- This work aims to solve the problem of Markowitz portfolio optimization for a one-year horizon investment, through the pairs trading cointegrated strategy.

- Specifically, we’ll look at market-neutral trading strategies (MNTS). The goal of MNTS is to generate returns that are independent of market swings and achieve a zero beta against its relevant market index.

- Market-neutral alpha strategy is an investment method designed to provide significant alpha but little or no beta. Here, beta refers to the correlation of an investment with the usual swings in a broad stock market index such as the S&P 500, while alpha refers to the excess return beyond the market return earned through active trading.

- Statistical arbitrage (SA) is a classical example of MNTS. SA involves exploiting the price discrepancies of financial instruments that are highly correlated.

- We’ll analyze the relationship between market efficiency and a SA technique based on portfolio efficient frontiers combined with popular technical indicators, the Z-score analysis, and portfolio backtesting in 2023.

- We’ll examine asset allocation across a number of sectors including technology, financial services, and industrials.

- To measure the return of the portfolio, this article uses the annualized return of the portfolio.

- In the sequel, our MNTS consists of the following steps: (1) evaluate our financial goals, time horizon, and resources to achieve your goals; (2) study the financial markets and investment tools, including stocks, bonds, and derivatives, to know the instruments to use for our strategy; (3) formulate our strategy (which could be statistical arbitrage, merger arbitrage, pair trading, or any other) and backtest it.

Table of Contents

- Credits

- Correlations with AAPL

- AAPL Stat-Arb Backtesting

- Portfolio Efficient Frontiers

- AAPL Technical Indicators

- Cointegrated Pairs of Stocks

- Z-Score vs Trading Signals

- Conclusions

- Explore More

Credits

- Naive Statistical Arbitrage Trading Analysis

- Analysis of a Naive Statistical Arbitrage for Trading

- Momentum and Reversion Trading Signals Analysis

- adamd1985

Correlations with AAPL

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

- Copying the utility functions analysis_utils.py to YOURPATH

- Importing the key libraries and reading the input stock data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import warnings

warnings.filterwarnings("ignore")

import yfinance as yf

from analysis_utils import calculate_profit, load_ticker_prices_ts_df, plot_strategy, load_ticker_ts_df

START_DATE = "2020-01-01"

END_DATE = "2023-12-24"

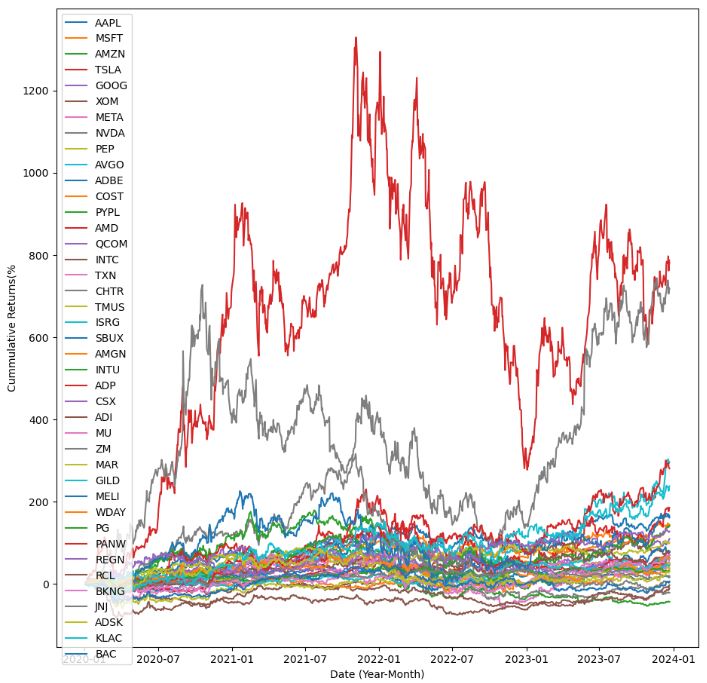

tickers = ["AAPL", "MSFT", "AMZN", "TSLA", "GOOG", "XOM", "META", "NVDA", "PEP", "AVGO", "ADBE", "COST", "PYPL", "AMD", "QCOM", "INTC", "TXN", "CHTR", "TMUS", "ISRG", "SBUX", "AMGN", "INTU", "ADP", "CSX", "ADI", "MU", "ZM", "MAR", "GILD", "MELI", "WDAY", "PG", "PANW", "REGN", "RCL", "BKNG", "JNJ", "ADSK", "KLAC", "BAC"]

tickers_df = load_ticker_prices_ts_df(tickers, START_DATE, END_DATE)

tickers_rets_df = tickers_df.dropna(axis=1).pct_change().dropna() # first % is NaN

# 1+ to allow the cumulative product of returns over time, and -1 to remove it at the end.

tickers_rets_df = (1 + tickers_rets_df).cumprod() - 1

plt.figure(figsize=(11, 11))

for ticker in tickers_rets_df.columns:

plt.plot(tickers_rets_df.index, tickers_rets_df[ticker] * 100.0, label=ticker)

plt.xlabel("Date (Year-Month)")

plt.ylabel("Cummulative Returns(%")

plt.legend()

plt.show()

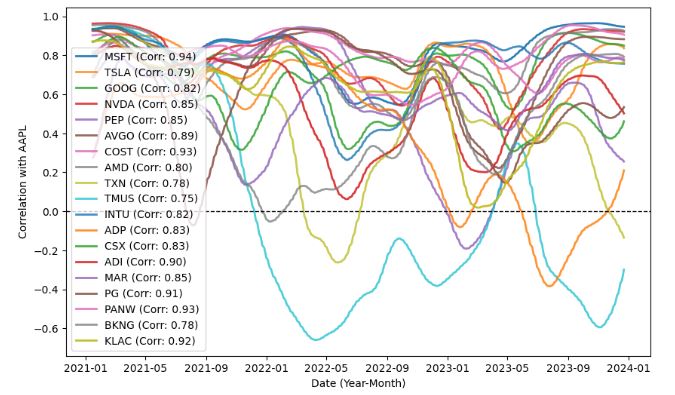

- Following the Macroaxis trading ideas, let’s examine the Apple stock correlation with its peers.

- Selecting peers with correlation > 0.75

TARGET = "AAPL"

MA_WINDOW = 24

ARB_WINDOW = MA_WINDOW * 10

plt.figure(figsize=(10, 6))

corr_ticks = []

LEADS = []

for ticker in tickers:

if ticker == TARGET:

continue

correlation = tickers_df[ticker].corr(tickers_df[TARGET])

if abs(correlation) < 0.75:

continue

LEADS.append(ticker)

corr_ts = tickers_df[ticker].rolling(ARB_WINDOW).corr(tickers_df[TARGET])

plt.plot(

tickers_df.index,

corr_ts.rolling(MA_WINDOW).mean(),

label=f"{ticker} (Corr: {correlation:.2f})",

alpha=correlation,

linewidth=2,

)

corr_ticks.append(ticker)

plt.axhline(y=0, color="k", linestyle="--", linewidth=1)

plt.xlabel("Date (Year-Month)")

plt.ylabel("Correlation with AAPL")

plt.legend()

plt.show()

- It is clear that some stocks oscillate between uncorrelated and correlated in ’23.

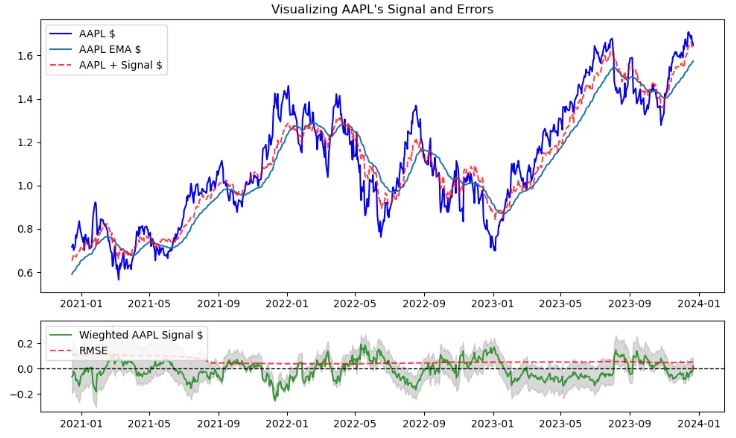

- Calculating EMA and the covariance ratios between stock pairs

arb_df = tickers_rets_df.copy()

arb_df["price"] = tickers_df[TARGET]

arb_df[f"ema_{TARGET}"] = arb_df[TARGET].ewm(MA_WINDOW).mean()

arb_df[f"ema_d_{TARGET}"] = arb_df[TARGET] - arb_df[f"ema_{TARGET}"]

arb_df[f"ema_d_{TARGET}"].fillna(0, inplace=True)

for ticker in LEADS:

arb_df[f"ema_{ticker}"] = arb_df[ticker].ewm(MA_WINDOW).mean()

arb_df[f"ema_d_{ticker}"] = arb_df[ticker] - arb_df[f"ema_{ticker}"]

arb_df[f"ema_d_{ticker}"].fillna(0, inplace=True)

arb_df[f"{ticker}_corr"] = (

arb_df[f"ema_d_{ticker}"].rolling(ARB_WINDOW).corr(arb_df[f"ema_d_{TARGET}"])

)

arb_df[f"{ticker}_covr"] = (

arb_df[[f"ema_d_{ticker}", f"ema_d_{TARGET}"]]

.rolling(ARB_WINDOW)

.cov(numeric_only=True)

.groupby(level=0, axis=0, dropna=True) # Cov returns pairwise!

.apply(lambda x: x.iloc[0, 1] / x.iloc[0, 0])

)

arb_df[f"{ticker}_emas_d_prj"] = (

arb_df[f"ema_d_{ticker}"] * arb_df[f"{ticker}_covr"]

)

arb_df[f"{ticker}_emas_act"] = (

arb_df[f"{ticker}_emas_d_prj"] - arb_df[f"ema_d_{TARGET}"]

)

arb_df.filter(regex=f"(_emas_d_prj|_corr|_covr)$").dropna().iloc[ARB_WINDOW:]

- Calculating the AAPL_signal weights based on absolute values of correlations

ts = 0

delta_projected = 0

weights=0

for ticker in LEADS:

corr_abs = abs(arb_df[f"{ticker}_corr"].fillna(0))

weights += corr_abs

arb_df[f"{ticker}_emas_act_w"] = arb_df[f"{ticker}_emas_act"].fillna(0) * corr_abs

delta_projected += arb_df[f"{ticker}_emas_act_w"]

weights = weights.replace(0, 1)

arb_df[f"{TARGET}_signal"] = delta_projected / weights

arb_df[f"{TARGET}_signal"].iloc[ARB_WINDOW:]

- Calculating errors and the signals confidence intervals at 95%

errors = (

arb_df[f"ema_{TARGET}"] + arb_df[f"ema_d_{TARGET}"] + arb_df[f"{TARGET}_signal"]

) - (arb_df[f"ema_{TARGET}"].shift(-1))

arb_df["rmse"] = np.sqrt((errors**2).rolling(ARB_WINDOW).mean()).fillna(0)

me = errors.rolling(ARB_WINDOW).mean().fillna(0)

e_std = errors.rolling(ARB_WINDOW).std().fillna(0)

ci = (me - 1.96 * e_std, me + 1.96 * e_std)

arb_df["ci_lower"] = arb_df[f"{TARGET}_signal"].fillna(0) + ci[0]

arb_df["ci_upper"] = arb_df[f"{TARGET}_signal"].fillna(0) + ci[1]

arb_df["ci_spread"] = arb_df["ci_upper"] - arb_df["ci_lower"]

arb_df.fillna(0, inplace=True)

arb_df[["ci_lower", "ci_upper"]].iloc[ARB_WINDOW:].tail(10)

- Plotting the AAPL’s signal and errors

fig, axes = plt.subplots(2, 1, gridspec_kw={"height_ratios": (3, 1)}, figsize=(10, 6))

axes[0].set_title(f"Visualizing {TARGET}'s Signal and Errors")

axes[0].plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df[TARGET].iloc[ARB_WINDOW:],

label=f"{TARGET} $",

alpha=1,

color="b",

)

axes[0].plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df[f"ema_{TARGET}"].iloc[ARB_WINDOW:],

label=f"{TARGET} EMA $",

alpha=1,

)

axes[0].plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df[f"{TARGET}_signal"].iloc[ARB_WINDOW:].fillna(0)

+ arb_df[TARGET].iloc[ARB_WINDOW:],

label=f"{TARGET} + Signal $",

alpha=0.75,

linestyle="--",

color="r",

)

axes[0].legend()

axes[1].plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df[f"{TARGET}_signal"].iloc[ARB_WINDOW:],

label=f"Wieghted {TARGET} Signal $",

alpha=0.75,

color="g",

)

axes[1].plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df["rmse"].iloc[ARB_WINDOW:],

label="RMSE",

alpha=0.75,

linestyle="--",

color="r",

)

axes[1].fill_between(

arb_df.iloc[ARB_WINDOW:].index,

arb_df["ci_lower"].iloc[ARB_WINDOW:],

arb_df["ci_upper"].iloc[ARB_WINDOW:],

color="gray",

alpha=0.3,

)

axes[1].axhline(0, color="black", linestyle="--", linewidth=1)

axes[1].legend()

plt.tight_layout()

plt.show()

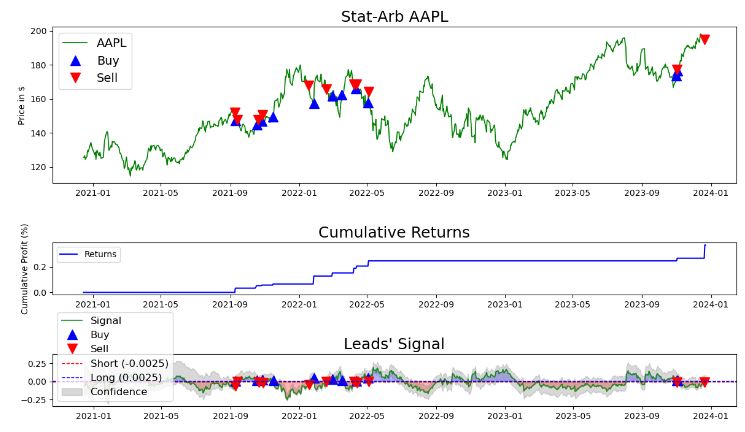

AAPL Stat-Arb Backtesting

- Let’s perform AAPL backtesting by acting upon the above trading signals with the following simulation parameters

LONG_THRESHOLD = 0.0025

SHORT_THRESHOLD = -0.0025

CONF_SPREAD_THRESHOLD = 0.15

MAX_SHARES = 1

arb_df["orders"] = 0

signals = arb_df[f"{TARGET}_signal"]

prev_signals = signals.shift(-1)

add_long_cond = (signals > LONG_THRESHOLD) & (prev_signals <= LONG_THRESHOLD) & (signals < arb_df["ci_upper"]) & (signals > arb_df["ci_lower"]) & (arb_df["ci_spread"] < CONF_SPREAD_THRESHOLD)

add_short_cond = (signals < SHORT_THRESHOLD) & (prev_signals >= SHORT_THRESHOLD) & (signals < arb_df["ci_upper"]) & (signals > arb_df["ci_lower"]) & (arb_df["ci_spread"] < CONF_SPREAD_THRESHOLD)

arb_df.loc[add_long_cond, "orders"] += MAX_SHARES

arb_df.loc[add_short_cond, "orders"] -= MAX_SHARES

arb_df["orders"].fillna(0, inplace=True)

arb_df.loc[arb_df["orders"] != 0, "orders"].tail(10)

2022-03-18 00:00:00 1

2022-04-08 00:00:00 -1

2022-04-12 00:00:00 1

2022-04-13 00:00:00 -1

2022-05-03 00:00:00 1

2022-05-04 00:00:00 -1

2023-11-01 00:00:00 1

2023-11-02 00:00:00 -1

2023-11-03 00:00:00 1

2023-12-21 00:00:00 -1

Name: orders, dtype: int64

signal_changes_df = arb_df.loc[(add_long_cond | add_short_cond), ["price", "orders", f"{TARGET}_signal"]]

signal_changes_df["holdings"] = signal_changes_df["orders"].cumsum()

signal_changes_df["stat_chng"] = np.sign(signal_changes_df["orders"].shift(1)) != np.sign(signal_changes_df["orders"])

prev_holdings = signal_changes_df["holdings"].shift(1)

signal_changes_df["price_open"] = signal_changes_df["price"].shift(1)

signal_changes_df["cost_open_avg"] = (signal_changes_df.loc[signal_changes_df["stat_chng"] == False, "price_open"].shift(1) + signal_changes_df.loc[signal_changes_df["stat_chng"]== False, "price_open"]) / 2

signal_changes_df["cost_open_avg"].fillna(signal_changes_df["price_open"], inplace=True)

signal_changes_df["price_close"] = signal_changes_df["price"]

signal_changes_df["price_close"].iloc[0] = np.nan # First signal shouldn't have a closing price

signal_changes_df["pnl"] = (signal_changes_df.loc[signal_changes_df["stat_chng"], "price_close"] - signal_changes_df.loc[signal_changes_df["stat_chng"], "cost_open_avg"]) * np.sign(signal_changes_df["holdings"].shift(1))

signal_changes_df["pnl_rets"] = signal_changes_df["pnl"] / signal_changes_df["cost_open_avg"].abs()

signal_changes_df.fillna(0, inplace=True)

arb_df = pd.concat([arb_df, signal_changes_df[["pnl", "pnl_rets", "holdings"]]], axis=1).drop_duplicates(keep='last')

#signal_changes_df.tail(10)

- Plotting the AAPL simulated trades and cumulative returns

plt.figure(figsize=(12, 7))

fig, (ax1, ax2, ax3) = plt.subplots(

3, 1, gridspec_kw={"height_ratios": (3, 1, 1)}, figsize=(12, 7)

)

ax1.plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df["price"].iloc[ARB_WINDOW:],

color="g",

lw=1.25,

label=f"{TARGET}",

)

ax1.plot(

arb_df.loc[add_long_cond].index,

arb_df.loc[add_long_cond, "price"],

"^",

markersize=12,

color="blue",

label="Buy",

)

ax1.plot(

arb_df.loc[add_short_cond].index,

arb_df.loc[add_short_cond, "price"],

"v",

markersize=12,

color="red",

label="Sell",

)

ax1.set_ylabel("Price in $")

ax1.legend(loc="upper left", fontsize=14)

ax1.set_title(f"Stat-Arb {TARGET}", fontsize=18)

ax2.plot(

arb_df["pnl"].iloc[ARB_WINDOW:].index, arb_df["pnl_rets"].iloc[ARB_WINDOW:].fillna(0).cumsum(), color="b", label="Returns"

)

ax2.set_ylabel("Cumulative Profit (%)")

ax2.legend(loc="upper left", fontsize=10)

ax2.set_title(f"Cumulative Returns", fontsize=18)

ax3.plot(

arb_df.iloc[ARB_WINDOW:].index,

arb_df[f"{TARGET}_signal"].iloc[ARB_WINDOW:],

label=f"Signal",

alpha=0.75,

color="g",

)

ax3.plot(

arb_df.loc[add_long_cond].index,

arb_df.loc[add_long_cond, f"{TARGET}_signal"],

"^",

markersize=12,

color="blue",

label="Buy",

)

ax3.plot(

arb_df.loc[add_short_cond].index,

arb_df.loc[add_short_cond, f"{TARGET}_signal"],

"v",

markersize=12,

color="red",

label="Sell",

)

ax3.axhline(0, color="black", linestyle="--", linewidth=1)

ax3.axhline(SHORT_THRESHOLD, color="r", linestyle="--", label=f"Short ({SHORT_THRESHOLD})",linewidth=1)

ax3.axhline(LONG_THRESHOLD, color="b", linestyle="--", label=f"Long ({LONG_THRESHOLD})",linewidth=1)

ax3.fill_between(arb_df.index, arb_df[f"{TARGET}_signal"], SHORT_THRESHOLD, where=(arb_df[f"{TARGET}_signal"] < SHORT_THRESHOLD), interpolate=True, color='red', alpha=0.3)

ax3.fill_between(arb_df.index, arb_df[f"{TARGET}_signal"], LONG_THRESHOLD, where=(arb_df[f"{TARGET}_signal"] > LONG_THRESHOLD), interpolate=True, color='blue', alpha=0.3)

ax3.fill_between(

arb_df.iloc[ARB_WINDOW:].index,

arb_df["ci_lower"].iloc[ARB_WINDOW:],

arb_df["ci_upper"].iloc[ARB_WINDOW:],

color="gray",

alpha=0.3,

label=f"Confidence"

)

ax3.legend(loc="lower left", fontsize=12)

ax3.set_title(f"Leads' Signal", fontsize=18)

plt.tight_layout()

plt.show()

- It appears that simulated trading yields the cumulative return return of 40%.

Portfolio Efficient Frontiers

- Let’s discuss the Efficient Frontier, a core concept in Harry Markowitz’s Modern Portfolio Theory (MPT). MPT is used in quantitative finance to build optimal portfolios that offer the highest expected return for a given level of risk.

- Importing the key libraries and selecting the portfolio of interest

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

from analysis_utils import calculate_profit, load_ticker_prices_ts_df, plot_strategy, load_ticker_ts_df

tickers = ["META", "AAPL","NVDA","TSLA","BAC","JNJ"]

START_DATE = "2020-01-01"

END_DATE = "2022-12-31"

tickers_orig_df = load_ticker_prices_ts_df(tickers, START_DATE, END_DATE)

tickers_df = tickers_orig_df.dropna(axis=1).pct_change().dropna() # first % is NaN

# 1+ to allow the cumulative product of returns over time, and -1 to remove it at the end.

tickers_df = (1 + tickers_df).cumprod() - 1

plt.figure(figsize=(10, 6))

for ticker in tickers_df.columns:

plt.plot(tickers_df.index, tickers_df[ticker] * 100.0, label=ticker)

plt.xlabel("Date (Year-Month)")

plt.ylabel("Cumulative Returns(%)")

plt.legend()

plt.show()

![Cumulative Returns(%) of selected stocks: tickers = ["META", "AAPL","NVDA","TSLA","BAC","JNJ"]](https://newdigitals.org/wp-content/uploads/2023/12/eff_portfolio-1.jpg?w=653)

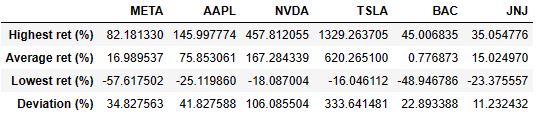

- Calculating the following descriptive statistics of cumulative returns

mean_returns = tickers_df.mean()

highest_returns = tickers_df.max()

lowest_returns = tickers_df.min()

std_deviation = tickers_df.std()

summary_table = pd.DataFrame(

{

"Highest ret (%)": highest_returns * 100.0,

"Average ret (%)": mean_returns * 100.0,

"Lowest ret (%)": lowest_returns * 100.0,

"Deviation (%)": std_deviation * 100.0,

}

)

summary_table.transpose()

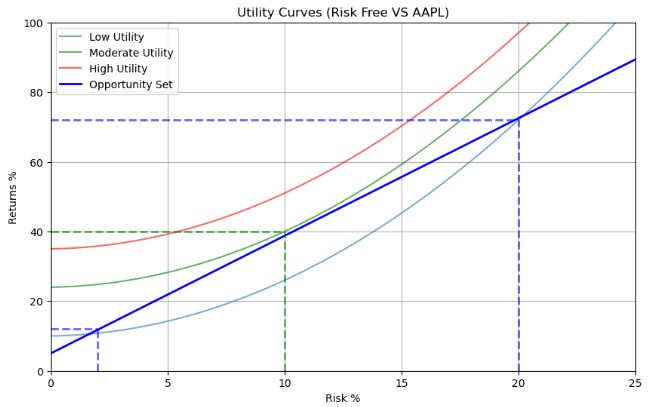

- Experimenting with the investors choices of risk/reward, through indifference curves.

def utility_fn(x, a=0.15, b=0.1, c=1):

return a * x**2 + b * x + c

plt.figure(figsize=(10, 6))

x_values_1 = np.linspace(0, 40, 100)

y_values_1 = utility_fn(x_values_1, c=10)

plt.plot(x_values_1, y_values_1, label="Low Utility", alpha=0.6)

x_values_2 = np.linspace(0, 35, 100)

y_values_2 = utility_fn(x_values_2, c=24)

plt.plot(x_values_2, y_values_2, label="Moderate Utility", color="g", alpha=0.6)

x_values_3 = np.linspace(0, 30, 100)

y_values_3 = utility_fn(x_values_3, c=35)

plt.plot(x_values_3, y_values_3, label="High Utility", color="r", alpha=0.6)

plt.plot([0, 40], [5, 140], label="Opportunity Set", color="b", linewidth=2)

plt.plot([2, 2], [0, 12], linestyle="--", color="b", alpha=0.6, linewidth=2)

plt.plot([0, 2], [12, 12], linestyle="--", color="b", alpha=0.6, linewidth=2)

plt.plot([10, 10], [0, 40], linestyle="--", color="g", alpha=0.6, linewidth=2)

plt.plot([0, 10], [40, 40], linestyle="--", color="g", alpha=0.6, linewidth=2)

plt.plot([20, 20], [0, 72], linestyle="--", color="b", alpha=0.6, linewidth=2)

plt.plot([0, 20], [72, 72], linestyle="--", color="b", alpha=0.6, linewidth=2)

plt.xlabel("Risk %")

plt.ylabel("Returns %")

plt.title("Utility Curves (Risk Free VS AAPL)")

plt.legend()

plt.grid()

plt.xlim(0, 25)

plt.ylim(0, 100)

plt.show()

- The optimal choice is when the opportunity set line is tangent to a curve, in our case the

moderateutility curve, giving us 70% returns for 20% risk. - Computing the annual covariance matrix and returns of our stocks

TRADING_DAYS_IN_YEAR = 252

tickers_df = tickers_orig_df.dropna(axis=1).pct_change().dropna()

rets = ((1 + tickers_df).prod() ** (TRADING_DAYS_IN_YEAR / len(tickers_df))) - 1

cov_matrix = tickers_df.cov() * TRADING_DAYS_IN_YEAR

print(cov_matrix)

META AAPL NVDA TSLA BAC JNJ

META 0.237390 0.113085 0.164167 0.130005 0.074333 0.030630

AAPL 0.113085 0.136407 0.147414 0.138480 0.073008 0.038126

NVDA 0.164167 0.147414 0.313340 0.221768 0.093156 0.037974

TSLA 0.130005 0.138480 0.221768 0.521113 0.085079 0.021494

BAC 0.074333 0.073008 0.093156 0.085079 0.171712 0.042495

JNJ 0.030630 0.038126 0.037974 0.021494 0.042495 0.047665

print(round(rets*100,2))

META -16.93

AAPL 20.91

NVDA 34.77

TSLA 62.65

BAC -0.16

JNJ 9.37

dtype: float64

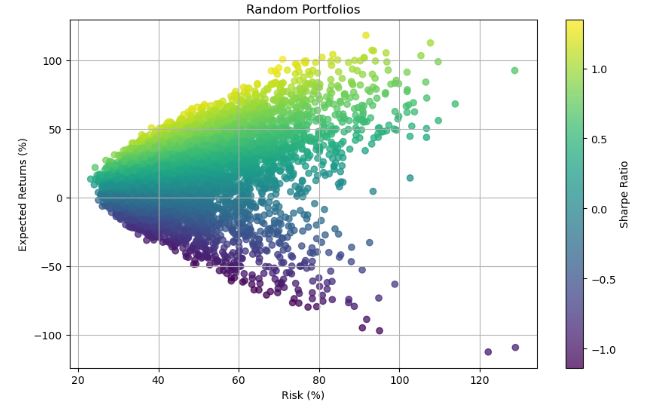

- A portfolio is a weighted collection of assets. Let’s create portfolios with randomly selected weights below

RISK_FREE_RATE = 0.05

MAX_PORTS = 10000

MAX_WEIGHT = 1.05

def port_generator(rets, cov_matrix):

port_rets = []

port_risks = []

port_sharpes = []

port_weights = []

for _ in range(MAX_PORTS):

# weights = np.random.random(len(rets))

weights = np.random.uniform(-MAX_WEIGHT, MAX_WEIGHT, len(rets))

weights /= np.sum(weights) # Normalize weights to 1

if any(weights > MAX_WEIGHT):

continue

port_weights.append(weights)

port_ret = np.dot(weights, rets)

port_rets.append(port_ret)

port_risk = np.sqrt(weights.T @ cov_matrix @ weights)

port_risks.append(port_risk)

port_sharpe = (port_ret - RISK_FREE_RATE) / port_risk

port_sharpes.append(port_sharpe)

port_rets = np.array(port_rets)

port_risks = np.array(port_risks)

plt.scatter(

port_risks * 100.0,

port_rets * 100.0,

c=port_sharpes,

cmap="viridis",

alpha=0.75,

)

plt.xlabel("Risk (%)")

plt.ylabel("Expected Returns (%)")

plt.colorbar(label="Sharpe Ratio")

plt.grid()

return port_risks, port_rets, port_sharpes

plt.figure(figsize=(10, 6))

plt.title("Random Portfolios")

port_risks, port_rets, port_sharpes=port_generator(rets, cov_matrix)

plt.show()

- Checking the portfolio risks

print(port_risks)

[0.33830614 0.31844794 0.515034 ... 0.62395826 0.51434099 0.41154064]

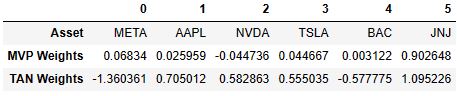

- Comparing minimum variance vs tangency portfolios

# Equal-weighted portfolio useful for matrix operations

equal_weights = np.ones(len(rets))

rets = ((1 + tickers_df).prod() ** (TRADING_DAYS_IN_YEAR / len(tickers_df))) - 1

cov_matrix = tickers_df.cov() * TRADING_DAYS_IN_YEAR

# Min variance weights

inv_cov_matrix = np.linalg.pinv(cov_matrix)

min_risk_vect = equal_weights @ inv_cov_matrix

expect_ret_vect = inv_cov_matrix @ rets

# Minimum variance portfolio

# Weights are normalized to sum to 1, and risk to std deviation.

mvp_weights = min_risk_vect / np.sum(min_risk_vect)

mvp_ret = mvp_weights @ rets

mvp_risk = np.sqrt(mvp_weights.T @ cov_matrix @ mvp_weights)

# Tangency portfolio

tan_weights = expect_ret_vect / np.sum(expect_ret_vect)

tan_ret = tan_weights @ rets

tan_risk = np.sqrt(tan_weights.T @ cov_matrix @ tan_weights)

summary_data = {

"Asset": tickers,

"MVP Weights": mvp_weights,

"TAN Weights": tan_weights,

}

print(f"mvp_ret: {mvp_ret*100:0.02f}%, mvp_risk {mvp_risk*100:0.02f}%")

print(f"tan_ret: {tan_ret*100:0.02f}%, tan_risk {tan_risk*100:0.02f}%")

summary_df = pd.DataFrame(summary_data)

summary_df.T

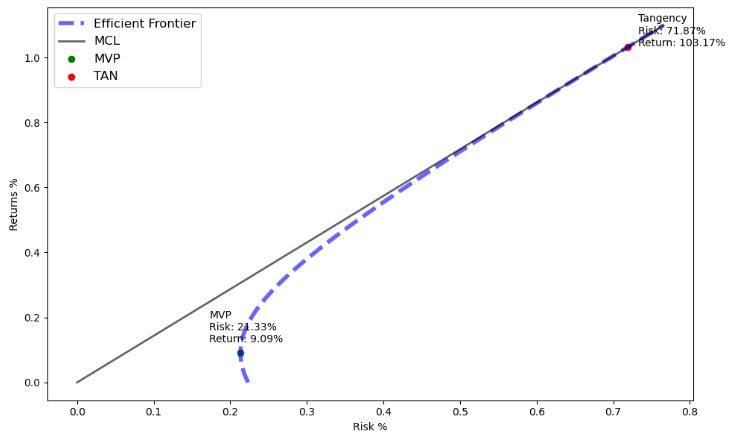

mvp_ret: 9.09%, mvp_risk 21.33%

tan_ret: 103.17%, tan_risk 71.87%

- Adding the Market Capital Line (MCL) to represent the market’s risk and returns at the time of this analysis, any portfolio under this line might be overpriced and suboptimal, any higher might be underpriced for its risk. When plotted against the expected returns, the CML will intercept the efficient frontier at the TAN portfolio, and this intercept is the most optimal market portfolio:

MAX_RETS = 1.1

TEN_BASIS_POINTS = 0.0001 * 10

c = np.sum(equal_weights * min_risk_vect) # Constant term

b = np.sum(rets * min_risk_vect) # Linear term

a = np.sum(rets * expect_ret_vect) # Quadratic term

utility_func = (a * c) + (-(b**2)) # U(X) to penalize risk

# The frontier curve & MCL, scaled by utility function

exp_rets = np.arange(0, MAX_RETS, TEN_BASIS_POINTS)

ports_risk_frontier = np.sqrt(

((c * (exp_rets**2)) - (2 * b * exp_rets) + a) / utility_func

)

mcl_vector = exp_rets * (1 / np.sqrt(a))

plt.figure(figsize=(10, 6))

plt.plot(

ports_risk_frontier,

exp_rets,

linestyle="--",

color="blue",

label="Efficient Frontier",

linewidth=4,

alpha=0.6,

)

plt.plot(

mcl_vector,

exp_rets,

label="MCL",

linewidth=2,

alpha=0.6,

color="black",

)

plt.scatter(mvp_risk, mvp_ret, color="green", label="MVP")

plt.annotate(

f"MVP\nRisk: {mvp_risk*100:.2f}%\nReturn: {mvp_ret*100:.2f}%",

(mvp_risk, mvp_ret),

textcoords="offset points",

xytext=(-30, 10),

)

plt.scatter(tan_risk, tan_ret, color="red", label="TAN")

plt.annotate(

f"Tangency\nRisk: {tan_risk*100:.2f}%\nReturn: {tan_ret*100:.2f}%",

(tan_risk, tan_ret),

textcoords="offset points",

xytext=(10, 1),

)

plt.legend(loc="upper left", fontsize=12)

plt.xlabel("Risk %")

plt.ylabel("Returns %")

plt.tight_layout()

plt.show()

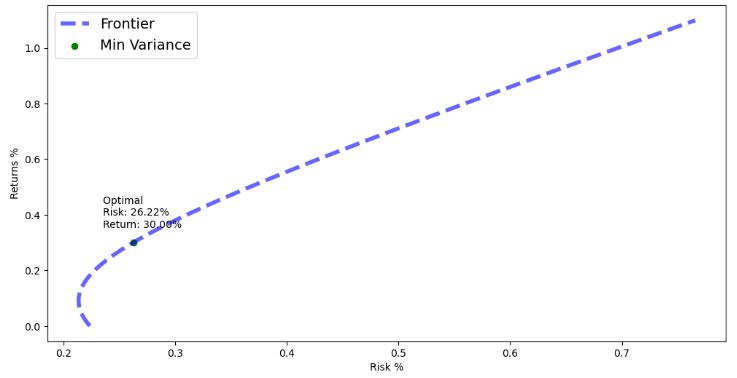

- Finding the min variance risk for the given return of 30%

TARGET_RET = 0.3

pt_port = None

opt_risk = None

opt_ret = None

mvp_weights = (a - (b * TARGET_RET)) / utility_func

tan_weights = ((c * TARGET_RET) - b) / utility_func

opt_port_weights = (mvp_weights * min_risk_vect) + (tan_weights * expect_ret_vect)

opt_ret = np.sum(opt_port_weights * rets)

opt_risk = np.sqrt(((c * (opt_ret**2)) - (2 * b * opt_ret) + a) / utility_func)

plt.figure(figsize=(12, 6))

plt.plot(

ports_risk_frontier,

exp_rets,

linestyle="--",

color="blue",

label="Frontier",

linewidth=4,

alpha=0.6,

)

plt.scatter(opt_risk, opt_ret, color="green", label="Min Variance")

plt.annotate(

f"Optimal \nRisk: {opt_risk*100:.2f}%\nReturn: {opt_ret*100:.2f}%",

(opt_risk, opt_ret),

textcoords="offset points",

xytext=(-30, 15),

)

plt.legend(loc="upper left", fontsize=14)

plt.xlabel("Risk %")

plt.ylabel("Returns %")

plt.tight_layout

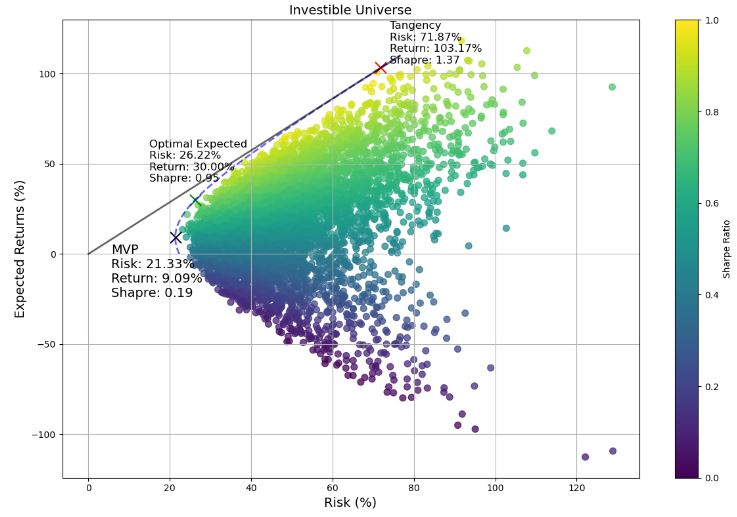

- Final output: the MVP, tangency points, the optimal expected risk, MCL, and the efficient frontier

# Add portfolios sharpe

opt_sharpe = (opt_ret - RISK_FREE_RATE) / opt_risk

mvp_sharpe = (mvp_ret - RISK_FREE_RATE) / mvp_risk

tan_sharpe = (tan_ret - RISK_FREE_RATE) / tan_risk

plt.figure(figsize=(12, 8)) # Increase figure size

plt.title("Investible Universe",fontsize=14)

plt.scatter(

port_risks * 100.0,

port_rets * 100.0,

c=port_sharpes,

cmap="viridis",

alpha=0.75,

s=50, # Adjust the size of the scatter points

)

plt.plot(

ports_risk_frontier * 100,

exp_rets * 100,

linestyle="--",

color="blue",

label="Frontier",

linewidth=2,

alpha=0.6,

)

# Adjust the size of the optimal point

plt.scatter(

opt_risk * 100,

opt_ret * 100,

color="green",

marker="x",

s=150,

label="Optimal Expected Returns",

)

plt.annotate(

f"Optimal Expected \nRisk: {opt_risk*100:.2f}%\nReturn: {opt_ret*100:.2f}%\nShapre: {opt_sharpe:.2f}",

(opt_risk * 100, opt_ret * 100),

textcoords="offset points",

xytext=(-50, 20), # Adjust the annotation position

fontsize=12, # Adjust the font size

)

plt.plot(

mcl_vector * 100,

exp_rets * 100,

label="MCL",

linewidth=2,

alpha=0.6,

color="black",

)

# Adjust the size and position of the MVP point

plt.scatter(

mvp_risk * 100,

mvp_ret * 100,

color="Black",

label="MVP",

marker="x",

s=150,

)

plt.annotate(

f"MVP\nRisk: {mvp_risk*100:.2f}%\nReturn: {mvp_ret*100:.2f}%\nShapre: {mvp_sharpe:.2f}",

(mvp_risk * 100, mvp_ret * 100),

textcoords="offset points",

xytext=(-70, -65),

fontsize=14,

)

# Adjust the size and position of the Tangency point

plt.scatter(

tan_risk * 100,

tan_ret * 100,

color="red",

label="TAN",

marker="x",

s=150,

)

plt.annotate(

f"Tangency\nRisk: {tan_risk*100:.2f}%\nReturn: {tan_ret*100:.2f}%\nShapre: {tan_sharpe:.2f}",

(tan_risk * 100, tan_ret * 100),

textcoords="offset points",

xytext=(10, 5),

fontsize=12,

)

plt.xlabel("Risk (%)",fontsize=14)

plt.ylabel("Expected Returns (%)",fontsize=14)

plt.colorbar(label="Sharpe Ratio")

plt.grid()

plt.tight_layout()

plt.show()

AAPL Technical Indicators

- Let’s compare the aforementioned findings to the results of technical analysis for AAPL in ’23.

- Consider the most popular trading strategies such as double SMA, naive momentum, mean reversion, APO, EMA, MACD, and RSI.

- Importing the key libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

from analysis_utils1 import calculate_profit, load_ticker_ts_df, plot_strategy

- Introducing the double SMA signals

APO_FAST_WINDOW=5

def double_simple_moving_average_signals(ticker_ts_df, short_window=5, long_window=30):

"""

Generate trading signals based on a double simple moving average (SMA) strategy.

Parameters:

- aapl_ts_df (pandas.DataFrame): A DataFrame containing historical stock data.

- short_window (int): The window size for the short-term SMA.

- long_window (int): The window size for the long-term SMA.

Returns:

- signals (pandas.DataFrame): A DataFrame containing the trading signals.

"""

signals = pd.DataFrame(index=ticker_ts_df.index)

signals['signal'] = 0.0

signals['short_mavg'] = ticker_ts_df['Close'].rolling(window=short_window,

min_periods=APO_FAST_WINDOW,

center=False).mean()

signals['long_mavg'] = ticker_ts_df['Close'].rolling(window=long_window,

min_periods=APO_FAST_WINDOW,

center=False).mean()

# Generate signal when SMAs cross

signals['signal'] = np.where(

signals['short_mavg'] > signals['long_mavg'], 1, 0)

signals['orders'] = signals['signal'].diff()

signals.loc[signals['orders'] == 0, 'orders'] = None

return signals

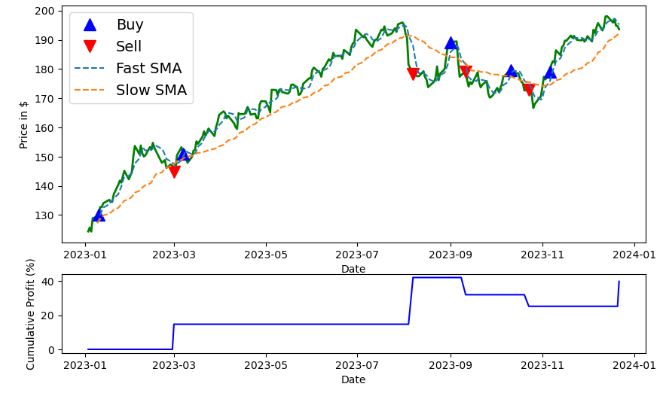

- Plotting double SMA trading signals and cumulative returns for AAPL in ’23

aapl_ts_df = load_ticker_ts_df('AAPL',

start_date='2023-01-01',

end_date='2023-12-24')

signal_df = double_simple_moving_average_signals(aapl_ts_df, 5, 30)

profit_series = calculate_profit(signal_df, aapl_ts_df["Adj Close"])

ax1, ax2 = plot_strategy(aapl_ts_df["Adj Close"], signal_df, profit_series)

# Add short and long moving averages

ax1.plot(signal_df.index, signal_df['short_mavg'],

linestyle='--', label='Fast SMA')

ax1.plot(signal_df.index, signal_df['long_mavg'],

linestyle='--', label='Slow SMA')

ax1.legend(loc='upper left', fontsize=14)

plt.show()

- It seems that the double SMA strategy yields the cumulative return of 40%.

- Generating naive momentum trading signals based on consecutive positive or negative price changes

def naive_momentum_signals(ticker_ts_df, nb_conseq_days=2):

"""

Generate naive momentum trading signals based on consecutive positive or negative price changes.

Parameters:

- ticker_ts_df (pandas.DataFrame): A DataFrame containing historical stock data.

- nb_conseq_days (int): The number of consecutive positive or negative days to trigger a signal.

Returns:

- signals (pandas.DataFrame): A DataFrame with 'orders' column containing buy (1) and sell (-1) signals.

"""

signals = pd.DataFrame(index=ticker_ts_df.index)

signals['orders'] = 0

price = ticker_ts_df['Adj Close']

price_diff = price.diff()

signal = 0

cons_day = 0

for i in range(1, len(ticker_ts_df)):

if price_diff[i] > 0:

cons_day = cons_day + 1 if price_diff[i] > 0 else 0

if cons_day == nb_conseq_days and signal != 1:

signals['orders'].iloc[i] = 1

signal = 1

elif price_diff[i] < 0:

cons_day = cons_day - 1 if price_diff[i] < 0 else 0

if cons_day == -nb_conseq_days and signal != -1:

signals['orders'].iloc[i] = -1

signal = -1

return signals

signal_df = naive_momentum_signals(aapl_ts_df)

profit_series = calculate_profit(signal_df, aapl_ts_df["Adj Close"])

ax1, _ = plot_strategy(aapl_ts_df["Adj Close"], signal_df, profit_series)

ax1.legend(loc='upper left', fontsize=14)

plt.show()

- It turns out that the naive momentum trading strategy yields the cumulative return over 60%.

- Generating mean reversion trading signals based on moving averages and thresholds

def mean_reversion_signals(ticker_ts_df, entry_threshold=1.0, exit_threshold=0.5):

"""

Generate mean reversion trading signals based on moving averages and thresholds.

Parameters:

- ticker_ts_df (pandas.DataFrame): A DataFrame containing historical stock data.

- entry_threshold (float): The entry threshold as a multiple of the standard deviation.

- exit_threshold (float): The exit threshold as a multiple of the standard deviation.

Returns:

- signals (pandas.DataFrame): A DataFrame with 'orders' column containing buy (1) and sell (-1) signals.

"""

signals = pd.DataFrame(index=ticker_ts_df.index)

signals['mean'] = ticker_ts_df['Adj Close'].rolling(

window=20).mean() # Adjust the window size as needed

signals['std'] = ticker_ts_df['Adj Close'].rolling(

window=20).std() # Adjust the window size as needed

signals['signal'] = np.where(ticker_ts_df['Adj Close'] > (

signals['mean'] + entry_threshold * signals['std']), 1, 0)

signals['signal'] = np.where(ticker_ts_df['Adj Close'] < (

signals['mean'] - exit_threshold * signals['std']), -1, 0)

signals['orders'] = signals['signal'].diff()

signals.loc[signals['orders'] == 0, 'orders'] = None

return signals

signal_df = mean_reversion_signals(aapl_ts_df)

profit_series = calculate_profit(signal_df, aapl_ts_df["Adj Close"])

ax1, _ = plot_strategy(aapl_ts_df["Adj Close"], signal_df, profit_series)

ax1.plot(signal_df.index, signal_df['mean'], linestyle='--', label="Mean")

ax1.plot(signal_df.index, signal_df['mean'] +

signal_df['std'], linestyle='--', label="Ceiling STD")

ax1.plot(signal_df.index, signal_df['mean'] -

signal_df['std'], linestyle='--', label="Floor STD")

ax1.legend(loc='upper left', fontsize=10)

plt.show()

- It appears that the mean reversion trading strategy yields the cumulative return over 45%.

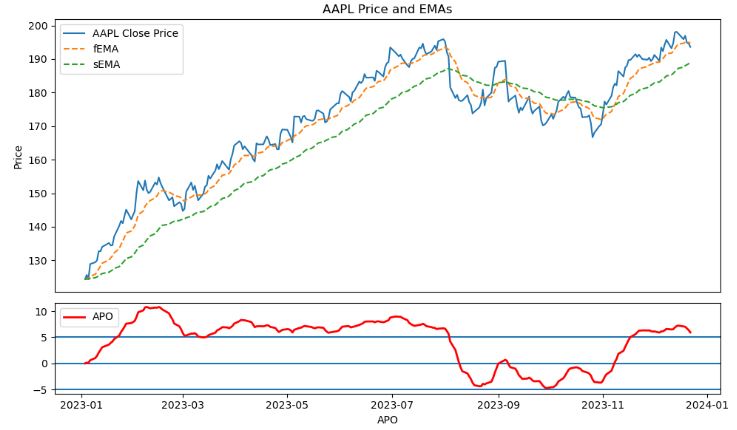

- Generating trading signals based on APO and double EMA for AAPL in ’23

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings("ignore")

import yfinance as yf

from analysis_utils import calculate_profit, load_ticker_ts_df, plot_strategy

tickers = ['AAPL']

START_DATE = '2023-01-01'

END_DATE = '2023-12-24'

APO_BULL_SIGNAL = 5

APO_BEAR_SIGNAL = -5

APO_FAST_WINDOW = 12

APO_SLOW_WINDOW = 45

ticker = load_ticker_ts_df('AAPL', START_DATE, END_DATE)

ticker['fEMA'] = ticker['Adj Close'].ewm(

span=APO_FAST_WINDOW, adjust=False).mean()

ticker['sEMA'] = ticker['Adj Close'].ewm(

span=APO_SLOW_WINDOW, adjust=False).mean()

ticker['APO'] = ticker['fEMA'] - ticker['sEMA']

fig, (ax1, ax2) = plt.subplots(2, 1, gridspec_kw={

'height_ratios': (3, 1)}, figsize=(10, 6))

ax1.plot(ticker.index, ticker['Adj Close'], label='AAPL Close Price')

ax1.plot(ticker.index, ticker['fEMA'], label='fEMA', linestyle='--')

ax1.plot(ticker.index, ticker['sEMA'], label='sEMA', linestyle='--')

ax1.set_title('AAPL Price and EMAs')

ax1.set_ylabel('Price')

ax1.set_xticks([])

ax2.axhline(APO_BULL_SIGNAL)

ax2.axhline(0.0)

ax2.axhline(APO_BEAR_SIGNAL)

ax2.plot(ticker.index, ticker['APO'], label='APO', lw=2, color='r')

ax2.set_xlabel('APO')

ax1.legend()

ax2.legend()

plt.tight_layout()

plt.show()

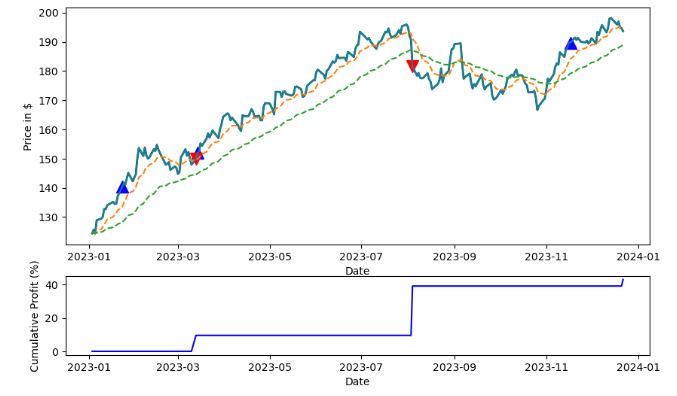

- Plotting the APO trading signals and cumulative returns for AAPL in ’23

def signal_apo_oscillator(ticker_ts, fast_window_size=APO_FAST_WINDOW, slow_window_size=APO_SLOW_WINDOW, buy_threshold=APO_BULL_SIGNAL, sell_threshold=APO_BEAR_SIGNAL):

"""

Calculate signals using the Absolute Price Oscillator (APO) indicator for a given stock's time series.

Parameters:

- ticker_ts (DataFrame): Time series data for the stock, typically containing 'Adj Close' prices.

- fast_window_size (int, optional): Fast EMA (Exponential Moving Average) window size. Default is APO_FAST_WINDOW.

- slow_window_size (int, optional): Slow EMA window size. Default is APO_SLOW_WINDOW.

- buy_threshold (float, optional): Buy signal threshold for the APO. Default is APO_BULL_SIGNAL.

- sell_threshold (float, optional): Sell signal threshold for the APO. Default is APO_BEAR_SIGNAL.

Returns:

- signals_df (DataFrame): DataFrame containing signals based on APO oscillator:

- 'signal': Signal values (1 for buy, -1 for sell, 0 for no signal).

- 'orders': Changes in signals (buy/sell orders) with None for no change.

"""

fema = ticker_ts['Adj Close'].ewm(

span=fast_window_size, adjust=False).mean()

sma = ticker_ts['Adj Close'].ewm(

span=slow_window_size, adjust=False).mean()

apo = fema - sma

signals_df = pd.DataFrame(index=ticker_ts.index)

signals_df['signal'] = np.where(

apo >= buy_threshold, 1, np.where(apo <= sell_threshold, -1, 0))

signals_df['orders'] = signals_df['signal'].diff()

signals_df.loc[signals_df['orders'] == 0, 'orders'] = None

return signals_df

signals_df = signal_apo_oscillator(ticker)

profit_series = calculate_profit(signals_df, ticker["Adj Close"])

ax1, ax2 = plot_strategy(ticker["Adj Close"], signals_df, profit_series)

ax1.plot(ticker.index, ticker['Adj Close'], label='AAPL Close Price')

ax1.plot(ticker.index, ticker['fEMA'], label='fEMA', linestyle='--')

ax1.plot(ticker.index, ticker['sEMA'], label='sEMA', linestyle='--')

plt.show()

- It looks like the APO trading strategy yields the cumulative return ca. 40%.

Cointegrated Pairs of Stocks

- Let’s implement the pair trading strategy by downloading the crypto Forex stocks, bank stocks, and global indexes

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings("ignore")

import yfinance as yf

from analysis_utils2 import calculate_profit, load_ticker_ts_df, plot_strategy

crypto_forex_stocks = ['BTC-USD', 'ETH-USD', 'BNB-USD', 'XRP-USD', 'ADA-USD', 'DOGE-USD', 'ETC-USD', 'XLM-USD', 'AAVE-USD', 'EOS-USD', 'XTZ-USD', 'ALGO-USD', 'XMR-USD', 'KCS-USD',

'MKR-USD', 'BSV-USD', 'RUNE-USD', 'DASH-USD', 'KAVA-USD', 'ICX-USD', 'LINA-USD', 'WAXP-USD', 'LSK-USD', 'EWT-USD', 'XCN-USD', 'HIVE-USD', 'FTX-USD', 'RVN-USD', 'SXP-USD', 'BTCB-USD']

bank_stocks = ['JPM', 'BAC', 'WFC', 'C', 'GS', 'MS', 'DB', 'UBS', 'BBVA', 'SAN', 'ING', ' BNPQY', 'HSBC', 'SMFG', 'PNC', 'USB', 'BK', 'STT', 'KEY', 'RF', 'HBAN', 'FITB', 'CFG',

'BLK', 'ALLY', 'MTB', 'NBHC', 'ZION', 'FFIN', 'FHN', 'UBSI', 'WAL', 'PACW', 'SBCF', 'TCBI', 'BOKF', 'PFG', 'GBCI', 'TFC', 'CFR', 'UMBF', 'SPFI', 'FULT', 'ONB', 'INDB', 'IBOC', 'HOMB']

global_indexes = ['^DJI', '^IXIC', '^GSPC', '^FTSE', '^N225', '^HSI', '^AXJO', '^KS11', '^BFX', '^N100',

'^RUT', '^VIX', '^TNX']

START_DATE = '2023-01-01'

END_DATE = '2023-12-24'

universe_tickers = crypto_forex_stocks + bank_stocks + global_indexes

universe_tickers_ts_map = {ticker: load_ticker_ts_df(

ticker, START_DATE, END_DATE) for ticker in universe_tickers}

def sanitize_data(data_map):

TS_DAYS_LENGTH = (pd.to_datetime(END_DATE) -

pd.to_datetime(START_DATE)).days

data_sanitized = {}

date_range = pd.date_range(start=START_DATE, end=END_DATE, freq='D')

for ticker, data in data_map.items():

if data is None or len(data) < (TS_DAYS_LENGTH / 2):

# We cannot handle shorter TSs

continue

if len(data) > TS_DAYS_LENGTH:

# Normalize to have the same length (TS_DAYS_LENGTH)

data = data[-TS_DAYS_LENGTH:]

# Reindex the time series to match the date range and fill in any blanks (Not Numbers)

data = data.reindex(date_range)

data['Adj Close'].replace([np.inf, -np.inf], np.nan, inplace=True)

data['Adj Close'].interpolate(method='linear', inplace=True)

data['Adj Close'].fillna(method='pad', inplace=True)

data['Adj Close'].fillna(method='bfill', inplace=True)

assert not np.any(np.isnan(data['Adj Close'])) and not np.any(

np.isinf(data['Adj Close']))

data_sanitized[ticker] = data

return data_sanitized

# Sample some

uts_sanitized = sanitize_data(universe_tickers_ts_map)

uts_sanitized['JPM'].shape, uts_sanitized['BTC-USD'].shape

((358, 6), (358, 6))

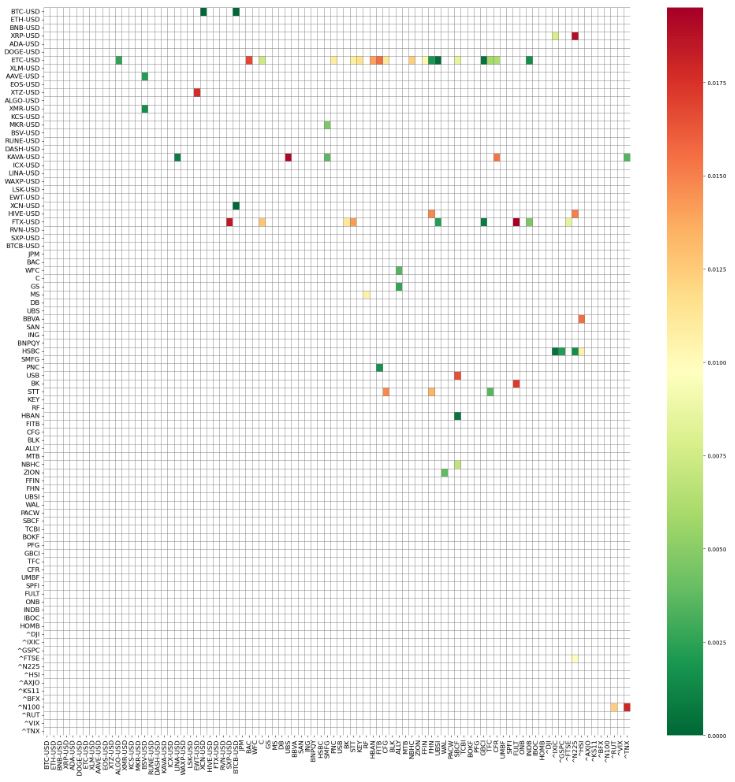

- Finding and plotting cointegrated pairs

from statsmodels.tsa.stattools import coint

from itertools import combinations

from statsmodels.tsa.stattools import coint

def find_cointegrated_pairs(tickers_ts_map, p_value_threshold=0.2):

"""

Find cointegrated pairs of stocks based on the Augmented Dickey-Fuller (ADF) test.

Parameters:

- tickers_ts_map (dict): A dictionary where keys are stock tickers and values are time series data.

- p_value_threshold (float): The significance level for cointegration testing.

Returns:

- pvalue_matrix (numpy.ndarray): A matrix of cointegration p-values between stock pairs.

- pairs (list): A list of tuples representing cointegrated stock pairs and their p-values.

"""

tickers = list(tickers_ts_map.keys())

n = len(tickers)

# Extract 'Adj Close' prices into a matrix (each column is a time series)

adj_close_data = np.column_stack(

[tickers_ts_map[ticker]['Adj Close'].values for ticker in tickers])

pvalue_matrix = np.ones((n, n))

# Calculate cointegration p-values for unique pair combinations

for i, j in combinations(range(n), 2):

result = coint(adj_close_data[:, i], adj_close_data[:, j])

pvalue_matrix[i, j] = result[1]

pairs = [(tickers[i], tickers[j], pvalue_matrix[i, j])

for i, j in zip(*np.where(pvalue_matrix < p_value_threshold))]

return pvalue_matrix, pairs

# This section can take up to 5mins

P_VALUE_THRESHOLD = 0.02

pvalues, pairs = find_cointegrated_pairs(

uts_sanitized, p_value_threshold=P_VALUE_THRESHOLD)

import seaborn as sns

plt.figure(figsize=(24, 24))

heatmap = sns.heatmap(pvalues, xticklabels=uts_sanitized.keys(),

yticklabels=uts_sanitized.keys(), cmap='RdYlGn_r',

mask=(pvalues > (P_VALUE_THRESHOLD)),

linecolor='gray', linewidths=0.5)

heatmap.set_xticklabels(heatmap.get_xticklabels(), size=12)

heatmap.set_yticklabels(heatmap.get_yticklabels(), size=12)

plt.show()

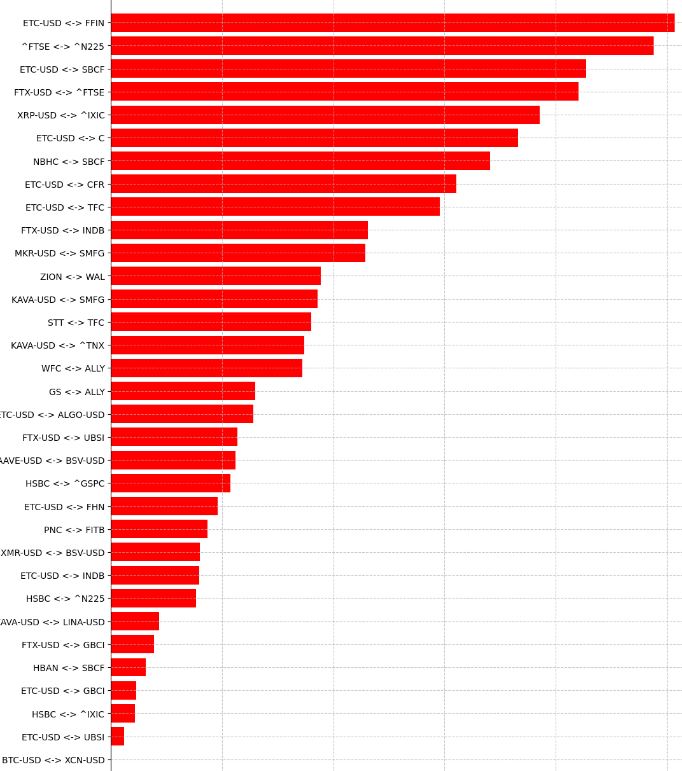

- Plotting cointegration P-values 0-10 (in 1000s)

sorted_pairs = sorted(pairs, key=lambda x: x[2], reverse=False)

sorted_pairs = sorted_pairs[0:35]

sorted_pairs_labels, pairs_p_values = zip(

*[(f'{y1} <-> {y2}', p*1000) for y1, y2, p in sorted_pairs])

plt.figure(figsize=(12, 18))

plt.barh(sorted_pairs_labels,

pairs_p_values, color='red')

plt.xlabel('P-Values (1000)', fontsize=8)

plt.ylabel('Pairs', fontsize=6)

plt.title('Cointegration P-Values (in 1000s)', fontsize=20)

plt.grid(axis='both', linestyle='--', alpha=0.7)

plt.show()

plt.savefig('pairs_pvalue.png')

P-Values 0-10 (1000)

- Comparing the following ticker pairs with highest correlations

from sklearn.preprocessing import MinMaxScaler

ticker_pairs = [("FTX-USD", "INDB"), ("ZION", "WAL"), ("GS", "ALLY")]

fig, axs = plt.subplots(3, 1, figsize=(12, 10))

scaler = MinMaxScaler()

for i, (ticker1, ticker2) in enumerate(ticker_pairs):

# Scale the price data for each pair using MIN MAX

scaled_data1 = scaler.fit_transform(

uts_sanitized[ticker1]['Adj Close'].values.reshape(-1, 1))

scaled_data2 = scaler.fit_transform(

uts_sanitized[ticker2]['Adj Close'].values.reshape(-1, 1))

axs[i].plot(scaled_data1, label=f'{ticker1}', color='lightgray', alpha=0.7,lw=2)

axs[i].plot(scaled_data2, label=f'{ticker2}', color='lightgray', alpha=0.7,lw=2)

# Apply rolling mean with a window of 15

scaled_data1_smooth = pd.Series(scaled_data1.flatten()).rolling(

window=15, min_periods=1).mean()

scaled_data2_smooth = pd.Series(scaled_data2.flatten()).rolling(

window=15, min_periods=1).mean()

axs[i].plot(scaled_data1_smooth, label=f'{ticker1} SMA', color='red')

axs[i].plot(scaled_data2_smooth, label=f'{ticker2} SMA', color='blue')

axs[i].set_ylabel('*Scaled* Price $', fontsize=12)

axs[i].set_title(f'{ticker1} vs {ticker2}', fontsize=18)

axs[i].legend()

axs[i].set_xticks([])

plt.tight_layout()

plt.show()

![Comparing the ticker pairs [("FTX-USD", "INDB"), ("ZION", "WAL"), ("GS", "ALLY")]](https://newdigitals.org/wp-content/uploads/2023/12/invest_ftx.jpg?w=730)

Z-Score vs Trading Signals

- Let’s create trading signals using the Z-score and mean.

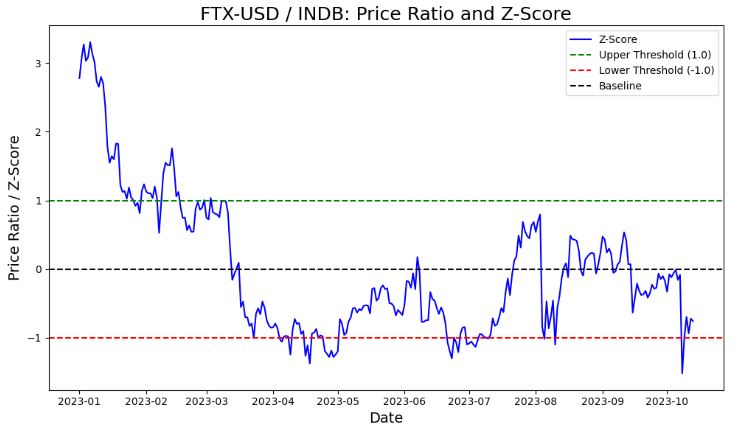

- Plotting FTX-USD / INDB: Price Ratio and Z-Score

TRAIN = int(len(uts_sanitized["FTX-USD"]) * 0.80)

TEST = len(uts_sanitized["FTX-USD"]) - TRAIN

AAVE_ts = uts_sanitized["FTX-USD"]["Adj Close"][:TRAIN]

C_ts = uts_sanitized["INDB"]["Adj Close"][:TRAIN]

ratios = C_ts/AAVE_ts

fig, ax = plt.subplots(figsize=(10, 6))

ratios_mean = np.mean(ratios)

ratios_std = np.std(ratios)

ratios_zscore = (ratios - ratios_mean) / ratios_std

ax.plot(ratios.index, ratios_zscore, label="Z-Score", color='blue')

# Plot reference lines

ax.axhline(1.0, color="green", linestyle='--', label="Upper Threshold (1.0)")

ax.axhline(-1.0, color="red", linestyle='--', label="Lower Threshold (-1.0)")

ax.axhline(0, color="black", linestyle='--', label="Baseline")

ax.set_title('FTX-USD / INDB: Price Ratio and Z-Score', fontsize=18)

ax.set_xlabel('Date',fontsize=14)

ax.set_ylabel('Price Ratio / Z-Score',fontsize=14)

ax.legend()

plt.tight_layout()

plt.show()

- The green horizontal line here will signal a buy for INDB if crossed and a sell for FTX-USD, the red line will do the opposite.

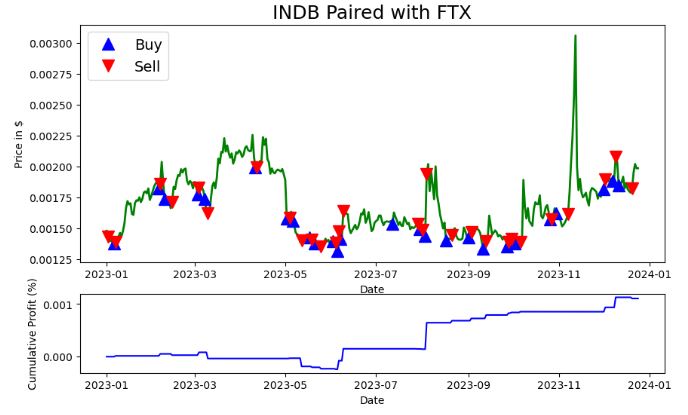

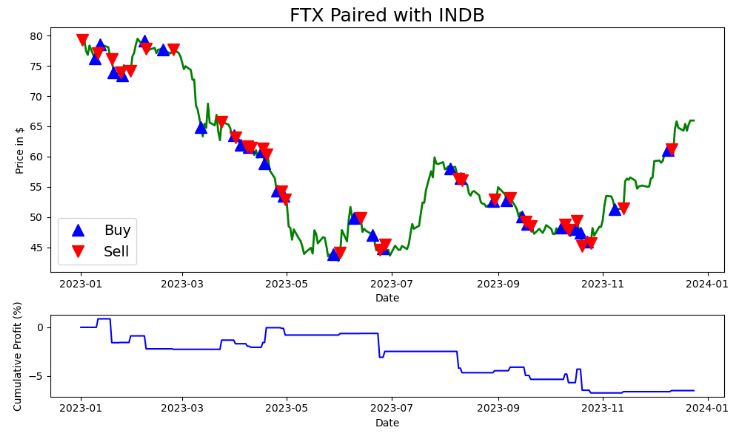

- Generating and plotting trading signals based on the Z-score analysis and the price ratio between FTX-USD and INDB

def signals_zscore_evolution(ticker1_ts, ticker2_ts, window_size=15, first_ticker=True):

"""

Generate trading signals based on z-score analysis of the ratio between two time series.

Parameters:

- ticker1_ts (pandas.Series): Time series data for the first security.

- ticker2_ts (pandas.Series): Time series data for the second security.

- window_size (int): The window size for calculating z-scores and ratios' statistics.

- first_ticker (bool): Set to True to use the first ticker as the primary signal source, and False to use the second.

Returns:

- signals_df (pandas.DataFrame): A DataFrame with 'signal' and 'orders' columns containing buy (1) and sell (-1) signals.

"""

ratios = ticker1_ts / ticker2_ts

ratios_mean = ratios.rolling(

window=window_size, min_periods=1, center=False).mean()

ratios_std = ratios.rolling(

window=window_size, min_periods=1, center=False).std()

z_scores = (ratios - ratios_mean) / ratios_std

buy = ratios.copy()

sell = ratios.copy()

if first_ticker:

# These are empty zones, where there should be no signal

# the rest is signalled by the ratio.

buy[z_scores > -1] = 0

sell[z_scores < 1] = 0

else:

buy[z_scores < 1] = 0

sell[z_scores > -1] = 0

signals_df = pd.DataFrame(index=ticker1_ts.index)

signals_df['signal'] = np.where(buy > 0, 1, np.where(sell < 0, -1, 0))

signals_df['orders'] = signals_df['signal'].diff()

signals_df.loc[signals_df['orders'] == 0, 'orders'] = None

return signals_df

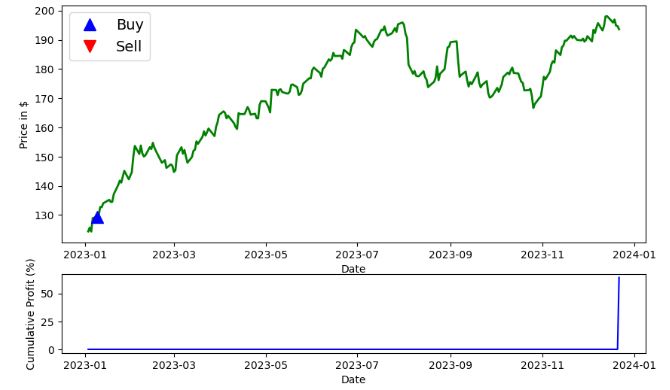

AAVE_ts = uts_sanitized["FTX-USD"]["Adj Close"]

C_ts = uts_sanitized["INDB"]["Adj Close"]

#plt.figure(figsize=(10, 6))

signals_df1 = signals_zscore_evolution(AAVE_ts, C_ts)

profit_df1 = calculate_profit(signals_df1, AAVE_ts)

ax1, _ = plot_strategy(AAVE_ts, signals_df1, profit_df1)

signals_df2 = signals_zscore_evolution(AAVE_ts, C_ts, first_ticker=False)

profit_df2 = calculate_profit(signals_df2, C_ts)

ax2, _ = plot_strategy(C_ts, signals_df2, profit_df2)

ax1.legend(loc='upper left', fontsize=14)

ax1.set_title(f'INDB Paired with FTX', fontsize=18)

ax2.legend(loc='lower left', fontsize=14)

ax2.set_title(f'FTX Paired with INDB', fontsize=18)

plt.tight_layout()

plt.show()

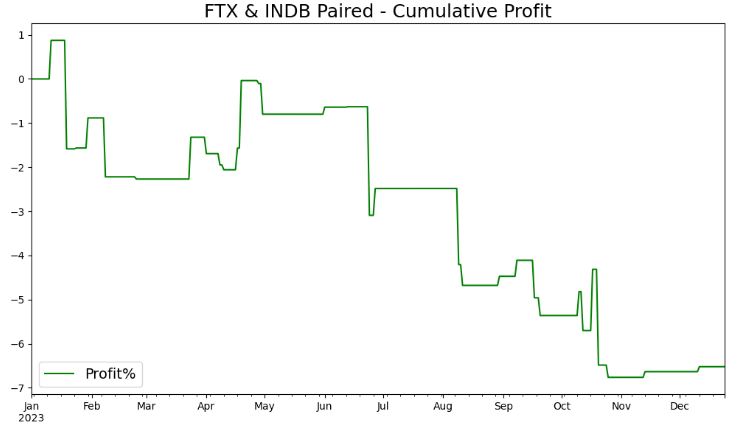

- Plotting FTX & INDB Paired – Cumulative Profit

plt.figure(figsize=(10, 6))

cumulative_profit_combined = profit_df1 + profit_df2

ax2_combined = cumulative_profit_combined.plot(

label='Profit%', color='green')

plt.legend(loc='lower left', fontsize=14)

plt.title(f'FTX & INDB Paired - Cumulative Profit', fontsize=18)

plt.tight_layout()

plt.show()

- It is clear that this trading strategy is not profitable in ’23.

Conclusions

- In this study, we focused on mitigating market risk while constructing market-neutral portfolios. In a situation where financial markets are characterized by high volatility, such portfolios are more likely to outperform other strategies.

- Quantitative analysis plays a critical role in market-neutral trading by providing traders with a data-driven approach to identifying pricing discrepancies and making investment decisions. This is performed with algorithms and statistical models to analyze large amounts of historical data and identify patterns and relationships in the market.

- Statistical arbitrage (aka Stat-Arb) was chosen to be the core trading strategy that seeks to profit from discrepancies in the prices of related securities.

- A mean-reversion statistical arbitrage strategy was implemented as pairs trading. Pairs trading involves identifying two securities that have a high correlation and taking positions in the hope that the prices of the two securities will eventually converge.

- A popular example of pairs trading: if the prices of two stocks have historically moved in tandem, and one of them suddenly drops in price, the trader could buy the undervalued stock and short sell the overvalued one.

- We addressed the problem of Markowitz portfolio optimization for a one-year horizon investment, through the pairs trading cointegrated strategy. Such a strategy allowed us to identify the prices and returns of each stock on the basis of a cointegration relationship estimated by means of EMA and the covariance ratios between stock pairs.

- We assessed the viability of our portfolios by means of backtesting while adding the Market Capital Line (MCL) to the efficient frontier of simulated trading in terms of max Sharpe ratio and min variance.

- We experimented with the investors choices of risk/reward, through indifference curves and descriptive statistics of cumulative returns.

- We compared our findings to the results of technical analysis by generating the double SMA/EMA strategy, mean reversion trading signals, naive momentum, and APO thresholds.

- We also created trading signals using the Z-score and mean.

- We examined asset allocation across a number of sectors including technology, financial services, and industrials in 2023.

- We checked correlations with AAPL, performed AAPL Stat-Arb 1Y backtesting, and constructed portfolio efficient frontiers by adding MCL, MVP, and TAN to simulated trades.

- We implemented the pair trading strategy by downloading the crypto Forex stocks, bank stocks, and global indexes.

- We believe the present diversified approach improves the market-neutral landscape by providing a set of optimal portfolios that offer the highest expected return for a defined level of risk or the lowest risk for a given level of expected return.

- Market-neutral trading is an evolving strategy. Following best practices and the present study, we prefer to focus on using statistical models and growth factors rather than fundamental arbitrage, as technology makes it easier to gain access to huge data and analyze them. However, regulatory changes and increased competition in the market could also impact the future of market-neutral trading.

Explore More

- A Comprehensive Analysis of Best Trading Technical Indicators w/ TA-Lib – Tesla ’23

- Real-Time Stock Sentiment Analysis w/ NLP Web Scraping

- Plotly Dash TA Stock Market App

- Optimizing NVIDIA Returns-Drawdowns MVA Crossovers vs Simple RNN Mean Reversal Trading Strategies in Python

- Multiple-Criteria Technical Analysis of Blue Chips in Python

- 360-Deg Revision of Risk Aware Investing after SVB Collapse – 1. The Financial Sector

- Towards Max(ROI/Risk) Trading

- Portfolio max(Return/Risk) Stochastic Optimization of 20 Dividend Growth Stocks

- Risk-Return Analysis and LSTM Price Predictions of 4 Major Tech Stocks in 2023

- The Donchian Channel vs Buy-and-Hold Breakout Trading Systems – $MO Use-Case

- Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

- Advanced Integrated Data Visualization (AIDV) in Python – 1. Stock Technical Indicators

- Quant Trading using Monte Carlo Predictions and 62 AI-Assisted Trading Technical Indicators (TTI)

- The Qullamaggie’s OXY Swing Breakouts

- The Qullamaggie’s TSLA Breakouts for Swing Traders

- Stock Portfolio Risk/Return Optimization

- Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

- Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

- Oracle Monte Carlo Stock Simulations

- Predicting the JPM Stock Price and Breakouts with Auto ARIMA, FFT, LSTM and Technical Trading Indicators

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- A TradeSanta’s Quick Guide to Best Swing Trading Indicators

- Top 6 Reliability/Risk Engineering Learnings

- Bear Market Similarity Analysis using Nasdaq 100 Index Data

- Are Blue Chips Perfect for This Bear Market?

- DJI Market State Analysis using the Cruz Fitting Algorithm

- The CodeX-Aroon Auto-Trading Approach – the AAPL Use Case

- AAPL Stock Technical Analysis 2 June 2022

- Risk-Aware Strategies for DCA Investors

- Inflation-Resistant Stocks to Buy

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment