Canva Template by SocialAdvisor

- This blog post is a deep dive into Time Series Forecasting (TSF) using SARIMAX and Supervised Machine Learning (ML) algorithms.

- The objective is to explain nuts & bolts of these powerful TSF techniques while evaluating and comparing their performance.

- Referring to the earlier studies [1], [2] & [3], we will predict Walmart weekly store sales using the Kaggle dataset.

- With more than 245 million customers visiting 10,900 stores and with 10 active websites across the globe, Walmart is definitely a name to reckon with in the retail sector.

- According to the data, Walmart’s net sales were forecast to be around 547 billion U.S. dollars in 2021, following the upsurge in 2020 that was driven by COVID-19. From 2021 onwards, Walmart’s net sales were forecast to increase with each consecutive year. By 2026, it was forecast that Walmart’s net sales would grow to 675.2 billion U.S. dollars, which includes store-based and e-commerce net sales.

- Our aim is to understand how different factors affect the Walmart sales by creating more efficient strategies of increasing revenues.

- Walmart Recruiting: We are provided with historical sales data for 45 Walmart stores located in different regions. Each store contains a number of departments, and we are tasked with predicting the department-wide sales for each store.

- In addition, Walmart runs several promotional markdown events throughout the year. These markdowns precede prominent holidays, the four largest of which are the Super Bowl, Labor Day, Thanksgiving, and Christmas. The weeks including these holidays are weighted five times higher in the evaluation than non-holiday weeks.

- TSF is a great strategy for predicting future sales using historical data. In an auto regressive (AR) model the model predicts the next data point by looking at previous data points and using a linear regression. ARIMA stands for auto regressive integrated moving average. SARIMAX is similar and stands for seasonal auto regressive integrated moving average with exogenous factors.

- In fact, the crucial point of this study is to combine SARIMAX and supervised ML into a single framework to optimized the advantages of each.

- Specifically, how ML helps in sales forecasting? SARIMAX methods require time-consuming manual work and data engineering, which can be difficult and expensive. ML, on the other hand, is able to automatically learn from data and make predictions without any human intervention.

- Here are some advantages you can anticipate if you introduce ML into your sales forecasting process:

- Better Sales Forecasting Accuracy

- Providing New Insights into Customer Behavior

- Saving Time and Resources (with excellent reporting capabilities)

- Spotting New Insights Through Uncovering Patterns.

Table of Contents

- Input Data Preparation

- Feature Correlation Matrix

- Seasonal Decomposition

- SARIMAX Diagnostics

- One-Step Ahead Forecast

- Dynamic Forecast

- Feature Engineering

- Linear Regression

- Random Forest

- KNN Regressor

- XGBoost Model

- Final Comparison

- Summary

- Explore More

- References

- Let’s start by installing/importing our libraries and preparing input data to get things going!

- Read more here and follow the notebook.

Input Data Preparation

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

- Installing and importing libraries

!pip install xgboost

!pip install catboost

!pip install lightgbm

import sklearn;

print(sklearn.__version__)

1.4.0

import warnings

import itertools

import numpy as np

import scipy.stats as stats

import warnings

warnings.filterwarnings("ignore")

import seaborn as sns

import matplotlib.pyplot as plt

import pandas as pd

import calendar

from sklearn.model_selection import cross_val_score, cross_val_predict

from sklearn import metrics

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import Lasso, LinearRegression, LassoCV

from sklearn.model_selection import train_test_split, cross_val_score

from sklearn.neighbors import KNeighborsRegressor

import random

import sqlite3

from itertools import cycle, islice

from sklearn.tree import DecisionTreeRegressor

from sklearn.ensemble import RandomForestRegressor

from sklearn.ensemble import GradientBoostingRegressor

import xgboost as xgb

import catboost as cb

import lightgbm as lgb

from sklearn.experimental import enable_hist_gradient_boosting

from sklearn.ensemble import HistGradientBoostingRegressor

from sklearn.svm import SVR

# Import timedelta from datetime library

from datetime import timedelta

ss = StandardScaler()

- Reading the input data

walmart = pd.read_csv('train.csv')

walmart_feature = pd.read_csv('features.csv')

walmart_store = pd.read_csv('stores.csv')

- Grouping, merging, encoding categorical variables, fill NaN, and converting “Date” to date time

walmart_store_group=walmart.groupby(["Store","Date"])[["Weekly_Sales"]].sum()

walmart_store_group.reset_index(inplace=True)

result = pd.merge(walmart_store_group, walmart_store, how='inner', on='Store', left_on=None, right_on=None,

left_index=False, right_index=False, sort=False,

suffixes=('_x', '_y'), copy=True, indicator=False)

data = pd.merge(result, walmart_feature, how='inner', on=['Store','Date'], left_on=None, right_on=None,

left_index=False, right_index=False, sort=False,

suffixes=('_x', '_y'), copy=True, indicator=False)

#let's encode the categorical column : IsHoliday

data['IsHoliday'] = data['IsHoliday'].apply(lambda x: 1 if x == True else 0)

# Now converting "Date" to date time

data["Date"]=pd.to_datetime(data.Date)

# Extracting details from date given. so that can be used for seasonal checks or grouping

data["Day"]=data.Date.dt.day

data["Month"]=data.Date.dt.month

data["Year"]=data.Date.dt.year

# Changing the Months value from numbers to real values like Jan, Feb to Dec

data['Month'] = data['Month'].apply(lambda x: calendar.month_abbr[x])

#will create this column for later use

data['MarkdownsSum'] = data['MarkDown1'] + data['MarkDown2'] + data['MarkDown3'] + data['MarkDown4'] + data['MarkDown5']

data.fillna(0, inplace = True)

data['Week'] = data.Date.dt.isocalendar().week

- Selecting stores 4 and 6

data1 = pd.read_csv('train.csv')

data1.set_index('Date', inplace=True)

store4 = data1[data1.Store == 4]

# there are about 45 different stores in this dataset.

sales4 = pd.DataFrame(store4.Weekly_Sales.groupby(store4.index).sum())

sales4.dtypes

sales4.head(20)

# Grouped weekly sales by store 4

#remove date from index to change its dtype because it clearly isnt acceptable.

sales4.reset_index(inplace = True)

#converting 'date' column to a datetime type

sales4['Date'] = pd.to_datetime(sales4['Date'])

# resetting date back to the index

sales4.set_index('Date',inplace = True)

# Lets take store 6 data for analysis

store6 = data1[data1.Store == 6]

# there are about 45 different stores in this dataset.

sales6 = pd.DataFrame(store6.Weekly_Sales.groupby(store6.index).sum())

sales6.dtypes

# Grouped weekly sales by store 6

#remove date from index to change its dtype because it clearly isnt acceptable.

sales6.reset_index(inplace = True)

#converting 'date' column to a datetime type

sales6['Date'] = pd.to_datetime(sales6['Date'])

# resetting date back to the index

sales6.set_index('Date',inplace = True)

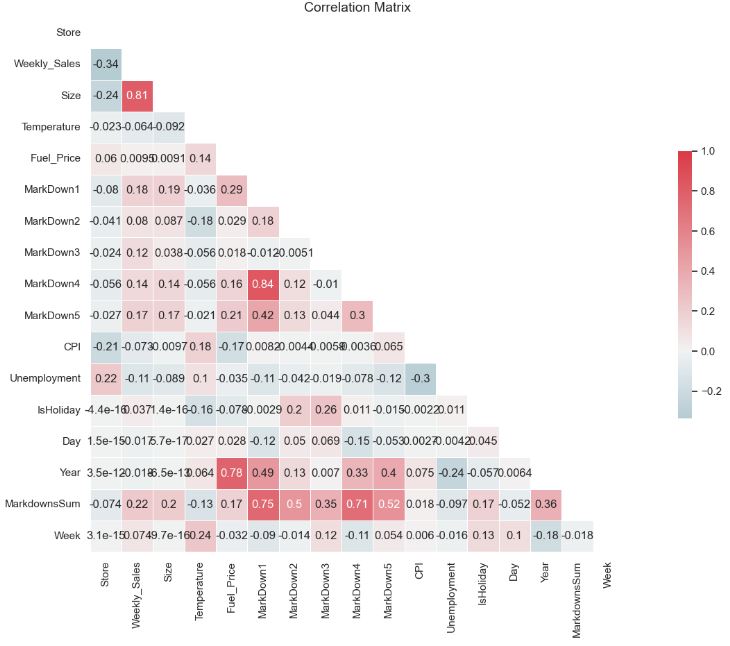

Feature Correlation Matrix

- Plotting the feature correlation matrix

sns.set(style="white")

corr = data.corr()

mask = np.triu(np.ones_like(corr))

f, ax = plt.subplots(figsize=(20, 10))

cmap = sns.diverging_palette(220, 10, as_cmap=True)

plt.title('Correlation Matrix', fontsize=14)

sns.heatmap(corr, mask=mask, cmap=cmap, vmax=1, center=0,

square=True, linewidths=.5, cbar_kws={"shrink": .5}, annot=True)

plt.show()

- The correlation matrix is a matrix that shows the correlation between variables. It gives the correlation between all the possible pairs of values in a matrix format. Using the above matrix, we can evaluate the relationship between our variables.

- In ML, highly correlated features refer to variables that have a strong linear relationship with each other. The presence of highly correlated features can lead to several issues, and removing them is often beneficial.

Seasonal Decomposition

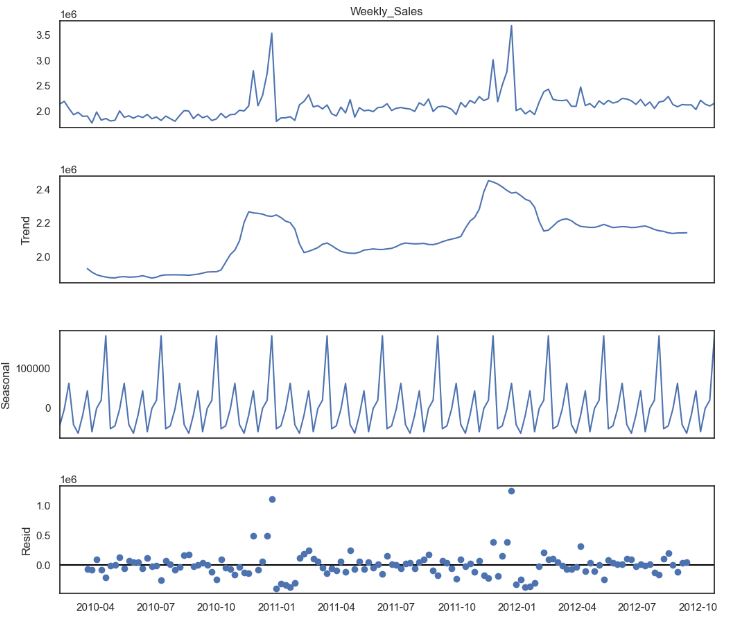

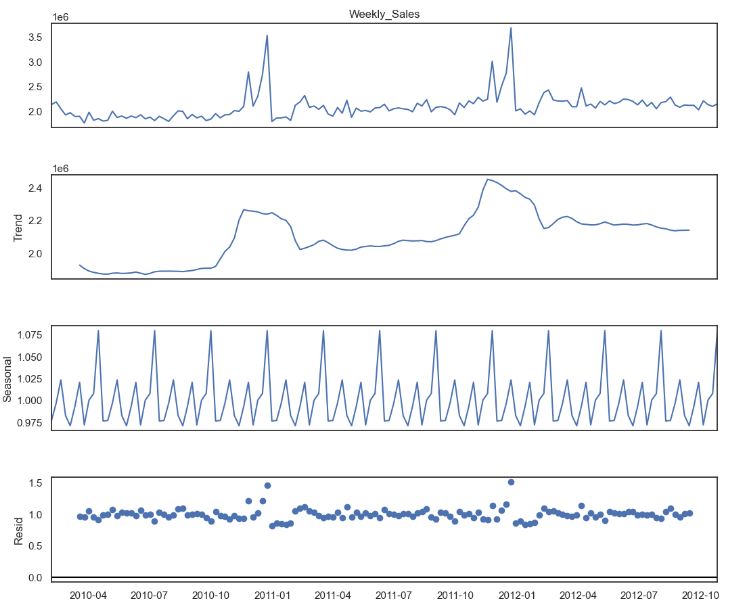

- Let’s look at the time series additive/multiplicative decomposition. It helps us disentangle our input data into components that may be easier to forecast. Basically, a time series consists of four components: level, trend, seasonality, and noise.

from statsmodels.tsa.seasonal import seasonal_decompose

decomposition = seasonal_decompose(sales4.Weekly_Sales, period=12)

fig = plt.figure()

fig = decomposition.plot()

fig.set_size_inches(12, 10)

plt.show()

decomposition = seasonal_decompose(sales4.Weekly_Sales, model= 'multiplicative', period=12)

fig = plt.figure()

fig = decomposition.plot()

fig.set_size_inches(12, 10)

plt.show()

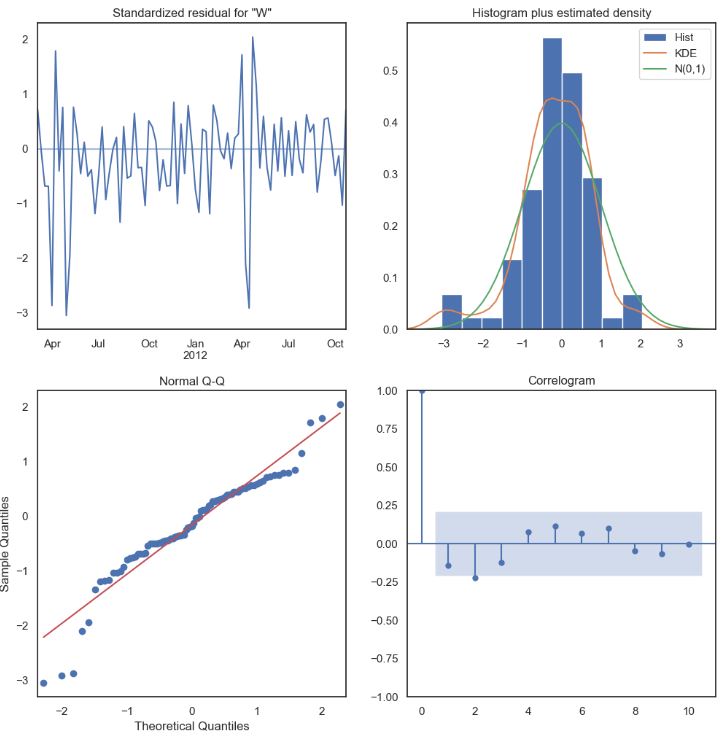

SARIMAX Diagnostics

- Let’s examine the Statsmodels’ SARIMAX (Seasonal AutoRegressive Integrated Moving Average) model with exogenous regressors.

# Define the p, d and q parameters to take any value between 0 and 2

p = d = q = range(0, 5)

# Generate all different combinations of p, d and q triplets

pdq = list(itertools.product(p, d, q))

# Generate all different combinations of seasonal p, d and q triplets

seasonal_pdq = [(x[0], x[1], x[2], 52) for x in list(itertools.product(p, d, q))]

import statsmodels.api as sm

mod = sm.tsa.statespace.SARIMAX(y1,

order=(4, 4, 3),

seasonal_order=(1, 1, 0, 52), #enforce_stationarity=False,

enforce_invertibility=False)

results = mod.fit()

print(results.summary().tables[1])

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 -1.7449 0.544 -3.207 0.001 -2.811 -0.679

ar.L2 -1.2798 0.586 -2.185 0.029 -2.428 -0.132

ar.L3 -0.5894 0.252 -2.340 0.019 -1.083 -0.096

ar.L4 -0.1879 0.092 -2.036 0.042 -0.369 -0.007

ma.L1 -1.3853 0.494 -2.805 0.005 -2.353 -0.417

ma.L2 -0.2065 1.063 -0.194 0.846 -2.290 1.877

ma.L3 0.5960 0.593 1.005 0.315 -0.566 1.758

ar.S.L52 -0.0672 0.048 -1.391 0.164 -0.162 0.027

sigma2 1.622e+10 6.23e-11 2.6e+20 0.000 1.62e+10 1.62e+10

==============================================================================

- Plotting SARIMAX QC diagnostics (standardized residuals, Histogram plus estimated density, Q-Q plot, and correlogram)

results.plot_diagnostics(figsize=(12, 12))

plt.show()

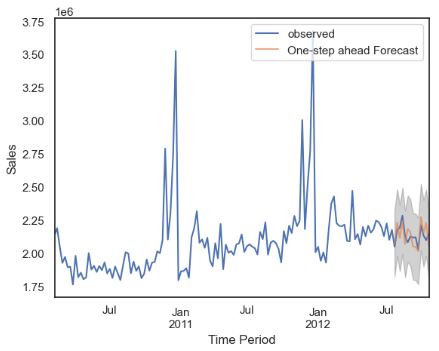

One-Step Ahead Forecast

- Let’s perform one-step ahead TSF for last 90 days

# Will predict for last 90 days. So setting the date according to that

pred = results.get_prediction(start=pd.to_datetime('2012-07-27'), dynamic=False)

pred_ci = pred.conf_int()

ax = y1['2010':].plot(label='observed')

pred.predicted_mean.plot(ax=ax, label='One-step ahead Forecast', alpha=.7)

ax.fill_between(pred_ci.index,

pred_ci.iloc[:, 0],

pred_ci.iloc[:, 1], color='k', alpha=.2)

ax.set_xlabel('Time Period')

ax.set_ylabel('Sales')

plt.legend()

plt.show()

y_forecasted = pred.predicted_mean

y_truth = y1['2012-7-27':]

# Compute the mean square error

mse = ((y_forecasted - y_truth) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format(round(mse, 2)))

The Mean Squared Error of our forecasts is 4757741704.39

Dynamic Forecast

- Performing the dynamic SARIMAX forecast

pred_dynamic = results.get_prediction(start=pd.to_datetime('2012-7-27'), dynamic=True, full_results=True)

pred_dynamic_ci = pred_dynamic.conf_int()

ax = y1['2010':].plot(label='observed', figsize=(12, 8))

pred_dynamic.predicted_mean.plot(label='Dynamic Forecast', ax=ax)

ax.fill_between(pred_dynamic_ci.index,

pred_dynamic_ci.iloc[:, 0],

pred_dynamic_ci.iloc[:, 1], color='k', alpha=.25)

ax.fill_betweenx(ax.get_ylim(), pd.to_datetime('2012-7-26'), y1.index[-1],

alpha=.1, zorder=-1)

ax.set_xlabel('Time Period')

ax.set_ylabel('Sales')

plt.legend()

plt.show()

# Extract the predicted and true values of our time series

y_forecasted = pred_dynamic.predicted_mean

y_truth = y1['2012-7-27':]

# Compute the Root mean square error

rmse = np.sqrt(((y_forecasted - y_truth) ** 2).mean())

print('The Root Mean Squared Error of our forecasts is {}'.format(round(rmse, 2)))

The Root Mean Squared Error of our forecasts is 77410.45

Residual= y_forecasted - y_truth

print("Residual for Store 4",np.abs(Residual).sum())

Residual for Store4 854828.1737922677

Feature Engineering

- Let’s prepare our data for training supervised ML models.

- Data pre-processing

#Importing Modules

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import statsmodels.api as sm

from sklearn.preprocessing import MinMaxScaler

import pickle

from os import path

from sklearn import metrics

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LinearRegression

from sklearn.ensemble import RandomForestRegressor

from sklearn.neighbors import KNeighborsRegressor

from xgboost import XGBRegressor

from keras.models import Sequential

from keras.layers import Dens

from scikeras.wrappers import KerasRegressor

#Importing Datasets

data = pd.read_csv('train.csv')

stores = pd.read_csv('stores.csv')

features = pd.read_csv('features.csv')

#Handling missing values of features dataset

features["CPI"].fillna(features["CPI"].median(),inplace=True)

features["Unemployment"].fillna(features["Unemployment"].median(),inplace=True)

for i in range(1,6):

features["MarkDown"+str(i)] = features["MarkDown"+str(i)].apply(lambda x: 0 if x < 0 else x)

features["MarkDown"+str(i)].fillna(value=0,inplace=True)

#Merging Training Dataset and merged stores-features Dataset

data = pd.merge(data,stores,on='Store',how='left')

data = pd.merge(data,features,on=['Store','Date'],how='left')

data['Date'] = pd.to_datetime(data['Date'])

data.sort_values(by=['Date'],inplace=True)

data.set_index(data.Date, inplace=True)

data['IsHoliday_x'].isin(data['IsHoliday_y']).all()

True

data.drop(columns='IsHoliday_x',inplace=True)

data.rename(columns={"IsHoliday_y" : "IsHoliday"}, inplace=True)

#Splitting Date Column

data['Year'] = data['Date'].dt.year

data['Month'] = data['Date'].dt.month

data['Week'] = data['Date'].dt.week

#Outlier Detection and Abnormalities

agg_data = data.groupby(['Store', 'Dept']).Weekly_Sales.agg(['max', 'min', 'mean', 'median', 'std']).reset_index()

agg_data.isnull().sum()

Store 0

Dept 0

max 0

min 0

mean 0

median 0

std 37

dtype: int64

store_data = pd.merge(left=data,right=agg_data,on=['Store', 'Dept'],how ='left')

store_data.dropna(inplace=True)

data = store_data.copy()

del store_data

data['Total_MarkDown'] = data['MarkDown1']+data['MarkDown2']+data['MarkDown3']+data['MarkDown4']+data['MarkDown5']

data.drop(['MarkDown1','MarkDown2','MarkDown3','MarkDown4','MarkDown5'], axis = 1,inplace=True)

numeric_col = ['Weekly_Sales','Size','Temperature','Fuel_Price','CPI','Unemployment','Total_MarkDown']

data_numeric = data[numeric_col].copy()

data = data[(np.abs(stats.zscore(data_numeric)) < 2.5).all(axis = 1)]

data=data[data['Weekly_Sales']>=0]

data['IsHoliday'] = data['IsHoliday'].astype('int')

- Data transformations for ML training

#One-hot-encoding

cat_col = ['Store','Dept','Type']

data_cat = data[cat_col].copy()

data_cat = pd.get_dummies(data_cat,columns=cat_col)

data = pd.concat([data, data_cat],axis=1)

data.drop(columns=cat_col,inplace=True)

data.drop(columns=['Date'],inplace=True)

#Data Normalization

num_col = ['Weekly_Sales','Size','Temperature','Fuel_Price','CPI','Unemployment','Total_MarkDown','max','min','mean','median','std']

minmax_scale = MinMaxScaler(feature_range=(0, 1))

def normalization(df,col):

for i in col:

arr = df[i]

arr = np.array(arr)

df[i] = minmax_scale.fit_transform(arr.reshape(len(arr),1))

return df

data = normalization(data.copy(),num_col)

#Recursive Feature Elimination

feature_col = data.columns.difference(['Weekly_Sales'])

- Calculating feature importance weights with Random Forest

radm_clf = RandomForestRegressor(oob_score=True,n_estimators=23)

radm_clf.fit(data[feature_col], data['Weekly_Sales'])

RandomForestRegressor(n_estimators=23, oob_score=True)

indices = np.argsort(radm_clf.feature_importances_)[::-1]

feature_rank = pd.DataFrame(columns = ['rank', 'feature', 'importance'])

for f in range(data[feature_col].shape[1]):

feature_rank.loc[f] = [f+1,

data[feature_col].columns[indices[f]],

radm_clf.feature_importances_[indices[f]]]

feature_rank

rank feature importance

0 1 median 5.239332e-01

1 2 mean 4.041693e-01

2 3 Week 1.983558e-02

3 4 Temperature 8.796048e-03

4 5 max 5.982970e-03

... ... ... ...

139 140 Dept_51 3.261420e-10

140 141 Dept_45 2.666958e-10

141 142 Dept_78 2.447811e-12

142 143 Dept_39 2.938813e-14

143 144 Dept_43 1.407660e-15

144 rows × 3 columns

x=feature_rank.loc[0:22,['feature']]

x=x['feature'].tolist()

print(x)

['median', 'mean', 'Week', 'Temperature', 'max', 'CPI', 'Fuel_Price', 'min', 'Unemployment', 'std', 'Month', 'Total_MarkDown', 'Dept_16', 'Dept_18', 'IsHoliday', 'Dept_3', 'Size', 'Dept_9', 'Dept_11', 'Year', 'Dept_1', 'Dept_5', 'Dept_56']

- Creating X, Y columns and splitting them with test_size=0.30

X = data[x]

Y = data['Weekly_Sales']

data = pd.concat([X,Y],axis=1)

#Data Split

X = data.drop(['Weekly_Sales'],axis=1)

Y = data.Weekly_Sales

X_train,X_test,y_train,y_test = train_test_split(X,Y,test_size=0.30, random_state=50)

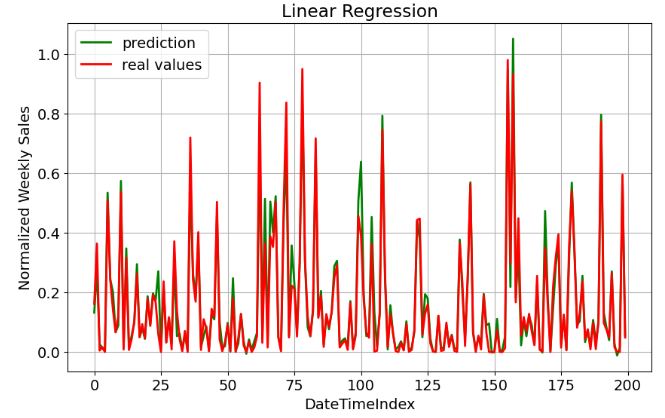

Linear Regression

- Training the Linear Regression (LR) model

#Linear Regression Model

lr = LinearRegression()

lr.fit(X_train, y_train)

lr_acc = lr.score(X_test,y_test)*100

print("Linear Regressor Accuracy - ",lr_acc)

Linear Regressor Accuracy - 92.23004968201279

y_pred = lr.predict(X_test)

print("MAE" , metrics.mean_absolute_error(y_test, y_pred))

print("MSE" , metrics.mean_squared_error(y_test, y_pred))

print("RMSE" , np.sqrt(metrics.mean_squared_error(y_test, y_pred)))

print("R2" , metrics.explained_variance_score(y_test, y_pred))

MAE 0.03010877755242702

MSE 0.0035040752885774932

RMSE 0.059195230285703705

R2 0.9223007841955709

- Plotting LR prediction vs real values

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 14})

plt.plot(lr.predict(X_test[:200]), label="prediction", linewidth=2.0,color='green')

plt.plot(y_test[:200].values, label="real values", linewidth=2.0,color='red')

plt.xlabel('DateTimeIndex')

plt.ylabel('Normalized Weekly Sales')

plt.title('Linear Regression')

plt.legend(loc="best")

plt.savefig('lr_real_pred.png')

plt.grid()

plt.show()

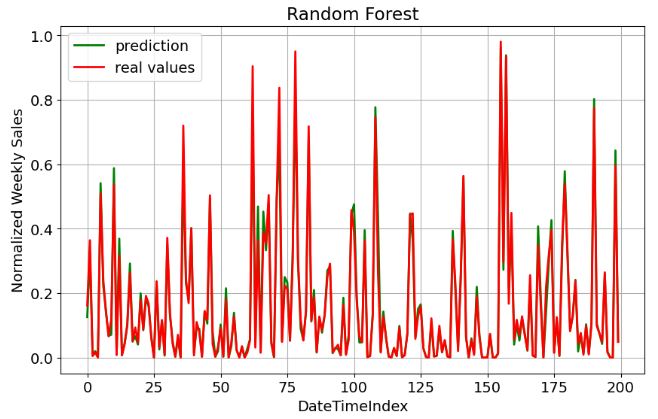

Random Forest

- Training the Random Forest (RF) model

#Random Forest Regressor Model

rf = RandomForestRegressor()

rf.fit(X_train, y_train)

rf_acc = rf.score(X_test,y_test)*100

print("Random Forest Regressor Accuracy - ",rf_acc)

Random Forest Regressor Accuracy - 97.75107356196521

y_pred = rf.predict(X_test)

print("MAE" , metrics.mean_absolute_error(y_test, y_pred))

print("MSE" , metrics.mean_squared_error(y_test, y_pred))

print("RMSE" , np.sqrt(metrics.mean_squared_error(y_test, y_pred)))

print("R2" , metrics.explained_variance_score(y_test, y_pred))

MAE 0.015971949755612464

MSE 0.001014215951819333

RMSE 0.03184675732031965

R2 0.9775111310889105

- Plotting RF prediction vs real values

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 14})

plt.plot(rf.predict(X_test[:200]), label="prediction", linewidth=2.0,color='green')

plt.plot(y_test[:200].values, label="real values", linewidth=2.0,color='red')

plt.xlabel('DateTimeIndex')

plt.ylabel('Normalized Weekly Sales')

plt.title('Random Forest')

plt.legend(loc="best")

plt.savefig('rf_real_pred.png')

plt.grid()

plt.show()

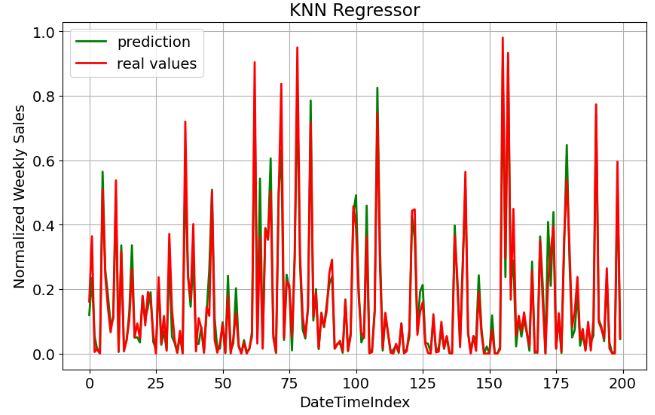

KNN Regressor

- Training the KNN regression model

#K Neighbors Regressor Model

knn = KNeighborsRegressor(n_neighbors = 5,weights = 'uniform')

knn.fit(X_train,y_train)

knn_acc = knn.score(X_test, y_test)*100

print("KNeigbhbors Regressor Accuracy - ",knn_acc)

KNeigbhbors Regressor Accuracy - 92.17276485694632

y_pred = knn.predict(X_test)

print("MAE" , metrics.mean_absolute_error(y_test, y_pred))

print("MSE" , metrics.mean_squared_error(y_test, y_pred))

print("RMSE" , np.sqrt(metrics.mean_squared_error(y_test, y_pred)))

print("R2" , metrics.explained_variance_score(y_test, y_pred))

MAE 0.032121861389530305

MSE 0.00352990947434587

RMSE 0.05941304128174108

R2 0.9231507700958216

- Plotting KNN prediction vs real values

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 14})

plt.plot(knn.predict(X_test[:200]), label="prediction", linewidth=2.0,color='green')

plt.plot(y_test[:200].values, label="real values", linewidth=2.0,color='red')

plt.xlabel('DateTimeIndex')

plt.ylabel('Normalized Weekly Sales')

plt.title('KNN Regressor')

plt.legend(loc="best")

plt.savefig('knn_real_pred.png')

plt.grid()

plt.show()

XGBoost Model

- Training the XGBoost model

#XGboost Model

xgbr = XGBRegressor()

xgbr.fit(X_train, y_train)

xgb_acc = xgbr.score(X_test,y_test)*100

print("XGBoost Regressor Accuracy - ",xgb_acc)

XGBoost Regressor Accuracy - 97.2773959867016

y_pred = xgbr.predict(X_test)

print("MAE" , metrics.mean_absolute_error(y_test, y_pred))

print("MSE" , metrics.mean_squared_error(y_test, y_pred))

print("RMSE" , np.sqrt(metrics.mean_squared_error(y_test, y_pred)))

print("R2" , metrics.explained_variance_score(y_test, y_pred))

MAE 0.019891003307968013

MSE 0.001227834034085841

RMSE 0.035040462812095406

R2 0.9727743194280883

- Plotting XGBoost prediction vs real values

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 14})

plt.plot(xgbr.predict(X_test[:200]), label="prediction", linewidth=2.0,color='green')

plt.plot(y_test[:200].values, label="real values", linewidth=2.0,color='red')

plt.xlabel('DateTimeIndex')

plt.ylabel('Normalized Weekly Sales')

plt.title('XGboost Regression')

plt.legend(loc="best")

plt.savefig('rf_real_pred.png')

plt.grid()

plt.show()

Final Comparison

- Summarizing our ML comparisons as follows

acc = {'model':['lr_acc','rf_acc','knn_acc','xgb_acc'],'accuracy':[lr_acc,rf_acc,knn_acc,xgb_acc]}

acc_df = pd.DataFrame(acc)

acc_df

model accuracy

0 lr_acc 92.230050

1 rf_acc 97.751074

2 knn_acc 92.172765

3 xgb_acc 97.277396

plt.figure(figsize=(10,8))

sns.barplot(x='model',y='accuracy',data=acc_df)

plt.savefig('compared_models.png')

plt.show()

- Random Forest (RF) seems to perform the best on our data.

Summary

- The main purpose of this study was to predict Walmart’s sales based on the available historic data and identify main factors that affect the weekly sales of selected stores.

- Relationships between independent and target variables were identified using the correlation matrix and feature importance weights implicit in RF.

- We have compared SARIMAX and ML TSF models with regard to their relative performance in terms of the Regressor Accuracy and other conventional metrics such as MAE, MSE, RMSE, and R2.

- There is no one-size-fits-all “best” ML algorithm for all situations, but RF and XGBoost appears to be 2 outstanding algorithms for e-commerce TSF (with R2, ACC ~ 97%), viz.

| No. | Metrics | Random Forest | XGBoost |

| 1 | Accuracy % | 97.751 | 97.277 |

| 2 | MAE | 0.01597 | 0.0199 |

| 3 | MSE | 0.0010 | 0.0012 |

| 4 | RMSE | 0.0318 | 0.0350 |

| 5 | R2 | 0.9775 | 0.9727 |

- Both SARIMAX TSF and best supervised ML algorithms help in overall business planning, budgeting, and financial risk management. It allows companies to efficiently allocate resources for future growth and manage their cash flow.

- An appropriate amount of training data is required to efficiently train the model and draw useful insights.

- Our future work will address a bias-variance tradeoff by combining SARIMAX and ML approaches into a hybrid statistical-AI model.

Explore More

- Uber’s Orbit Full Bayesian Time Series Forecasting & Inference

- Retail Sales, Store Item Demand Time-Series Analysis & Forecasting: AutoEDA, FB Prophet, SARIMAX & Model Tuning

- Leveraging Predictive Uncertainties of Time Series Forecasting Models

- Evaluation of ML Sales Forecasting: tslearn, Random Walk, Holt-Winters, SARIMAX, GARCH, Prophet, and LSTM

- A Balanced Mix-and-Match Time Series Forecasting: ThymeBoost, Prophet, and AutoARIMA

- Time Series Forecasting of Hourly U.S.A. Energy Consumption – PJM East Electricity Grid

- SARIMAX Cross-Validation of EIA Crude Oil Prices Forecast in 2023 – 2. Brent

- SARIMAX-TSA Forecasting, QC and Visualization of Online Food Delivery Sales

References

- Walmart Sales Prediction

- Predicting Walmart Sales, Exploratory Data Analysis, and Walmart Sales Dashboard

- Fork of Machine Learning Models on Walmart Data

- walmart-sales-forecasting

- Weekly Sales Forecasts Using Non-Seasonal ARIMA Models

- Forecasting – Final Project

- Project Report – Walmart Sales Prediction

- Walmart Sales Forecasting Using Regression Analysis

- Retail Sales Forecasting at Walmart

- Walmart Sales Prediction – (Best ML Algorithms)

- Walmart Sales Project

- Walmart Sales: Refurbished Learning

- Walmart Sales Prediction Using ML Regressors

- Walmart_sales_predict 94% accuracy

- Walmart Sales Prediction

- Forecasting Sales Walmart Condensed

- Walmart_sales_prediction(Best_ml_algo)

- Demo X E-Training

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment