SEO Title: Can Dividends, Natural Gas and Crypto Diversify Big Techs?

- The objective of this project is to implement several basic Quant Trading (QT) optimization ideas by analyzing tech growth, dividend stocks and highly volatile assets (commodities and crypto) in terms of risk/return optimization scenarios and (potential) diversification options.

- We will use the financial APIs to download real-time price charts of both individual stocks and stock portfolios.

- Several steps will be undertaken to validate the performance and reliability of our QT algorithms on historical data before going live with them in algorithmic trading.

- Project Scope and Specific Goals:

- Portfolio Optimization Scenario 1: MO + (AAPL, META, AMZN)

- Portfolio Optimization Scenario 2: (DIS, AMD) + (AAPL, TSLA)

- Portfolio 3: (a) [‘TATAMOTORS’,’DABUR’, ‘ICICIBANK’,’WIPRO’,’INFY’] and (b) [‘AXISBANK’, ‘HDFCBANK’, ‘ICICIBANK’, ‘KOTAKBANK’, ‘SBIN’] (Indian Stocks)

- In-Depth QT Analysis of Tech Growth Stocks: AAPL, META, and NVDA

- Backtesting of S&P 500 historical prices in terms of price anomalies

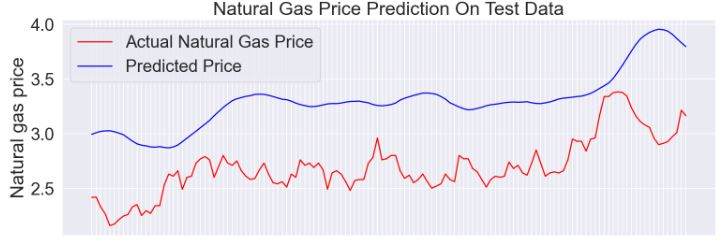

- Feasibility of short-term price prediction of the most volatile assets: commodities such as Natural Gas (NG) and crypto (BTC-USD).

Ultimately, we need to answer the following fundamental question: Can Dividend Kings, NGUSD and BTC-USD Diversify Growth Tech assets?

- Why Dividend Stocks:

Dividends are very popular among investors, especially those who want a steady stream of income from their investments. Some companies choose to share their profits with shareholders. These distributions are called dividends. First, they provide investors with regular income monthly, quarterly, or annually. Secondly, they offer a sense of safety. Stock prices are subject to volatility—whether that’s company-specific or industry-specific news or factors that affect the overall economy—so investors want to be sure they have some stability as well. Many companies that pay dividends already have an established track record of profits and profit-sharing.

- Why NGUSD:

Commodities are an alternative asset class that can provide a hedge against inflation and diversification away from the more mainstream asset classes.

Natural gas (NG) is one of the most traded commodities. NG prices have soared in 2022, reaching price levels not seen since 2008. From heating homes to powering industrial facilities, NG is a mainstay of the global energy mix. As the cleanest-burning fossil fuel, it’s a critical bridge fuel in the energy transition to lower-carbon alternatives. Read more here.

Alex Campbell, head of communications at Freetrade, comments: “Rather than backing some of these high-flying green energy companies that are still yet to ship a tried-and-tested product, companies in the natural gas supply sector tend to target efficient and hopefully predictable capital returns to shareholders through buybacks and dividends.”

Looking at demand and supply, the US is by far the largest consumer and exporter of NG.

- Is crypto mining a good idea?

While the cryptocurrency market appears to be more resilient now than it has been in the past, it’s still an extremely volatile, high risk and complex investment.

However, the stock correlation analysis indicates that BTC correlations with other assets are less than 0.2. In addition, most of its correlations with other assets are negative. This makes it ideal for inclusion in a portfolio to add diversification.

Table of Contents

- Portfolio 1: MO + (AAPL, META, AMZN)

- Portfolio 2: (DIS, AMD) + (AAPL, TSLA)

- AAPL Price LSTM Forecasting

- NVDA Entry/Exit Trading Signals

- NVDA Fundamental Analysis

- Indian Dividend Stock Portfolio 3

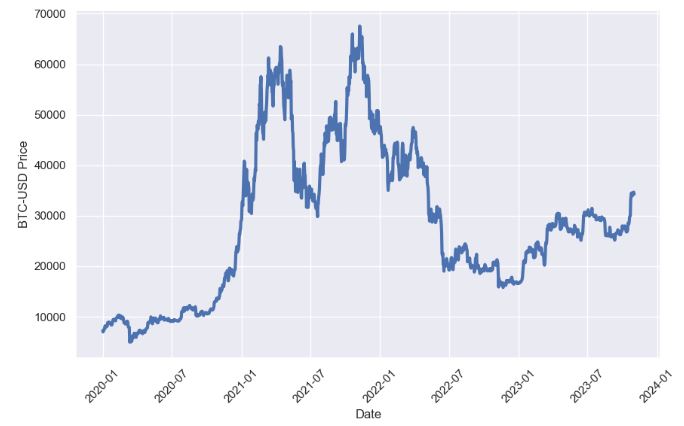

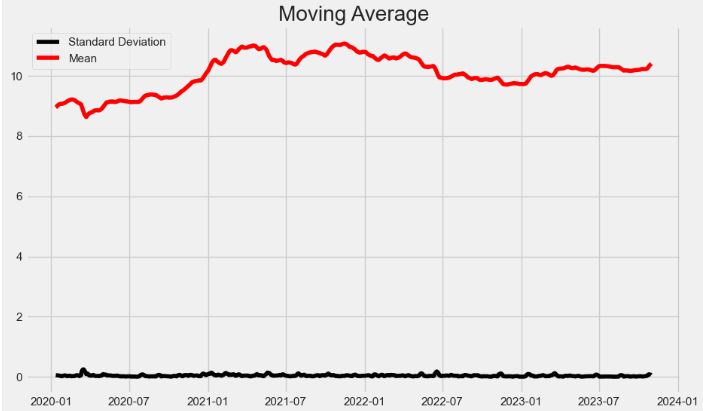

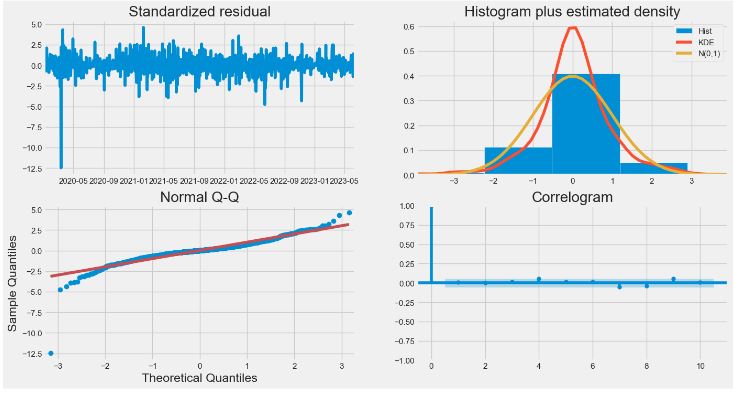

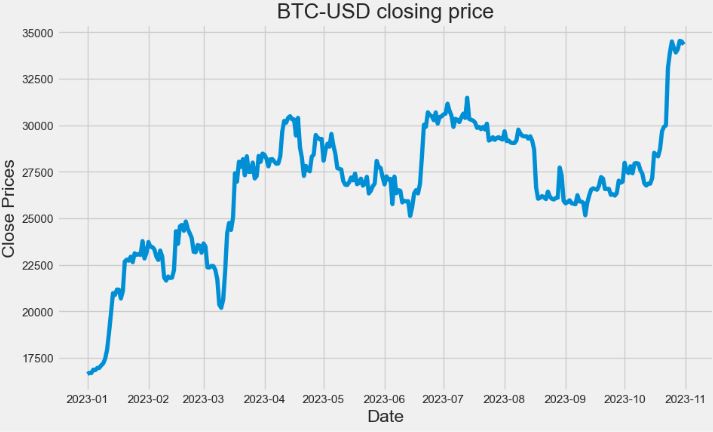

- BTC-USD Price Analysis and Forecasting

- Natural Gas Price Forecasting

- META Stock Isolation Forest Anomalies

- S&P 500 Historical Price Anomalies

- Summary

- References

- Explore More

- Prerequisites: Python, Jupyter with Anaconda IDE, Pandas, Numpy, Seaborn, Matplotlib, yfinance, pypfopt, OS, requests, Quantstats, sklearn, Plotly, and TensorFlow.

Portfolio 1: MO + (AAPL, META, AMZN)

- In this section, we will examine Portfolio 1 by implementing the stock market analysis and LSTM prediction pipeline.

- The stocks of interest are MO + (AAPL, META, AMZN).

- Why MO? Altria’s dividend yield is a huge 9.37%; the company’s main product has a loyal customer base; Altria walks a fine line between price and demand.

- Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH')

os. getcwd()

- Importing the key libraries and downloading stock prices

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

plt.style.use("fivethirtyeight")

%matplotlib inline

# For reading stock data from yahoo

from pandas_datareader.data import DataReader

import yfinance as yf

from pandas_datareader import data as pdr

yf.pdr_override()

# For time stamps

from datetime import datetime

# The stocks we'll use for this analysis

tech_list = ['AAPL', 'META', 'MO', 'AMZN']

# Set up End and Start times for data grab

end = datetime.now()

start = datetime(end.year - 1, end.month, end.day)

for stock in tech_list:

globals()[stock] = yf.download(stock, start, end)

company_list = [AAPL, META, MO, AMZN]

company_name = ["APPLE", "META", "ALTRIA", "AMAZON"]

for company, com_name in zip(company_list, company_name):

company["company_name"] = com_name

df = pd.concat(company_list, axis=0)

df.tail(10)

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

![Input data table of portfolio 1 ['AAPL', 'META', 'MO', 'AMZN']](https://newdigitals.org/wp-content/uploads/2023/10/port1_inputab.jpg?w=609)

- Performing automated Exploratory Data Analysis (EDA) using Pandas Profiling and SweetViz

import pandas as pd

from pandas_profiling import ProfileReport

#Descriptive Statistics about the Data

profile = ProfileReport(df, title="Pandas Profiling Report")

profile.to_file("report.html")

# importing sweetviz

import sweetviz as sv

#analyzing the dataset

advert_report = sv.analyze(df)

#display the report

advert_report.show_html('report_sv.html')

- Example MO descriptive statistics

# MO Summary Stats

MO.describe()

- Closing price charts of portfolio 1

# Let's see a historical view of the closing price

plt.figure(figsize=(15, 10))

plt.rcParams.update({'font.size': 18})

plt.subplots_adjust(top=1.25, bottom=1.2)

plt.rc('xtick', labelsize=16) #fontsize of the x tick labels

plt.rc('ytick', labelsize=16) #fontsize of the y tick labels

for i, company in enumerate(company_list, 1):

plt.subplot(2, 2, i)

company['Adj Close'].plot(linewidth=2)

plt.ylabel('Adj Close')

plt.xlabel(None)

plt.title(f"Closing Price of {tech_list[i - 1]}")

plt.tight_layout()

- Sales volumes of portfolio 1

# Now let's plot the total volume of stock being traded each day

plt.figure(figsize=(15, 10))

plt.subplots_adjust(top=1.25, bottom=1.2)

for i, company in enumerate(company_list, 1):

plt.subplot(2, 2, i)

company['Volume'].plot(linewidth=2)

plt.ylabel('Volume')

plt.xlabel(None)

plt.title(f"Sales Volume for {tech_list[i - 1]}")

plt.tight_layout()

- MAs of portfolio 1 for 10-20-50 days

ma_day = [10, 20, 50]

for ma in ma_day:

for company in company_list:

column_name = f"MA for {ma} days"

company[column_name] = company['Adj Close'].rolling(ma).mean()

fig, axes = plt.subplots(nrows=2, ncols=2)

fig.set_figheight(10)

fig.set_figwidth(15)

AAPL[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[0,0],linewidth=2)

axes[0,0].set_title('APPLE')

META[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[0,1],linewidth=2)

axes[0,1].set_title('META')

MO[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[1,0],linewidth=2)

axes[1,0].set_title('ALTRIA')

AMZN[['Adj Close', 'MA for 10 days', 'MA for 20 days', 'MA for 50 days']].plot(ax=axes[1,1],linewidth=2)

axes[1,1].set_title('AMAZON')

fig.tight_layout()

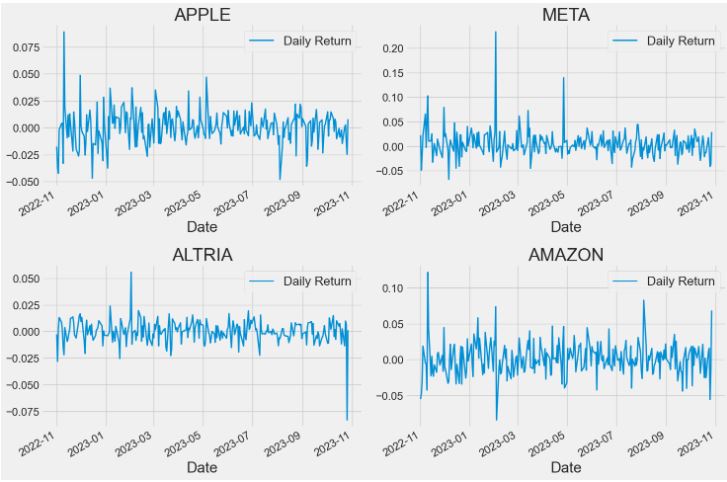

- Daily returns of portfolio 1 as line charts

#What was the daily return of the stock on average?

# We'll use pct_change to find the percent change for each day

for company in company_list:

company['Daily Return'] = company['Adj Close'].pct_change()

# Then we'll plot the daily return percentage

fig, axes = plt.subplots(nrows=2, ncols=2)

fig.set_figheight(10)

fig.set_figwidth(15)

AAPL['Daily Return'].plot(ax=axes[0,0], legend=True, linestyle='-', linewidth=2)

axes[0,0].set_title('APPLE')

META['Daily Return'].plot(ax=axes[0,1], legend=True, linestyle='-', linewidth=2)

axes[0,1].set_title('META')

MO['Daily Return'].plot(ax=axes[1,0], legend=True, linestyle='-', linewidth=2)

axes[1,0].set_title('ALTRIA')

AMZN['Daily Return'].plot(ax=axes[1,1], legend=True, linestyle='-', linewidth=2)

axes[1,1].set_title('AMAZON')

fig.tight_layout()

- Daily returns of portfolio 1 as histograms

plt.figure(figsize=(12, 9))

for i, company in enumerate(company_list, 1):

plt.subplot(2, 2, i)

company['Daily Return'].hist(bins=50)

plt.xlabel('Daily Return')

plt.ylabel('Counts')

plt.title(f'{company_name[i - 1]}')

plt.tight_layout()

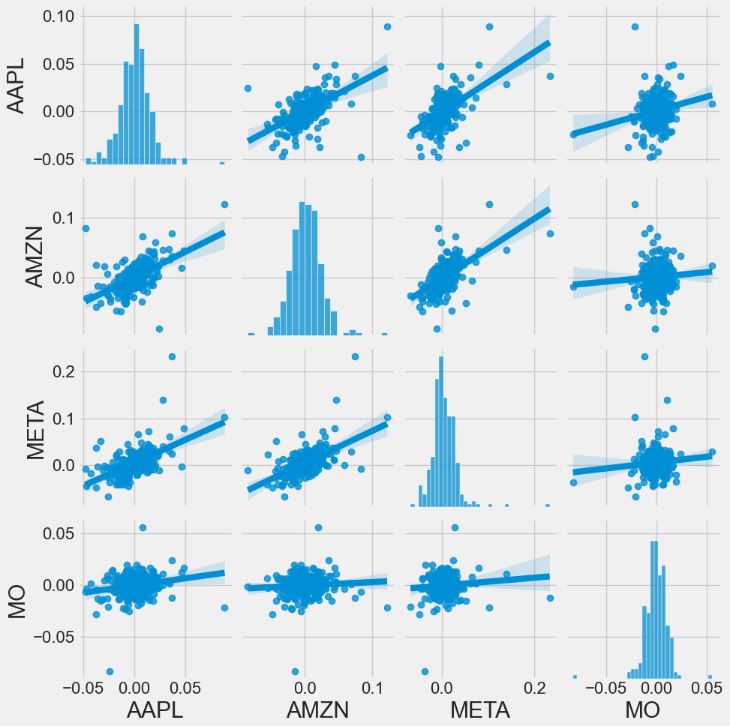

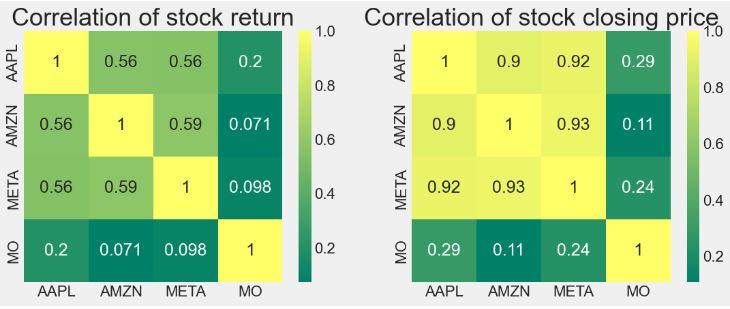

- Stock correlations of portfolio 1

#What was the correlation between different stocks closing prices?

# Grab all the closing prices for the tech stock list into one DataFrame

closing_df = pdr.get_data_yahoo(tech_list, start=start, end=end)['Adj Close']

# Make a new tech returns DataFrame

tech_rets = closing_df.pct_change()

tech_rets.head()

[*********************100%***********************] 4 of 4 completed

# We can simply call pairplot on our DataFrame for an automatic visual analysis

# of all the comparisons

sns.pairplot(tech_rets, kind='reg')

- Correlation matrix of portfolio 1: stock returns vs closing price

plt.figure(figsize=(12, 10))

plt.subplot(2, 2, 1)

sns.heatmap(tech_rets.corr(), annot=True, cmap='summer')

plt.title('Correlation of stock return')

plt.subplot(2, 2, 2)

sns.heatmap(closing_df.corr(), annot=True, cmap='summer')

plt.title('Correlation of stock closing price')

- Risk-return mapping of portfolio 1

#How much value do we put at risk by investing in a particular stock?

rets = tech_rets.dropna()

area = np.pi * 20

plt.figure(figsize=(10, 8))

plt.scatter(rets.mean(), rets.std(), s=area)

plt.xlabel('Expected return')

plt.ylabel('Risk')

for label, x, y in zip(rets.columns, rets.mean(), rets.std()):

plt.annotate(label, xy=(x, y), xytext=(50, 50), textcoords='offset points', ha='right', va='bottom',

arrowprops=dict(arrowstyle='-', color='blue', connectionstyle='arc3,rad=-0.3'))

plt.grid(lw=3)

plt.show()

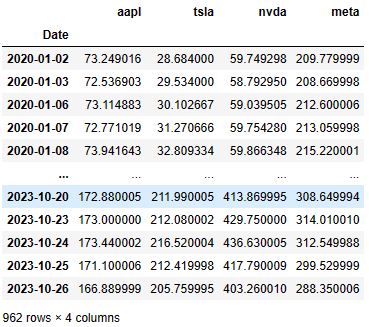

Portfolio 2: (DIS, AMD) + (AAPL, TSLA)

- In this section, we will invoke Quantstats to optimize portfolio 2 that consists of Apple, Tesla, The Walt Disney Company, and AMD stocks.

- Reading input stock data from yfinance

import yfinance as yf

startdate='2020-01-01'

enddate='2023-10-27'

# Getting dataframes info for Stocks using yfinance

aapl_df = yf.download('AAPL', start = startdate, end = enddate)

tsla_df = yf.download('TSLA', start = startdate, end = enddate)

dis_df = yf.download('NVDA', start = startdate, end = enddate)

amd_df = yf.download('META', start = startdate, end = enddate)

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

# Extracting Adjusted Close for each stock

aapl_df = aapl_df['Adj Close']

tsla_df = tsla_df['Adj Close']

dis_df = dis_df['Adj Close']

amd_df = amd_df['Adj Close']

# Merging and creating an Adj Close dataframe for stocks

df = pd.concat([aapl_df, tsla_df, dis_df, amd_df], join = 'outer', axis = 1)

df.columns = ['aapl', 'tsla', 'nvda', 'meta']

df # Visualizing dataframe for input

- Optimizing portfolio 2 in terms of max Sharpe ratio and Efficient Frontier

# Importing libraries for portfolio optimization

from pypfopt.efficient_frontier import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

# Calculating the annualized expected returns and the annualized sample covariance matrix

mu = expected_returns.mean_historical_return(df) #expected returns

S = risk_models.sample_cov(df) #Covariance matrix

# Visualizing the annualized expected returns

mu

aapl 0.241023

tsla 0.676460

nvda 0.649880

meta 0.086997

dtype: float64

# Visualizing the covariance matrix

S

aapl tsla nvda meta

aapl 0.116819 0.121311 0.126178 0.098940

tsla 0.121311 0.477221 0.200507 0.120923

nvda 0.126178 0.200507 0.303958 0.148242

meta 0.098940 0.120923 0.148242 0.226365

# Optimizing for maximal Sharpe ratio

ef = EfficientFrontier(mu, S) # Providing expected returns and covariance matrix as input

weights = ef.max_sharpe() # Optimizing weights for Sharpe ratio maximization

clean_weights = ef.clean_weights() # clean_weights rounds the weights and clips near-zeros

# Printing optimized weights and expected performance for portfolio

clean_weights

OrderedDict([('aapl', 0.0),

('tsla', 0.30239),

('nvda', 0.69761),

('meta', 0.0)])

#Original portfolio (benchmark)

portfolio = tsla_df*0.25 + dis_df*0.25+aapl_df*0.25+amd_df*0.25

# Creating new portfolio with optimized weights

new_weights = [0.65871, 0.34129]

optimized_portfolio = tsla_df*new_weights[0] + aapl_df*new_weights[1]

optimized_portfolio # Visualizing daily returns

Date

2020-01-02 43.893594

2020-01-03 44.210453

2020-01-06 44.782306

2020-01-07 45.434324

2020-01-08 46.847374

...

2023-10-20 198.642153

2023-10-23 198.742388

2023-10-24 201.817230

2023-10-25 198.317898

2023-10-26 192.494054

Name: Adj Close, Length: 962, dtype: float64

# Displaying new reports comparing the optimized portfolio to the first portfolio constructed

from IPython.core.display import display, HTML

display(HTML("<style>div.output_scroll { height: 144em; }</style>"))

import quantstats as qs

qs.reports.full(optimized_portfolio, benchmark = portfolio)

Performance Metrics

Strategy Benchmark

------------------------- ---------- -----------

Start Period 2020-01-02 2020-01-02

End Period 2023-10-26 2023-10-26

Risk-Free Rate 0.0% 0.0%

Time in Market 100.0% 100.0%

Cumulative Return 338.55% 82.5%

CAGR﹪ 47.31% 17.07%

Sharpe 0.99 0.6

Prob. Sharpe Ratio 97.28% 87.8%

Smart Sharpe 0.94 0.57

Sortino 1.45 0.85

Smart Sortino 1.38 0.81

Sortino/√2 1.02 0.6

Smart Sortino/√2 0.98 0.57

Omega 1.19 1.19

Max Drawdown -65.0% -56.61%

Longest DD Days 660 660

Volatility (ann.) 53.88% 39.1%

R^2 0.86 0.86

Information Ratio 0.08 0.08

Calmar 0.73 0.3

Skew -0.13 -0.24

Kurtosis 2.21 2.38

Expected Daily % 0.15% 0.06%

Expected Monthly % 3.27% 1.32%

Expected Yearly % 44.71% 16.23%

Kelly Criterion 7.65% 4.69%

Risk of Ruin 0.0% 0.0%

Daily Value-at-Risk -5.37% -3.96%

Expected Shortfall (cVaR) -5.37% -3.96%

Max Consecutive Wins 13 11

Max Consecutive Losses 8 8

Gain/Pain Ratio 0.19 0.11

Gain/Pain (1M) 0.97 0.53

Payoff Ratio 1.01 0.93

Profit Factor 1.19 1.11

Common Sense Ratio 1.25 1.08

CPC Index 0.64 0.56

Tail Ratio 1.05 0.97

Outlier Win Ratio 3.0 4.24

Outlier Loss Ratio 3.15 4.11

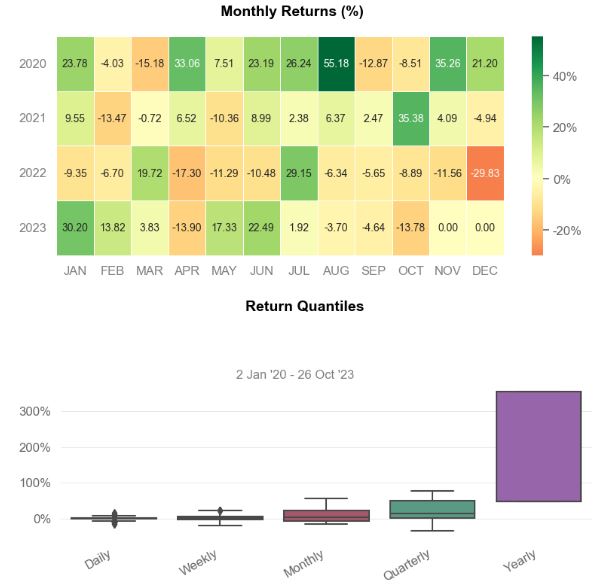

MTD -13.78% -9.78%

3M -20.04% -16.91%

6M 19.14% 7.97%

YTD 53.63% 35.1%

1Y -2.88% 1.19%

3Y (ann.) 5.44% 0.3%

5Y (ann.) 47.31% 17.07%

10Y (ann.) 47.31% 17.07%

All-time (ann.) 47.31% 17.07%

Best Day 15.9% 12.86%

Worst Day -16.67% -12.25%

Best Month 55.18% 30.87%

Worst Month -29.83% -21.91%

Best Year 354.51% 113.44%

Worst Year -57.1% -51.11%

Avg. Drawdown -10.07% -7.7%

Avg. Drawdown Days 50 51

Recovery Factor 5.21 1.46

Ulcer Index 0.28 0.25

Serenity Index 0.85 0.18

Avg. Up Month 19.01% 11.77%

Avg. Down Month -10.16% -7.98%

Win Days % 53.69% 54.01%

Win Month % 52.17% 50.0%

Win Quarter % 68.75% 56.25%

Win Year % 75.0% 75.0%

Beta 1.27 -

Alpha 0.23 -

Correlation 92.49% -

Treynor Ratio 265.64% -

None

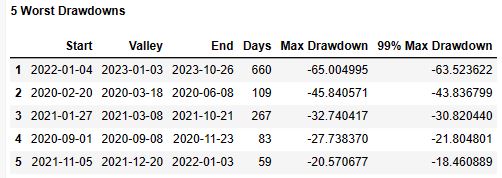

5 Worst Drawdowns

Start Valley End Days Max Drawdown 99% Max Drawdown

1 2022-01-04 2023-01-03 2023-10-26 660 -65.004995 -63.523622

2 2020-02-20 2020-03-18 2020-06-08 109 -45.840571 -43.836799

3 2021-01-27 2021-03-08 2021-10-21 267 -32.740417 -30.820440

4 2020-09-01 2020-09-08 2020-11-23 83 -27.738370 -21.804801

5 2021-11-05 2021-12-20 2022-01-03 59 -20.570677 -18.460889

- Let’s build the entire portfolio optimization (PO) pipeline

# Importing libraries

import pandas as pd

import numpy as np

import quantstats as qs

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.linear_model import LinearRegression

import plotly.express as px

import yfinance as yf

# Getting daily returns for 4 different US stocks in the same time window

aapl = qs.utils.download_returns('AAPL')

aapl = aapl.loc[startdate:enddate]

tsla = qs.utils.download_returns('TSLA')

tsla = tsla.loc[startdate:enddate]

dis = qs.utils.download_returns('DIS')

dis = dis.loc[startdate:enddate]

amd = qs.utils.download_returns('AMD')

amd = amd.loc[startdate:enddate]

# Plotting Daily Returns for each stock

print('\nApple Daily Returns Plot:\n')

qs.plots.daily_returns(aapl)

print('\nTesla Inc. Daily Returns Plot:\n')

qs.plots.daily_returns(tsla)

print('\nThe Walt Disney Company Daily Returns Plot:\n')

qs.plots.daily_returns(dis)

print('\nAdvances Micro Devices, Inc. Daily Returns Plot:\n')

qs.plots.daily_returns(amd)

- Plotting histograms of the above daily returns

# Plotting histograms

from IPython.core.display import display, HTML

display(HTML("<style>div.output_scroll { height: 144em; }</style>"))

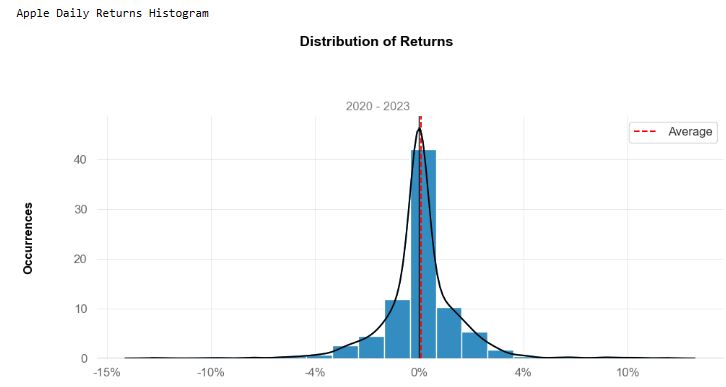

print('\nApple Daily Returns Histogram')

qs.plots.histogram(aapl, resample = 'D')

print('\nTesla Inc. Daily Returns Histogram')

qs.plots.histogram(tsla, resample = 'D')

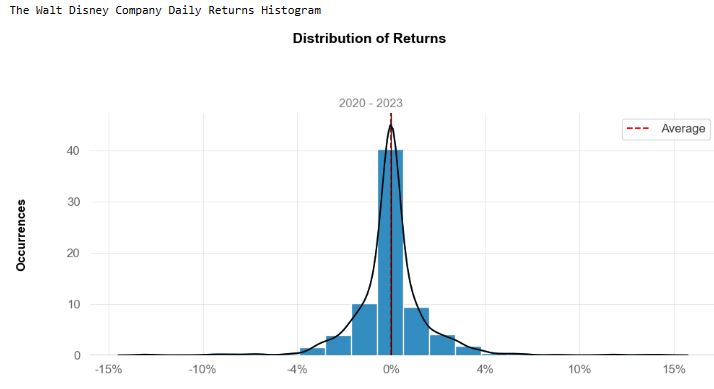

print('\nThe Walt Disney Company Daily Returns Histogram')

qs.plots.histogram(dis, resample = 'D')

print('\nAdvances Micro Devices, Inc. Daily Returns Histogram')

qs.plots.histogram(amd, resample = 'D')

- Comparing cumulative returns of these 4 stocks in a single line plot

fig, ax = plt.subplots()

((aapl + 1).cumprod() - 1).plot(ax=ax)

((tsla + 1).cumprod() - 1).plot(ax=ax)

((dis + 1).cumprod() - 1).plot(ax=ax)

((amd + 1).cumprod() - 1).plot(ax=ax)

ax.legend(["AAPL","TSLA","DIS","AMD"]);

- Comparing STD, kurtosis, and skewness of these 4 stocks

# Using quantstats to measure kurtosis

print("Apple's kurtosis: ", qs.stats.kurtosis(aapl).round(2))

print("Tesla's kurtosis: ", qs.stats.kurtosis(tsla).round(2))

print("Walt Disney's kurtosis: ", qs.stats.kurtosis(dis).round(3))

print("Advances Micro Devices' kurtosis: ", qs.stats.kurtosis(amd).round(3))

Apple's kurtosis: 4.67

Tesla's kurtosis: 2.78

Walt Disney's kurtosis: 7.357

Advances Micro Devices' kurtosis: 2.1

# Measuring skewness with quantstats

print("Apple's skewness: ", qs.stats.skew(aapl).round(2))

print("Tesla's skewness: ", qs.stats.skew(tsla).round(2))

print("Walt Disney's skewness: ", qs.stats.skew(dis).round(3))

print("Advances Micro Devices' skewness: ", qs.stats.skew(amd).round(3))

Apple's skewness: 0.08

Tesla's skewness: 0.08

Walt Disney's skewness: 0.28

Advances Micro Devices' skewness: 0.202

# Calculating Standard Deviations

print("Apple's Standard Deviation: ", aapl.std())

print("\nTesla's Standard Deviation: ", tsla.std())

print("\nDisney's Standard Deviation: ", dis.std())

print("\nAMD's Standard Deviation: ", amd.std())

Apple's Standard Deviation: 0.021520708530783472

Tesla's Standard Deviation: 0.043479817357367966

Disney's Standard Deviation: 0.02271810742856512

AMD's Standard Deviation: 0.03403554120470168

- Let’s compare portfolio 2 against the most popular S&P 500 benchmark

# Loading data from the SP500, the American benchmark

sp500 = qs.utils.download_returns('^GSPC')

sp500 = sp500.loc[startdate:enddate]

sp500.index = sp500.index.tz_convert(None)

aapl_no_index=aapl.reset_index(drop=True)

sp500_no_index=sp500.reset_index(drop=True)

# Fitting linear relation among Apple's returns and Benchmark

X = sp500_no_index.values.reshape(-1,1)

y = aapl_no_index.values.reshape(-1,1)

linreg = LinearRegression().fit(X, y)

beta = linreg.coef_[0]

alpha = linreg.intercept_

print('AAPL beta: ', beta.round(3))

print('\nAAPL alpha: ', alpha.round(3))

AAPL beta: [1.194]

AAPL alpha: [0.001]

tsla_no_index=tsla.reset_index(drop=True)

dis_no_index=dis.reset_index(drop=True)

amd_no_index=amd.reset_index(drop=True)

X = sp500_no_index.values.reshape(-1,1)

y = tsla_no_index.values.reshape(-1,1)

linreg = LinearRegression().fit(X, y)

beta = linreg.coef_[0]

alpha = linreg.intercept_

print('TSLA beta: ', beta.round(3))

print('\nTSLA alpha: ', alpha.round(3))

TSLA beta: [1.516]

TSLA alpha: [0.002]

X = sp500_no_index.values.reshape(-1,1)

y = dis_no_index.values.reshape(-1,1)

linreg = LinearRegression().fit(X, y)

beta = linreg.coef_[0]

alpha = linreg.intercept_

print('DIS beta: ', beta.round(3))

print('\nDIS alpha: ', alpha.round(3))

DIS beta: [1.075]

DIS alpha: [-0.001]

X = sp500_no_index.values.reshape(-1,1)

y = amd_no_index.values.reshape(-1,1)

linreg = LinearRegression().fit(X, y)

beta = linreg.coef_[0]

alpha = linreg.intercept_

print('AMD beta: ', beta.round(3))

print('\nAMD alpha: ', alpha.round(3))

AMD beta: [1.508]

AMD alpha: [0.001]

- Calculating the Sharpe Ratio

# Calculating the Sharpe ratio

print("Sharpe Ratio for AAPL: ", qs.stats.sharpe(aapl).round(2))

print("Sharpe Ratio for TSLA: ", qs.stats.sharpe(tsla).round(2))

print("Sharpe Ratio for DIS: ", qs.stats.sharpe(dis).round(2))

print("Sharpe Ratio for AMD: ", qs.stats.sharpe(amd).round(2))

Sharpe Ratio for AAPL: 0.82

Sharpe Ratio for TSLA: 1.11

Sharpe Ratio for DIS: -0.26

Sharpe Ratio for AMD: 0.63

- Summary of the Portfolio Optimization (PO) workflow applied to portfolio 2

# Getting dataframes info for Stocks using yfinance

aapl_df = yf.download('AAPL', start = startdate, end = enddate)

tsla_df = yf.download('TSLA', start = startdate, end = enddate)

dis_df = yf.download('DIS', start = startdate, end = enddate)

amd_df = yf.download('AMD', start = startdate, end = enddate)

# Extracting Adjusted Close for each stock

aapl_df = aapl_df['Adj Close']

tsla_df = tsla_df['Adj Close']

dis_df = dis_df['Adj Close']

amd_df = amd_df['Adj Close']

# Merging and creating an Adj Close dataframe for stocks

df = pd.concat([aapl_df, tsla_df, dis_df, amd_df], join = 'outer', axis = 1)

df.columns = ['aapl', 'tsla', 'dis', 'amd']

# Importing libraries for portfolio optimization

from pypfopt.efficient_frontier import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

# Calculating the annualized expected returns and the annualized sample covariance matrix

mu = expected_returns.mean_historical_return(df) #expected returns

S = risk_models.sample_cov(df) #Covariance matrix

# Visualizing the annualized expected returns

mu

aapl 0.241023

tsla 0.676460

dis -0.149894

amd 0.184567

dtype: float64

# Visualizing the covariance matrix

S

aapl tsla dis amd

aapl 0.116818 0.121311 0.060739 0.112920

tsla 0.121311 0.477221 0.088326 0.180042

dis 0.060739 0.088326 0.130159 0.077896

amd 0.112920 0.180042 0.077896 0.291059

# Optimizing for maximal Sharpe ratio

ef = EfficientFrontier(mu, S) # Providing expected returns and covariance matrix as input

weights = ef.max_sharpe() # Optimizing weights for Sharpe ratio maximization

clean_weights = ef.clean_weights() # clean_weights rounds the weights and clips near-zeros

# Printing optimized weights and expected performance for portfolio

clean_weights

rderedDict([('aapl', 0.34129), ('tsla', 0.65871), ('dis', 0.0), ('amd', 0.0)])

#Benchmark portfolio

portfolio = aapl*0.25 + tsla*0.25+dis*0.25+amd*0.25

# Creating new portfolio with optimized weights

new_weights = [0.34129, 0.65871]

optimized_portfolio = aapl*new_weights[0] + tsla*new_weights[1]

optimized_portfolio # Visualizing daily returns

- Comparing portfolio 2 cumulative returns % before and after portfolio optimization (PO)

# Displaying new reports comparing the optimized portfolio to the first portfolio constructed

#https://stackoverflow.com/questions/40204396/plot-cumulative-returns-of-a-pandas-dataframe

fig, ax = plt.subplots()

((optimized_portfolio + 1).cumprod() - 1).plot(ax=ax)

((portfolio + 1).cumprod() - 1).plot(ax=ax)

ax.legend(["After PO","Before PO"]);

plt.title('Portfolio Cumulative Return')

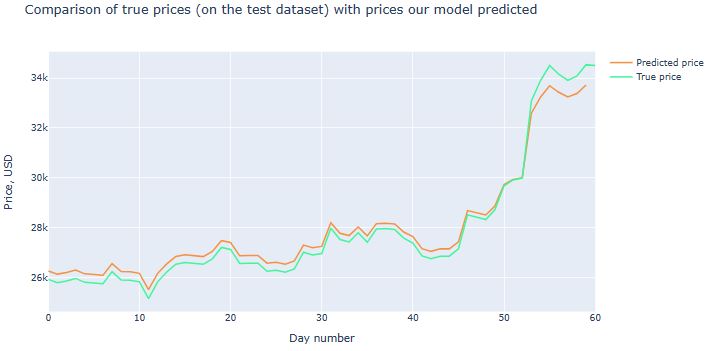

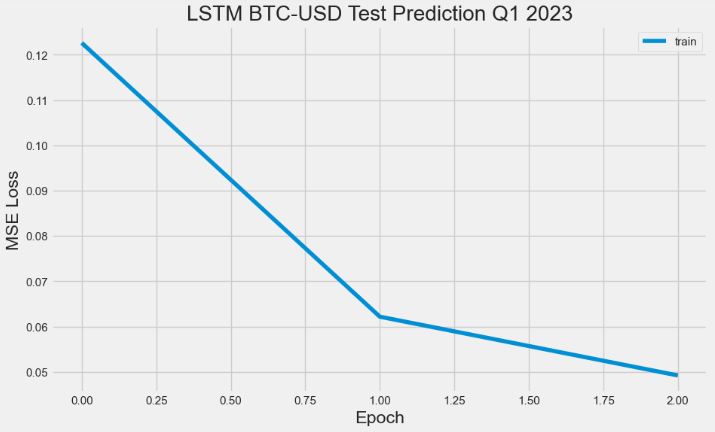

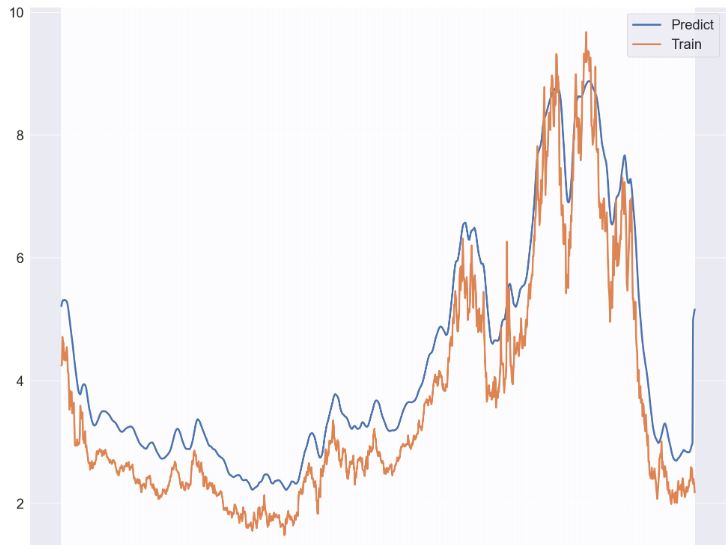

AAPL Price LSTM Forecasting

- It appears that AAPL is the most appealing asset of portfolio 1 in terms of risk/return balance.

- Let’s predict the AAPL price using Keras LSTM

#Predicting the closing price stock price of APPLE inc:

# Get the stock quote

df = pdr.get_data_yahoo('AAPL', start='2012-01-01', end=datetime.now())

[*********************100%***********************] 1 of 1 completed

plt.figure(figsize=(16,6))

plt.title('Close Price History')

plt.plot(df['Close'],linewidth=3)

plt.xlabel('Date', fontsize=18)

plt.ylabel('Close Price USD ($)', fontsize=18)

plt.grid(lw=3)

plt.show()

- Train/test data preparation

# Create a new dataframe with only the 'Close column

data = df.filter(['Close'])

# Convert the dataframe to a numpy array

dataset = data.values

# Get the number of rows to train the model on

training_data_len = int(np.ceil( len(dataset) * .95 ))

training_data_len

2828

# Scale the data

from sklearn.preprocessing import StandardScaler

#scaler = MinMaxScaler(feature_range=(0,1))

scaler = StandardScaler()

scaled_data = scaler.fit_transform(dataset)

# Create the training data set

# Create the scaled training data set

train_data = scaled_data[0:int(training_data_len), :]

# Split the data into x_train and y_train data sets

x_train = []

y_train = []

for i in range(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])

if i<= 61:

print(x_train)

print(y_train)

print()

# Convert the x_train and y_train to numpy arrays

x_train, y_train = np.array(x_train), np.array(y_train)

# Reshape the data

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

# Create the testing data set

# Create a new array containing scaled values from index 1543 to 2002

test_data = scaled_data[training_data_len - 60: , :]

# Create the data sets x_test and y_test

x_test = []

y_test = dataset[training_data_len:, :]

for i in range(60, len(test_data)):

x_test.append(test_data[i-60:i, 0])

# Convert the data to a numpy array

x_test = np.array(x_test)

# Reshape the data

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1 ))

- Train the model and get test predictions

from keras.models import Sequential

from keras.layers import Dense, LSTM

# Build the LSTM model

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

# Compile the model

model.compile(optimizer='adam', loss='mean_squared_error')

# Train the model

model.fit(x_train, y_train, batch_size=1, epochs=1)

2768/2768 [==============================] - 38s 13ms/step - loss: 0.0081

# Get the models predicted price values

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

# Get the root mean squared error (RMSE)

rmse = np.sqrt(np.mean(((predictions - y_test) ** 2)))

rmse

5.9636350262044076

# Plot the data

train = data[:training_data_len]

valid = data[training_data_len:]

valid['Predictions'] = predictions

# Visualize the data

plt.figure(figsize=(16,6))

plt.title('Model')

plt.xlabel('Date', fontsize=18)

plt.ylabel('Close Price USD ($)', fontsize=18)

plt.plot(train['Close'],linewidth=3)

plt.plot(valid[['Close', 'Predictions']],linewidth=3)

plt.legend(['Train', 'Val', 'Predictions'], loc='lower right')

plt.grid(lw=3)

plt.show()

NVDA Entry/Exit Trading Signals

- In this section, we will implement the NVIDIA trading dashboard with Yfinance & Python

# Import libraries and dependencies

import numpy as np

import pandas as pd

import hvplot.pandas

from pathlib import Path

import yfinance as yf

#Define ticker

net = yf.Ticker("NVDA")

net

# Set the timeframe you are interested in viewing.

net_historical = net.history(start="2020-01-1", end="2023-10-30", interval="1d")

# Create a new DataFrame called signals, keeping only the 'Date' & 'Close' columns.

signals_df = net_historical.drop(columns=['Open', 'High', 'Low', 'Volume','Dividends', 'Stock Splits'])

- Calculating the short/long window smooth moving averages (SMAs) for 50 and 100 days

# Set the short window and long windows

short_window = 50

long_window = 100

# Generate the short and long moving averages (50 and 100 days, respectively)

signals_df['SMA50'] = signals_df['Close'].rolling(window=short_window).mean()

signals_df['SMA100'] = signals_df['Close'].rolling(window=long_window).mean()

signals_df['Signal'] = 0.0

# Generate the trading signal 0 or 1,

# where 0 is when the SMA50 is under the SMA100, and

# where 1 is when the SMA50 is higher (or crosses over) the SMA100

signals_df['Signal'][short_window:] = np.where(

signals_df['SMA50'][short_window:] > signals_df['SMA100'][short_window:], 1.0, 0.0

)

# Calculate the points in time at which a position should be taken, 1 or -1

signals_df['Entry/Exit'] = signals_df['Signal'].diff()

# Print the DataFrame

signals_df.tail(10)

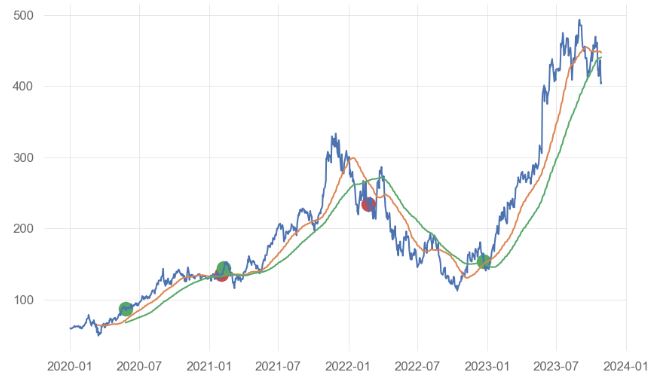

- Plotting the Entry/Exit trading signals

signals_df1=signals_df.reset_index()

# Visualize exit position relative to close price

sigx=signals_df1[signals_df1['Entry/Exit'] == -1.0]['Date']

sigy=signals_df1[signals_df1['Entry/Exit'] == -1.0]['Close']

plt.scatter(sigx,sigy,s=170,c='r')

sigx=signals_df1[signals_df1['Entry/Exit'] == 1.0]['Date']

sigy=signals_df1[signals_df1['Entry/Exit'] == 1.0]['Close']

plt.scatter(sigx,sigy,s=170,c='g')

sigx=signals_df1['Date']

sigy=signals_df1['Close']

plt.plot(sigx,sigy)

sigx=signals_df1['Date']

sigy=signals_df1['SMA50']

plt.plot(sigx,sigy)

sigx=signals_df1['Date']

sigy=signals_df1['SMA100']

plt.plot(sigx,sigy)

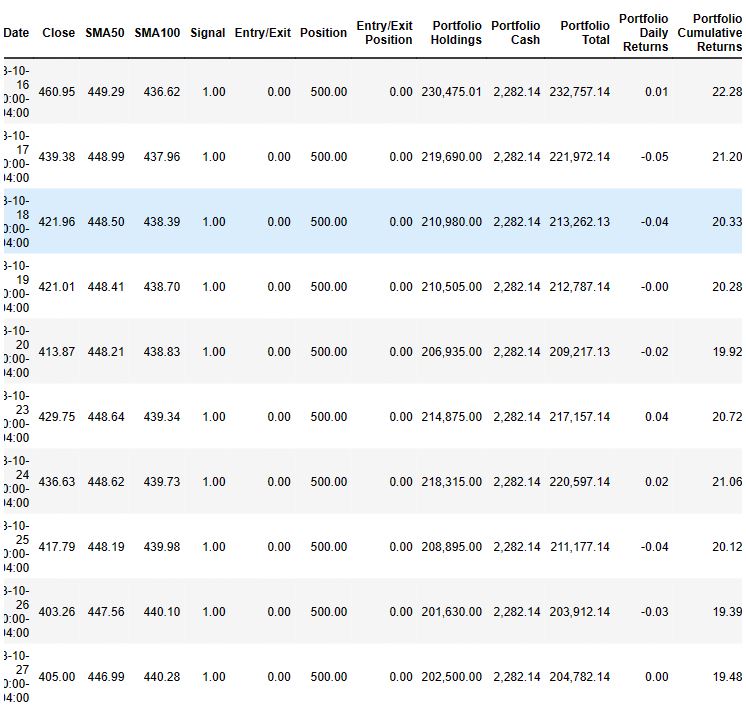

- Calculating the portfolio returns by setting initial_capital = float(10000)

# Set initial capital

initial_capital = float(10000)

# Set the share size

share_size = 500

# Take a 500 share position where the dual moving average crossover is 1 (SMA50 is greater than SMA100)

signals_df1['Position'] = share_size * signals_df1['Signal']

# Find the points in time where a 500 share position is bought or sold

signals_df1['Entry/Exit Position'] = signals_df1['Position'].diff()

# Multiply share price by entry/exit positions and get the cumulatively sum

signals_df1['Portfolio Holdings'] = signals_df1['Close'] * signals_df1['Entry/Exit Position'].cumsum()

# Subtract the initial capital by the portfolio holdings to get the amount of liquid cash in the portfolio

signals_df1['Portfolio Cash'] = initial_capital - (signals_df1['Close'] * signals_df1['Entry/Exit Position']).cumsum()

# Get the total portfolio value by adding the cash amount by the portfolio holdings (or investments)

signals_df1['Portfolio Total'] = signals_df1['Portfolio Cash'] + signals_df1['Portfolio Holdings']

# Calculate the portfolio daily returns

signals_df1['Portfolio Daily Returns'] = signals_df1['Portfolio Total'].pct_change()

# Calculate the cumulative returns

signals_df1['Portfolio Cumulative Returns'] = (1 + signals_df1['Portfolio Daily Returns']).cumprod() - 1

# Print the DataFrame

signals_df1.tail(10)

- Plotting portfolio cumulative returns vs trading signals

sigx=signals_df1[signals_df1['Entry/Exit'] == -1.0]['Date']

sigy=signals_df1[signals_df1['Entry/Exit'] == -1.0]['Portfolio Total']

plt.scatter(sigx,sigy,s=150,c='red')

sigx=signals_df1[signals_df1['Entry/Exit'] == 1.0]['Date']

sigy=signals_df1[signals_df1['Entry/Exit'] == 1.0]['Portfolio Total']

plt.scatter(sigx,sigy,s=150,c='green')

sigx=signals_df1['Date']

sigy=signals_df1['Portfolio Total']

plt.plot(sigx,sigy)

- Initiating the NVDA portfolio evaluation process based on signals_df1

# Prepare DataFrame for metrics

metrics = [

'Annual Return',

'Cumulative Returns',

'Annual Volatility',

'Sharpe Ratio',

'Sortino Ratio']

columns = ['Backtest']

# Initialize the DataFrame with index set to evaluation metrics and column as `Backtest` (just like PyFolio)

portfolio_evaluation_df = pd.DataFrame(index=metrics, columns=columns)

# Calculate cumulative return

portfolio_evaluation_df.loc['Cumulative Returns'] = signals_df1['Portfolio Cumulative Returns'].iloc[-1]

# Calculate annualized return

portfolio_evaluation_df.loc['Annual Return'] = (

signals_df1['Portfolio Daily Returns'].mean() * 252

)

# Calculate annual volatility

portfolio_evaluation_df.loc['Annual Volatility'] = (

signals_df1['Portfolio Daily Returns'].std() * np.sqrt(252)

)

# Calculate Sharpe Ratio

portfolio_evaluation_df.loc['Sharpe Ratio'] = (

signals_df1['Portfolio Daily Returns'].mean() * 252) / (

signals_df1['Portfolio Daily Returns'].std() * np.sqrt(252)

)

# Calculate Downside Return

sortino_ratio_df = signals_df1[['Portfolio Daily Returns']].copy()

sortino_ratio_df.loc[:,'Downside Returns'] = 0

target = 0

mask = sortino_ratio_df['Portfolio Daily Returns'] < target

sortino_ratio_df.loc[mask, 'Downside Returns'] = sortino_ratio_df['Portfolio Daily Returns']**2

portfolio_evaluation_df

# Calculate Sortino Ratio

down_stdev = np.sqrt(sortino_ratio_df['Downside Returns'].mean()) * np.sqrt(252)

expected_return = sortino_ratio_df['Portfolio Daily Returns'].mean() * 252

sortino_ratio = expected_return/down_stdev

portfolio_evaluation_df.loc['Sortino Ratio'] = sortino_ratio

portfolio_evaluation_df.head()

Backtest

--------------------------

Annual Return 1.01

Cumulative Returns 19.48

Annual Volatility 0.66

Sharpe Ratio 1.53

Sortino Ratio 2.47

# Initialize trade evaluation DataFrame with columns.

trade_evaluation_df = pd.DataFrame(

columns=[

'Stock',

'Entry Date',

'Exit Date',

'Shares',

'Entry Share Price',

'Exit Share Price',

'Entry Portfolio Holding',

'Exit Portfolio Holding',

'Profit/Loss']

)

print (row)

Close 403.26

SMA50 447.56

SMA100 440.10

Signal 1.00

Entry/Exit 0.00

Name: 2023-10-26 00:00:00-04:00, dtype: float64

# Initialize iterative variables

entry_date = ''

exit_date = ''

entry_portfolio_holding = 0

exit_portfolio_holding = 0

share_size = 0

entry_share_price = 0

exit_share_price = 0

for index, row in signals_df.iterrows():

if row['Entry/Exit'] == 1:

entry_date = index

entry_portfolio_holding = abs(row['Close'] * row['Entry/Exit'])

share_size = row['Entry/Exit']

entry_share_price = row['Close']

elif row['Entry/Exit'] == -1:

exit_date = index

exit_portfolio_holding = abs(row['Close'] * row['Entry/Exit'])

exit_share_price = row['Close']

profit_loss = entry_portfolio_holding - exit_portfolio_holding

trade_evaluation_df = trade_evaluation_df.append(

{

'Stock': 'NVDA',

'Entry Date': entry_date,

'Exit Date': exit_date,

'Shares': share_size,

'Entry Share Price': entry_share_price,

'Exit Share Price': exit_share_price,

'Entry Portfolio Holding': entry_portfolio_holding,

'Exit Portfolio Holding': exit_portfolio_holding,

'Profit/Loss': profit_loss

},

ignore_index=True)

price_df = signals_df[['Close', 'SMA50', 'SMA100']]

print(price_df)

Close SMA50 SMA100

Date

2020-01-02 00:00:00-05:00 59.75 NaN NaN

2020-01-03 00:00:00-05:00 58.79 NaN NaN

2020-01-06 00:00:00-05:00 59.04 NaN NaN

2020-01-07 00:00:00-05:00 59.75 NaN NaN

2020-01-08 00:00:00-05:00 59.87 NaN NaN

... ... ... ...

2023-10-23 00:00:00-04:00 429.75 448.64 439.34

2023-10-24 00:00:00-04:00 436.63 448.62 439.73

2023-10-25 00:00:00-04:00 417.79 448.19 439.98

2023-10-26 00:00:00-04:00 403.26 447.56 440.10

2023-10-27 00:00:00-04:00 405.00 446.99 440.28

[963 rows x 3 columns]

plt.plot(signals_df['Close'])

plt.plot(signals_df['SMA50'])

plt.plot(signals_df['SMA100']

portfolio_evaluation_df.reset_index(inplace=True)

print(portfolio_evaluation_df)

index Backtest

-------------------------------

0 Annual Return 1.01

1 Cumulative Returns 19.48

2 Annual Volatility 0.66

3 Sharpe Ratio 1.53

4 Sortino Ratio 2.47

NVDA Fundamental Analysis

- Based upon the highly encouraging outcome of the aforementioned NVDA portfolio evaluation procedure, let’s dive deeper into the stock’s fundamentals using the Financial Modeling Prep API:

#Retrieve Company Fundamentals with Python

import pandas as pd

import requests

pd.options.display.float_format = '{:,.2f}'.format

#pass ticker of the company

company = 'NVDA'

api = 'YOUR FMP API KEY'

# Request Financial Data from API and load to variables

IS = requests.get(f'https://financialmodelingprep.com/api/v3/income-statement/{company}?apikey={api}').json()

BS = requests.get(f'https://financialmodelingprep.com/api/v3/balance-sheet-statement/{company}?apikey={api}').json()

CF = requests.get(f'https://financialmodelingprep.com/api/v3/cash-flow-statement/{company}?apikey={api}').json()

Ratios = requests.get(f'https://financialmodelingprep.com/api/v3/ratios/{company}?apikey={api}').json()

key_Metrics = requests.get(f'https://financialmodelingprep.com/api/v3/key-metrics/{company}?apikey={api}').json()

profile = requests.get(f'https://financialmodelingprep.com/api/v3/profile/{company}?apikey={api}').json()

millions = 1000000

#Create empty dictionary and add the financials to it

financials = {}

dates = [2023,2022,2021,2020,2019]

for item in range(5):

financials[dates[item]] ={}

#Key Metrics

financials[dates[item]]['Mkt Cap'] = key_Metrics[item]['marketCap'] /millions

financials[dates[item]]['Debt to Equity'] = key_Metrics[item]['debtToEquity']

financials[dates[item]]['Debt to Assets'] = key_Metrics[item]['debtToAssets']

financials[dates[item]]['Revenue per Share'] = key_Metrics[item]['revenuePerShare']

financials[dates[item]]['NI per Share'] = key_Metrics[item]['netIncomePerShare']

financials[dates[item]]['Revenue'] = IS[item]['revenue'] / millions

financials[dates[item]]['Gross Profit'] = IS[item]['grossProfit'] / millions

financials[dates[item]]['R&D Expenses'] = IS[item]['researchAndDevelopmentExpenses']/ millions

financials[dates[item]]['Op Expenses'] = IS[item]['operatingExpenses'] / millions

financials[dates[item]]['Op Income'] = IS[item]['operatingIncome'] / millions

financials[dates[item]]['Net Income'] = IS[item]['netIncome'] / millions

financials[dates[item]]['Cash'] = BS[item]['cashAndCashEquivalents'] / millions

financials[dates[item]]['Inventory'] = BS[item]['inventory'] / millions

financials[dates[item]]['Cur Assets'] = BS[item]['totalCurrentAssets'] / millions

financials[dates[item]]['LT Assets'] = BS[item]['totalNonCurrentAssets'] / millions

financials[dates[item]]['Int Assets'] = BS[item]['intangibleAssets'] / millions

financials[dates[item]]['Total Assets'] = BS[item]['totalAssets'] / millions

financials[dates[item]]['Cur Liab'] = BS[item]['totalCurrentLiabilities'] / millions

financials[dates[item]]['LT Debt'] = BS[item]['longTermDebt'] / millions

financials[dates[item]]['LT Liab'] = BS[item]['totalNonCurrentLiabilities'] / millions

financials[dates[item]]['Total Liab'] = BS[item]['totalLiabilities'] / millions

financials[dates[item]]['SH Equity'] = BS[item]['totalStockholdersEquity'] / millions

financials[dates[item]]['CF Operations'] = CF[item]['netCashProvidedByOperatingActivities'] / millions

financials[dates[item]]['CF Investing'] = CF[item]['netCashUsedForInvestingActivites'] / millions

financials[dates[item]]['CF Financing'] = CF[item]['netCashUsedProvidedByFinancingActivities'] / millions

financials[dates[item]]['CAPEX'] = CF[item]['capitalExpenditure'] / millions

financials[dates[item]]['FCF'] = CF[item]['freeCashFlow'] / millions

financials[dates[item]]['Dividends Paid'] = CF[item]['dividendsPaid'] / millions

#Income Statement Ratios

financials[dates[item]]['Gross Profit Margin'] = Ratios[item]['grossProfitMargin']

financials[dates[item]]['Op Margin'] = Ratios[item]['operatingProfitMargin']

financials[dates[item]]['Int Coverage'] = Ratios[item]['interestCoverage']

financials[dates[item]]['Net Profit Margin'] = Ratios[item]['netProfitMargin']

financials[dates[item]]['Dividend Yield'] = Ratios[item]['dividendYield']

#BS Ratios

financials[dates[item]]['Current Ratio'] = Ratios[item]['currentRatio']

financials[dates[item]]['Operating Cycle'] = Ratios[item]['operatingCycle']

financials[dates[item]]['Days of AP Outstanding'] = Ratios[item]['daysOfPayablesOutstanding']

financials[dates[item]]['Cash Conversion Cycle'] = Ratios[item]['cashConversionCycle']

#Return Ratios

financials[dates[item]]['ROA'] = Ratios[item]['returnOnAssets']

financials[dates[item]]['ROE'] = Ratios[item]['returnOnEquity']

financials[dates[item]]['ROCE'] = Ratios[item]['returnOnCapitalEmployed']

financials[dates[item]]['Dividend Yield'] = Ratios[item]['dividendYield']

#Price Ratios

financials[dates[item]]['PE'] = Ratios[item]['priceEarningsRatio']

financials[dates[item]]['PS'] = Ratios[item]['priceToSalesRatio']

financials[dates[item]]['PB'] = Ratios[item]['priceToBookRatio']

financials[dates[item]]['Price To FCF'] = Ratios[item]['priceToFreeCashFlowsRatio']

financials[dates[item]]['PEG'] = Ratios[item]['priceEarningsToGrowthRatio']

financials[dates[item]]['EPS'] = IS[item]['eps']

financials[dates[item]]['EPS'] = IS[item]['eps']

#Transform the dictionary into a Pandas

fundamentals = pd.DataFrame.from_dict(financials,orient='columns')

#Calculate Growth measures

fundamentals['CAGR'] = (fundamentals[2023]/fundamentals[2019])**(1/5) - 1

fundamentals['2023 growth'] = (fundamentals[2023] - fundamentals[2022] )/ fundamentals[2022]

fundamentals['2022 growth'] = (fundamentals[2022] - fundamentals[2021] )/ fundamentals[2021]

fundamentals['2021 growth'] = (fundamentals[2021] - fundamentals[2020] )/ fundamentals[2020]

fundamentals['2020 growth'] = (fundamentals[2020] - fundamentals[2019] )/ fundamentals[2019]

#Export to Excel

fundamentals.to_excel('fundamentalsnvda.xlsx')

print(fundamentals)

2023 2022 2021 2020 2019 \

Mkt Cap 476,558.94 611,170.56 326,689.16 146,281.80 83,904.00

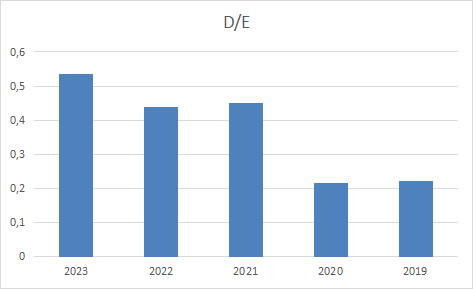

Debt to Equity 0.54 0.44 0.45 0.22 0.22

Debt to Assets 0.29 0.26 0.26 0.15 0.16

Revenue per Share 10.85 10.78 6.76 4.48 4.82

NI per Share 1.76 3.91 1.76 1.15 1.70

Revenue 26,974.00 26,914.00 16,675.00 10,918.00 11,716.00

Gross Profit 15,356.00 17,475.00 10,396.00 6,768.00 7,171.00

R&D Expenses 7,339.00 5,268.00 3,924.00 2,829.00 2,376.00

Op Expenses 9,779.00 7,434.00 5,864.00 3,922.00 3,367.00

Op Income 4,224.00 10,041.00 4,532.00 2,846.00 3,804.00

Net Income 4,368.00 9,752.00 4,332.00 2,796.00 4,141.00

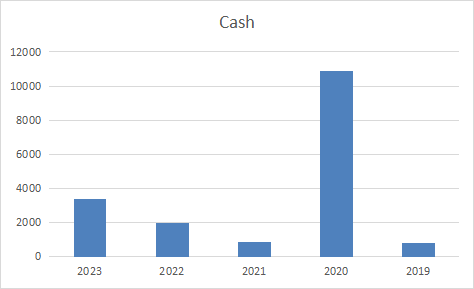

Cash 3,389.00 1,990.00 847.00 10,896.00 782.00

Inventory 5,159.00 2,605.00 1,826.00 979.00 1,575.00

Cur Assets 23,073.00 28,829.00 16,055.00 13,690.00 10,557.00

LT Assets 18,109.00 15,358.00 12,736.00 3,625.00 2,735.00

Int Assets 1,676.00 2,339.00 2,737.00 49.00 45.00

Total Assets 41,182.00 44,187.00 28,791.00 17,315.00 13,292.00

Cur Liab 6,563.00 4,335.00 3,925.00 1,784.00 1,329.00

LT Debt 10,605.00 11,687.00 6,598.00 2,552.00 1,988.00

LT Liab 12,518.00 13,240.00 7,973.00 3,327.00 2,621.00

Total Liab 19,081.00 17,575.00 11,898.00 5,111.00 3,950.00

SH Equity 22,101.00 26,612.00 16,893.00 12,204.00 9,342.00

CF Operations 5,641.00 9,108.00 5,822.00 4,761.00 3,743.00

CF Investing 7,375.00 -9,830.00 -19,675.00 6,145.00 -4,097.00

CF Financing -11,617.00 1,865.00 3,804.00 -792.00 -2,866.00

CAPEX -1,833.00 -976.00 -1,128.00 -489.00 -600.00

FCF 3,808.00 8,132.00 4,694.00 4,272.00 3,143.00

Dividends Paid -398.00 -399.00 -395.00 -390.00 -371.00

Gross Profit Margin 0.57 0.65 0.62 0.62 0.61

Op Margin 0.16 0.37 0.27 0.26 0.32

Int Coverage 16.12 42.55 24.63 54.73 65.59

Net Profit Margin 0.16 0.36 0.26 0.26 0.35

Dividend Yield 0.00 0.00 0.00 0.00 0.00

Current Ratio 3.52 6.65 4.09 7.67 7.94

Operating Cycle 213.86 163.80 159.31 141.50 170.85

Days of AP Outstanding 37.48 68.95 69.81 60.42 41.04

Cash Conversion Cycle 176.38 94.85 89.50 81.08 129.81

ROA 0.11 0.22 0.15 0.16 0.31

ROE 0.20 0.37 0.26 0.23 0.44

ROCE 0.12 0.25 0.18 0.18 0.32

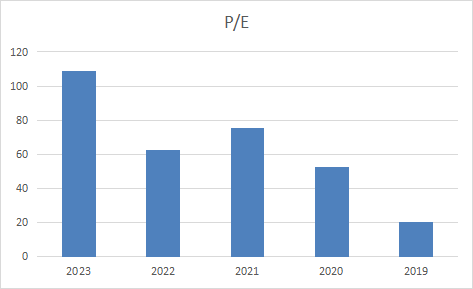

PE 109.10 62.67 75.41 52.32 20.26

PS 17.67 22.71 19.59 13.40 7.16

PB 21.56 22.97 19.34 11.99 8.98

Price To FCF 125.15 75.16 69.60 34.24 26.70

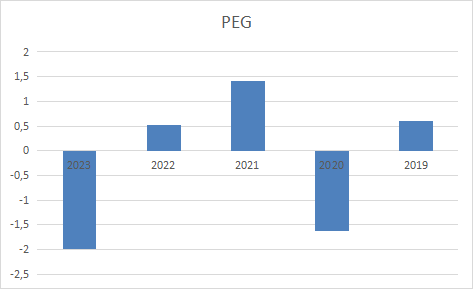

PEG -1.98 0.51 1.42 -1.62 0.60

EPS 1.76 3.91 1.76 1.15 1.70

CAGR 2023 growth 2022 growth 2021 growth \

Mkt Cap 0.42 -0.22 0.87 1.23

Debt to Equity 0.19 0.22 -0.02 1.08

Debt to Assets 0.13 0.09 0.00 0.73

Revenue per Share 0.18 0.01 0.60 0.51

NI per Share 0.01 -0.55 1.23 0.53

Revenue 0.18 0.00 0.61 0.53

Gross Profit 0.16 -0.12 0.68 0.54

R&D Expenses 0.25 0.39 0.34 0.39

Op Expenses 0.24 0.32 0.27 0.50

Op Income 0.02 -0.58 1.22 0.59

Net Income 0.01 -0.55 1.25 0.55

Cash 0.34 0.70 1.35 -0.92

Inventory 0.27 0.98 0.43 0.87

Cur Assets 0.17 -0.20 0.80 0.17

LT Assets 0.46 0.18 0.21 2.51

Int Assets 1.06 -0.28 -0.15 54.86

Total Assets 0.25 -0.07 0.53 0.66

Cur Liab 0.38 0.51 0.10 1.20

LT Debt 0.40 -0.09 0.77 1.59

LT Liab 0.37 -0.05 0.66 1.40

Total Liab 0.37 0.09 0.48 1.33

SH Equity 0.19 -0.17 0.58 0.38

CF Operations 0.09 -0.38 0.56 0.22

CF Investing NaN -1.75 -0.50 -4.20

CF Financing 0.32 -7.23 -0.51 -5.80

CAPEX 0.25 0.88 -0.13 1.31

FCF 0.04 -0.53 0.73 0.10

Dividends Paid 0.01 -0.00 0.01 0.01

Gross Profit Margin -0.01 -0.12 0.04 0.01

Op Margin -0.14 -0.58 0.37 0.04

Int Coverage -0.24 -0.62 0.73 -0.55

Net Profit Margin -0.14 -0.55 0.39 0.01

Dividend Yield -0.28 0.28 -0.46 -0.55

Current Ratio -0.15 -0.47 0.63 -0.47

Operating Cycle 0.05 0.31 0.03 0.13

Days of AP Outstanding -0.02 -0.46 -0.01 0.16

Cash Conversion Cycle 0.06 0.86 0.06 0.10

ROA -0.19 -0.52 0.47 -0.07

ROE -0.15 -0.46 0.43 0.12

ROCE -0.17 -0.52 0.38 -0.01

PE 0.40 0.74 -0.17 0.44

PS 0.20 -0.22 0.16 0.46

PB 0.19 -0.06 0.19 0.61

Price To FCF 0.36 0.67 0.08 1.03

PEG NaN -4.87 -0.64 -1.88

EPS 0.01 -0.55 1.22 0.53

2020 growth

Mkt Cap 0.74

Debt to Equity -0.03

Debt to Assets -0.02

Revenue per Share -0.07

NI per Share -0.33

Revenue -0.07

Gross Profit -0.06

R&D Expenses 0.19

Op Expenses 0.16

Op Income -0.25

Net Income -0.32

Cash 12.93

Inventory -0.38

Cur Assets 0.30

LT Assets 0.33

Int Assets 0.09

Total Assets 0.30

Cur Liab 0.34

LT Debt 0.28

LT Liab 0.27

Total Liab 0.29

SH Equity 0.31

CF Operations 0.27

CF Investing -2.50

CF Financing -0.72

CAPEX -0.18

FCF 0.36

Dividends Paid 0.05

Gross Profit Margin 0.01

Op Margin -0.20

Int Coverage -0.17

Net Profit Margin -0.28

Dividend Yield -0.40

Current Ratio -0.03

Operating Cycle -0.17

Days of AP Outstanding 0.47

Cash Conversion Cycle -0.38

ROA -0.48

ROE -0.48

ROCE -0.42

PE 1.58

PS 0.87

PB 0.33

Price To FCF 0.28

PEG -3.70

EPS -0.32

#Building an Investing Model with Fundamentals in Python

import requests

import pandas as pd

companies = []

demo = 'YOUR FMP API KEY'

marketcap = str(100000000000)

url = (f'https://financialmodelingprep.com/api/v3/stock-screener?marketCapMoreThan={marketcap}&betaMoreThan=1&volumeMoreThan=10000§or=Technology&exchange=NASDAQ÷ndMoreThan=0&limit=1000&apikey={demo}')

#get companies based on criteria defined about

screener = requests.get(url).json()

print(screener)

[{'symbol': 'AAPL', 'companyName': 'Apple Inc.', 'marketCap': 2622011606866, 'sector': 'Technology', 'industry': 'Consumer Electronics', 'beta': 1.286802, 'price': 167.71, 'lastAnnualDividend': 0.96, 'volume': 15417567, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'NVDA', 'companyName': 'NVIDIA Corporation', 'marketCap': 999628811803, 'sector': 'Technology', 'industry': 'Semiconductors', 'beta': 1.753377, 'price': 404.708, 'lastAnnualDividend': 0.16, 'volume': 13475410, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'AVGO', 'companyName': 'Broadcom Inc.', 'marketCap': 342260505384, 'sector': 'Technology', 'industry': 'Semiconductors', 'beta': 1.129, 'price': 829.25, 'lastAnnualDividend': 18.4, 'volume': 327481, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'ADBE', 'companyName': 'Adobe Inc.', 'marketCap': 232403332000, 'sector': 'Technology', 'industry': 'Software—Infrastructure', 'beta': 1.336, 'price': 510.44, 'lastAnnualDividend': 0, 'volume': 683006, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'ASML', 'companyName': 'ASML Holding N.V.', 'marketCap': 231610316000, 'sector': 'Technology', 'industry': 'Semiconductor Equipment & Materials', 'beta': 1.168, 'price': 588.74, 'lastAnnualDividend': 6.49, 'volume': 280741, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'NL', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'AMD', 'companyName': 'Advanced Micro Devices, Inc.', 'marketCap': 154441896829, 'sector': 'Technology', 'industry': 'Semiconductors', 'beta': 1.648, 'price': 95.59, 'lastAnnualDividend': 0, 'volume': 16278383, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'INTU', 'companyName': 'Intuit Inc.', 'marketCap': 133868517761, 'sector': 'Technology', 'industry': 'Software—Application', 'beta': 1.189, 'price': 477.66, 'lastAnnualDividend': 3.6, 'volume': 357351, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'TXN', 'companyName': 'Texas Instruments Incorporated', 'marketCap': 130815203755, 'sector': 'Technology', 'industry': 'Semiconductors', 'beta': 1.004849, 'price': 144.075, 'lastAnnualDividend': 4.96, 'volume': 971438, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'QCOM', 'companyName': 'QUALCOMM Incorporated', 'marketCap': 119317140000, 'sector': 'Technology', 'industry': 'Semiconductors', 'beta': 1.224, 'price': 106.915, 'lastAnnualDividend': 3.2, 'volume': 1818900, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}, {'symbol': 'AMAT', 'companyName': 'Applied Materials, Inc.', 'marketCap': 109615234787, 'sector': 'Technology', 'industry': 'Semiconductor Equipment & Materials', 'beta': 1.581, 'price': 131.035, 'lastAnnualDividend': 1.28, 'volume': 1107537, 'exchange': 'NASDAQ Global Select', 'exchangeShortName': 'NASDAQ', 'country': 'US', 'isEtf': False, 'isActivelyTrading': True}]

for item in screener:

companies.append(item['symbol'])

#print(companies)

value_ratios ={}

#get the financial ratios

count = 0

for company in companies:

try:

if count <30:

count = count + 1

fin_ratios = requests.get(f'https://financialmodelingprep.com/api/v3/ratios/{company}?apikey={demo}').json()

value_ratios[company] = {}

value_ratios[company]['ROE'] = fin_ratios[0]['returnOnEquity']

value_ratios[company]['ROA'] = fin_ratios[0]['returnOnAssets']

value_ratios[company]['Debt_Ratio'] = fin_ratios[0]['debtRatio']

value_ratios[company]['Interest_Coverage'] = fin_ratios[0]['interestCoverage']

value_ratios[company]['Payout_Ratio'] = fin_ratios[0]['payoutRatio']

value_ratios[company]['Dividend_Payout_Ratio'] = fin_ratios[0]['dividendPayoutRatio']

value_ratios[company]['PB'] = fin_ratios[0]['priceToBookRatio']

value_ratios[company]['PS'] = fin_ratios[0]['priceToSalesRatio']

value_ratios[company]['PE'] = fin_ratios[0]['priceEarningsRatio']

value_ratios[company]['Dividend_Yield'] = fin_ratios[0]['dividendYield']

value_ratios[company]['Gross_Profit_Margin'] = fin_ratios[0]['grossProfitMargin']

#more financials on growth:https://financialmodelingprep.com/api/v3/financial-growth/AAPL?apikey=demo

growth_ratios = requests.get(f'https://financialmodelingprep.com/api/v3/financial-growth/{company}?apikey={demo}').json()

value_ratios[company]['Revenue_Growth'] = growth_ratios[0]['revenueGrowth']

value_ratios[company]['NetIncome_Growth'] = growth_ratios[0]['netIncomeGrowth']

value_ratios[company]['EPS_Growth'] = growth_ratios[0]['epsgrowth']

value_ratios[company]['RD_Growth'] = growth_ratios[0]['rdexpenseGrowth']

except:

pass

print(value_ratios)

{'AAPL': {'ROE': 1.9695887275023682, 'ROA': 0.2829244092925685, 'Debt_Ratio': 0.3403750478377344, 'Interest_Coverage': 40.74957352439441, 'Payout_Ratio': 0.14870294480125848, 'Dividend_Payout_Ratio': 0.14870294480125848, 'PB': 48.14034011071204, 'PS': 6.186137718067193, 'PE': 24.441823533260525, 'Dividend_Yield': 0.006083954603424043, 'Gross_Profit_Margin': 0.43309630561360085, 'Revenue_Growth': 0.07793787604184606, 'NetIncome_Growth': 0.05410857625686523, 'EPS_Growth': 0.08465608465608473, 'RD_Growth': 0.19791001186456147}, 'NVDA': {'ROE': 0.19763811592235644, 'ROA': 0.10606575688407557, 'Debt_Ratio': 0.28786848623184885, 'Interest_Coverage': 16.12213740458015, 'Payout_Ratio': 0.09111721611721611, 'Dividend_Payout_Ratio': 0.09111721611721613, 'PB': 21.562777249898193, 'PS': 17.667344109142135, 'PE': 109.10232142857144, 'Dividend_Yield': 0.0008351537797192516, 'Gross_Profit_Margin': 0.5692889449099132, 'Revenue_Growth': 0.0022293230289068887, 'NetIncome_Growth': -0.5520918785890074, 'EPS_Growth': -0.5498721227621484, 'RD_Growth': 0.3931283219438117}, 'AVGO': {'ROE': 0.5061869743273592, 'ROA': 0.15693047004054664, 'Debt_Ratio': 0.5394612895739191, 'Interest_Coverage': 8.189407023603914, 'Payout_Ratio': 0.6117442366246194, 'Dividend_Payout_Ratio': 0.6117442366246194, 'PB': 8.488307648354397, 'PS': 5.805528969866579, 'PE': 16.769115127140495, 'Dividend_Yield': 0.0364804124717662, 'Gross_Profit_Margin': 0.6654519169954523, 'Revenue_Growth': 0.20958105646630237, 'NetIncome_Growth': 0.7065023752969121, 'EPS_Growth': 0.7477650063856961, 'RD_Growth': 0.013391017717346519}, 'ADBE': {'ROE': 0.3384812468863426, 'ROA': 0.17507822565801584, 'Debt_Ratio': 0.17055034051168783, 'Interest_Coverage': 54.44642857142857, 'Payout_Ratio': 0, 'Dividend_Payout_Ratio': 0, 'PB': 11.424033876592413, 'PS': 9.117295240259002, 'PE': 33.75086206896552, 'Dividend_Yield': 0, 'Gross_Profit_Margin': 0.8770305577643985, 'Revenue_Growth': 0.11536268609439342, 'NetIncome_Growth': -0.013687266694317711, 'EPS_Growth': 0.002970297029703083, 'RD_Growth': 0.17598425196850392}, 'ASML': {'ROE': 0.5667021088073719, 'ROA': 0.16472982022356153, 'Debt_Ratio': 0.10973059290166383, 'Interest_Coverage': 120.41118421052632, 'Payout_Ratio': 0.40023140185746897, 'Dividend_Payout_Ratio': 0.40023140185746897, 'PB': 18.033130071096934, 'PS': 9.612150433203926, 'PE': 31.821180459426497, 'Dividend_Yield': 0.012577515858275053, 'Gross_Profit_Margin': 0.49650504878762974, 'Revenue_Growth': 0.1376820160120359, 'NetIncome_Growth': 0.08712945335871634, 'EPS_Growth': -0.015320334261838361, 'RD_Growth': -0.10400471142520612}, 'AMD': {'ROE': 0.02410958904109589, 'ROA': 0.01953240603728914, 'Debt_Ratio': 0.04698135543060077, 'Interest_Coverage': 14.363636363636363, 'Payout_Ratio': 0, 'Dividend_Payout_Ratio': 0, 'PB': 1.8466843835616435, 'PS': 4.283969747044617, 'PE': 76.59543181818181, 'Dividend_Yield': 0, 'Gross_Profit_Margin': 0.4492606245498072, 'Revenue_Growth': 0.43610806863818913, 'NetIncome_Growth': -0.5825426944971537, 'EPS_Growth': -0.6743295019157087, 'RD_Growth': 0.7592267135325131}, 'INTU': {'ROE': 0.13805084255023453, 'ROA': 0.08581713462922966, 'Debt_Ratio': 0.2866450683945284, 'Interest_Coverage': 12.665322580645162, 'Payout_Ratio': 0.3729026845637584, 'Dividend_Payout_Ratio': 0.3729026845637584, 'PB': 8.326347790839076, 'PS': 10.007495824053452, 'PE': 60.313632550335576, 'Dividend_Yield': 0.006182726338901033, 'Gross_Profit_Margin': 0.78125, 'Revenue_Growth': 0.12902718843312902, 'NetIncome_Growth': 0.15392061955469508, 'EPS_Growth': 0.1490514905149052, 'RD_Growth': 0.0818065615679591}, 'TXN': {'ROE': 0.6001920834190848, 'ROA': 0.321571654353659, 'Debt_Ratio': 0.3210570808982982, 'Interest_Coverage': 47.38317757009346, 'Payout_Ratio': 0.4911418447822608, 'Dividend_Payout_Ratio': 0.49114184478226086, 'PB': 10.461553131645744, 'PS': 7.614243059716397, 'PE': 17.43034175334324, 'Dividend_Yield': 0.02817740763390695, 'Gross_Profit_Margin': 0.6875873776712602, 'Revenue_Growth': 0.09180113388573921, 'NetIncome_Growth': 0.12614236066417814, 'EPS_Growth': 0.1258907363420428, 'RD_Growth': 0.07464607464607464}, 'QCOM': {'ROE': 0.718148004219175, 'ROA': 0.2639245929734362, 'Debt_Ratio': 0.31586893540621047, 'Interest_Coverage': 32.36734693877551, 'Payout_Ratio': 0.24829931972789115, 'Dividend_Payout_Ratio': 0.24829931972789115, 'PB': 7.46505412757453, 'PS': 3.042262895927602, 'PE': 10.394868583797154, 'Dividend_Yield': 0.02388672042616527, 'Gross_Profit_Margin': 0.5783936651583711, 'Revenue_Growth': 0.31680867544539115, 'NetIncome_Growth': 0.43049872829813113, 'EPS_Growth': 0.4418022528160199, 'RD_Growth': 0.14186176142697882}, 'AMAT': {'ROE': 0.5350992291290799, 'ROA': 0.24414427897927113, 'Debt_Ratio': 0.20736361595450123, 'Interest_Coverage': 34.1578947368421, 'Payout_Ratio': 0.13379310344827586, 'Dividend_Payout_Ratio': 0.13379310344827586, 'PB': 6.3064285714285715, 'PS': 2.9823769633507853, 'PE': 11.78553103448276, 'Dividend_Yield': 0.011352318623303149, 'Gross_Profit_Margin': 0.465115377157262, 'Revenue_Growth': 0.11802454147335559, 'NetIncome_Growth': 0.10818614130434782, 'EPS_Growth': 0.15765069551777441, 'RD_Growth': 0.11509054325955734}}

- Let’s look at top 4 stocks in the aforementioned list

DF = pd.DataFrame.from_dict(value_ratios,orient='index')

print(DF.head(4))

ROE ROA Debt_Ratio Interest_Coverage Payout_Ratio \

AAPL 1.97 0.28 0.34 40.75 0.15

NVDA 0.20 0.11 0.29 16.12 0.09

AVGO 0.51 0.16 0.54 8.19 0.61

ADBE 0.34 0.18 0.17 54.45 0.00

Dividend_Payout_Ratio PB PS PE Dividend_Yield \

AAPL 0.15 48.14 6.19 24.44 0.01

NVDA 0.09 21.56 17.67 109.10 0.00

AVGO 0.61 8.49 5.81 16.77 0.04

ADBE 0.00 11.42 9.12 33.75 0.00

Gross_Profit_Margin Revenue_Growth NetIncome_Growth EPS_Growth \

AAPL 0.43 0.08 0.05 0.08

NVDA 0.57 0.00 -0.55 -0.55

AVGO 0.67 0.21 0.71 0.75

ADBE 0.88 0.12 -0.01 0.00

RD_Growth

AAPL 0.20

NVDA 0.39

AVGO 0.01

ADBE 0.18

#criteria ranking

ROE = 1.2

ROA = 1.1

Debt_Ratio = -1.1

Interest_Coverage = 1.05

Dividend_Payout_Ratio = 1.01

PB = -1.10

PS = -1.05

Revenue_Growth = 1.25

Net_Income_Growth = 1.10

#mean to enable comparison across ratios

ratios_mean = []

for item in DF.columns:

ratios_mean.append(DF[item].mean())

#divide each value in dataframe by mean to normalize values

DF = DF / ratios_mean

DF['ranking'] = DF['NetIncome_Growth']*Net_Income_Growth + DF['Revenue_Growth']*Revenue_Growth + DF['ROE']*ROE + DF['ROA']*ROA + DF['Debt_Ratio'] * Debt_Ratio + DF['Interest_Coverage'] * Interest_Coverage + DF['Dividend_Payout_Ratio'] * Dividend_Payout_Ratio + DF['PB']*PB + DF['PS']*PS

print(DF.sort_values(by=['ranking'],ascending=False))

ROE ROA Debt_Ratio Interest_Coverage Payout_Ratio \

AVGO 0.90 0.86 2.05 0.22 2.45

QCOM 1.28 1.45 1.20 0.85 0.99

ASML 1.01 0.90 0.42 3.16 1.60

TXN 1.07 1.77 1.22 1.24 1.97

AMAT 0.96 1.34 0.79 0.90 0.54

INTU 0.25 0.47 1.09 0.33 1.49

AAPL 3.52 1.55 1.30 1.07 0.60

ADBE 0.61 0.96 0.65 1.43 0.00

AMD 0.04 0.11 0.18 0.38 0.00

NVDA 0.35 0.58 1.10 0.42 0.36

Dividend_Payout_Ratio PB PS PE Dividend_Yield \

AVGO 2.45 0.60 0.76 0.43 2.91

QCOM 0.99 0.53 0.40 0.26 1.90

ASML 1.60 1.27 1.26 0.81 1.00

TXN 1.97 0.74 1.00 0.44 2.24

AMAT 0.54 0.44 0.39 0.30 0.90

INTU 1.49 0.59 1.31 1.54 0.49

AAPL 0.60 3.39 0.81 0.62 0.48

ADBE 0.00 0.80 1.19 0.86 0.00

AMD 0.00 0.13 0.56 1.95 0.00

NVDA 0.36 1.52 2.31 2.78 0.07

Gross_Profit_Margin Revenue_Growth NetIncome_Growth EPS_Growth \

AVGO 1.11 1.28 13.63 15.90

QCOM 0.96 1.94 8.31 9.39

ASML 0.83 0.84 1.68 -0.33

TXN 1.15 0.56 2.43 2.68

AMAT 0.77 0.72 2.09 3.35

INTU 1.30 0.79 2.97 3.17

AAPL 0.72 0.48 1.04 1.80

ADBE 1.46 0.71 -0.26 0.06

AMD 0.75 2.67 -11.24 -14.34

NVDA 0.95 0.01 -10.65 -11.69

RD_Growth ranking

AVGO 0.07 17.62

QCOM 0.77 14.27

ASML -0.56 6.87

TXN 0.40 6.70

AMAT 0.62 5.54

INTU 0.44 3.70

AAPL 1.07 3.40

ADBE 0.95 1.02

AMD 4.11 -9.40

NVDA 2.13 -15.13

- NVDA bar chart visuals of the Excel spreadsheet fundamentalsnvda.xlsx

Rows:

Mkt Cap

Debt to Equity

Debt to Assets

Revenue per Share

NI per Share

Revenue

Gross Profit

R&D Expenses

Op Expenses

Op Income

Net Income

Cash

Inventory

Cur Assets

LT Assets

Int Assets

Total Assets

Cur Liab

LT Debt

LT Liab

Total Liab

SH Equity

CF Operations

CF Investing

CF Financing

CAPEX

FCF

Dividends Paid

Gross Profit Margin

Op Margin

Int Coverage

Net Profit Margin

Dividend Yield

Current Ratio

Operating Cycle

Days of AP Outstanding

Cash Conversion Cycle

ROA

ROE

ROCE

PE

PS

PB

Price To FCF

PEG

EPS

Columns:

2023 2022 2021 2020 2019 CAGR 2023 growth 2022 growth 2021 growth

- Overall NVDA gets a fundamental rating of 7 out of 10.

- The Altman-Z score of NVDA (29.91) is better than 95.24% of its industry peers.

- NVDA has a better Debt to FCF ratio (0.94) than 77.14% of its industry peers.

- NVDA‘s Current ratio of 2.79 is in line compared to the rest of the industry. NVDA outperforms 41.90% of its industry peers.

- In the last year, the EPS has been growing by 20.41%, which is quite impressive.

- The EPS will grow by 54.68% on average per year.

- NVDA is valuated quite expensively with a Price/Earnings ratio of 77.68.

- The average S&P500 Price/Earnings ratio is at 22.86. NVDA is valued rather expensively when compared to this.

- 68.57% of the companies in the same industry are cheaper than NVDA, based on the Enterprise Value to EBITDA ratio.

- The excellent profitability rating of NVDA may justify a higher PE ratio.

- NVDA has a yearly dividend return of 0.04%, which is pretty low.

- The dividend of NVDA has a limited annual growth rate of 2.26%.

Indian Dividend Stock Portfolio 3

- In this section, we will use the CAPM model to examine the risk/return ratio of Indian dividend stocks listed in NIFTY 50 (a benchmark Indian stock market index).

- Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH')

os. getcwd()

- Importing the key libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from nsepy import get_history as gh

from datetime import date

- Defining the time interval and tickers (initial configuration)

start_date = date(2018,2,2)

end_date = date(2023,2,2)

tickers = ['TATAMOTORS','DABUR', 'ICICIBANK','WIPRO','INFY']

- Loading the stock data, creating portfolio 3 and calculating the daily returns

def load_stock_data(start_date, end_date, ticker):

df = pd.DataFrame()

for i in range(len(ticker)):

data = gh(symbol=ticker[i],start= start_date, end=end_date)[['Symbol','Close']]

data.rename(columns={'Close':data['Symbol'][0]},inplace=True)

data.drop(['Symbol'], axis=1,inplace=True)

if i == 0:

df = data

if i != 0:

df = df.join(data)

return df

# Loading the stock data in the tickers from NSEPY data for specified period

df_stock = load_stock_data(start_date, end_date, tickers)

# Loading the NIFTY data for specified period

df_nifty = gh(symbol = 'NIFTY',start = date(2018,2,2), end = date(2023,2,2), index= True)[['Close']]

df_nifty.rename(columns = {'Close':'NIFTY'}, inplace = True)

df_port = pd.concat([df_stock, df_nifty], axis = 1)

# Calculating daily returns

df_returns = df_port.pct_change().dropna().reset_index()

df_port 5 selected rows:

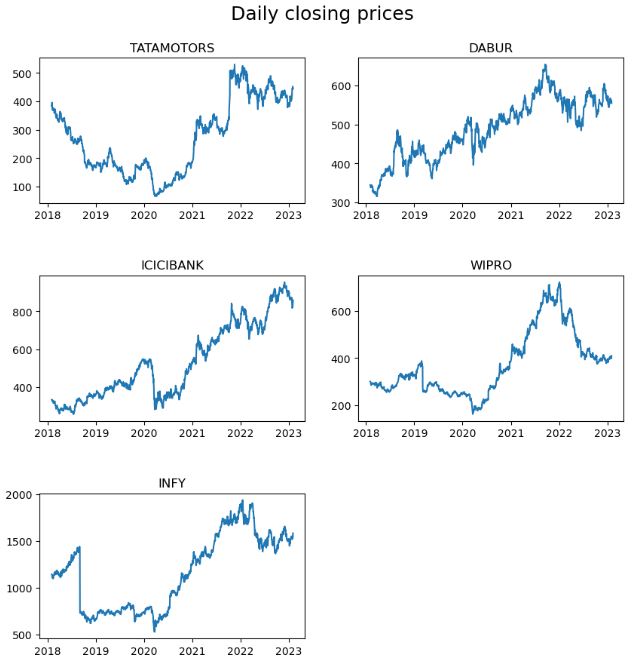

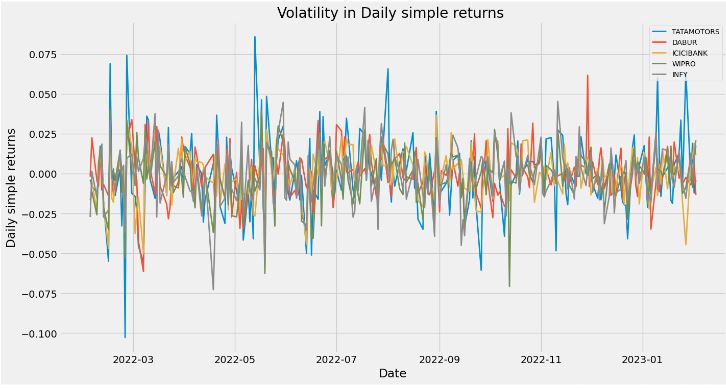

- Plotting the stock daily closing prices

plt.figure(figsize=(10, 10))

plt.subplots_adjust(hspace=0.5)

plt.suptitle("Daily closing prices", fontsize=18, y=0.95)

for n, ticker in enumerate(tickers):

ax = plt.subplot(3, 2, n + 1)

df_stock[ticker].plot(ax= ax)

ax.set_title(ticker.upper())

ax.set_xlabel("")

plt.savefig('capmprice.png', transparent=True)

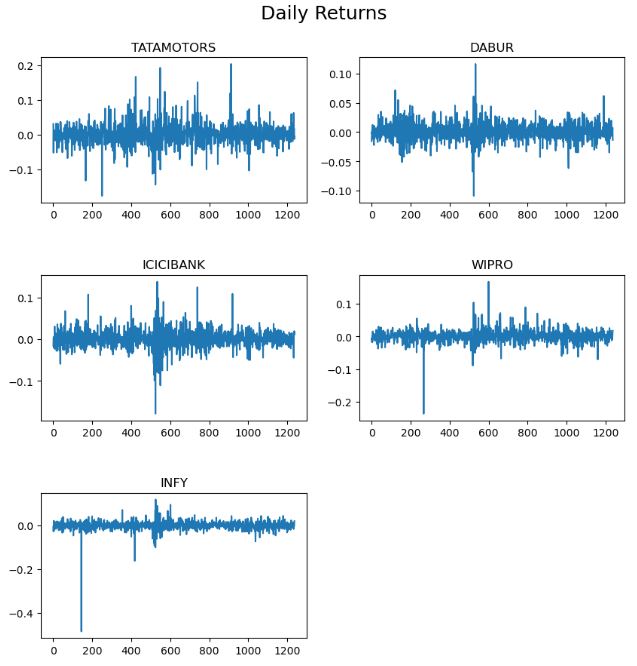

- Plotting daily returns

plt.figure(figsize=(10, 10))

plt.subplots_adjust(hspace=0.5)

plt.suptitle("Daily Returns", fontsize=18, y=0.95)

for n, ticker in enumerate(tickers):

ax = plt.subplot(3, 2, n + 1)

df_returns[ticker].plot(ax= ax)

ax.set_title(ticker.upper())

ax.set_xlabel("")

plt.savefig('capmreturns.png', transparent=True)

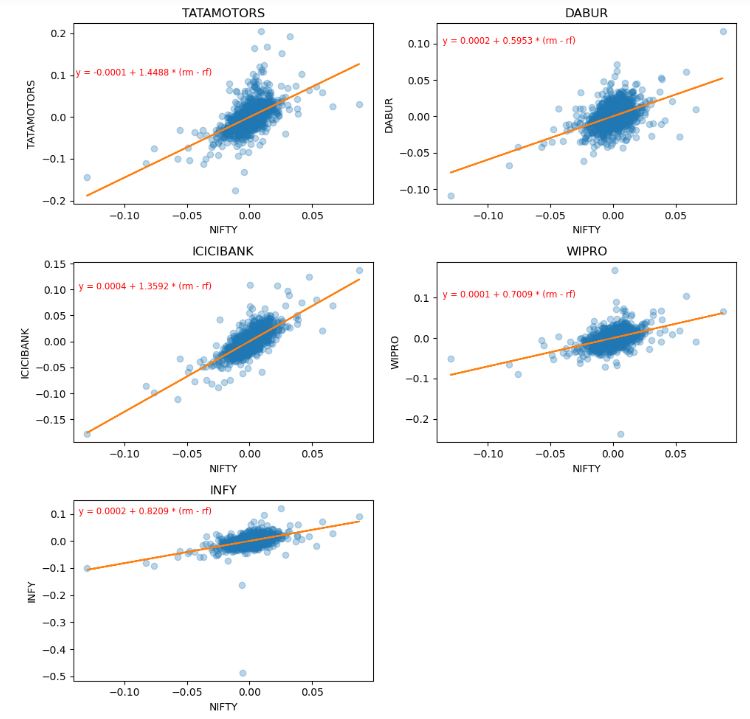

- Fitting a regression line stock vs NIFTY to estimate beta and alpha

beta = []

alpha = []

for i in df_returns.columns:

if i != 'Date' and i != 'NIFTY':

df_returns.plot(kind = 'scatter', x = 'NIFTY', y = i)

b, a = np.polyfit(df_returns['NIFTY'], df_returns[i], 1)

plt.plot(df_returns['NIFTY'], b * df_returns['NIFTY'] + a, '-', color = 'r')

beta.append(b)

alpha.append(a)

- Plotting the linear regression lines

plt.figure(figsize=(10, 10))

plt.subplots_adjust(hspace=0.5)

plt.suptitle("", fontsize=18, y=0.95)

for n, ticker in enumerate(tickers):

ax = plt.subplot(3, 2, n + 1)

plt.plot(df_returns['NIFTY'], df_returns[ticker], 'o', alpha = 0.3)

b, a = np.polyfit(df_returns['NIFTY'], df_returns[ticker], 1)

plt.plot(df_returns['NIFTY'], b * df_returns['NIFTY'] + a, '-')

ax.set_title(ticker.upper())

ax.set_xlabel('NIFTY')

ax.set_ylabel(ticker)

plt.tight_layout()

plt.text(-0.03, 0.1, f'y = {round(a, 4)} + {round(b, 4)} * (rm - rf)',

horizontalalignment='right',

size='small', color='red')

plt.savefig('capmreg.png', transparent=True)

- Calculating CAPM-based expected returns

ER = []

rf = 0

rm = df_returns['NIFTY'].mean() * 252

print(f'Market return is {rm}%')

for i, b in enumerate(beta):

ER_tmp = rf + (b * (rf - rm)) * 100

ER.append(ER_tmp)

print(f'Expected return based on CAPM for {tickers[i]} is {round(ER_tmp,2)} %')

Market return is 0.11933857013790888%

Expected return based on CAPM for TATAMOTORS is -17.29 %

Expected return based on CAPM for DABUR is -7.1 %

Expected return based on CAPM for ICICIBANK is -16.22 %

Expected return based on CAPM for WIPRO is -8.36 %

Expected return based on CAPM for INFY is -9.8 %

- Assigning portfolio weights and calculating the expected portfolio return

portfolio_weights = 1/len(tickers) * np.ones(len(tickers))

ER_portfolio = sum(ER * portfolio_weights)

print(f'Portfolio expected return is {round(ER_portfolio,2)} %')

Portfolio expected return is -11.76 %

print(portfolio_weights)

[0.2 0.2 0.2 0.2 0.2]

print(alpha)

[-8.918248566266388e-05, 0.00022239414251699533, 0.00035961301093695073, 0.0001049024358274514, 0.0001856998089880721]

print(beta)

[1.4488042079008974, 0.5953470049512081, 1.3592314779510428, 0.7008874168511913, 0.8208594560575715]

- Computing the Security market Line (SML)

sml_beta = pd.DataFrame(beta,columns =['beta'])

sml_returns = pd.DataFrame(ER,columns =['ER'])

sml = pd.concat([sml_beta, sml_returns], axis = 1)

fig, ax = plt.subplots(figsize=(8, 5))

plt.plot(sml['beta'], sml['ER'])

ax.set_title('Security Market Line')

ax.set_xlabel('Beta')

ax.set_ylabel('Expected Returns')

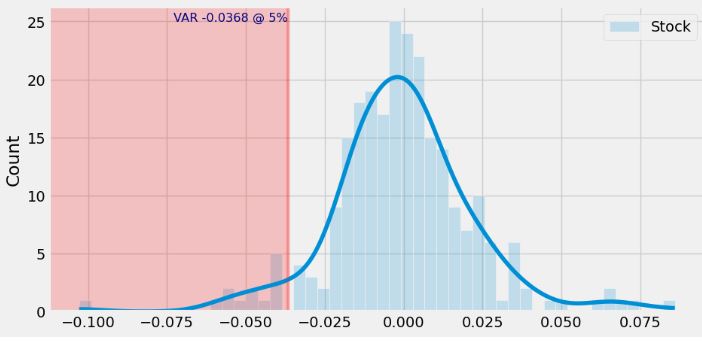

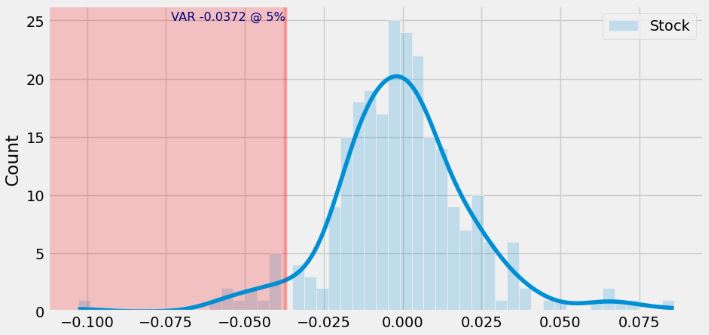

- Let’s optimize portfolio 3 in terms of stock VAR

# Import libraries

import numpy as np

import pandas as pd

import warnings

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

from statistics import NormalDist

import statistics

import seaborn as sns

from datetime import date

from tabulate import tabulate

from nsepy import get_history as gh

from mplcursors import cursor

plt.style.use('fivethirtyeight')

warnings.filterwarnings('ignore')

pd.set_option('display.max_rows', None)

# Define configurations

initial_investment: int = 100000

start_date = date(2022,2,2)

# end_date = date.today()

end_date = date(2023,2,2)

stocksymbols = ['TATAMOTORS','DABUR', 'ICICIBANK','WIPRO','INFY']

weights = np.array([0.4, 0.2, 0.1, 0.1, 0.2])

# Data loading and computing Return-VAR

def load_stock_data(start_date, end_date, investment: int, ticker: str):

df = pd.DataFrame()

for i in range(len(ticker)):

data = gh(symbol=ticker[i],start= start_date, end=end_date)[['Symbol','Close']]

data.rename(columns={'Close':data['Symbol'][0]},inplace=True)

data.drop(['Symbol'], axis=1,inplace=True)

if i == 0:

df = data

if i != 0:

df = df.join(data)

return df

df_stockPrice = load_stock_data(start_date, end_date, initial_investment, stocksymbols)

df_returns = df_stockPrice.pct_change().dropna()

portfolio = (weights * df_returns.values).sum(axis=1)

port_var = np.percentile(portfolio, 5, interpolation = 'lower')

port_var

-0.022599923823150847

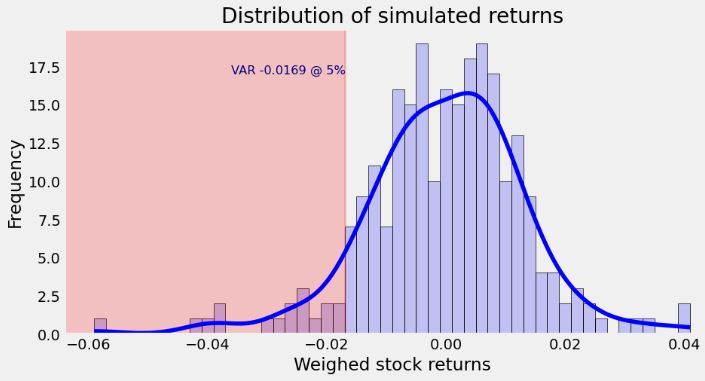

- Bootstrap (basic) simulation

def sim_portfolio(weights):

# port_stdev = np.sqrt(weights.T.dot(cov_matrix).dot(weights))

# return port_stdev

tmp_pp = (weights * df_returns.values).sum(axis=1)

var_sim_port = np.percentile(tmp_pp, 5, interpolation = 'lower')

return var_sim_port

port_returns = []

port_volatility = []

port_weights = []

num_assets = len(stocksymbols)

num_portfolios = 10000

np.random.seed(1357)

for port in range(num_portfolios):

weights = np.random.random(num_assets)

weights = weights/sum(weights)

port_weights.append(weights)

df_wts_returns = df_returns.mean().dot(weights)

port_returns.append(df_wts_returns*100)

var_port_95 = sim_portfolio(weights)

port_volatility.append(var_port_95)

port_weights = [[round(wt[0],5), round(wt[1],5), round(wt[2],5),round(wt[3],5),round(wt[4],5)] for wt in port_weights]

dff = {'Returns': port_returns, 'Risk': port_volatility, 'Weights': port_weights}

df_risk = pd.DataFrame(dff)

df_risk.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 10000 entries, 0 to 9999

Data columns (total 3 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Returns 10000 non-null float64

1 Risk 10000 non-null float64

2 Weights 10000 non-null object

dtypes: float64(2), object(1)

memory usage: 234.5+ KB

df_risk[(df_risk['Risk'] > -0.02) & (df_risk['Returns'] > 0.01)]

Returns Risk Weights

997 0.010809 -0.019637 [0.15549, 0.30334, 0.48221, 0.01111, 0.04785]

1095 0.011785 -0.018679 [0.02925, 0.11915, 0.65296, 0.02588, 0.17276]

4526 0.010994 -0.019101 [0.08346, 0.13514, 0.6049, 0.01273, 0.16377]

5457 0.011373 -0.019397 [0.12779, 0.31885, 0.47465, 0.00504, 0.07367]

6658 0.010704 -0.019479 [0.12018, 0.32579, 0.50025, 0.0314, 0.02238]

8159 0.012759 -0.019898 [0.08113, 0.2709, 0.54323, 0.01251, 0.09222]

9963 0.010442 -0.019877 [0.0012, 0.42383, 0.44869, 0.03354, 0.09274]

df_risk['Risk'].max()

-0.016895038141191226

df_risk['Risk'].min()

-0.03263339159510597

df_risk['Returns'].max()

0.017049520522481834

df_risk['Returns'].min()

-0.09880198482191363

- Selecting new weights for min/max returns and risk

max_risk = df_risk.iloc[df_risk['Risk'].idxmin()]

max_risk[0]

max_risk[1]

max_risk[2]

[0.82771, 0.00729, 0.14223, 0.0197, 0.00307]

min_risk = df_risk.iloc[df_risk['Risk'].idxmax()]

min_risk[0]

min_risk[1]

min_risk[2]

[0.05294, 0.34003, 0.30989, 0.18632, 0.11082]

max_returns = df_risk.iloc[df_risk['Returns'].idxmax()]

max_returns[0]

max_returns[1]

max_returns[2]

[0.03087, 0.3918, 0.52679, 0.00689, 0.04365]

min_returns = df_risk.iloc[df_risk['Returns'].idxmin()]

min_returns[0]

min_returns[1]

min_returns[2]

[0.00399, 0.04691, 0.09405, 0.74185, 0.1132]

# Portfolio VAR for the basic simulation

port_var_basic_sim = sim_portfolio(min_risk[2])

port_var_basic_sim

-0.01689496173724531

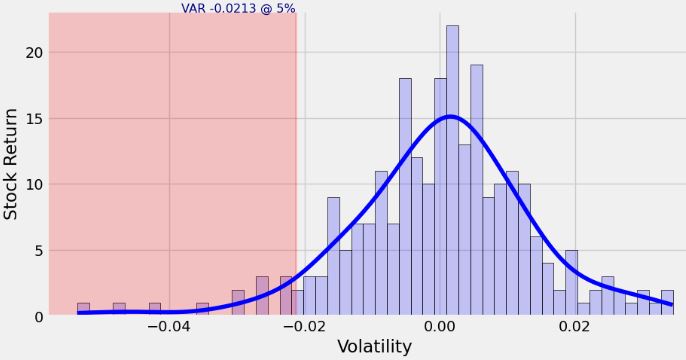

- Selecting new weights using the decay factor

def var_weighted_decay_factor(weights):

returns = df_returns.copy()

returns['Stock'] = (weights * returns.values).sum(axis=1)

# returns = returns['Stock']

decay_factor = 0.5 #we’re picking this arbitrarily

n = len(returns)

wts = [(decay_factor**(i-1) * (1-decay_factor))/(1-decay_factor**n) for i in range(1, n+1)]

#Need to reverse the PnL to put recent returns on top

returns_recent_first = returns[::-1]

weights_dict = {'Returns':returns_recent_first, 'Weights':wts}

wts_returns = pd.DataFrame(returns_recent_first['Stock'])

wts_returns['wts'] = wts