Featured Photo by Pixabay

In this post, we will look at the JPM stock price and relevant breakout strategies for 2022-23. Referring to the previous case study, our goal is to combine the Auto ARIMA, FFT, LSTM models and Technical Trading Indicators (TTIs) into a single framework to optimize advantages of each. Specifically, we will focus on the following TTIs: EMA, RSI, OBV, and MCAD.

Table of Contents

- ARIMA

- FFT

- TTIs

- LSTM

- Summary

- Continue Reading

- Algo Trading Links

- Stock Market Links

- min(Risk/Reward Ratio) Links

- Portfolio De-Risking Links

ARIMA

Let’s set the working directory

import os

os.chdir(‘YOURPATH’)

os. getcwd()

Let’s download the input data

import yfinance as yf

gs = yf.download(“JPM”, start=”2022-01-03″, end=”2023-03-21″)

[*********************100%***********************] 1 of 1 completed

gs.tail()

Let’s preprocess the data

import pandas as pd

dataset_ex_df = gs.copy()

dataset_ex_df = dataset_ex_df.reset_index()

dataset_ex_df[‘Date’] = pd.to_datetime(dataset_ex_df[‘Date’])

dataset_ex_df.set_index(‘Date’, inplace=True)

dataset_ex_df = dataset_ex_df[‘Close’].to_frame()

Let’s run Auto ARIMA to select optimal ARIMA parameters

from pmdarima.arima import auto_arima

model = auto_arima(dataset_ex_df[‘Close’], seasonal=False, trace=True)

print(model.summary())

Performing stepwise search to minimize aic

ARIMA(2,1,2)(0,0,0)[0] intercept : AIC=inf, Time=0.32 sec

ARIMA(0,1,0)(0,0,0)[0] intercept : AIC=1393.617, Time=0.01 sec

ARIMA(1,1,0)(0,0,0)[0] intercept : AIC=1394.786, Time=0.02 sec

ARIMA(0,1,1)(0,0,0)[0] intercept : AIC=1394.835, Time=0.02 sec

ARIMA(0,1,0)(0,0,0)[0] : AIC=1392.302, Time=0.01 sec

ARIMA(1,1,1)(0,0,0)[0] intercept : AIC=1396.288, Time=0.07 sec

Best model: ARIMA(0,1,0)(0,0,0)[0]

Total fit time: 0.456 seconds

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 304

Model: SARIMAX(0, 1, 0) Log Likelihood -695.151

Date: Tue, 21 Mar 2023 AIC 1392.302

Time: 11:09:24 BIC 1396.016

Sample: 0 HQIC 1393.788

- 304

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

sigma2 5.7579 0.365 15.773 0.000 5.042 6.473

===================================================================================

Ljung-Box (L1) (Q): 0.82 Jarque-Bera (JB): 22.57

Prob(Q): 0.36 Prob(JB): 0.00

Heteroskedasticity (H): 0.50 Skew: -0.25

Prob(H) (two-sided): 0.00 Kurtosis: 4.24

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Let’s define the ARIMA prediction model

from statsmodels.tsa.arima.model import ARIMA

import numpy as np

def arima_forecast(history):

# Fit the model

model = ARIMA(history, order=(0,1,0))

model_fit = model.fit()

# Make the prediction

output = model_fit.forecast()

yhat = output[0]

return yhat

Let’s split the data into train and test sets

X = dataset_ex_df.values

size = int(len(X) * 0.8)

train, test = X[0:size], X[size:len(X)]

Walk-forward validation to generate a prediction:

history = [x for x in train]

predictions = list()

for t in range(len(test)):

yhat = arima_forecast(history)

predictions.append(yhat)

Let’s add the predicted value to the training set

obs = test[t]

history.append(obs)

Let’s plot the result

import matplotlib.pyplot as plt

plt.figure(figsize=(12, 6), dpi=100)

plt.plot(dataset_ex_df.iloc[size:,:].index, test, label=’Real’)

plt.plot(dataset_ex_df.iloc[size:,:].index, predictions, color=’red’, label=’Predicted’)

plt.title(‘ARIMA Predictions vs Actual Values’)

plt.xlabel(‘Date’)

plt.ylabel(‘Stock Price’)

plt.legend()

plt.show()

FFT

Let’ calculate the Fourier Transform

data_FT = dataset_ex_df[[‘Close’]]

close_fft = np.fft.fft(np.asarray(data_FT[‘Close’].tolist()))

fft_df = pd.DataFrame({‘fft’:close_fft})

fft_df[‘absolute’] = fft_df[‘fft’].apply(lambda x: np.abs(x))

fft_df[‘angle’] = fft_df[‘fft’].apply(lambda x: np.angle(x))

and plot the partial Fourier Transforms

plt.figure(figsize=(14, 7), dpi=100)

plt.plot(np.asarray(data_FT[‘Close’].tolist()), label=’Real’)

for num_ in [9, 12, 15]:

fft_list_m10= np.copy(close_fft); fft_list_m10[num_:-num_]=0

plt.plot(np.fft.ifft(fft_list_m10), label=’Fourier transform with {} components’.format(num_))

plt.xlabel(‘Days’)

plt.ylabel(‘USD’)

plt.title(‘JPM (close) stock prices & Fourier transforms’)

plt.legend()

plt.show()

TTIs

Let’s calculate EMA

def ema(close, period=20):

return close.ewm(span=period, adjust=False).mean()

Let’s calculate RSI

def rsi(close, period=14):

delta = close.diff()

gain, loss = delta.copy(), delta.copy()

gain[gain < 0] = 0 loss[loss > 0] = 0

avg_gain = gain.rolling(period).mean()

avg_loss = abs(loss.rolling(period).mean())

rs = avg_gain / avg_loss

rsi = 100.0 – (100.0 / (1.0 + rs))

return rsi

Let’s calculate MACD

def macd(close, fast_period=12, slow_period=26, signal_period=9):

fast_ema = close.ewm(span=fast_period, adjust=False).mean()

slow_ema = close.ewm(span=slow_period, adjust=False).mean()

macd_line = fast_ema – slow_ema

signal_line = macd_line.ewm(span=signal_period, adjust=False).mean()

histogram = macd_line – signal_line

return macd_line

Let’s calculate OBV

def obv(close, volume):

obv = np.where(close > close.shift(), volume, np.where(close < close.shift(), -volume, 0)).cumsum()

return obv

Let’s add TTIs to the dataset DF

dataset_ex_df[’ema_20′] = ema(gs[“Close”], 20)

dataset_ex_df[’ema_50′] = ema(gs[“Close”], 50)

dataset_ex_df[’ema_100′] = ema(gs[“Close”], 100)

dataset_ex_df[‘rsi’] = rsi(gs[“Close”])

dataset_ex_df[‘macd’] = macd(gs[“Close”])

dataset_ex_df[‘obv’] = obv(gs[“Close”], gs[“Volume”])

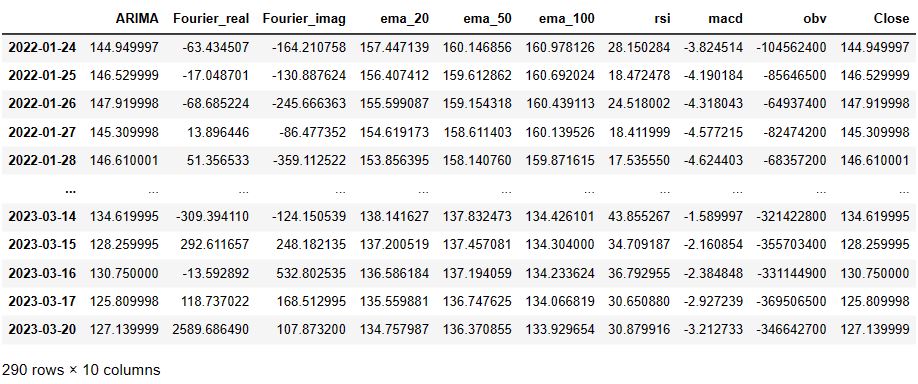

Let’s create arima DF using predictions

arima_df = pd.DataFrame(history, index=dataset_ex_df.index, columns=[‘ARIMA’])

Let’s set the Fourier Transforms DF

fft_df.reset_index(inplace=True)

fft_df[‘index’] = pd.to_datetime(dataset_ex_df.index)

fft_df.set_index(‘index’, inplace=True)

fft_df_real = pd.DataFrame(np.real(fft_df[‘fft’]), index=fft_df.index, columns=[‘Fourier_real’])

fft_df_imag = pd.DataFrame(np.imag(fft_df[‘fft’]), index=fft_df.index, columns=[‘Fourier_imag’])

The TTIs DF is

technical_indicators_df = dataset_ex_df[[’ema_20′, ’ema_50′, ’ema_100′, ‘rsi’, ‘macd’, ‘obv’, ‘Close’]]

Let’s create the merged DF

merged_df = pd.concat([arima_df, fft_df_real, fft_df_imag, technical_indicators_df], axis=1)

merged_df = merged_df.dropna()

merged_df

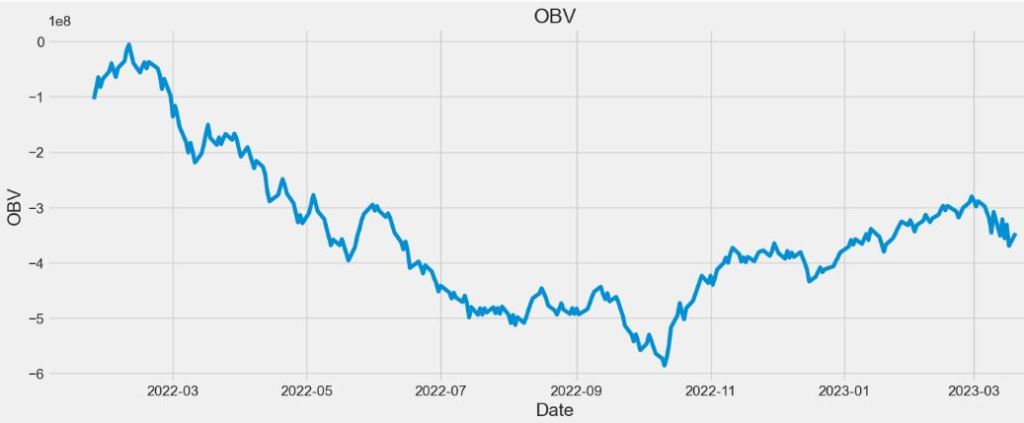

Let’s plot OBV

plt.figure(figsize=(16,6))

plt.title(‘OBV’)

plt.plot(merged_df[‘obv’])

plt.xlabel(‘Date’, fontsize=18)

plt.ylabel(‘OBV’, fontsize=18)

plt.show()

Let’s plot other TTIs against the stock price

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style(‘whitegrid’)

plt.style.use(“fivethirtyeight”)

%matplotlib inline

from pandas_datareader.data import DataReader

import yfinance as yf

from pandas_datareader import data as pdr

yf.pdr_override()

from datetime import datetime

df = pdr.get_data_yahoo(‘JPM’, start=’2022-01-01′, end=datetime.now())

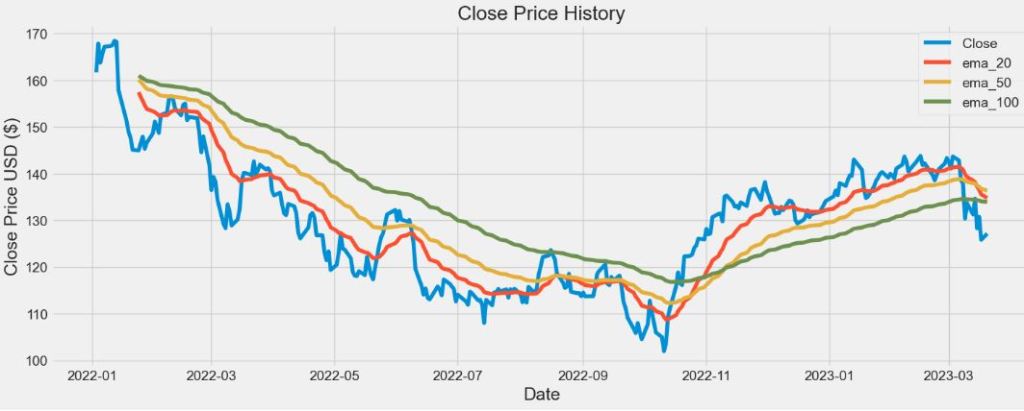

Let’s plot EMA TTI

plt.figure(figsize=(16,6))

plt.title(‘Close Price History’)

plt.plot(df[‘Close’])

plt.plot(merged_df[’ema_20′])

plt.plot(merged_df[’ema_50′])

plt.plot(merged_df[’ema_100′])

plt.legend([‘Close’, ’ema_20′,’ema_50′,’ema_100′], loc=’upper right’)

plt.xlabel(‘Date’, fontsize=18)

plt.ylabel(‘Close Price USD ($)’, fontsize=18)

plt.show()

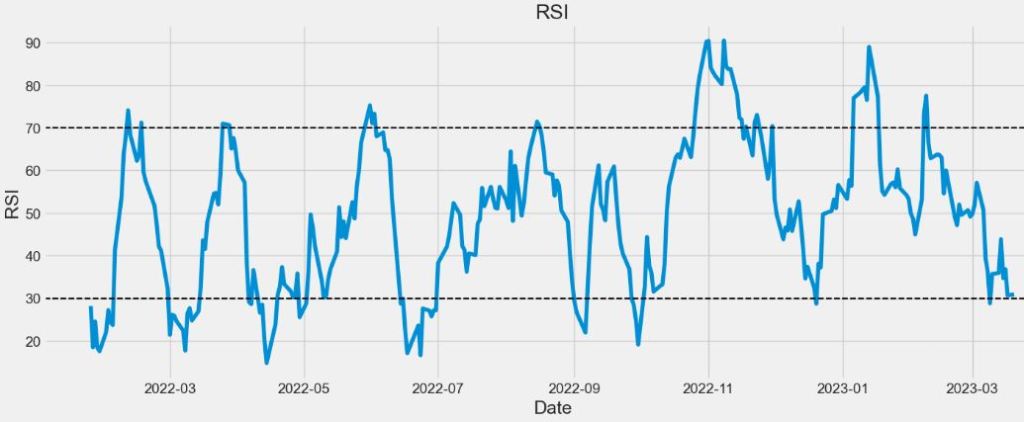

Let’s plot RSI TTI

plt.figure(figsize=(16,6))

plt.title(‘RSI’)

plt.plot(merged_df[‘rsi’])

plt.xlabel(‘Date’, fontsize=18)

plt.ylabel(‘RSI’, fontsize=18)

plt.axhline(30, linestyle = ‘–‘, linewidth = 1.5, color = ‘black’)

plt.axhline(70, linestyle = ‘–‘, linewidth = 1.5, color = ‘black’)

plt.show()

Let’s plot MACD TTI

def get_macd(price, slow, fast, smooth):

exp1 = price.ewm(span = fast, adjust = False).mean()

exp2 = price.ewm(span = slow, adjust = False).mean()

macd = pd.DataFrame(exp1 – exp2).rename(columns = {‘Close’:’macd’})

signal = pd.DataFrame(macd.ewm(span = smooth, adjust = False).mean()).rename(columns = {‘macd’:’signal’})

hist = pd.DataFrame(macd[‘macd’] – signal[‘signal’]).rename(columns = {0:’hist’})

frames = [macd, signal, hist]

df = pd.concat(frames, join = ‘inner’, axis = 1)

return df

googl_macd = get_macd(df[‘Close’], 26, 12, 9)

googl_macd.tail()

def plot_macd(prices, macd, signal, hist):

plt.figure(figsize=(16,6))

plt.plot(macd, color = 'black', linewidth = 1.5, label = 'MACD')

plt.plot(signal, color = 'blue', linewidth = 1.5, label = 'SIGNAL')

for i in range(len(prices)):

if str(hist[i])[0] == '-':

plt.bar(prices.index[i], hist[i], color = '#ef5350')

else:

plt.bar(prices.index[i], hist[i], color = '#26a69a')

plt.legend(loc = 'upper left')

plot_macd(df[‘Close’], googl_macd[‘macd’], googl_macd[‘signal’], googl_macd[‘hist’])

LSTM

Create a new dataframe with only the ‘Close column

data = df.filter([‘Close’])

dataset = data.values

training_data_len = int(np.ceil( len(dataset) * .95 ))

training_data_len

289

Let’s scale the data

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler(feature_range=(0,1))

scaled_data = scaler.fit_transform(dataset)

Let’s create the scaled training data set

train_data = scaled_data[0:int(training_data_len), :]

x_train = []

y_train = []

for i in range(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])

if i<= 61:

print(x_train)

print(y_train)

print()

x_train, y_train = np.array(x_train), np.array(y_train)

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

Let’s build, compile and train the LSTM model

from keras.models import Sequential

from keras.layers import Dense, LSTM

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

model.compile(optimizer=’adam’, loss=’mean_squared_error’)

history=model.fit(x_train, y_train, batch_size=1, epochs=32)

print(model.summary())

Model: "sequential_7"

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

lstm_6 (LSTM) (None, 60, 128) 66560

lstm_7 (LSTM) (None, 64) 49408

dense_18 (Dense) (None, 25) 1625

dense_19 (Dense) (None, 1) 26

=================================================================

Total params: 117,619

Trainable params: 117,619

Non-trainable params: 0

___________________________

Let’s create the testing data set

test_data = scaled_data[training_data_len – 60: , :]

x_test = []

y_test = dataset[training_data_len:, :]

for i in range(60, len(test_data)):

x_test.append(test_data[i-60:i, 0])

x_test = np.array(x_test)

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1 ))

Let’s get the predicted price values

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

rmse = np.sqrt(np.mean(((predictions – y_test) ** 2)))

rmse

3.6409877950086997

Let’s calculate the test data metrics

y_pred=predictions

mse = mean_squared_error(y_test, y_pred)

rmse = np.sqrt(mse)

mae = mean_absolute_error(y_test, y_pred)

r2 = r2_score(y_test, y_pred)

evs = explained_variance_score(y_test, y_pred)

mape = np.mean(np.abs((y_test – y_pred) / y_test)) * 100

mpe = np.mean((y_test – y_pred) / y_test) * 100

print(f”Mean Squared Error (MSE): {mse}”)

print(f”Mean Absolute Error (MAE): {mae}”)

print(f”R2 Score: {r2}”)

print(f”Explained Variance Score: {evs}”)

print(f”Mean Absolute Percentage Error (MAPE): {mape}”)

print(f”Mean Percentage Error (MPE): {mpe}”)

Mean Squared Error (MSE): 13.256792123402313 Mean Absolute Error (MAE): 3.025512186686198 R2 Score: 0.64814314091558 Explained Variance Score: 0.6481807176153842 Mean Absolute Percentage Error (MAPE): 2.2817656702555715 Mean Percentage Error (MPE): -0.0674398726228619

Let’s visualize the data

train = data[:training_data_len]

valid = data[training_data_len:]

valid[‘Predictions’] = predictions

plt.figure(figsize=(16,6))

plt.title(‘Model’)

plt.xlabel(‘Date’, fontsize=18)

plt.ylabel(‘Close Price USD ($)’, fontsize=18)

plt.plot(train[‘Close’])

plt.plot(valid[[‘Close’, ‘Predictions’]])

plt.legend([‘Train’, ‘Val’, ‘Predictions’], loc=’lower right’)

plt.show()

Let’s plot the keys

print(history.history.keys())

dict_keys(['loss'])

plt.plot(history.history[‘loss’])

plt.ylabel(‘Loss’)

plt.xlabel(‘epoch’)

Finally, let’ print the validation and predicted prices

valid

Summary

We compared several techniques to predict the JPM stock price for 2022-2023.

- The (Auto) ARIMA model was built using historical data to forecast future trends.

- This best model ARIMA(0,1,0)(0,0,0)[0] was assessed using the SARIMAX comprehensive statistical output.

- We invoked the FFT partial spectral decompositions of stock prices as model features.

- We calculated s set of TTIs (EMA, RSI, MACD, and OBV) to validate the JPM trading breakouts.

- The reliable LSTM model was built to predict stock prices with RMSE=3.6.

- We assessed the LSTM performance using MSE, MAE, R2 score, explained variance score, MAPE, and MPE.

Continue Reading

Risk-Return Analysis and LSTM Price Predictions of 4 Major Tech Stocks in 2023

Revision 360 of Risk Aware Investing after SVB Collapse – 1. The Financial Sector

Portfolio max(Return/Risk) Stochastic Optimization of 20 Dividend Growth Stocks

SARIMAX X-Validation of EIA Crude Oil Prices Forecast in 2023 – 2. Brent

SARIMAX X-Validation of EIA Crude Oil Prices Forecast in 2023 – 1. WTI

SARIMAX-TSA Forecasting, QC and Visualization of E-Commerce Food Delivery Sales

Python Technical Analysis for BioTech – Get Buy Alerts on ABBV in 2023

Algo Trading Links

- DJI Market State Analysis using the Cruz Fitting Algorithm

- A TradeSanta’s Quick Guide to Best Swing Trading Indicators

- The Qullamaggie’s OXY Swing Breakouts

- The Qullamaggie’s TSLA Breakouts for Swing Traders

- Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

- Algorithmic Trading using Monte Carlo Predictions and 62 AI-Assisted Trading Technical Indicators (TTI)

- Basic Stock Price Analysis in Python

- S&P 500 Algorithmic Trading with FBProphet

- Predicting Trend Reversal in Algorithmic Trading using Stochastic Oscillator in Python

- Stock Forecasting with FBProphet

- Short-Term Stock Market Price Prediction using Deep Learning Models

- ML/AI Regression for Stock Prediction – AAPL Use Case

- Supervised ML/AI Stock Prediction using Keras LSTM Models

Stock Market Links

- A Comparative Analysis of The 3 Best Global Growth Stocks in Q1’23 – 2. AZN

- Stocks to Watch in 2023: MarketBeat Ideas

- Zacks Investment Research Update Q4’22

- The Zacks Steady Investor – A Quick Look

- All Eyes on ETFs Sep ’22

- Zacks Insights into this High Inflation/Rising Rate Market

- SeekingAlpha Risk/Reward July Rundown

- Zacks Insights into the Commodity Bull Market

- Are Blue-Chips Perfect for This Bear Market?

- Bear Market Similarity Analysis using Nasdaq 100 Index Data

- AAPL Stock Technical Analysis 2 June 2022

- Inflation-Resistant Stocks to Buy

- A Weekday Market Research Update

- Stocks on Watch Tomorrow

- Stock Market ’22 Round Up & ’23 Outlook: Zacks Strategy vs Seeking Alpha Tactics

min(Risk/Reward Ratio) Links

- Towards min(Risk/Reward) – SeekingAlpha August Bear Market Update

- Upswing Resilient Investor Guide

- Investment Risk Management Study

- RISK AWARE INVESTMENT: GUIDE FOR EVERYONE

Portfolio De-Risking Links

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- Risk/Return POA – Dr. Dividend’s Positions

- Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

- Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

- Stock Portfolio Risk/Return Optimization

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment