Tag: sharpe ratio

-

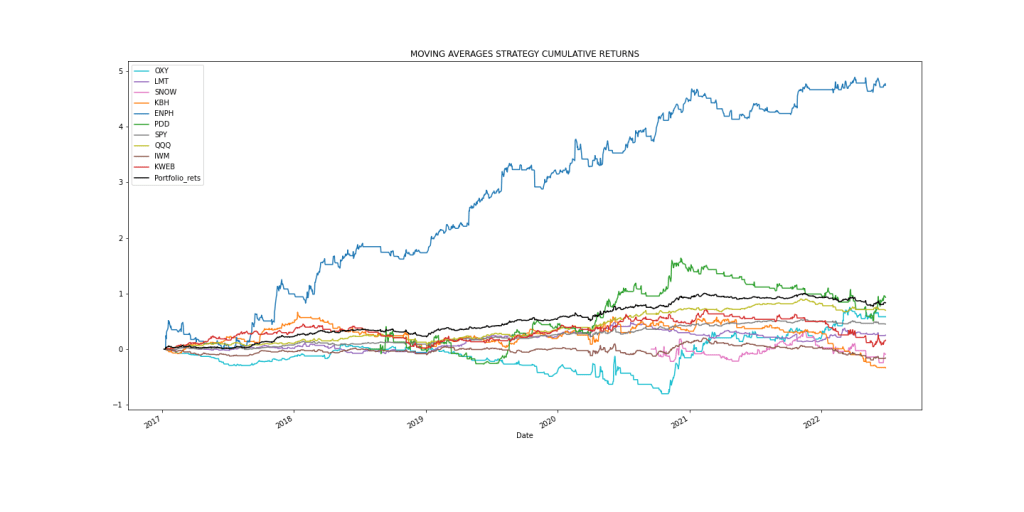

Multiple-Criteria Technical Analysis of Blue Chips in Python

Blue chip stocks are the stocks of well-known, high-quality companies. We demonstrate that the proposed approach can help optimize the blue-chip portfolios comprehensively.

-

Joint Analysis of Bitcoin, Gold and Crude Oil Prices

The content discusses a comprehensive analysis on a joint time-series analysis of Bitcoin, Gold and Crude Oil prices from 2021 to 2023. It explores data processing, exploratory data analysis before running a range of statistical tests, ARIMA models fitting, and finally, using the Markowitz portfolio optimization method. It then presents a detailed analysis, including data…

-

Gold Price Linear Regression

This content focuses on predicting gold prices using machine learning algorithms in Python. With an 80% R2-score and a Sharpe ratio of 2.33, it suggests a potential 8% revenue from an investment starting in December 2022. The forecasted next-day price for SPDR Gold Trust Shares is $185.136, aligning with Barchart’s “100% BUY” signal.

-

Donchian Channel Trading Systems

This article explores the application of algo trading using Python for Altria Group, Inc., a Dividend King diversifying beyond smoking. The historical data for Altria is used to test and contrast trading strategies based on the Donchian Channel indicator. The key is to compare the highest total return when using the Donchian Channel Breakout versus…

-

Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

Based on the Portfolio Allocation and Optimization Algorithm discussed earlier and the related portfolio management, let’s run the Bear vs. Bull QC test of the portfolio P=[MSFT, AAPL, NDAQ] in terms of the Risk/Return Ratio (RRR). We have got a Sharpe ratio of less than one that is considered unacceptable or bad. The risk the…

-

Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

Investors can optimize their stock portfolio by invoking backtesting within the realm of algorithmic trading. The goal is to optimize the specific portfolio by maximizing returns and the Sharpe ratio.