Contents:

Introduction

Facebook Prophet is open-source library released by Facebook’s Core Data Science team. It is available in R and Python. Prophet is a procedure for univariate (one variable) time series forecasting data based on an additive model, and the implementation supports trends, seasonality, and holidays. It works best with time series that have strong seasonal effects and several seasons of historical data. Prophet is robust to missing data and shifts in the trend, and typically handles outliers well.

See References below.

Installations

Let’s install Anaconda IDE and set up the appropriate Conda environment

cd ~\anaconda3\condabin

conda info

conda update conda

#To activate this environment, use

#conda activate stan_env

#To deactivate an active environment, use

#conda deactivate

conda activate stan_env

conda install libpython m2w64-toolchain -c msys2

conda install numpy cython -c conda-forge

conda install matplotlib scipy pandas -c conda-forge

conda install pystan -c conda-forge

conda install -c anaconda ephem

conda install -c conda-forge fbprophet

Let’s open the Jupyter notebook and install the following libraries within stan_env

!pip install yfinance

import yfinance as yf

!pip install chart_studio

import pandas as pd

import numpy as np

import scipy as sp

import chart_studio.plotly as py

from fbprophet import Prophet

Predictions

We read historical stock data using Yahoo Finance. For example, let’s look at AMZN

stock_ticker = ‘AMZN’

yfin = yf.Ticker(stock_ticker)

hist = yfin.history(period=”max”)

hist = hist[[‘Close’]]

hist.reset_index(level=0, inplace=True)

hist = hist.rename({‘Date’: ‘ds’, ‘Close’: ‘y’}, axis=’columns’)

m = Prophet(daily_seasonality=True)

m.fit(hist)

future = m.make_future_dataframe(periods=365)

forecast = m.predict(future)

pd.options.display.max_columns = None

print(forecast.tail(2))

ds trend yhat_lower yhat_upper trend_lower \

6669 2023-06-02 4078.16732 3849.983952 4234.406491 4062.805046

6670 2023-06-03 4079.59198 3858.633118 4244.843251 4064.126297

trend_upper additive_terms additive_terms_lower additive_terms_upper \

6669 4094.250080 -27.515668 -27.515668 -27.515668

6670 4095.713544 -20.885808 -20.885808 -20.885808

daily daily_lower daily_upper weekly weekly_lower \

6669 -4.041229 -4.041229 -4.041229 -2.170906 -2.170906

6670 -4.041229 -4.041229 -4.041229 0.505153 0.505153

weekly_upper yearly yearly_lower yearly_upper \

6669 -2.170906 -21.303533 -21.303533 -21.303533

6670 0.505153 -17.349732 -17.349732 -17.349732

multiplicative_terms multiplicative_terms_lower \

6669 0.0 0.0

6670 0.0 0.0

multiplicative_terms_upper yhat

6669 0.0 4050.651652

6670 0.0 4058.706171

print(forecast[[‘ds’, ‘yhat’, ‘yhat_lower’, ‘yhat_upper’]].tail())

ds yhat yhat_lower yhat_upper 6666 2023-05-30 4037.772562 3842.484407 4226.067427 6667 2023-05-31 4043.137454 3847.566906 4241.015891 6668 2023-06-01 4047.812058 3841.219833 4243.001044 6669 2023-06-02 4050.651652 3849.983952 4234.406491 6670 2023-06-03 4058.706171 3858.633118 4244.843251

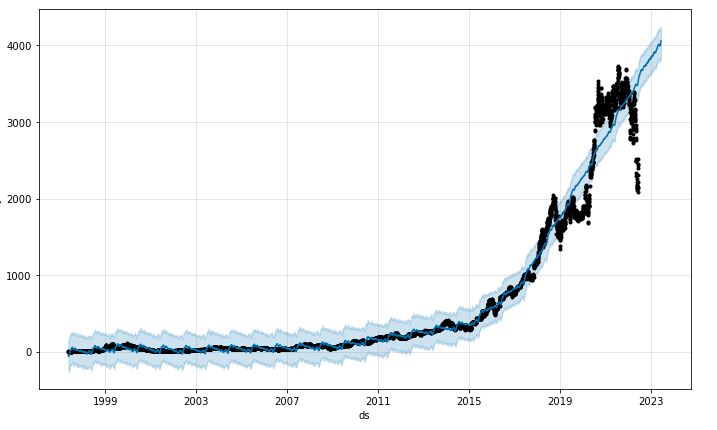

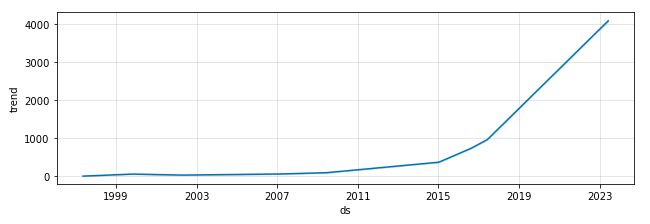

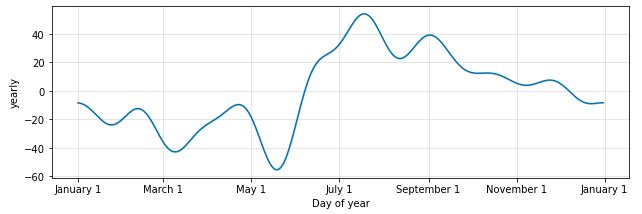

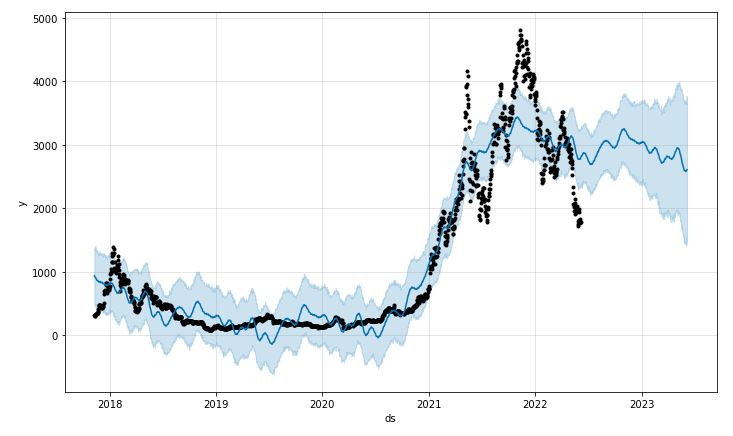

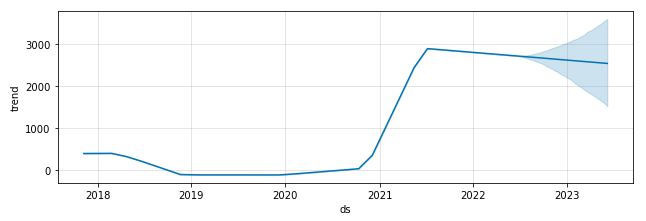

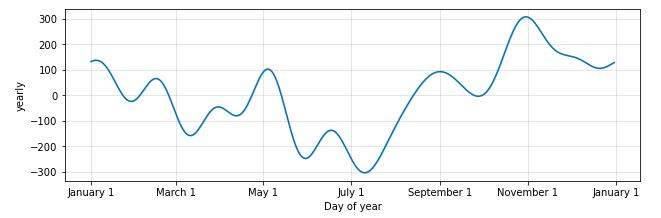

figure1 = m.plot(forecast)

figure2 = m.plot_components(forecast)

Let’s apply the function

def predict(ticker,days):

yfin = yf.Ticker(ticker)

print(“Stock: “, yfin.info[‘name’])

hist = yfin.history(period=”max”)

hist = hist[[‘Close’]]

hist.reset_index(level=0, inplace=True)

hist = hist.rename({‘Date’: ‘ds’, ‘Close’: ‘y’}, axis=’columns’)

print(“Curent Data”)

print(hist.tail())

m = Prophet(daily_seasonality=True)

m.fit(hist)

future = m.make_future_dataframe(periods=days)

forecast = m.predict(future)

print(“Predicted Data”)

print(forecast[[‘ds’, ‘yhat’, ‘yhat_lower’, ‘yhat_upper’]].tail())

figure1 = m.plot(forecast)

figure2 = m.plot_components(forecast)

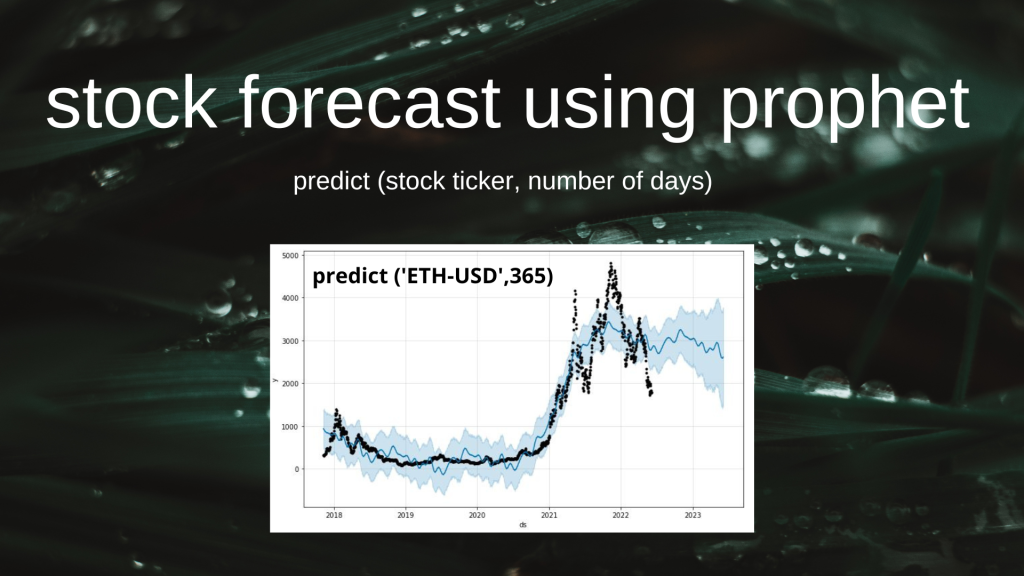

to the ETH-USD stock

predict(“ETH-USD”,365)

Stock: Ethereum

Curent Data

ds y

1665 2022-06-01 1823.569336

1666 2022-06-02 1834.150513

1667 2022-06-03 1775.078613

1668 2022-06-04 1801.609497

1669 2022-06-05 1784.663208

Predicted Data

ds yhat yhat_lower yhat_upper

2030 2023-06-01 2582.743017 1444.113747 3676.835993

2031 2023-06-02 2580.967269 1406.940449 3641.467382

2032 2023-06-03 2590.692980 1542.385844 3718.909670

2033 2023-06-04 2599.084116 1497.965969 3772.736086

2034 2023-06-05 2609.541418 1444.553404 3732.228581

For comparison, let’s look at BTC-USD

predict(“BTC-USD”,365)

Stock: Bitcoin

Curent Data

ds y

2814 2022-06-01 29799.080078

2815 2022-06-02 30467.488281

2816 2022-06-03 29704.390625

2817 2022-06-04 29832.914062

2818 2022-06-05 29661.175781

Predicted Data

ds yhat yhat_lower yhat_upper

3179 2023-06-01 62526.361633 53359.687572 71979.300304

3180 2023-06-02 62678.484615 52661.381831 71895.027878

3181 2023-06-03 62855.408456 52764.612352 73328.871401

3182 2023-06-04 63017.050166 53448.588579 72521.046230

3183 2023-06-05 63261.548650 53875.600863 73277.660442

Comments

- Time series forecasting is one of most demanding object in machine learning. The easiest way for projecting your time series data is using a module named Prophet (aka fbprophet). This is a procedure for forecasting time series data based on an additive model where non-linear trends are fit with yearly, weekly, and daily seasonality, plus holiday effects.

- Prophet follows the

sklearnmodel API. We create an instance of theProphetclass and then call itsfitandpredictmethods. We fit the model by instantiating a newProphetobject. Any settings to the forecasting procedure are passed into the constructor. Then you call itsfitmethod and pass in the historical dataframe. Fitting should take 1-5 seconds.

- By default, Prophet uses a linear model for its forecast. When forecasting growth, there is usually some maximum achievable point: total market size, total population size, etc. This is called the carrying capacity, and the forecast should saturate at this point.

- Prophet allows you to make forecasts using a logistic growth trend model, with a specified carrying capacity.

- Prophet will only work for Python < 3.9. We need to build a new environment in Anaconda. This environment will only focus on time series forecasting using fbprophet. Don’t forget to add anaconda python path into environment variable inside Windows system Path.

- You can plot the forecast by calling the

Prophet.plotmethod and passing in your forecast dataframe.

Summary

We have implemented fbprophet assisted stock prediction in Python by applying the function predict(stock ticker, number of days) to stocks AMZN, ETH-USD and BTC-USD while importing historical stock data from Yahoo Finance.

References

Hareesh Pallathoor Balakrishnan (2021) Stock Prediction using Prophet (Python).

Handhika Yanuar Pratama (2021) Installing FBProphet/Prophet for Time Series Forecasting in Jupyter Notebook.

GitHub Prophet Documentation – Quick Start.

StackOverflow: Installing fbprophet Python on Windows 10

Mitchell Krieger (2021) Time Series Analysis with Facebook Prophet: How it works and How to use it.

Leave a comment