Some experts call Bitcoin “the currency of the future”. The Bitcoin price has increased several times during the 2017 year. At the same time, it is very volatile.

The objective of this project is to test the deep learning algorithm of real-time BTC-USD price prediction in Q4 ’22.

The entire Python workflow looks like this:

- Importing the necessary Python libraries

- Load and check the real-time input dataset

- Data editing, transformations and preparations

- Exploratory Data Analysis (EDA)

- Training 2-layers LSTM Neural Network (NN)

- Check Predicted vs Actual Prices USD + RMSE

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’) # Set working directory

os. getcwd()

and import the libraries

import warnings

warnings.filterwarnings(“ignore”)

import numpy as np

import pandas as pd

import statsmodels.api as sm

from scipy import stats

from sklearn.metrics import mean_squared_error

from math import sqrt

from random import randint

from keras.models import Sequential

from keras.layers import Dense

from keras.layers import LSTM

from keras.layers import GRU

from keras.callbacks import EarlyStopping

from keras import initializers

from matplotlib import pyplot

from datetime import datetime

from matplotlib import pyplot as plt

import plotly.offline as py

import plotly.graph_objs as go

py.init_notebook_mode(connected=True)

%matplotlib inline

import yfinance as yf

import datetime

from datetime import date, timedelta

Let’s load the input real-time dataset

today = date.today()

d1 = today.strftime(“%Y-%m-%d”)

end_date = d1

d2 = date.today() – timedelta(days=730)

d2 = d2.strftime(“%Y-%m-%d”)

start_date = d2

data = yf.download(‘BTC-USD’,

start=start_date,

end=end_date,

progress=False)

data[“Date”] = data.index

data = data[[“Date”, “Open”, “High”, “Low”, “Close”, “Adj Close”, “Volume”]]

data.reset_index(drop=True, inplace=True)

print(data.tail())

Date Open High Low Close \

725 2022-10-21 19053.203125 19237.384766 18770.970703 19172.468750

726 2022-10-22 19172.380859 19248.068359 19132.244141 19208.189453

727 2022-10-23 19207.734375 19646.652344 19124.197266 19567.007812

728 2022-10-24 19567.769531 19589.125000 19206.324219 19345.572266

729 2022-10-25 19344.964844 20348.412109 19261.447266 20095.857422

Adj Close Volume

725 19172.468750 32459287866

726 19208.189453 16104440957

727 19567.007812 22128794335

728 19345.572266 30202235805

729 20095.857422 47761524910

and check the content

data.shape

(730, 7)

data.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 730 entries, 0 to 729 Data columns (total 7 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Date 730 non-null datetime64[ns] 1 Open 730 non-null float64 2 High 730 non-null float64 3 Low 730 non-null float64 4 Close 730 non-null float64 5 Adj Close 730 non-null float64 6 Volume 730 non-null int64 dtypes: datetime64[ns](1), float64(5), int64(1) memory usage: 40.0 KB

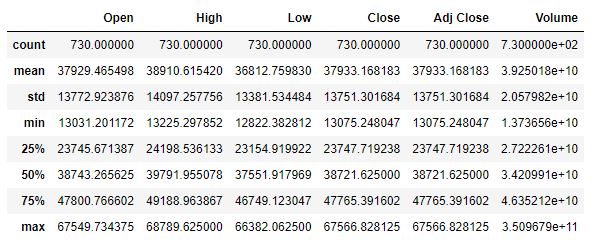

data.describe()

and check for the null/missing values

data.isnull().values.any()

False

Let’s group the Close price by the date

group = data.groupby(‘Date’)

Daily_Price = group[‘Close’].mean()

Daily_Price.tail()

Date 2022-10-21 19172.468750 2022-10-22 19208.189453 2022-10-23 19567.007812 2022-10-24 19345.572266 2022-10-25 20095.857422 Name: Close, dtype: float64

and create the time slots for training, testing and validation purposes

from datetime import date

d0 = date(2022, 1, 1)

d1 = date(2022, 10, 25)

delta = d1 – d0

days_look = delta.days + 1

print(days_look)

298

d0 = date(2022, 8, 25)

d1 = date(2022, 10, 25)

delta = d1 – d0

days_from_train = delta.days + 1

print(days_from_train)

62

d0 = date(2022, 10, 15)

d1 = date(2022, 10, 25)

delta = d1 – d0

days_from_end = delta.days + 1

print(days_from_end)

11

Let’s create the train and test data

df_train= Daily_Price[len(Daily_Price)-days_look-days_from_end:len(Daily_Price)-days_from_train]

df_test= Daily_Price[len(Daily_Price)-days_from_train:]

print(len(df_train), len(df_test))

247 62

Let’s concatenate these data

working_data = [df_train, df_test]

working_data = pd.concat(working_data)

working_data = working_data.reset_index()

working_data[‘Date’] = pd.to_datetime(working_data[‘Date’])

working_data = working_data.set_index(‘Date’)

We are ready to apply sm.tsa.seasonal_decompose

s = sm.tsa.seasonal_decompose(working_data.Close.values,period=61)

and plot the result

trace1 = go.Scatter(x = np.arange(0, len(s.trend), 1),y = s.trend,mode = ‘lines’,name = ‘Trend’,

line = dict(color = (‘rgb(244, 146, 65)’), width = 4))

trace2 = go.Scatter(x = np.arange(0, len(s.seasonal), 1),y = s.seasonal,mode = ‘lines’,name = ‘Seasonal’,

line = dict(color = (‘rgb(66, 244, 155)’), width = 2))

trace3 = go.Scatter(x = np.arange(0, len(s.resid), 1),y = s.resid,mode = ‘lines’,name = ‘Residual’,

line = dict(color = (‘rgb(209, 244, 66)’), width = 2))

trace4 = go.Scatter(x = np.arange(0, len(s.observed), 1),y = s.observed,mode = ‘lines’,name = ‘Observed’,

line = dict(color = (‘rgb(66, 134, 244)’), width = 2))

data = [trace1, trace2, trace3, trace4]

layout = dict(title = ‘Seasonal decomposition’, xaxis = dict(title = ‘Time’), yaxis = dict(title = ‘Price, USD’))

fig = dict(data=data, layout=layout)

py.iplot(fig, filename=’seasonal_decomposition’)

We can plot autocorrelation

plt.figure(figsize=(15,7))

ax = plt.subplot(211)

sm.graphics.tsa.plot_acf(working_data.Close.values.squeeze(), lags=48, ax=ax)

ax = plt.subplot(212)

sm.graphics.tsa.plot_pacf(working_data.Close.values.squeeze(), lags=48, ax=ax)

plt.tight_layout()

plt.show()

Let’s look at the train and test data

df_train = working_data[:-61]

df_test = working_data[-61:]

and call the function

ef create_lookback(dataset, look_back=1):

X, Y = [], []

for i in range(len(dataset) – look_back):

a = dataset[i:(i + look_back), 0]

X.append(a)

Y.append(dataset[i + look_back, 0])

return np.array(X), np.array(Y)

Let’s prepare our data for ML

from sklearn.preprocessing import RobustScaler

training_set = df_train.values

training_set = np.reshape(training_set, (len(training_set), 1))

test_set = df_test.values

test_set = np.reshape(test_set, (len(test_set), 1))

Scale datasets:

scaler = RobustScaler()

training_set = scaler.fit_transform(training_set)

test_set = scaler.transform(test_set)

Create datasets which are suitable for time series forecasting

look_back = 1

X_train, Y_train = create_lookback(training_set, look_back)

X_test, Y_test = create_lookback(test_set, look_back)

# reshape datasets so that they will be ok for the requirements of the LSTM model in Keras

X_train = np.reshape(X_train, (len(X_train), 1, X_train.shape[1]))

X_test = np.reshape(X_test, (len(X_test), 1, X_test.shape[1]))

Let’s create our trained model

Initialize sequential model, add 2 stacked LSTM layers and densely connected output neuron

model = Sequential()

model.add(LSTM(256, return_sequences=True, input_shape=(X_train.shape[1], X_train.shape[2])))

model.add(LSTM(256))

model.add(Dense(1))

Compile and fit the NN model

model.compile(loss=’mean_squared_error’, optimizer=’adam’)

history = model.fit(X_train, Y_train, epochs=100, batch_size=16, shuffle=False,

validation_data=(X_test, Y_test),

callbacks = [EarlyStopping(monitor=’val_loss’, min_delta=5e-5, patience=20, verbose=1)])

Epoch 1/100 16/16 [==============================] - 3s 42ms/step - loss: 0.2524 - val_loss: 0.6315 Epoch 2/100 16/16 [==============================] - 0s 7ms/step - loss: 0.0893 - val_loss: 0.0899 Epoch 3/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0289 - val_loss: 0.0048 Epoch 4/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0079 - val_loss: 0.0016 Epoch 5/100 16/16 [==============================] - 0s 5ms/step - loss: 0.0050 - val_loss: 0.0016 Epoch 6/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0047 - val_loss: 8.0767e-04 Epoch 7/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0046 - val_loss: 8.8796e-04 Epoch 8/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0049 - val_loss: 8.3084e-04 Epoch 9/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0051 - val_loss: 8.0932e-04 Epoch 10/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0061 - val_loss: 8.4507e-04 Epoch 11/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0071 - val_loss: 0.0013 Epoch 12/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0109 - val_loss: 8.1699e-04 Epoch 13/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0133 - val_loss: 0.0031 Epoch 14/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0244 - val_loss: 0.0075 Epoch 15/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0196 - val_loss: 0.0016 Epoch 16/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0299 - val_loss: 0.0226 Epoch 17/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0136 - val_loss: 0.0010 Epoch 18/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0145 - val_loss: 0.0094 Epoch 19/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0084 - val_loss: 0.0010 Epoch 20/100 16/16 [==============================] - 0s 6ms/step - loss: 0.0085 - val_loss: 0.0039

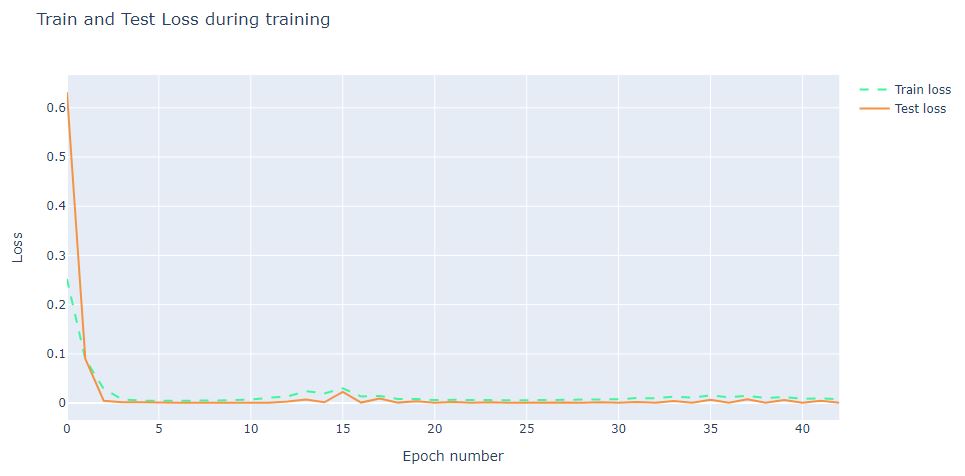

and plot the training process

trace1 = go.Scatter(

x = np.arange(0, len(history.history[‘loss’]), 1),

y = history.history[‘loss’],

mode = ‘lines’,

name = ‘Train loss’,

line = dict(color=(‘rgb(66, 244, 155)’), width=2, dash=’dash’)

)

trace2 = go.Scatter(

x = np.arange(0, len(history.history[‘val_loss’]), 1),

y = history.history[‘val_loss’],

mode = ‘lines’,

name = ‘Test loss’,

line = dict(color=(‘rgb(244, 146, 65)’), width=2)

)

data = [trace1, trace2]

layout = dict(title = ‘Train and Test Loss during training’,

xaxis = dict(title = ‘Epoch number’), yaxis = dict(title = ‘Loss’))

fig = dict(data=data, layout=layout)

py.iplot(fig, filename=’training_process’)

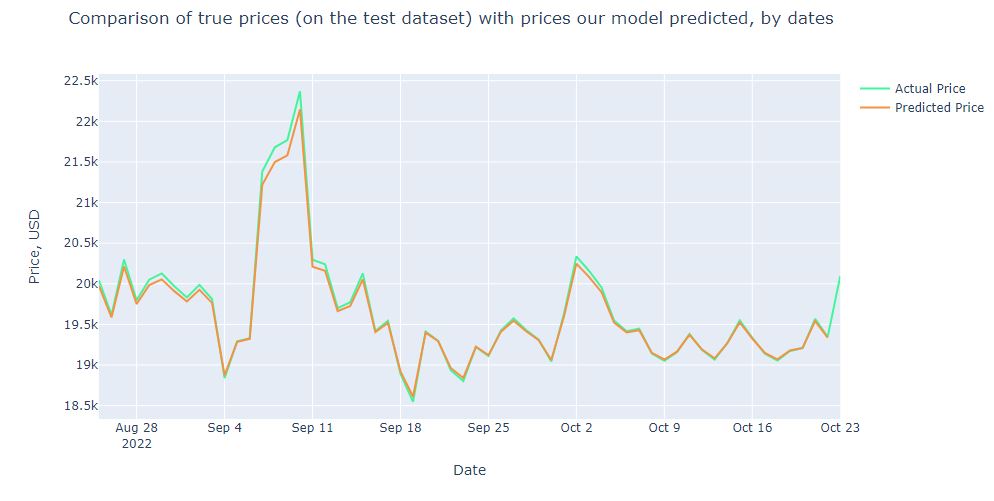

Let’s get predictions and then make some transformations to be able to calculate RMSE properly in USD

prediction = model.predict(X_test)

prediction_inverse = scaler.inverse_transform(prediction.reshape(-1, 1))

Y_test_inverse = scaler.inverse_transform(Y_test.reshape(-1, 1))

prediction2_inverse = np.array(prediction_inverse[:,0][1:])

Y_test2_inverse = np.array(Y_test_inverse[:,0])

2/2 [==============================] - 0s 2ms/step

The resulting plot is

trace1 = go.Scatter(

x = np.arange(0, len(prediction2_inverse), 1),

y = prediction2_inverse,

mode = ‘lines’,

name = ‘Predicted price’,

hoverlabel= dict(namelength=-1),

line = dict(color=(‘rgb(244, 146, 65)’), width=2)

)

trace2 = go.Scatter(

x = np.arange(0, len(Y_test2_inverse), 1),

y = Y_test2_inverse,

mode = ‘lines’,

name = ‘True price’,

line = dict(color=(‘rgb(66, 244, 155)’), width=2)

)

data = [trace1, trace2]

layout = dict(title = ‘Comparison of true prices (on the test dataset) with prices our model predicted’,

xaxis = dict(title = ‘Day number’), yaxis = dict(title = ‘Price, USD’))

fig = dict(data=data, layout=layout)

py.iplot(fig, filename=’results_demonstrating0′)

The RMSE is

RMSE = sqrt(mean_squared_error(Y_test2_inverse1, prediction2_inverse))

print(‘Test RMSE: %.3f’ % RMSE)

Test RMSE: 63.566

Let’s plot our BTC prices against the dates

Summary

- We trained the 2-layers Long Short Term Memory Neural Network using Bitcoin Historical Data.

- The trained LSTM model can be used to predict future price movements of bitcoin.

- RMSE ~ $64, with the mean price of $20k (Oct ’22), which means the prediction error ~0.3%.

- The model performance is excellent, with an error of only tens of USD.

Explore More

Bitcoin price forecasting with deep learning algorithms

Cryptocurrency Price Prediction with Machine Learning

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment