- The objective of this study is to apply the Deep Reinforcement (DRL) algorithm to USA stocks yielding +4% DIV in 2022-23 (according to @buyingincome):

- Today we focus on Altria Group, Inc. (NYSE: MO) – a Dividend King moving beyond smoking. This post is a continuation of our previous case study dedicated to the candlestick-based Donchian channel trading indicator to identify potential breakouts and retracements of the $MO stock. Recall that our results appeared to be consistent with the TradingView and @simply_robo technical analysis summary and recommendations.

- Problem: Accurate predictions of stock prices is the common concerns of stock traders. This is because the majority of stock prices are highly volatile. The correlation between various factors is frequently so obscure that it is rather difficult to isolate the factors affecting rapid fluctuations of stock prices.

- Solution: Recent advances in DRL have enabled more accurate stock forecasting, and the majority of papers have demonstrated that their models can outperform the market average returns.

- Testimonies:

MLQ.ai: In fact, many AI experts agree that DRL is likely to be the best path towards AGI, or artificial general intelligence.

Spinning Up in DRL at OpenAI: “We believe that deep learning generally—and DRL specifically—will play central roles in the development of powerful AI technology.”

- This project intends to leverage DRL in stock portfolio management.

Key assumptions and limitations of the DRL framework:

- trading has no impact on the market

- only single stock type is supported

- only 3 basic actions: buy, hold, sell (no short selling or other complex actions)

- the agent performs only 1 action for portfolio reallocation at the end of each trade day

- all reallocations can be finished at the closing prices

- no missing data in price history

- no transaction cost.

Key challenges of the DRL framework:

- implementing algorithms from scratch with a thorough understanding of their pros and cons

- building a reliable reward mechanism (learning tends to be stationary/stuck in local optima quite often)

- ensuring the framework is scalable and extensible.

Flow Chart

The flowchart below illustrates the DRL procedure for agent-environment interaction at a high level. The goal is to maximize the agent’s reward in a limited number of actions by mapping environmental states to actions. The reward function serves as the overarching goal of training and serves as the standard against which all other factors are measured.

Key Steps

The key steps for designing a DRL model are as follows:

- Importing Libraries

- Create the agent who will make all decisions

- Define basic functions for formatting the values, sigmoid function, reading the data file, etc

- Training the agent

- Evaluating the agent performance.

Algorithm

let’s set the working directory

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and download the stock data

import yfinance as yf

data = yf.download(“MO”, start=”2022-01-03″, end=”2023-03-22″)

[*********************100%***********************] 1 of 1 completed

We need to install the extra library

!pip install chainer

and import other libraries

import time

import copy

import numpy as np

import pandas as pd

import chainer

import chainer.functions as F

import chainer.links as L

from plotly import tools

from plotly.graph_objs import *

from plotly.offline import init_notebook_mode, iplot, iplot_mpl

init_notebook_mode()

Let’s check the data structure

data.tail()

data.shape

(305, 6)

data.info()

<class 'pandas.core.frame.DataFrame'> DatetimeIndex: 305 entries, 2022-01-03 to 2023-03-21 Data columns (total 6 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Open 305 non-null float64 1 High 305 non-null float64 2 Low 305 non-null float64 3 Close 305 non-null float64 4 Adj Close 305 non-null float64 5 Volume 305 non-null int64 dtypes: float64(5), int64(1) memory usage: 24.8 KB

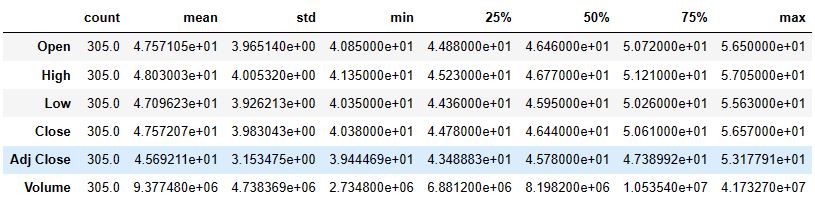

data.describe().T

Train/test data split:

date_split = ‘2022-10-01’

train = data[:date_split]

test = data[date_split:]

len(train), len(test)

(188, 117)

let’s plot these two datasets using plotly

def plot_train_test(train, test, date_split):

data = [

Candlestick(x=train.index, open=train['Open'], high=train['High'], low=train['Low'], close=train['Close'], name='train'),

Candlestick(x=test.index, open=test['Open'], high=test['High'], low=test['Low'], close=test['Close'], name='test')

]

layout = {

'shapes': [

{'x0': date_split, 'x1': date_split, 'y0': 0, 'y1': 1, 'xref': 'x', 'yref': 'paper', 'line': {'color': 'rgb(0,0,0)', 'width': 1}}

],

'annotations': [

{'x': date_split, 'y': 1.0, 'xref': 'x', 'yref': 'paper', 'showarrow': False, 'xanchor': 'left', 'text': ' test data'},

{'x': date_split, 'y': 1.0, 'xref': 'x', 'yref': 'paper', 'showarrow': False, 'xanchor': 'right', 'text': 'train data '}

]

}

figure = Figure(data=data, layout=layout)

iplot(figure)

plot_train_test(train, test, date_split)

Let’s define the class Environment1

class Environment1:

def __init__(self, data, history_t=90):

self.data = data

self.history_t = history_t

self.reset()

def reset(self):

self.t = 0

self.done = False

self.profits = 0

self.positions = []

self.position_value = 0

self.history = [0 for _ in range(self.history_t)]

return [self.position_value] + self.history # obs

def step(self, act):

reward = 0

# act = 0: stay, 1: buy, 2: sell

if act == 1:

self.positions.append(self.data.iloc[self.t, :]['Close'])

elif act == 2: # sell

if len(self.positions) == 0:

reward = -1

else:

profits = 0

for p in self.positions:

profits += (self.data.iloc[self.t, :]['Close'] - p)

reward += profits

self.profits += profits

self.positions = []

# set next time

self.t += 1

self.position_value = 0

for p in self.positions:

self.position_value += (self.data.iloc[self.t, :]['Close'] - p)

self.history.pop(0)

self.history.append(self.data.iloc[self.t, :]['Close'] - self.data.iloc[(self.t-1), :]['Close'])

# clipping reward

if reward > 0:

reward = 1

elif reward < 0:

reward = -1

return [self.position_value] + self.history, reward, self.done # obs, reward, done

Let’s invoke this class as follows:

env = Environment1(train)

print(env.reset())

for _ in range(3):

pact = np.random.randint(3)

print(env.step(pact))

[0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0] ([0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 1.05999755859375], 0, False) ([-0.3899993896484375, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 1.05999755859375, -0.3899993896484375], 0, False) ([0.18000030517578125, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 1.05999755859375, -0.3899993896484375, 0.5699996948242188], 0, False)

Let’s define DQN

def train_dqn(env):

class Q_Network(chainer.Chain):

def __init__(self, input_size, hidden_size, output_size):

super(Q_Network, self).__init__(

fc1 = L.Linear(input_size, hidden_size),

fc2 = L.Linear(hidden_size, hidden_size),

fc3 = L.Linear(hidden_size, output_size)

)

def __call__(self, x):

h = F.relu(self.fc1(x))

h = F.relu(self.fc2(h))

y = self.fc3(h)

return y

def reset(self):

self.zerograds()

Q = Q_Network(input_size=env.history_t+1, hidden_size=100, output_size=3)

Q_ast = copy.deepcopy(Q)

optimizer = chainer.optimizers.Adam()

optimizer.setup(Q)

epoch_num = 50

step_max = len(env.data)-1

memory_size = 200

batch_size = 20

epsilon = 1.0

epsilon_decrease = 1e-3

epsilon_min = 0.1

start_reduce_epsilon = 200

train_freq = 10

update_q_freq = 20

gamma = 0.97

show_log_freq = 5

memory = []

total_step = 0

total_rewards = []

total_losses = []

start = time.time()

for epoch in range(epoch_num):

pobs = env.reset()

step = 0

done = False

total_reward = 0

total_loss = 0

while not done and step < step_max:

# select act

pact = np.random.randint(3)

if np.random.rand() > epsilon:

pact = Q(np.array(pobs, dtype=np.float32).reshape(1, -1))

pact = np.argmax(pact.data)

# act

obs, reward, done = env.step(pact)

# add memory

memory.append((pobs, pact, reward, obs, done))

if len(memory) > memory_size:

memory.pop(0)

# train or update q

if len(memory) == memory_size:

if total_step % train_freq == 0:

shuffled_memory = np.random.permutation(memory)

memory_idx = range(len(shuffled_memory))

for i in memory_idx[::batch_size]:

batch = np.array(shuffled_memory[i:i+batch_size])

b_pobs = np.array(batch[:, 0].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_pact = np.array(batch[:, 1].tolist(), dtype=np.int32)

b_reward = np.array(batch[:, 2].tolist(), dtype=np.int32)

b_obs = np.array(batch[:, 3].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_done = np.array(batch[:, 4].tolist(), dtype=bool)

q = Q(b_pobs)

maxq = np.max(Q_ast(b_obs).data, axis=1)

target = copy.deepcopy(q.data)

for j in range(batch_size):

target[j, b_pact[j]] = b_reward[j]+gamma*maxq[j]*(not b_done[j])

Q.reset()

loss = F.mean_squared_error(q, target)

total_loss += loss.data

loss.backward()

optimizer.update()

if total_step % update_q_freq == 0:

Q_ast = copy.deepcopy(Q)

# epsilon

if epsilon > epsilon_min and total_step > start_reduce_epsilon:

epsilon -= epsilon_decrease

# next step

total_reward += reward

pobs = obs

step += 1

total_step += 1

total_rewards.append(total_reward)

total_losses.append(total_loss)

if (epoch+1) % show_log_freq == 0:

log_reward = sum(total_rewards[((epoch+1)-show_log_freq):])/show_log_freq

log_loss = sum(total_losses[((epoch+1)-show_log_freq):])/show_log_freq

elapsed_time = time.time()-start

print('\t'.join(map(str, [epoch+1, epsilon, total_step, log_reward, log_loss, elapsed_time])))

start = time.time()

return Q, total_losses, total_rewards

Let’s invoke this class

Q, total_losses, total_rewards = train_dqn(Environment1(train))

5 0.26599999999999935 935 -15.6 8.378280513733625 1.882044792175293 10 0.0999999999999992 1870 1.6 212.92116943709553 2.9393341541290283 15 0.0999999999999992 2805 0.0 197.6353921659291 3.1940603256225586 20 0.0999999999999992 3740 -0.2 76.21642142683268 2.6600332260131836 25 0.0999999999999992 4675 8.4 16.361252902820706 2.7394282817840576 30 0.0999999999999992 5610 10.6 11.873821935988962 2.6485908031463623 35 0.0999999999999992 6545 10.2 18.863544968515633 2.7909960746765137 40 0.0999999999999992 7480 10.8 11.163612035475671 2.586214065551758 45 0.0999999999999992 8415 9.0 5.021430662972852 2.617769956588745 50 0.0999999999999992 9350 13.6 6.592287559248507 2.6137917041778564

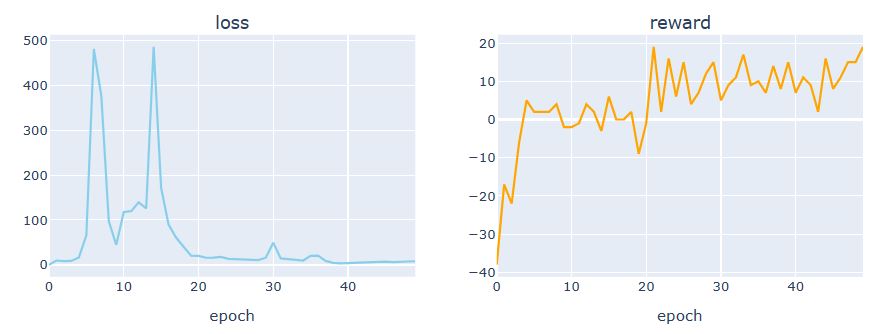

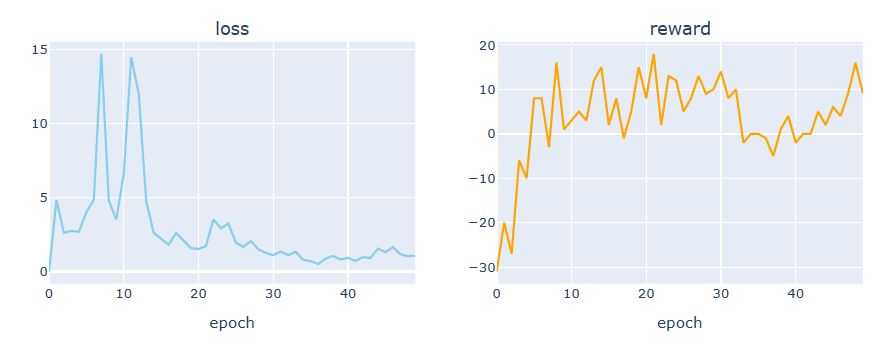

Let’s plot the loss vs reward using plotly

def plot_loss_reward(total_losses, total_rewards):

figure = tools.make_subplots(rows=1, cols=2, subplot_titles=('loss', 'reward'), print_grid=False)

figure.append_trace(Scatter(y=total_losses, mode='lines', line=dict(color='skyblue')), 1, 1)

figure.append_trace(Scatter(y=total_rewards, mode='lines', line=dict(color='orange')), 1, 2)

figure['layout']['xaxis1'].update(title='epoch')

figure['layout']['xaxis2'].update(title='epoch')

figure['layout'].update(height=400, width=900, showlegend=False)

iplot(figure)

plot_loss_reward(total_losses, total_rewards)

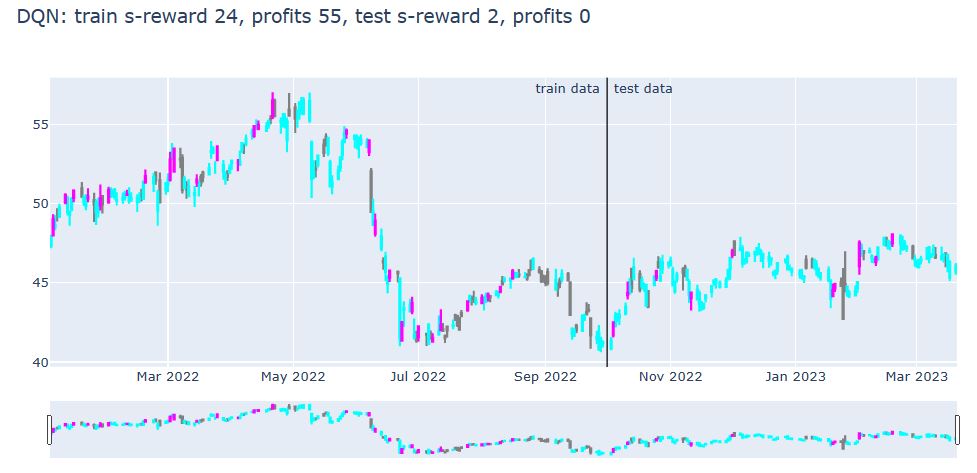

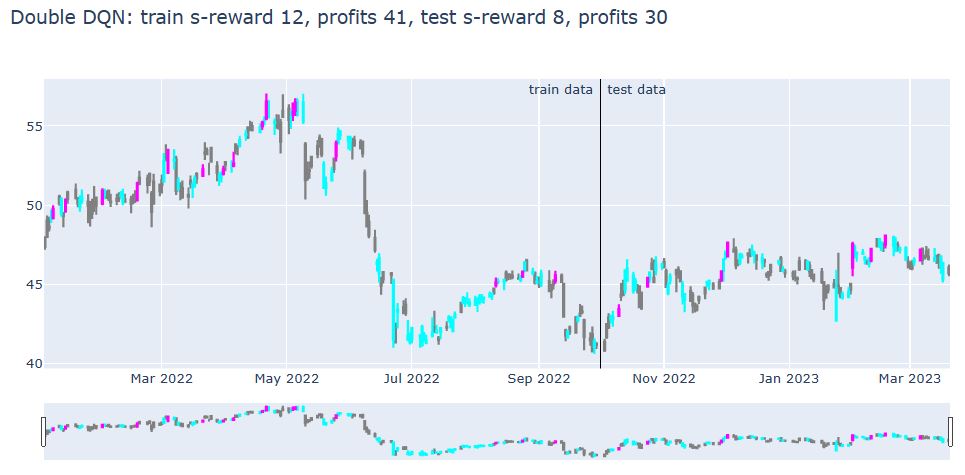

Let’s compare the DQN train/test s-reward vs profits

def plot_train_test_by_q(train_env, test_env, Q, algorithm_name):

# train

pobs = train_env.reset()

train_acts = []

train_rewards = []

for _ in range(len(train_env.data)-1):

pact = Q(np.array(pobs, dtype=np.float32).reshape(1, -1))

pact = np.argmax(pact.data)

train_acts.append(pact)

obs, reward, done = train_env.step(pact)

train_rewards.append(reward)

pobs = obs

train_profits = train_env.profits

# test

pobs = test_env.reset()

test_acts = []

test_rewards = []

for _ in range(len(test_env.data)-1):

pact = Q(np.array(pobs, dtype=np.float32).reshape(1, -1))

pact = np.argmax(pact.data)

test_acts.append(pact)

obs, reward, done = test_env.step(pact)

test_rewards.append(reward)

pobs = obs

test_profits = test_env.profits

# plot

train_copy = train_env.data.copy()

test_copy = test_env.data.copy()

train_copy['act'] = train_acts + [np.nan]

train_copy['reward'] = train_rewards + [np.nan]

test_copy['act'] = test_acts + [np.nan]

test_copy['reward'] = test_rewards + [np.nan]

train0 = train_copy[train_copy['act'] == 0]

train1 = train_copy[train_copy['act'] == 1]

train2 = train_copy[train_copy['act'] == 2]

test0 = test_copy[test_copy['act'] == 0]

test1 = test_copy[test_copy['act'] == 1]

test2 = test_copy[test_copy['act'] == 2]

act_color0, act_color1, act_color2 = 'gray', 'cyan', 'magenta'

data = [

Candlestick(x=train0.index, open=train0['Open'], high=train0['High'], low=train0['Low'], close=train0['Close'], increasing=dict(line=dict(color=act_color0)), decreasing=dict(line=dict(color=act_color0))),

Candlestick(x=train1.index, open=train1['Open'], high=train1['High'], low=train1['Low'], close=train1['Close'], increasing=dict(line=dict(color=act_color1)), decreasing=dict(line=dict(color=act_color1))),

Candlestick(x=train2.index, open=train2['Open'], high=train2['High'], low=train2['Low'], close=train2['Close'], increasing=dict(line=dict(color=act_color2)), decreasing=dict(line=dict(color=act_color2))),

Candlestick(x=test0.index, open=test0['Open'], high=test0['High'], low=test0['Low'], close=test0['Close'], increasing=dict(line=dict(color=act_color0)), decreasing=dict(line=dict(color=act_color0))),

Candlestick(x=test1.index, open=test1['Open'], high=test1['High'], low=test1['Low'], close=test1['Close'], increasing=dict(line=dict(color=act_color1)), decreasing=dict(line=dict(color=act_color1))),

Candlestick(x=test2.index, open=test2['Open'], high=test2['High'], low=test2['Low'], close=test2['Close'], increasing=dict(line=dict(color=act_color2)), decreasing=dict(line=dict(color=act_color2)))

]

title = '{}: train s-reward {}, profits {}, test s-reward {}, profits {}'.format(

algorithm_name,

int(sum(train_rewards)),

int(train_profits),

int(sum(test_rewards)),

int(test_profits)

)

layout = {

'title': title,

'showlegend': False,

'shapes': [

{'x0': date_split, 'x1': date_split, 'y0': 0, 'y1': 1, 'xref': 'x', 'yref': 'paper', 'line': {'color': 'rgb(0,0,0)', 'width': 1}}

],

'annotations': [

{'x': date_split, 'y': 1.0, 'xref': 'x', 'yref': 'paper', 'showarrow': False, 'xanchor': 'left', 'text': ' test data'},

{'x': date_split, 'y': 1.0, 'xref': 'x', 'yref': 'paper', 'showarrow': False, 'xanchor': 'right', 'text': 'train data '}

]

}

figure = Figure(data=data, layout=layout)

iplot(figure)

plot_train_test_by_q(Environment1(train), Environment1(test), Q, ‘DQN’)

Let’s look at Double DQN

def train_ddqn(env):

class Q_Network(chainer.Chain):

def __init__(self, input_size, hidden_size, output_size):

super(Q_Network, self).__init__(

fc1 = L.Linear(input_size, hidden_size),

fc2 = L.Linear(hidden_size, hidden_size),

fc3 = L.Linear(hidden_size, output_size)

)

def __call__(self, x):

h = F.relu(self.fc1(x))

h = F.relu(self.fc2(h))

y = self.fc3(h)

return y

def reset(self):

self.zerograds()

Q = Q_Network(input_size=env.history_t+1, hidden_size=100, output_size=3)

Q_ast = copy.deepcopy(Q)

optimizer = chainer.optimizers.Adam()

optimizer.setup(Q)

epoch_num = 50

step_max = len(env.data)-1

memory_size = 200

batch_size = 50

epsilon = 1.0

epsilon_decrease = 1e-3

epsilon_min = 0.1

start_reduce_epsilon = 200

train_freq = 10

update_q_freq = 20

gamma = 0.97

show_log_freq = 5

memory = []

total_step = 0

total_rewards = []

total_losses = []

start = time.time()

for epoch in range(epoch_num):

pobs = env.reset()

step = 0

done = False

total_reward = 0

total_loss = 0

while not done and step < step_max:

# select act

pact = np.random.randint(3)

if np.random.rand() > epsilon:

pact = Q(np.array(pobs, dtype=np.float32).reshape(1, -1))

pact = np.argmax(pact.data)

# act

obs, reward, done = env.step(pact)

# add memory

memory.append((pobs, pact, reward, obs, done))

if len(memory) > memory_size:

memory.pop(0)

# train or update q

if len(memory) == memory_size:

if total_step % train_freq == 0:

shuffled_memory = np.random.permutation(memory)

memory_idx = range(len(shuffled_memory))

for i in memory_idx[::batch_size]:

batch = np.array(shuffled_memory[i:i+batch_size])

b_pobs = np.array(batch[:, 0].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_pact = np.array(batch[:, 1].tolist(), dtype=np.int32)

b_reward = np.array(batch[:, 2].tolist(), dtype=np.int32)

b_obs = np.array(batch[:, 3].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_done = np.array(batch[:, 4].tolist(), dtype=np.bool)

q = Q(b_pobs)

""" <<< DQN -> Double DQN

maxq = np.max(Q_ast(b_obs).data, axis=1)

=== """

indices = np.argmax(q.data, axis=1)

maxqs = Q_ast(b_obs).data

""" >>> """

target = copy.deepcopy(q.data)

for j in range(batch_size):

""" <<< DQN -> Double DQN

target[j, b_pact[j]] = b_reward[j]+gamma*maxq[j]*(not b_done[j])

=== """

target[j, b_pact[j]] = b_reward[j]+gamma*maxqs[j, indices[j]]*(not b_done[j])

""" >>> """

Q.reset()

loss = F.mean_squared_error(q, target)

total_loss += loss.data

loss.backward()

optimizer.update()

if total_step % update_q_freq == 0:

Q_ast = copy.deepcopy(Q)

# epsilon

if epsilon > epsilon_min and total_step > start_reduce_epsilon:

epsilon -= epsilon_decrease

# next step

total_reward += reward

pobs = obs

step += 1

total_step += 1

total_rewards.append(total_reward)

total_losses.append(total_loss)

if (epoch+1) % show_log_freq == 0:

log_reward = sum(total_rewards[((epoch+1)-show_log_freq):])/show_log_freq

log_loss = sum(total_losses[((epoch+1)-show_log_freq):])/show_log_freq

elapsed_time = time.time()-start

print('\t'.join(map(str, [epoch+1, epsilon, total_step, log_reward, log_loss, elapsed_time])))

start = time.time()

return Q, total_losses, total_rewards

Let’s call this function

Q, total_losses, total_rewards = train_ddqn(Environment1(train))

5 0.26599999999999935 935 -18.8 2.58153205383569 1.4034900665283203 10 0.0999999999999992 1870 6.0 6.38107671495527 2.023881196975708 15 0.0999999999999992 2805 7.6 8.102847685292364 1.800950527191162 20 0.0999999999999992 3740 5.8 2.074553413130343 1.7402253150939941 25 0.0999999999999992 4675 10.6 2.588063887692988 1.7767736911773682 30 0.0999999999999992 5610 9.0 1.692694649938494 1.7709689140319824 35 0.0999999999999992 6545 6.0 1.140931996051222 1.732893943786621 40 0.0999999999999992 7480 -0.2 0.7938342220382765 1.6818647384643555 45 0.0999999999999992 8415 1.0 1.0210695683024824 1.8096415996551514 50 0.0999999999999992 9350 8.8 1.2512135957367718 1.974039077758789

let’s plot loss vs reward

plot_loss_reward(total_losses, total_rewards)

let’s plot Double DQN train/test s-reward vs profits

plot_train_test_by_q(Environment1(train), Environment1(test), Q, ‘Double DQN’)

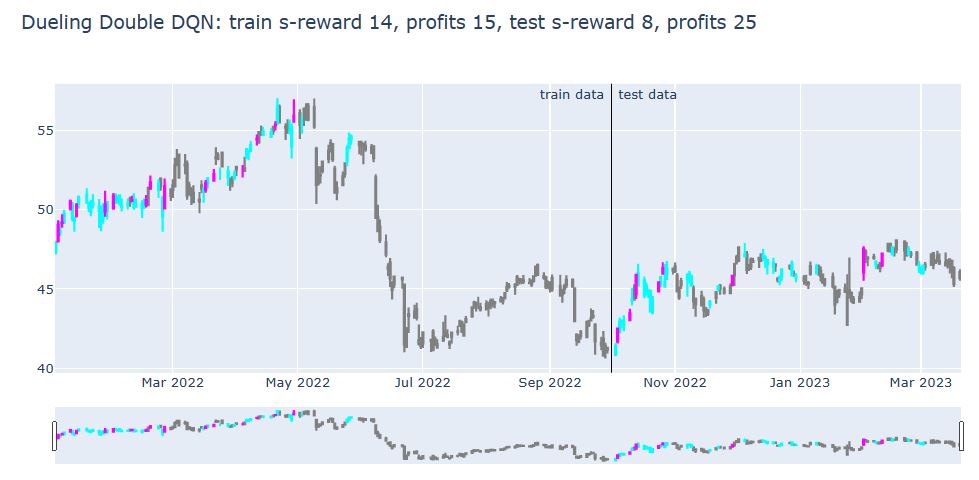

Let’s look at Dueling Double DQN

def train_dddqn(env):

""" <<< Double DQN -> Dueling Double DQN

class Q_Network(chainer.Chain):

def __init__(self, input_size, hidden_size, output_size):

super(Q_Network, self).__init__(

fc1 = L.Linear(input_size, hidden_size),

fc2 = L.Linear(hidden_size, hidden_size),

fc3 = L.Linear(hidden_size, output_size)

)

def __call__(self, x):

h = F.relu(self.fc1(x))

h = F.relu(self.fc2(h))

y = self.fc3(h)

return y

def reset(self):

self.zerograds()

=== """

class Q_Network(chainer.Chain):

def __init__(self, input_size, hidden_size, output_size):

super(Q_Network, self).__init__(

fc1 = L.Linear(input_size, hidden_size),

fc2 = L.Linear(hidden_size, hidden_size),

fc3 = L.Linear(hidden_size, hidden_size//2),

fc4 = L.Linear(hidden_size, hidden_size//2),

state_value = L.Linear(hidden_size//2, 1),

advantage_value = L.Linear(hidden_size//2, output_size)

)

self.input_size = input_size

self.hidden_size = hidden_size

self.output_size = output_size

def __call__(self, x):

h = F.relu(self.fc1(x))

h = F.relu(self.fc2(h))

hs = F.relu(self.fc3(h))

ha = F.relu(self.fc4(h))

state_value = self.state_value(hs)

advantage_value = self.advantage_value(ha)

advantage_mean = (F.sum(advantage_value, axis=1)/float(self.output_size)).reshape(-1, 1)

q_value = F.concat([state_value for _ in range(self.output_size)], axis=1) + (advantage_value - F.concat([advantage_mean for _ in range(self.output_size)], axis=1))

return q_value

def reset(self):

self.zerograds()

""" >>> """

Q = Q_Network(input_size=env.history_t+1, hidden_size=100, output_size=3)

Q_ast = copy.deepcopy(Q)

optimizer = chainer.optimizers.Adam()

optimizer.setup(Q)

epoch_num = 50

step_max = len(env.data)-1

memory_size = 200

batch_size = 50

epsilon = 1.0

epsilon_decrease = 1e-3

epsilon_min = 0.1

start_reduce_epsilon = 200

train_freq = 10

update_q_freq = 20

gamma = 0.97

show_log_freq = 5

memory = []

total_step = 0

total_rewards = []

total_losses = []

start = time.time()

for epoch in range(epoch_num):

pobs = env.reset()

step = 0

done = False

total_reward = 0

total_loss = 0

while not done and step < step_max:

# select act

pact = np.random.randint(3)

if np.random.rand() > epsilon:

pact = Q(np.array(pobs, dtype=np.float32).reshape(1, -1))

pact = np.argmax(pact.data)

# act

obs, reward, done = env.step(pact)

# add memory

memory.append((pobs, pact, reward, obs, done))

if len(memory) > memory_size:

memory.pop(0)

# train or update q

if len(memory) == memory_size:

if total_step % train_freq == 0:

shuffled_memory = np.random.permutation(memory)

memory_idx = range(len(shuffled_memory))

for i in memory_idx[::batch_size]:

batch = np.array(shuffled_memory[i:i+batch_size])

b_pobs = np.array(batch[:, 0].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_pact = np.array(batch[:, 1].tolist(), dtype=np.int32)

b_reward = np.array(batch[:, 2].tolist(), dtype=np.int32)

b_obs = np.array(batch[:, 3].tolist(), dtype=np.float32).reshape(batch_size, -1)

b_done = np.array(batch[:, 4].tolist(), dtype=np.bool)

q = Q(b_pobs)

""" <<< DQN -> Double DQN

maxq = np.max(Q_ast(b_obs).data, axis=1)

=== """

indices = np.argmax(q.data, axis=1)

maxqs = Q_ast(b_obs).data

""" >>> """

target = copy.deepcopy(q.data)

for j in range(batch_size):

""" <<< DQN -> Double DQN

target[j, b_pact[j]] = b_reward[j]+gamma*maxq[j]*(not b_done[j])

=== """

target[j, b_pact[j]] = b_reward[j]+gamma*maxqs[j, indices[j]]*(not b_done[j])

""" >>> """

Q.reset()

loss = F.mean_squared_error(q, target)

total_loss += loss.data

loss.backward()

optimizer.update()

if total_step % update_q_freq == 0:

Q_ast = copy.deepcopy(Q)

# epsilon

if epsilon > epsilon_min and total_step > start_reduce_epsilon:

epsilon -= epsilon_decrease

# next step

total_reward += reward

pobs = obs

step += 1

total_step += 1

total_rewards.append(total_reward)

total_losses.append(total_loss)

if (epoch+1) % show_log_freq == 0:

log_reward = sum(total_rewards[((epoch+1)-show_log_freq):])/show_log_freq

log_loss = sum(total_losses[((epoch+1)-show_log_freq):])/show_log_freq

elapsed_time = time.time()-start

print('\t'.join(map(str, [epoch+1, epsilon, total_step, log_reward, log_loss, elapsed_time])))

start = time.time()

return Q, total_losses, total_rewards

Let’s call the function

plot_train_test_by_q(Environment1(train), Environment1(test), Q, ‘Dueling Double DQN’)

Summary

- This work represents a DRL model to generate profitable trades in the $MO stock data, effectively overcoming the limitations of supervised ML approaches.

- Results show that the accuracy of DRL in stock price prediction as well as the stability of rapid prediction have both been significantly enhanced.

- Therefore, it is more suitable for use in periods of turbulent market compared to traditional forecast methods.

- Overall, this study demonstrates the superiority of DRL in financial markets over other types of ML/AI and proves its credibility and advantages of investment decision-making.

Explore More

The Donchian Channel vs Buy-and-Hold Breakout Trading Systems – $MO Use-Case

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment