- Sales forecasting, a cornerstone of strategic planning, equips organizations with insights to anticipate market trends and drive informed decision-making.

- The goal of this data science project is to evaluate the available sales forecasting algorithms in Python using the challenging time-series Kaggle dataset.

- We are provided with daily historical sales data. The task is to predict total sales for every product and store in the next month. Note that the list of shops and products slightly changes every month. Creating a robust model that can handle such situations is part of the challenge.

- We will compare the following Python open-source libraries designed for ML-type forecasting of univariate time series: tslearn, Random Walk, Holt-Winters, SARIMA, GARCH, Prophet, and LSTM (cf. Appendix).

- q.v. [1-5].

Table of Contents

- Input Data

- Time Series Analysis

- Train/Test Splitting

- Random Walk Model

- Holt-Winters Model

- SARIMAX Model

- GARCH Model

- LSTM Model

- Prophet Model

- Di Pietro’s Model

- Conclusions

- References

- Explore More

- Appendix

Input Data

- Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH')

os. getcwd()

- Importing the key libraries and utility functions from Appendix

import warnings

import pandas as pd

warnings.filterwarnings("ignore")

from ts_utils6 import * # See Appendix

import pyts

- Reading the input dataset

dtf = pd.read_csv('data_sales.csv')

dtf.head()

date date_block_num shop_id item_id item_price item_cnt_day

0 02.01.2013 0 59 22154 999.00 1.0

1 03.01.2013 0 25 2552 899.00 1.0

2 05.01.2013 0 25 2552 899.00 -1.0

3 06.01.2013 0 25 2554 1709.05 1.0

4 15.01.2013 0 25 2555 1099.00 1.0

- Grouping the data by date after datetime format conversion

dtf["date"] = pd.to_datetime(dtf['date'], format='%d.%m.%Y')

ts = dtf.groupby("date")["item_cnt_day"].sum().rename("sales")

ts.tail()date

2015-10-27 1551.0

2015-10-28 3593.0

2015-10-29 1589.0

2015-10-30 2274.0

2015-10-31 3104.0

Name: sales, dtype: float64

- Printing the descriptive population and 1-month moving statistics

print("population --> len:", len(ts), "| mean:", round(ts.mean()), " | std:", round(ts.std()))

w = 30

print("moving --> len:", w, " | mean:", round(ts.ewm(span=w).mean()[-1]), " | std:", round(ts.ewm(span=w).std()[-1]))

population --> len: 1034 | mean: 3528 | std: 1585

moving --> len: 30 | mean: 2305 | std: 773

Time Series Analysis

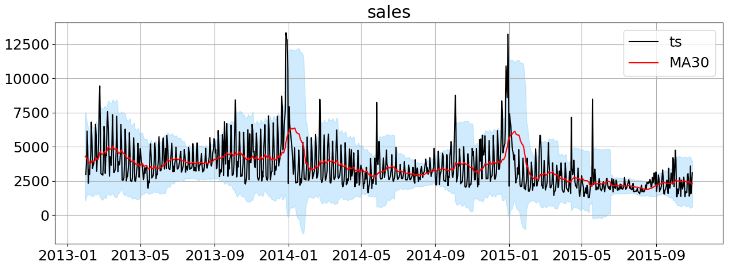

- Plotting time series (ts) sales data vs MA30

import matplotlib.pyplot as plt

plt.rcParams.update({'font.size': 18})

plot_ts(ts, plot_ma=True, plot_intervals=True, window=w, figsize=(15,5))

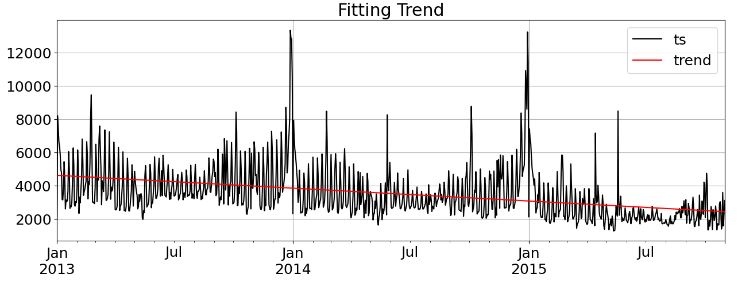

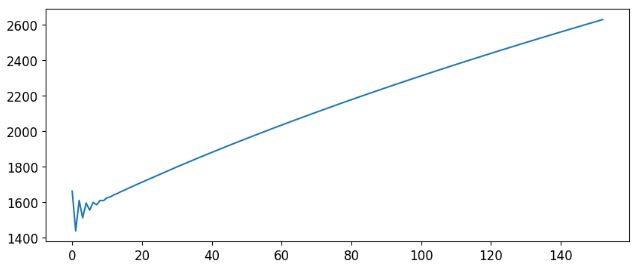

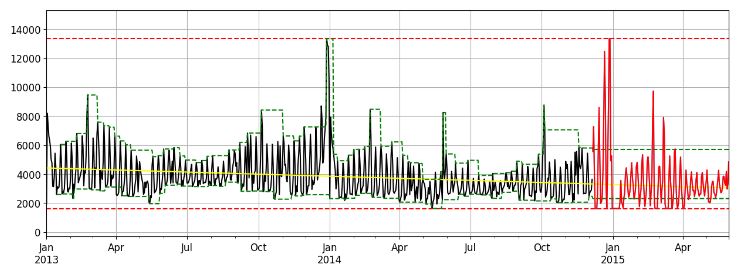

- Fitting the linear trend line

trend, line = fit_trend(ts, degree=1, plot=True, figsize=(15,5))

There is a slight trend and it’s linear (“additive”)

print(“constant:”, round(line[-1],2), “| slope:”, round(line[0],2))

constant: 4622.02 | slope: -2.12

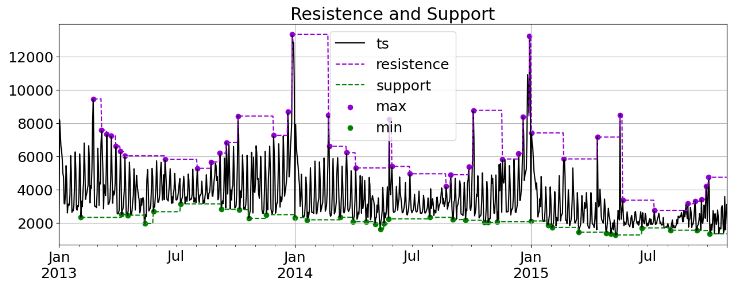

- Plotting the 1-month moving resistance/support lines with local min/max values

res_sup = resistence_support(ts, window=30, trend=False, plot=True, figsize=(15,5))

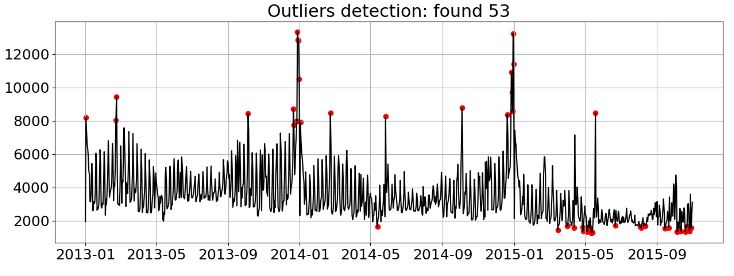

- Detecting outliers

dtf_outliers = find_outliers(ts, perc=0.05, figsize=(15,5))

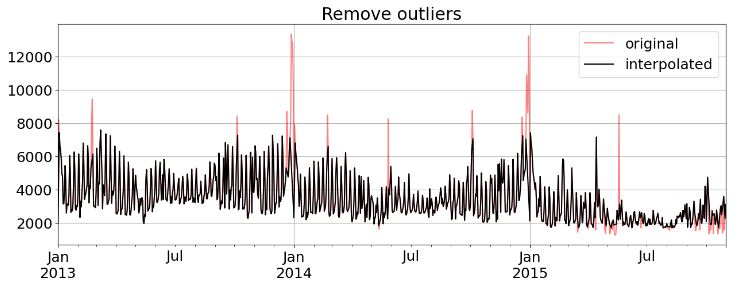

- Removing outliers

ts_clean = remove_outliers(ts, outliers_idx=dtf_outliers[dtf_outliers["outlier"]==1].index, figsize=(15,5))

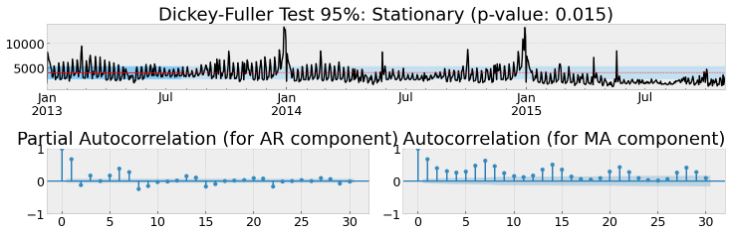

- Testing stationarity of the original data ts

test_stationarity_acf_pacf(ts, sample=0.20, maxlag=w, figsize=(15,5))

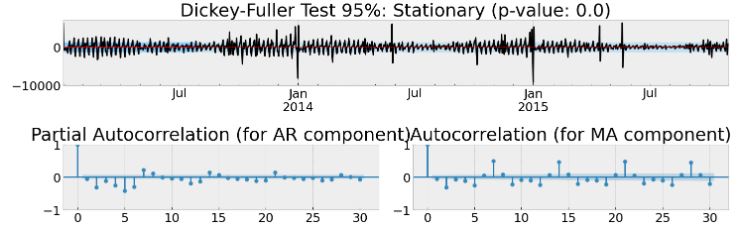

- Testing stationarity of the first-order differences

test_stationarity_acf_pacf(diff_ts(ts, order=1), sample=0.20, maxlag=30, figsize=(15,5))

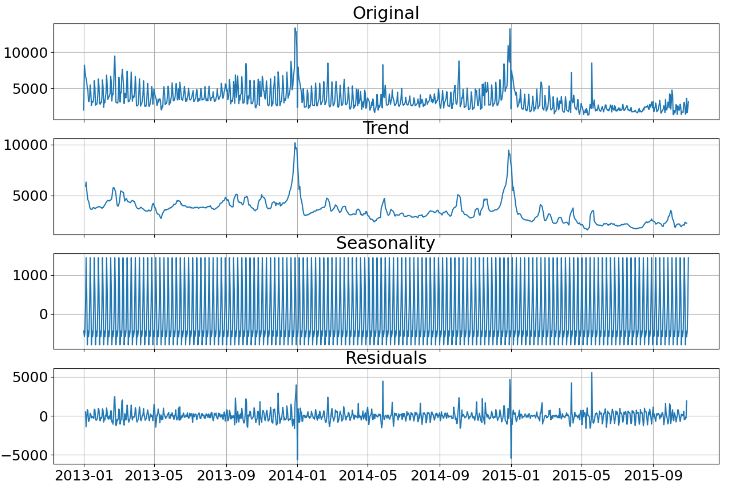

- Performing weekly seasonality & trend decomposition

dic_decomposed = decompose_ts(ts, s=7, figsize=(15,10))

Train/Test Splitting

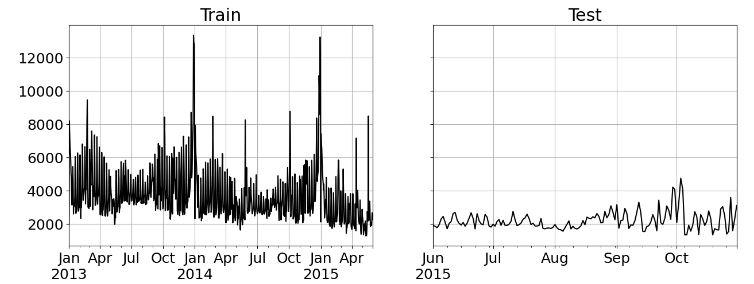

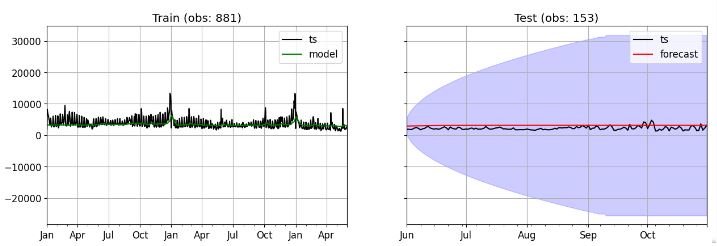

- Train/test data splitting

ts_train, ts_test = split_train_test(ts, exog=None, test="2015-06-01", plot=True, figsize=(15,5))

print("train:", len(ts_train), "obs | test:", len(ts_test), "obs")

--- splitting at index: 881 | 2015-06-01 00:00:00 | test size: 0.15 ---

train: 881 obs | test: 153 obs

Random Walk Model

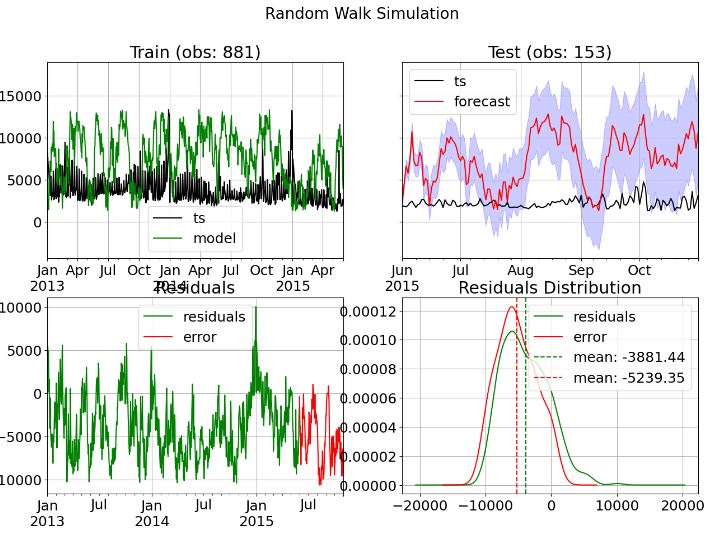

- Implementing the Random Walk model

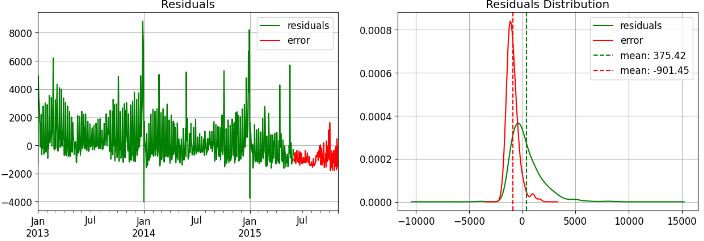

dtf = simulate_rw(ts_train, ts_test, conf=0.10, figsize=(15,10))

Training --> Residuals mean: -3881.0 | std: 3535.0

Test --> Error mean: -5239.0 | std: 2955.0 | mae: 5271.0 | mape: 255.0 % | mse: 36123903.0 | rmse: 6010.0

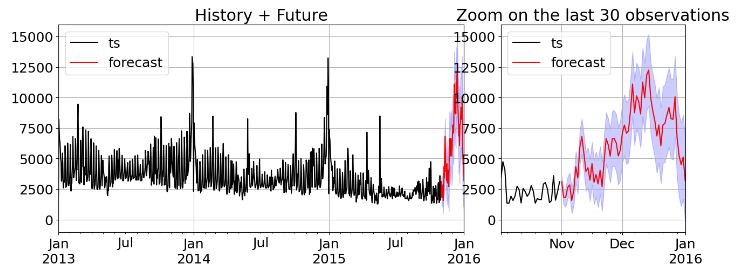

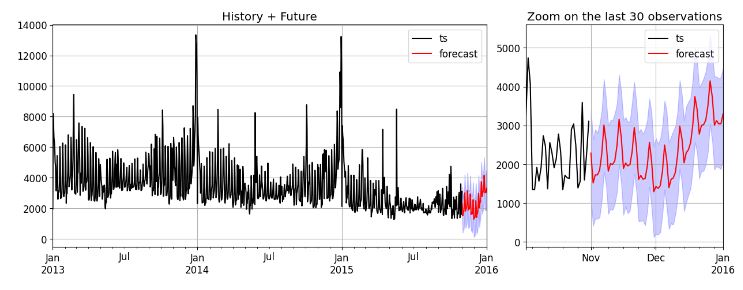

- Generating the future forecast using the Random Walk model

future = forecast_rw(ts, end="2016-01-01", conf=0.10, zoom=30, figsize=(15,5))

--- generating index date --> freq: D | start: 2015-11-01 00:00:00 | end: 2016-01-01 00:00:00 | len: 62 ---

--- computing confidence interval ---

Holt-Winters Model

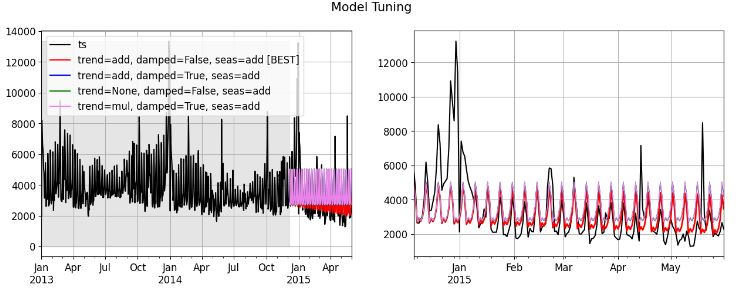

- Implementing the Exponential Smoothing Model (ESM) with tuning

res = tune_expsmooth_model(ts_train, s=s, val_size=0.2, scoring=metrics.mean_absolute_error, top=4, figsize=(15,5))

res.head()

combo score model

0 trend=add, damped=False, seas=add 1048.356846 <statsmodels.tsa.holtwinters.results.HoltWinte...

1 trend=add, damped=True, seas=add 1301.840904 <statsmodels.tsa.holtwinters.results.HoltWinte...

2 trend=None, damped=False, seas=add 1309.152958 <statsmodels.tsa.holtwinters.results.HoltWinte...

3 trend=mul, damped=True, seas=add 1319.483026 <statsmodels.tsa.holtwinters.results.HoltWinte...

4 trend=add, damped=True, seas=None 1483.018551 <statsmodels.tsa.holtwinters.results.HoltWinte...

- Implementing the ESM multiplicative seasonality every 6 observations

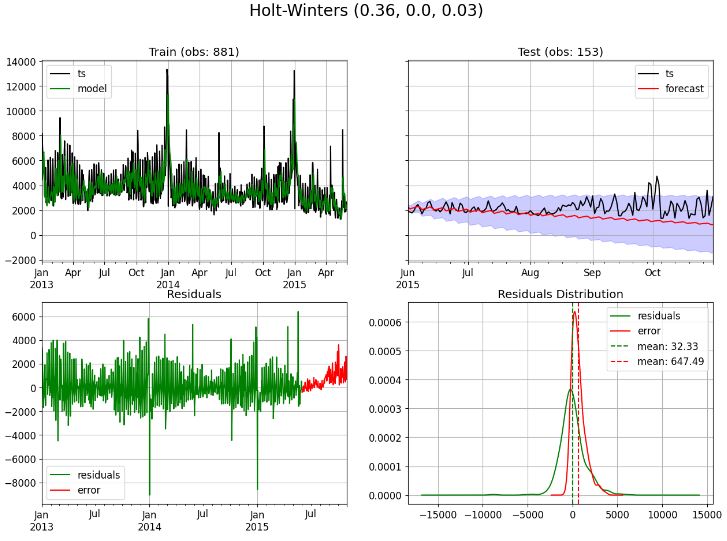

dtf, model = fit_expsmooth(ts_train, ts_test, trend="additive", damped=False, seasonal="multiplicative", s=6,

factors=(None,None,None), conf=0.10, figsize=(15,10)

Seasonal parameters: multiplicative Seasonality every 6 observations

--- computing confidence interval ---

Training --> Residuals mean: 32.0 | std: 1413.0

Test --> Error mean: 647.0 | std: 748.0 | mae: 696.0 | mape: 28.0 % | mse: 974519.0 | rmse: 987.0

It seems that the average error of prediction is in 388 unit of sales (16% of the predicted value).

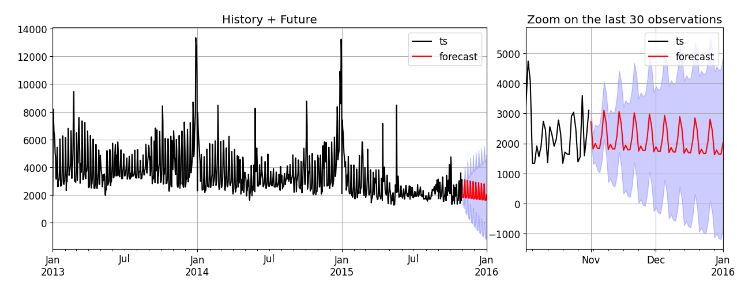

- Generating the future forecast using the ESM model

model = smt.ExponentialSmoothing(ts, trend="additive", damped=False,

seasonal="multiplicative", seasonal_periods=s).fit(0.64)

future = forecast_autoregressive(ts, model, end="2016-01-01", conf=0.30, zoom=30, figsize=(15,5))

--- generating index date --> freq: D | start: 2015-11-01 00:00:00 | end: 2016-01-01 00:00:00 | len: 62 ---

--- computing confidence interval ---

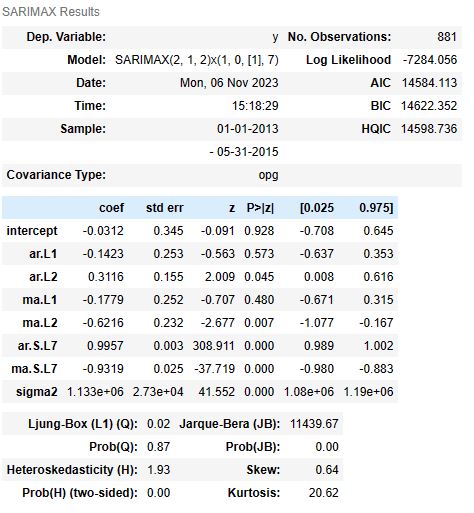

SARIMAX Model

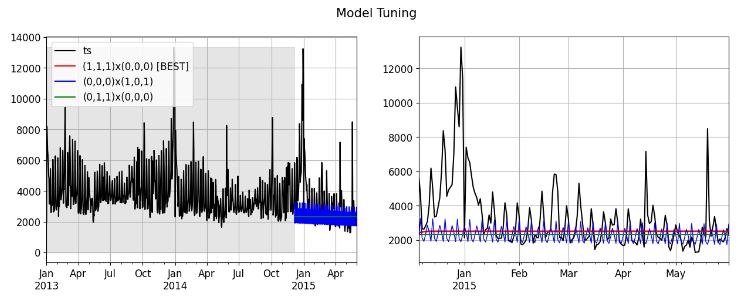

- Tuning the SARIMAX model

res = tune_arima_model(ts_train, s=s, val_size=0.2, max_order=(1,1,1), seasonal_order=(1,0,1),

scoring=metrics.mean_absolute_error, top=3, figsize=(15,5))

res.head()

combo score model

0 (1,1,1)x(0,0,0) 1267.729997 <statsmodels.tsa.statespace.sarimax.SARIMAXRes...

1 (0,0,0)x(1,0,1) 1284.688508 <statsmodels.tsa.statespace.sarimax.SARIMAXRes...

2 (0,1,1)x(0,0,0) 1288.717213 <statsmodels.tsa.statespace.sarimax.SARIMAXRes...

3 (1,1,0)x(0,0,0) 1293.258417 <statsmodels.tsa.statespace.sarimax.SARIMAXRes...

4 (0,1,0)x(0,0,0) 1296.548023 <statsmodels.tsa.statespace.sarimax.SARIMAXRes...

- Finding the best SARIMAX model

find_best_sarimax(ts_train, seasonal=True, stationary=False, s=s, exog=None,

max_p=10, max_d=3, max_q=10,

max_P=1, max_D=1, max_Q=1)

best model --> (p, d, q): (2, 1, 2) and (P, D, Q, s): (1, 0, 1, 7)

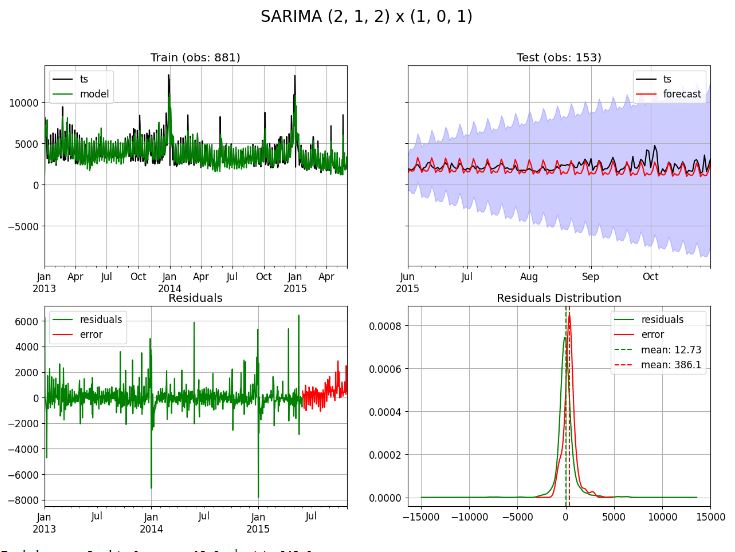

- Fitting with the best SARIMAX model

dtf, model = fit_sarimax(ts_train, ts_test, order=(2,1,2), seasonal_order=(1, 0, 1), s=s, conf=0.95, figsize=(15,10))

Trend parameters: d=1

Seasonal parameters: Seasonality every 7 observations

Exog parameters: Not given

Training --> Residuals mean: 13.0 | std: 948.0

Test --> Error mean: 386.0 | std: 644.0 | mae: 567.0 | mape: 24.0 % | mse: 560661.0 | rmse: 749.0

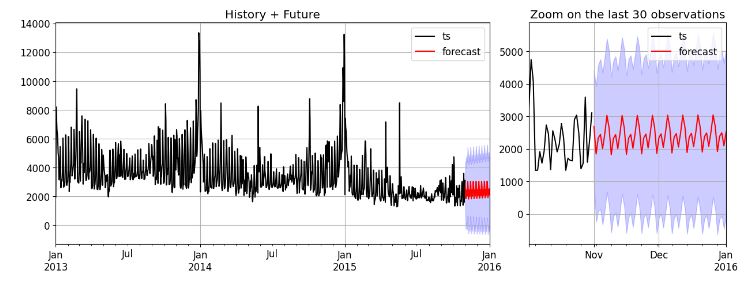

- Forecast with the best SARIMAX model

model = smt.SARIMAX(ts, order=(2,1,2), seasonal_order=(1,0,1,s), exog=None).fit()

future = forecast_autoregressive(ts, model, end="2016-01-01", conf=0.95, zoom=30, figsize=(15,5))

--- generating index date --> freq: D | start: 2015-11-01 00:00:00 | end: 2016-01-01 00:00:00 | len: 62 ---

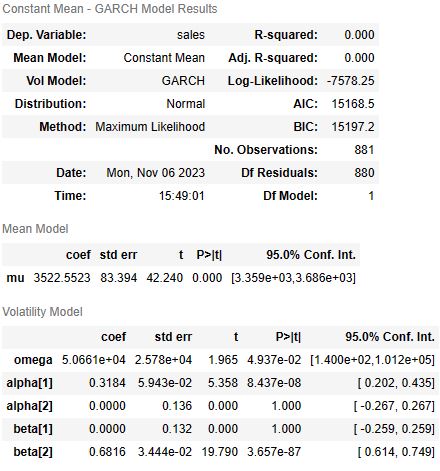

GARCH Model

- Implementing the GARCH model

fit_garch(ts_train, ts_test, order=(2,1,2), seasonal_order=(1,0,1,s), figsize=(15,10))

Iteration: 7, Func. Count: 70, Neg. LLF: 7732.775377088017

Iteration: 14, Func. Count: 139, Neg. LLF: 6935.63535033199

Iteration: 21, Func. Count: 202, Neg. LLF: 6931.972089490232

Iteration: 28, Func. Count: 265, Neg. LLF: 6929.40082625206

Optimization terminated successfully (Exit mode 0)

Current function value: 6929.400098515533

Iterations: 32

Function evaluations: 300

Gradient evaluations: 32

--- got error ---

unsupported operand type(s) for -: 'float' and 'ARCHModelForecast'

(None,

Constant Mean - GJR-GARCH Model Results

====================================================================================

Dep. Variable: None R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GJR-GARCH Log-Likelihood: -6929.40

Distribution: Standardized Student's t AIC: 13874.8

Method: Maximum Likelihood BIC: 13913.0

No. Observations: 881

Date: Mon, Nov 06 2023 Df Residuals: 880

Time: 15:36:09 Df Model: 1

Mean Model

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

mu -46.3875 17.871 -2.596 9.440e-03 [-81.414,-11.361]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 2.6917e+05 9.054e+04 2.973 2.950e-03 [9.171e+04,4.466e+05]

alpha[1] 0.4922 0.216 2.274 2.294e-02 [6.806e-02, 0.916]

alpha[2] 0.3848 0.267 1.442 0.149 [ -0.138, 0.908]

gamma[1] -0.2185 0.230 -0.949 0.343 [ -0.670, 0.233]

beta[1] 0.1428 0.231 0.618 0.536 [ -0.310, 0.595]

beta[2] 0.0000 5.892e-02 0.000 1.000 [ -0.115, 0.115]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 2.7612 0.187 14.790 1.700e-49 [ 2.395, 3.127]

========================================================================

Covariance estimator: robust

ARCHModelResult, id: 0x2412979da00)

- Fitting the GARCH model

import arch

from arch import arch_model

model = arch_model(ts_train, p=2, q=2)

model_fit = model.fit()

model_fit.summary()

Iteration: 1, Func. Count: 8, Neg. LLF: 8625.687094584897

Iteration: 2, Func. Count: 16, Neg. LLF: 7591.663085839065

Iteration: 3, Func. Count: 23, Neg. LLF: 7590.181494531133

Iteration: 4, Func. Count: 30, Neg. LLF: 7589.836295096868

Iteration: 5, Func. Count: 37, Neg. LLF: 7589.827769095689

Iteration: 6, Func. Count: 44, Neg. LLF: 7589.806877638113

Iteration: 7, Func. Count: 51, Neg. LLF: 7589.782971327825

Iteration: 8, Func. Count: 58, Neg. LLF: 7589.697896589118

Iteration: 9, Func. Count: 65, Neg. LLF: 7589.475629047222

Iteration: 10, Func. Count: 72, Neg. LLF: 7588.901641267379

Iteration: 11, Func. Count: 79, Neg. LLF: 7587.335035285622

Iteration: 12, Func. Count: 86, Neg. LLF: 7583.837150680619

Iteration: 13, Func. Count: 93, Neg. LLF: 7579.646854205145

Iteration: 14, Func. Count: 100, Neg. LLF: 7578.593139426219

Iteration: 15, Func. Count: 107, Neg. LLF: 7578.292100471091

Iteration: 16, Func. Count: 114, Neg. LLF: 7578.255669462309

Iteration: 17, Func. Count: 121, Neg. LLF: 7578.2502424651775

Iteration: 18, Func. Count: 128, Neg. LLF: 7578.245473206713

Iteration: 19, Func. Count: 135, Neg. LLF: 7583.610036013718

Iteration: 20, Func. Count: 145, Neg. LLF: 7578.245736636854

Iteration: 21, Func. Count: 154, Neg. LLF: 7578.245736770681

Iteration: 22, Func. Count: 160, Neg. LLF: 7578.24573671558

Optimization terminated successfully (Exit mode 0)

Current function value: 7578.245736770681

Iterations: 23

Function evaluations: 160

Gradient evaluations: 22

- GARCH predictions with horizon=153 which is len(ts_test)

predictions = model_fit.forecast(horizon=153)

plt.figure(figsize=(10,4))

preds, = plt.plot(np.sqrt(predictions.variance.values[-1, :]))

LSTM Model

- Implementing the LSTM Sequential model

s = 130

n_features = 1

model = models.Sequential()

model.add( layers.LSTM(input_shape=(s,n_features), units=50, activation='relu', return_sequences=True) )

model.add( layers.Dropout(0.2) )

model.add( layers.LSTM(units=50, activation='relu', return_sequences=False) )

model.add( layers.Dense(1) )

model.compile(optimizer='adam', loss='mean_absolute_error')

model.summary()

Model: "sequential_1"

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

lstm_2 (LSTM) (None, 130, 50) 10400

dropout_1 (Dropout) (None, 130, 50) 0

lstm_3 (LSTM) (None, 50) 20200

dense_1 (Dense) (None, 1) 51

=================================================================

Total params: 30,651

Trainable params: 30,651

Non-trainable params: 0

dtf, model = fit_lstm(ts_train, ts_test, model, exog=None, s=s, epochs=1, conf=0.30, figsize=(15,10))

Training --> Residuals mean: 375.0 | std: 1451.0

Test --> Error mean: -901.0 | std: 559.0 | mae: 976.0 | mape: 50.0 % | mse: 1123190.0 | rmse: 1060.0

- LSTM (memory: 130) forecasting

Prophet Model

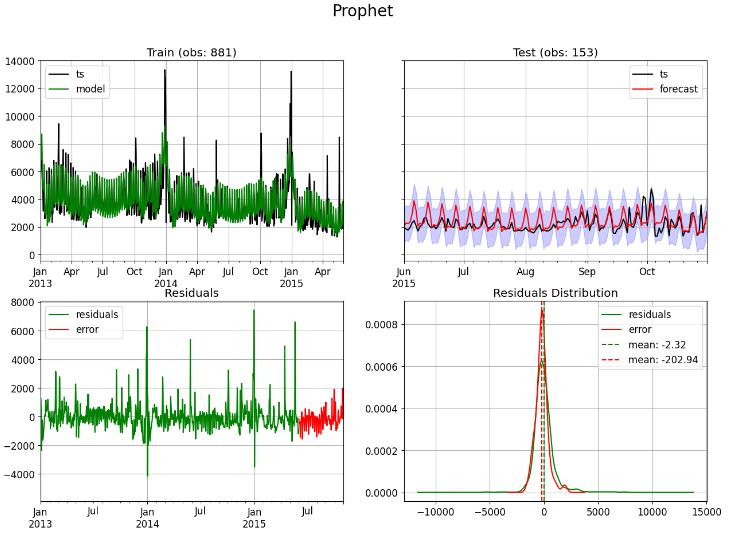

- Implementing the Prophet model

dtf_train = ts_train.reset_index().rename(columns={"date":"ds", "sales":"y"})

dtf_test = ts_test.reset_index().rename(columns={"date":"ds", "sales":"y"})

dtf_train.tail()

ds y

876 2015-05-27 1953.0

877 2015-05-28 1885.0

878 2015-05-29 2146.0

879 2015-05-30 2665.0

880 2015-05-31 2283.0

dtf_holidays = None

from prophet.forecaster import Prophet

model = Prophet(growth="linear", changepoints=None, n_changepoints=25, seasonality_mode="multiplicative",

yearly_seasonality="auto", weekly_seasonality="auto", daily_seasonality=False,

holidays=dtf_holidays, interval_width=0.80)

dtf, model = fit_prophet(dtf_train, dtf_test, model=model, figsize=(15,10))

future = forecast_prophet(dtf, model, end="2016-01-01", zoom=30, figsize=(15,5))

Training --> Residuals mean: -2.0 | std: 962.0

Test --> Error mean: -203.0 | std: 573.0 | mae: 448.0 | mape: 20.0 % | mse: 367888.0 | rmse: 607.0

Di Pietro’s Model

- Tuning the custom model

# Tuning

tune = custom_model(ts_train.head(int(0.8*len(ts_train))), pred_ahead=int(0.2*len(ts_train)),

trend=True, seasonality_types=["dow","dom","doy","woy","moy"],

level_window=7, sup_res_windows=(365,365), floor_cap=(True,True),

plot=True, figsize=(15,5))

--- generating index date --> freq: D | start: 2014-12-06 00:00:00 | end: 2015-05-30 00:00:00 | len: 176 ---

- Fitting the custom model

trend = True

seasonality_types = ["dow","dom","doy","woy","moy"]

level_window = 7

sup_res_windows = (365,365)

floor_cap = (True,True)

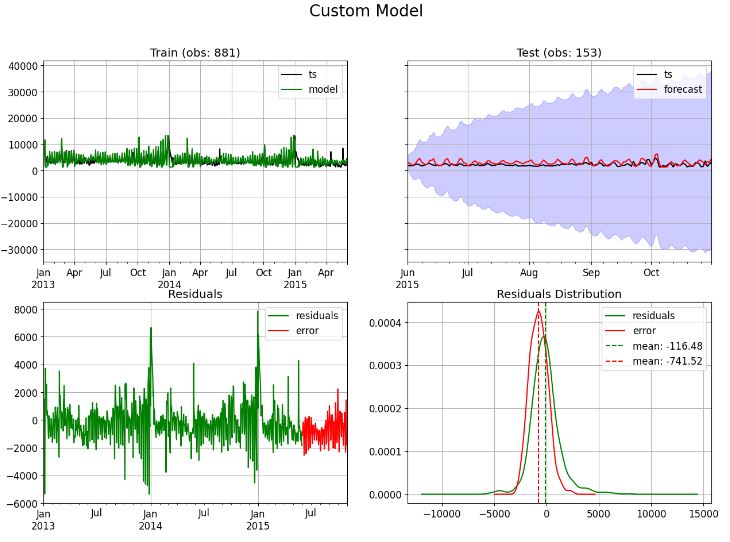

dtf = fit_custom_model(ts_train, ts_test, trend, seasonality_types, level_window, sup_res_windows, floor_cap,

conf=0.1, figsize=(15,10))

--- generating index date --> freq: D | start: 2015-06-01 00:00:00 | end: 2015-10-31 00:00:00 | len: 153 ---

--- computing confidence interval ---

Training --> Residuals mean: -116.0 | std: 1398.0

Test --> Error mean: -742.0 | std: 851.0 | mae: 930.0 | mape: 44.0 % | mse: 1269838.0 | rmse: 1127.0

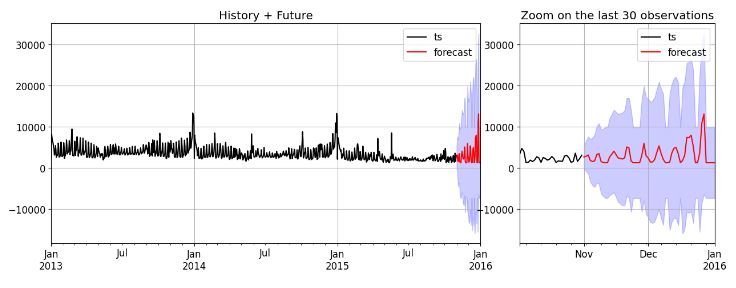

- Custom model future forecasting

future = forecast_custom_model(ts, trend, seasonality_types, level_window, sup_res_windows, floor_cap,

conf=0.3, end="2016-01-01", zoom=30, figsize=(15,5))

--- generating index date --> freq: D | start: 2015-11-01 00:00:00 | end: 2016-01-01 00:00:00 | len: 62 ---

--- generating index date --> freq: D | start: 2015-11-01 00:00:00 | end: 2016-01-01 00:00:00 | len: 62 ---

--- computing confidence interval ---

Conclusions

- We have evaluated several ML-type time series analysis (TSA) algorithms to analyze historical sales data and make predictions about future sales.

- TSA involves analyzing data collected over time, such as sales data, and modeling historical trends and seasonal patterns to make predictions about the future.

- TSA s useful for predicting sales because it takes into account historical patterns and trends, such as seasonality and long-term trends, to make accurate predictions.

- The technique can also identify anomalies or unexpected events that may impact future sales, allowing businesses to make necessary adjustments to their strategy.

- In this case study, tslearn, Random Walk and GARCH did not performed well on the training and test sets.

- We summarize the key performance metrics of other 5 models in Table below:

| Methods/Scores | RMSE | STD | MAPE % |

| Prophet | 607 | 573 | 20 |

| LSTM | 1060 | 559 | 50 |

| SARIMAX | 749 | 644 | 24 |

| HW | 987 | 748 | 28 |

| Custom | 1127 | 851 | 44 |

- It appears that the 3 best performing models are Prophet, SARIMAX, and Holt-Winters.

- These models use TSA to generate most accurate future sales based on historical train data. Traditional methods, on the other hand, can be time-intensive, error-prone, and vulnerable to human biases.

- Our results enable businesses to swiftly generate accurate forecasts, monitor market trends, and make data-driven decisions.

References

- Predict Future Sales

- DataScience_ArtificialIntelligence_Utils

- Time Series Analysis for Machine Learning

- Time Series Forecasting with Random Walk

- Time Series Forecasting: ARIMA vs LSTM vs PROPHET

Explore More

- A Balanced Mix-and-Match Time Series Forecasting: ThymeBoost, Prophet, and AutoARIMA

- Predicting Rolling Volatility of the NVIDIA Stock – GARCH vs XGBoost

- Time Series Forecasting of Hourly U.S.A. Energy Consumption – PJM East Electricity Grid

- Risk-Return Analysis and LSTM Price Predictions of 4 Major Tech Stocks in 2023

- SARIMAX X-Validation of EIA Crude Oil Prices Forecast in 2023 – 1. WTI

- BTC-USD Freefall vs FB/Meta Prophet 2022-23 Predictions

- BTC-USD Price Prediction with LSTM

- SARIMAX-TSA Forecasting, QC and Visualization of Online Food Delivery Sales

- Stock Forecasting with FBProphet

- Predicting the JPM Stock Price and Breakouts with Auto ARIMA, FFT, LSTM and Technical Trading Indicators

- S&P 500 Algorithmic Trading with FBProphet

Appendix

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment