- Referring to the Monte Carlo series, we will explore future scenarios by simulating Oracle stock returns by random sampling and extrapolating the stock price into the near future.

- TX-based Oracle Corporation (NYSE:ORCL) is making significant strides in generative AI (GenAI) technology, earnings double in Q4 2023. The company’s progress is marked by its lucrative partnerships with Nvidia (NASDAQ:NVDA) and Elon Musk’s xAI.

- In fact, Oracle has secured contracts exceeding $4 billion for capacity on its Generation 2 Cloud to train generative AI models. These models are linked with platforms like ChatGPT and Bard. This development has contributed to a remarkable doubling of Oracle’s earnings for the Q4 2023.

- YF Summary: ORCL boasts a Growth Style Score of A and VGM Score of B, and holds a Zacks Rank #3 (Hold) rating. Its bottom-line is projected to rise 8.2% year-over-year for 2024, while Wall Street anticipates its top line to improve by 7.2%. Looking at cash flow, Oracle is expected to report cash flow growth of 18.6% this year; ORCL has generated cash flow growth of 3.2% over the past three to five years.

Input Stock Data

- Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

and download the stock data

import datetime as dt

from datetime import datetime as dt

from dateutil.relativedelta import relativedelta

import yfinance as yf

end = dt.today()

start = dt.today() - relativedelta(years=1)

data = yf.download('ORCL', start, end)

data.tail()

Monte Carlo Simulation

- Let’s run the Monte Carlo stock simulator

# Distribution parameters

v = 2.91162520

scale = 1.21872294e-02

loc = -8.13209384e-05

# importing the datetime library to generate dates for the future

from datetime import datetime, timedelta

from scipy import stats

# the simulations' starting price

initial_price = data['Close'].iloc[-1]

# number of simulation days

N_steps = 14

# number of scenarios in simulation

N_sims = 1000

# here we sample the distribution for 14x50000 future returns

rets_t= stats.t.rvs(df= v,loc = loc, scale =scale, size = (N_steps, N_sims))

# here we calculate the price at each timestep from the generated log returns

sim = (np.exp(rets_t.cumsum(axis = 1)))

# we save the results in a dataframe and put them on equal footing

results = pd.DataFrame(np.array(sim).reshape(N_sims, N_steps).T)

results = results.divide(results.iloc[0])*initial_price

time = pd.date_range(start = data.index[-1],

end = data.index[-1] + timedelta(days = N_steps - 1))

# lets look at the final price

final_price_t = results.iloc[-1]

plt.figure(figsize=(10,6))

plt.hist(final_price_t[final_price_t < 5*initial_price], density = True, bins = 100)

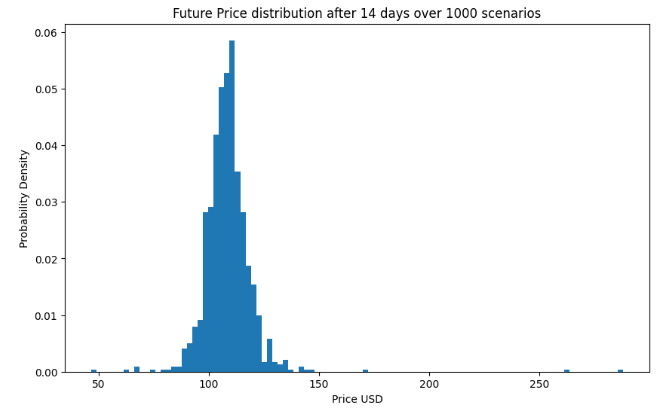

plt.title(f'Future Price distribution after {N_steps} days over {N_sims} scenarios')

plt.xlabel('Price USD')

plt.ylabel('Probability Density')

print (time)

DatetimeIndex(['2023-10-19', '2023-10-20', '2023-10-21', '2023-10-22',

'2023-10-23', '2023-10-24', '2023-10-25', '2023-10-26',

'2023-10-27', '2023-10-28', '2023-10-29', '2023-10-30',

'2023-10-31', '2023-11-01'],

dtype='datetime64[ns]', freq='D')

plt.figure(figsize=(18,15))

SMALL_SIZE = 20

MEDIUM_SIZE = 20

BIGGER_SIZE = 20

plt.rc('font', size=SMALL_SIZE) # controls default text sizes

plt.rc('axes', titlesize=SMALL_SIZE) # fontsize of the axes title

plt.rc('axes', labelsize=MEDIUM_SIZE) # fontsize of the x and y labels

plt.rc('xtick', labelsize=18) # fontsize of the tick labels

plt.rc('ytick', labelsize=SMALL_SIZE) # fontsize of the tick labels

plt.rc('legend', fontsize=SMALL_SIZE) # legend fontsize

plt.rc('figure', titlesize=BIGGER_SIZE) # fontsize of the figure title

plt.xticks(rotation=45, ha='right')

plt.plot(time,results)

plt.xlabel('Date')

plt.ylabel('Price USD')

plt.title('Oracle Price Monte Carlo Simulation')

plt.ylim(top=200)

- According to TradingView, the ORCL beta value of 1.2 suggests that the stock tends to move with more momentum than the S&P 500.

- The above simulation supports the weekly ORCL technical analysis based upon the most popular technical indicators, such as Moving Averages, Oscillators and Pivots.

Summary

- Our Monte Carlo simulation results are consistent with the current Zacks Rank 3-Hold for ORCL.

- Regarding the most recent ORCL trading ideas, these simulations confirm that the stock has a bullish potential. It is looking like a reversal on the weekly and daily chart.

- We believe that ORCL should be on investors’ short lists because of its impressive growth fundamentals, a good Zacks Rank, and strong Growth and VGM Style Scores.

Explore More

- Eric Marsden’s Top 6 Reliability/Risk Engineering Learnings

- Blue-Chip Stock Portfolios for Quant Traders

- Predicting Rolling Volatility of the NVIDIA Stock – GARCH vs XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Cloud-Native Tech Autumn 2022 Fair

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment