Tag: returns

-

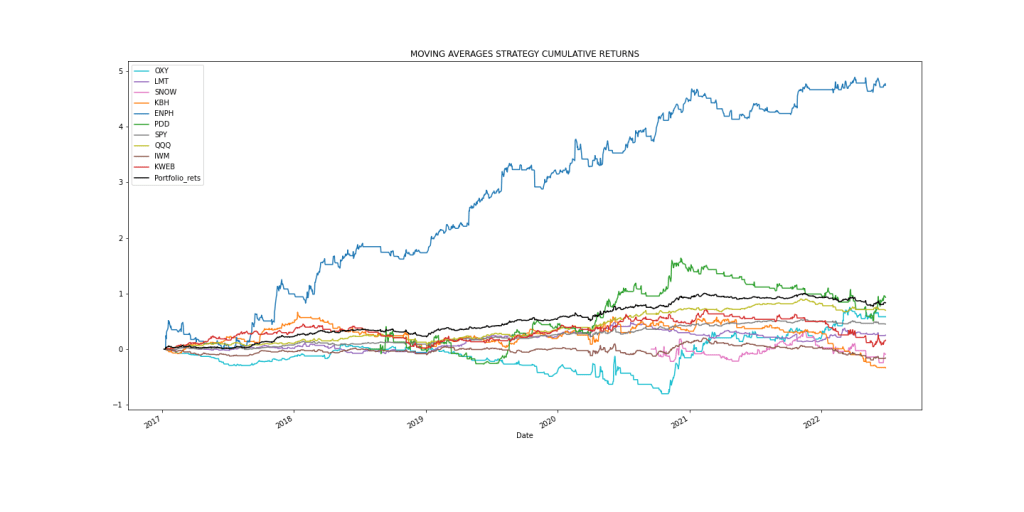

NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

The study presents a machine learning-focused analytical approach to optimize NVIDIA’s stock performance using moving average crossovers and aims at comparing the outcomes with simple RNN mean reversal trading strategies. The steps taken involve preparing the stock data, calculating moving averages and drawdowns, plotting heatmaps of returns and drawdowns, and predicting returns and cumulative returns…

-

Portfolio Optimization of 20 Dividend Growth Stocks

The post discusses implementing a stochastic optimization algorithm to create a balanced portfolio of 20 dividend growth stocks for maximum return within defined risk tolerance. By analyzing daily stock and benchmark data, the algorithm optimizes the portfolio to outperform the benchmark index and achieve desired risk-reward outcomes. The results facilitate spreading investment capital across diverse…

-

Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

Based on the Portfolio Allocation and Optimization Algorithm discussed earlier and the related portfolio management, let’s run the Bear vs. Bull QC test of the portfolio P=[MSFT, AAPL, NDAQ] in terms of the Risk/Return Ratio (RRR). We have got a Sharpe ratio of less than one that is considered unacceptable or bad. The risk the…

-

Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

Investors can optimize their stock portfolio by invoking backtesting within the realm of algorithmic trading. The goal is to optimize the specific portfolio by maximizing returns and the Sharpe ratio.