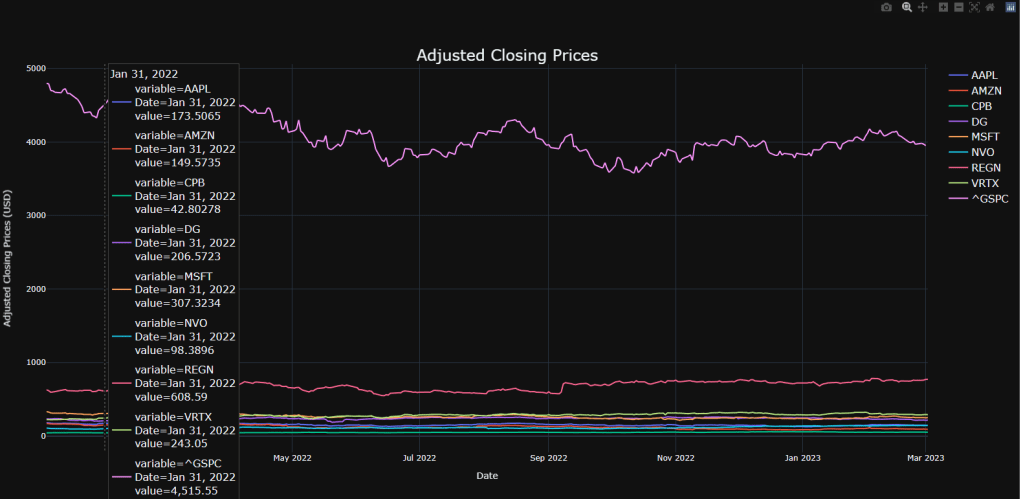

Looking at the closing price of a stock over time is a good way to track its performance

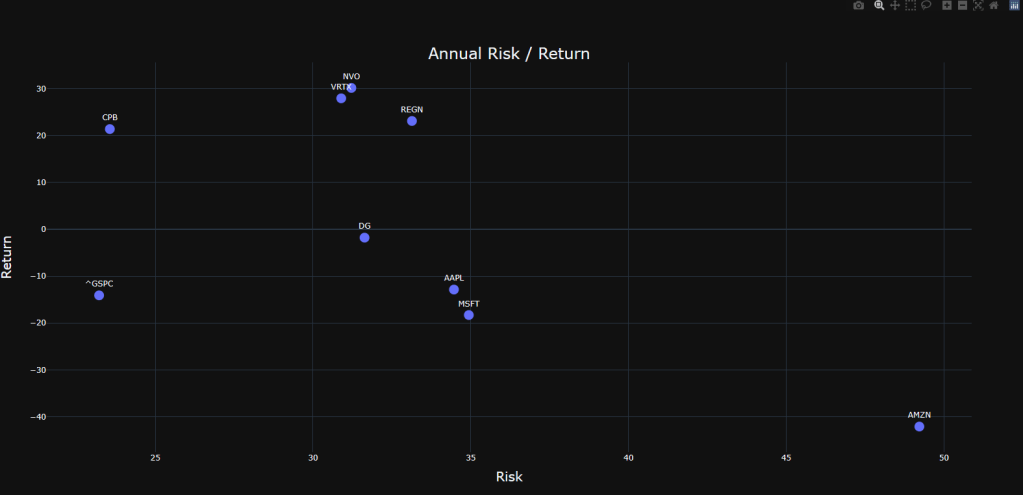

- Visualizing and comparing annual risk and return

We combine the risk and return metrics into a single plot; we define return as the percent change in 1Y closing price and risk will be the corresponding standard deviation (STDV) of daily returns over the period of time.

- Examining correlation matrix of stock returns

We look at the correlation matrix that would give us useful insights into how certain stocks will react under similar market conditions.

Requirements

import os

os.chdir(‘YOURPATH’)

os. getcwd()

import pandas as pd

import plotly.offline as offline

from plotly.offline import download_plotlyjs, init_notebook_mode, plot, iplot

import plotly.express as px

import plotly.graph_objs as go

offline.init_notebook_mode(connected=True)

pd.set_option(‘display.max_rows’, 10)

Input Data

import yfinance as yf

import plotly.express as px

import plotly.io as pio

import numpy as np

import plotly.graph_objects as go

pio.renderers.default = “browser”

tickers=[‘AMZN’,’AAPL’,’MSFT’,’CPB’,’DG’,’^GSPC’,’NVO’,’REGN’,’VRTX’]

start_date=”2022-01-01″

mydf=yf.download(tickers,start=start_date)

[*********************100%***********************] 9 of 9 completed

Price

def close_plot(df, adj = True, normalize = False):

if adj:

close = df.loc[:,"Adj Close"].copy()

title = "Adjusted Closing Prices"

else:

close = df.loc[:,"Close"].copy()

title = "Closing Prices"

if normalize:

normclose = close.div(close.iloc[0]) #Normalizes data

fig = px.line(normclose,

x = normclose.index,

y = normclose.columns,

title = "Normalized " + title,

template = 'plotly_dark') # Plotting Normalized closing data

fig.update_layout(

legend = dict(title = None, font = dict(size = 16)),

title={

'y':0.9,

'x':0.5,

'font': {'size': 24},

'xanchor': 'center',

'yanchor': 'top'},

hovermode = "x unified",

xaxis_title = "Date",

yaxis_title = "Normalized " + title + " (USD)"

)

fig.show()

else:

fig = px.line(close,

x = close.index,

y = close.columns,

title = title,

template = 'plotly_dark') # Plotting Normalized closing data

fig.update_layout(

legend = dict(title = None, font = dict(size = 16)),

title={

'y':0.9,

'x':0.5,

'font': {'size': 24},

'xanchor': 'center',

'yanchor': 'top'},

hovermode = "x unified",

xaxis_title = "Date",

yaxis_title = title + " (USD)"

)

fig.show()

close_plot(mydf, adj = True, normalize = False)

close_plot(mydf, adj = True, normalize = True)

Return

def returns_plot(df, adj = True):

if adj:

close = df.loc[:,"Adj Close"].copy()

else:

close = df.loc[:,"Close"].copy()

ret = close.pct_change().dropna()

cum_ret = ((1 + ret).cumprod() -1) * 100

fig = px.line(cum_ret, template = 'plotly_dark')

fig.update_layout(

legend = dict(title = None, font = dict(size = 16)),

title={

'y':0.95,

'x':0.5,

'text': "Daily Cumulative Returns",

'font': {'size': 24},

'xanchor': 'center',

'yanchor': 'top'},

hovermode = "x unified",

xaxis_title = "Date",

yaxis_title = "% Returns")

fig.show()

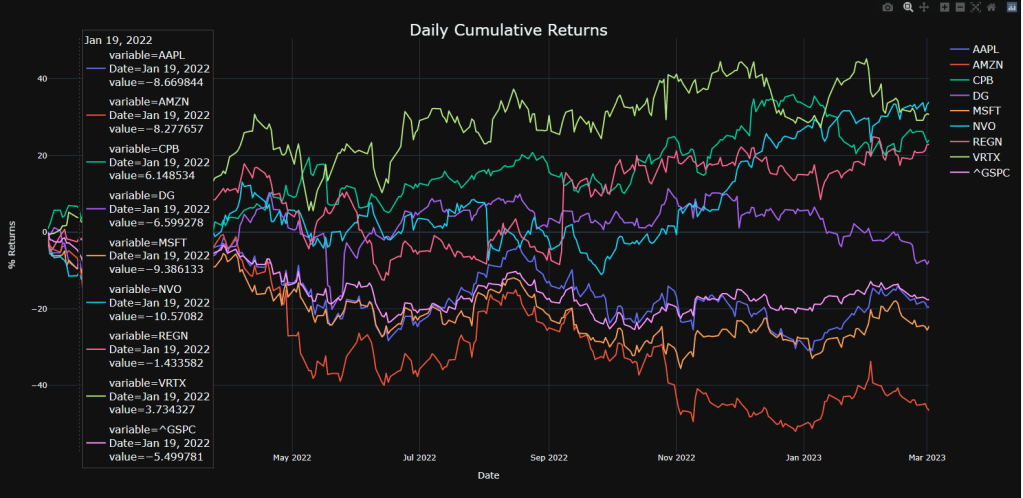

returns_plot(mydf, adj = True)

ROI/Risk

def risk_return(df, adj = True, crypto = False):

if adj:

close = df.loc[:,"Adj Close"].copy()

else:

close = df.loc[:,"Close"].copy()

if crypto:

trading_days = 365

else:

trading_days = 252

ret = close.pct_change().dropna().mul(100) #Returns of each stock in terms of percent change

summary = ret.describe().T.loc[:,["mean","std"]]

summary["mean"] = summary["mean"]*trading_days # Multiply by number of trading days

summary["std"] = summary["std"]*np.sqrt(trading_days) # Multiply by number of trading dayss

summary.rename(columns = {'mean':'Return', 'std':'Risk'}, inplace = True)

fig = px.scatter(summary,

x = 'Risk',

y = 'Return',

title = "Annual Risk / Return",

text = summary.index,

template = 'plotly_dark')

fig.update_traces(marker={'size': 15},

textposition='top center',

hoverlabel=dict(font=dict(size=20) ))

fig.update_layout(

legend = dict(title = None),

title={

'y':0.9,

'x':0.5,

'font': {'size': 24},

'xanchor': 'center',

'yanchor': 'top',},

xaxis = dict(title = dict(font = dict(size = 20))),

yaxis = dict(title = dict(font = dict(size = 20)))

)

fig.show()

risk_return(mydf, adj = True, crypto = False)

Correlations

def ret_corr(df, adj = True, crypto = False):

if adj:

close = df.loc[:,"Adj Close"].copy()

else:

close = df.loc[:,"Close"].copy()

if crypto:

trading_days = 365

else:

trading_days = 252

ret = close.pct_change().dropna().mul(100) #Returns of each stock in terms of percent change

summary = ret.describe().T.loc[:,["mean","std"]]

summary["mean"] = summary["mean"]*trading_days # Multiply by number of trading days

summary["std"] = summary["std"]*np.sqrt(trading_days) # Multiply by number of trading days

summary.rename(columns = {'mean':'Return', 'std':'Risk'}, inplace = True)

fig = px.imshow(ret.corr(), text_auto=True, color_continuous_scale='tempo', template = 'plotly_dark', title = "Returns Correlation")

fig.update_layout(

legend = dict(title = None),

title={

'y':0.9,

'x':0.5,

'xanchor': 'center',

'yanchor': 'top'}

)

fig.show()

ret_corr(mydf, adj = True, crypto = False)

Summary

Based on the above plots, we select the CPB stock for trading because of:

- Low correlation between CPB and ^GSPC

- High return(CPB) ~20% compared to loss(^GSPC) ~ 13%

- Low risk(CPB) ~ 23% comparable to low risk(^GSPC).

Explore More

Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

A TradeSanta’s Quick Guide to Best Swing Trading Indicators

Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

Stock Portfolio Risk/Return Optimization

Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

Risk/Return POA – Dr. Dividend’s Positions

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment