Investors can optimize their stock portfolio by invoking backtesting within the realm of algorithmic trading. The goal is to optimize the specific portfolio by maximizing returns and the Sharpe ratio.

The workflow in Python consists of the following steps:

- Import/install relevant libraries

- Define the stock portfolio & time interval

- Download historical data from Yfinance

- Apply the MVA strategy function to stock data

- Calculate cumulative returns and the annual Sharpe ratio

- Plot cumulative returns of individual stocks and the portfolio return

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

and import/install the following libraries

!pip install nsepy

import warnings

warnings.filterwarnings(‘ignore’)

import numpy as np

import pandas as pd

from datetime import datetime as dt

import yfinance as yf

import nsepy

from statistics import mean

Let’s define the following functions

Get daily data from Yfinance

def get_daily_data(symbol, start, end):

data = yf.download(tickers=symbol, start=start, end=end)

return data

MVA strategy on close price data

def ma(data,ma1,ma2):

# calculating moving averages

data[‘ma_short’] = data[‘Close’].ewm(span=ma1).mean().shift()

data[‘ma_long’] = data[‘Close’].ewm(span=ma2).mean().shift()

# creating positions

# data["position"] = [0]*len(data)

data['position'] = np.where(data["ma_short"] > data["ma_long"], 1, 0)

data["strategy_returns"] = data["bnh_returns"] * data["position"]

# returning strategy returns

return data["strategy_returns"]

Cumulative returns function

def get_cumulative_return(df):

return list(df.cumsum())[-1]

Annual Sharpe ratio function

def get_annualized_sharpe_ratio(df):

return 252**(1/2) * (df.mean() / df.std())

Let’s define the backtesting parameters

days = 2000

end = dt.today()

start = end – pd.Timedelta(days=days)

and the stock portfolio

portfolio_stocks = [“OXY”,”LMT”,”SNOW”,”KBH”,”ENPH”,”PDD”,”SPY”,”QQQ”,”IWM”,”KWEB”,]

based on the available market research studies, technical analysis, updates, market trends, and stock screeners.

Let’s define a data frame to store portfolio returns

portfolio_strategy_returns = pd.DataFrame()

portfolio_bnh_returns = pd.DataFrame()

Buy and hold returns for individual stocs

bnh_stock_returns = []

bnh_stock_sharpe = []

iterating over stocks in the portfolio

for stock in portfolio_stocks:

data = get_daily_data(stock, start, end)

# Calculating daily returns

data["bnh_returns"] = np.log(data["Close"]/data["Close"].shift())

portfolio_strategy_returns[stock] = ma(data,ma1 = 3, ma2 = 8)

bnh_stock_returns.append(get_cumulative_return(data["strategy_returns"]))

bnh_stock_sharpe.append(get_annualized_sharpe_ratio(data["strategy_returns"]))

[*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed

print(“\nSTRATEGY RETURNS ON PORTFOLIO”)

portfolio_strategy_returns[“Portfolio_rets”] = portfolio_strategy_returns.mean(axis=1)

portfolio_strategy_returns.round(decimals = 4).tail(10)

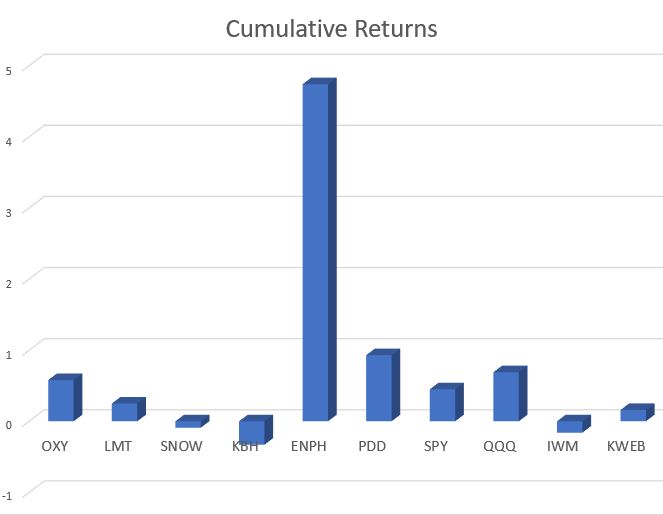

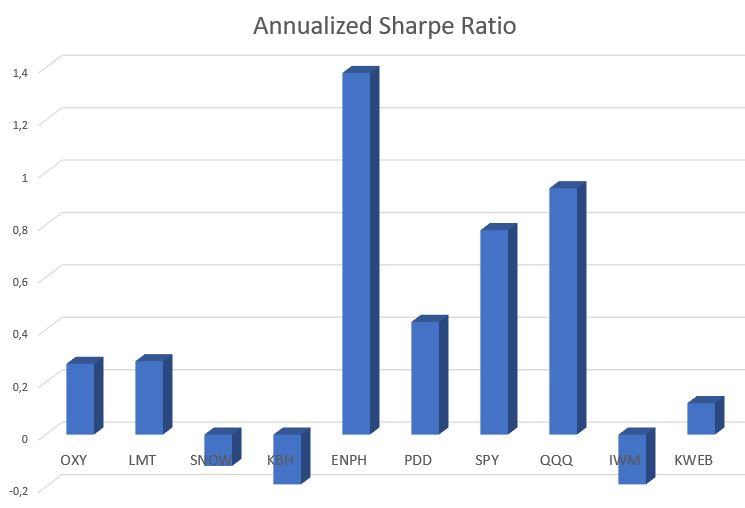

perf = pd.DataFrame(index=portfolio_stocks,columns=[“Cumulative returns”,”Annualized Sharpe Ratio”])

for i,stock in enumerate(portfolio_stocks):

cum_ret = bnh_stock_returns[i]

anu_shp = bnh_stock_sharpe[i]

perf.loc[stock] = [cum_ret,anu_shp]

perf

perf.mean()

Cumulative returns 0.722194 Annualized Sharpe Ratio 0.369893 dtype: float64

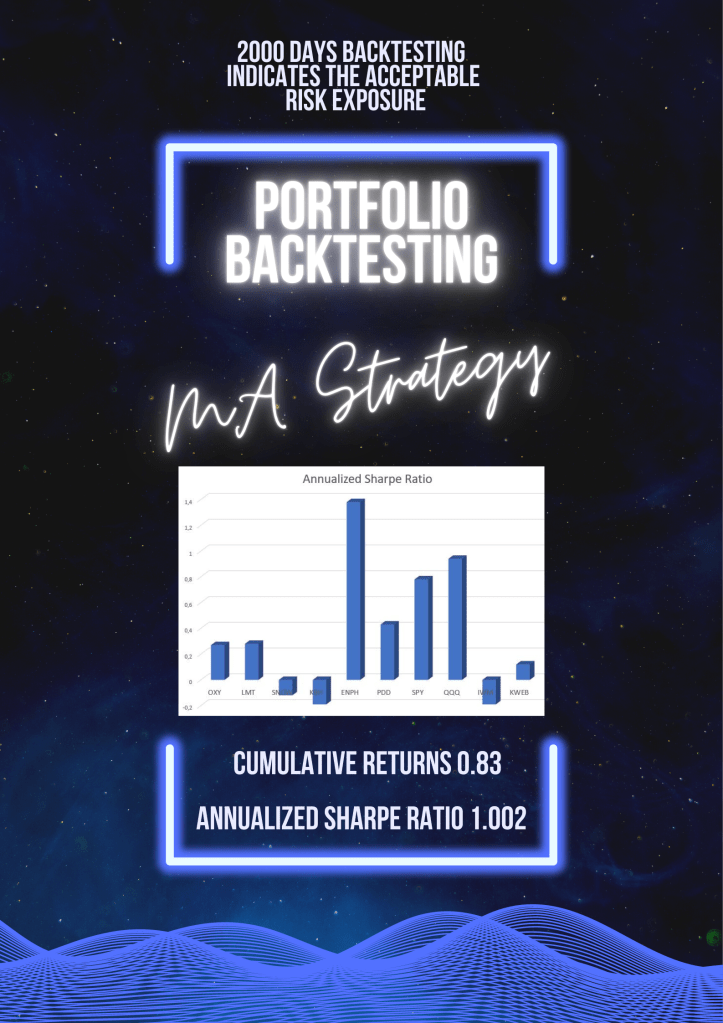

print(“Cumulative returns MA Strategy :”,get_cumulative_return(portfolio_strategy_returns[“Portfolio_rets”]))

print(“Annualized sharpe ratio MA Strategy :”,get_annualized_sharpe_ratio(portfolio_strategy_returns[“Portfolio_rets”]))

print(“\n”)

Cumulative returns MA Strategy : 0.832610455484652 Annualized sharpe ratio MA Strategy : 1.0024619067938556

import matplotlib.pyplot as plt

colors = [‘tab:cyan’,’tab:purple’,’tab:pink’,’tab:orange’,’tab:blue’,’tab:green’,’tab:gray’,’tab:olive’,’tab:brown’,’tab:red’,”k”]

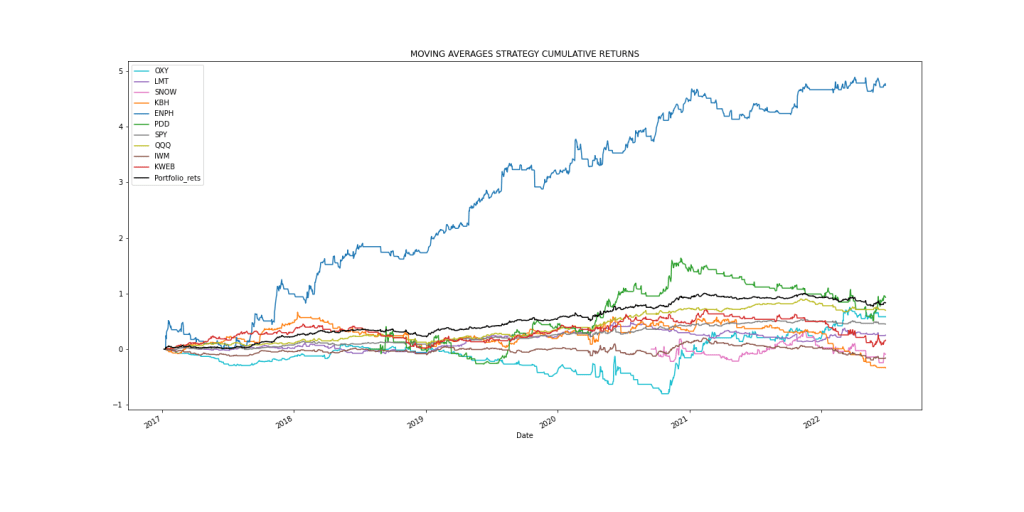

portfolio_strategy_returns.cumsum().plot(figsize=(20,10), title=”MOVING AVERAGES STRATEGY CUMULATIVE RETURNS”, color=colors)

plt.savefig(‘portfolioreturnspup.png’)

The plot shows that the portfolio has almost no variation as compared to the individual stock performance. The Sharpe ratio of 1.0024 indicates the acceptable risk exposure.

Infographic

Leave a comment