Featured Photo by Monstera on Pexels.

- In this post, we will put forward advanced integrated data visualization (AIDV) in the stock trading decisions and stock price prediction. The objective is to implement and visualize most popular stock technical indicators that are commonly used in technical analysis.

- From the point of view of algo trading, this study proves the credibility and advantages of AIDV in Python for the stock trading decisions and stock price prediction.

- Our final goal is to provide the trader with a dynamically changing and interactive UI using the technical analysis libraries available for Python and Plotly’s interactive AIDV tools.

In this project, we will implement the following Technical Indicators in Python:

- RSI, Volume (plain), Bollinger Bands, Aroon, Price Volume Trend, acceleration bands

- Stochastic, Chaikin Money Flow, Parabolic SAR, Rate of Change, Volume weighted average Price, momentum

- Commodity Channel Index, On Balance Volume, Keltner Channels, Triple Exponential Moving Average, Normalized Average True Range , directional movement indicators

- MACD, Money Flow index , Ichimoku, William %R, Volume MINMAX, adaptive moving average.

Conventionally, we will look at the following three main groups of technical indicators:

- Trend indicators — Simple Moving Average(SMA), Exponential Moving Average (EMA), Average Directional Movement Index (ADX), etc.

- Momentum indicators — Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), etc.

- Volatility indicators — e.g. Bollinger Bands.

Input Stock Data

Let’s set the working directory VIZ

import os

os.chdir(‘VIZ’)

os. getcwd()

and import the key libraries

import datetime as dt

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import random

import copy

plt.style.use(‘fivethirtyeight’)

plt.rcParams[‘figure.figsize’] = (20,10)

Let’s download the stock data

def download_stock_data(ticker,timestamp_start,timestamp_end):

url=f”https://query1.finance.yahoo.com/v7/finance/download/{ticker}?period1={timestamp_start}&period2={timestamp_end}&interval\

=1d&events=history&includeAdjustedClose=true”

df = pd.read_csv(url)

return df

datetime_start=dt.datetime(2022, 1, 1, 7, 35, 51)

datetime_end=dt.datetime.today()

timestamp_start=int(datetime_start.timestamp())

timestamp_end=int(datetime_end.timestamp())

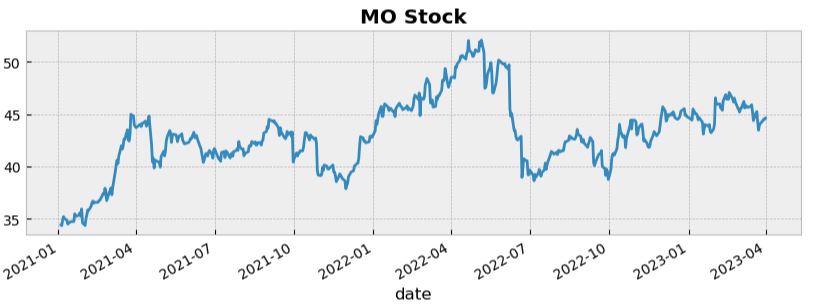

ticklist=[‘XOM’,’O’,’AZN’,’MO’,’COST’,’SBUX’,’AAPL’,’LMT’]

datac = []

for tick in ticklist:

df = download_stock_data(tick,timestamp_start,timestamp_end)

df = df.set_index(‘Date’)

df[‘Label’] = tick

datac.append(df)

print (datac)

[ Open High Low Close Adj Close \

Date

2022-01-03 61.240002 63.599998 61.209999 63.540001 60.648853

2022-01-04 64.129997 66.190002 64.099998 65.930000 62.930103

2022-01-05 66.500000 67.610001 66.480003 66.750000 63.712791

2022-01-06 68.000000 68.480003 67.070000 68.320000 65.211357

2022-01-07 68.519997 69.180000 67.980003 68.879997 65.745872

... ... ... ... ... ...

2023-03-30 109.550003 109.570000 108.519997 109.489998 109.489998

2023-03-31 109.680000 110.169998 109.050003 109.660004 109.660004

2023-04-03 113.389999 116.849998 113.120003 116.129997 116.129997

2023-04-04 116.260002 116.699997 114.169998 115.019997 115.019997

2023-04-05 115.349998 117.000000 114.309998 116.989998 116.989998

Volume Label

Date

2022-01-03 24282400 XOM

2022-01-04 38584000 XOM

2022-01-05 34033300 XOM

2022-01-06 30668500 XOM

2022-01-07 23985400 XOM

... ... ...

2023-03-30 11578200 XOM

2023-03-31 14416800 XOM

2023-04-03 28087700 XOM

2023-04-04 16365500 XOM

2023-04-05 16475200 XOM

[316 rows x 7 columns], Open High Low Close Adj Close Volume \

Date

2022-01-03 71.730003 71.809998 70.099998 71.199997 67.311935 3110500

2022-01-04 71.150002 72.480003 71.120003 72.250000 68.304596 3410700

2022-01-05 72.120003 72.480003 70.889999 71.080002 67.198494 3237600

2022-01-06 71.360001 71.870003 70.889999 71.410004 67.510460 2869800

2022-01-07 71.129997 71.540001 70.709999 71.410004 67.510460 3108900

... ... ... ... ... ... ...

2023-03-30 62.430000 62.860001 62.349998 62.610001 62.355000 3008000

2023-03-31 62.520000 63.360001 62.470001 63.320000 63.320000 4141500

2023-04-03 62.950001 63.400002 62.389999 62.869999 62.869999 5758400

2023-04-04 62.830002 62.990002 62.389999 62.840000 62.840000 2832400

2023-04-05 62.959999 63.110001 62.470001 62.709999 62.709999 4000600

Label

Date

2022-01-03 O

2022-01-04 O

2022-01-05 O

2022-01-06 O

2022-01-07 O

... ...

2023-03-30 O

2023-03-31 O

2023-04-03 O

2023-04-04 O

2023-04-05 O

[316 rows x 7 columns], Open High Low Close Adj Close Volume \

Date

2022-01-03 58.270000 58.369999 57.750000 58.310001 56.144096 3321000

2022-01-04 57.160000 57.700001 57.070000 57.270000 55.142727 4646600

2022-01-05 57.240002 57.730000 56.849998 56.880001 54.767216 4804400

2022-01-06 56.810001 57.040001 56.110001 56.669998 54.565006 6196400

2022-01-07 56.650002 57.549999 56.529999 57.480000 55.344921 4594800

... ... ... ... ... ... ...

2023-03-30 69.050003 69.220001 68.629997 69.199997 69.199997 4648100

2023-03-31 69.879997 69.930000 69.239998 69.410004 69.410004 3500300

2023-04-03 69.529999 69.949997 69.360001 69.910004 69.910004 4749200

2023-04-04 69.980003 70.570000 69.809998 70.250000 70.250000 4383400

2023-04-05 72.000000 72.480003 71.800003 72.050003 72.050003 5873200

Label

Date

2022-01-03 AZN

2022-01-04 AZN

2022-01-05 AZN

2022-01-06 AZN

2022-01-07 AZN

... ...

2023-03-30 AZN

2023-03-31 AZN

2023-04-03 AZN

2023-04-04 AZN

2023-04-05 AZN

[316 rows x 7 columns], Open High Low Close Adj Close Volume \

Date

2022-01-03 47.369999 48.000000 47.180000 47.970001 43.408066 10308100

2022-01-04 48.000000 49.340000 47.980000 49.029999 44.367256 11647900

2022-01-05 48.549999 49.270000 48.330002 48.639999 44.014351 11506500

2022-01-06 49.180000 49.720001 48.869999 49.209999 44.530140 10134100

2022-01-07 49.200001 50.000000 49.099998 49.770000 45.036888 8098600

... ... ... ... ... ... ...

2023-03-30 44.639999 44.830002 44.349998 44.500000 44.500000 6862400

2023-03-31 44.630001 44.720001 44.430000 44.619999 44.619999 7710000

2023-04-03 44.720001 45.330002 44.599998 44.980000 44.980000 8385800

2023-04-04 44.880001 44.910000 44.240002 44.450001 44.450001 7379600

2023-04-05 44.459999 44.700001 44.189999 44.430000 44.430000 7865000

Label

Date

2022-01-03 MO

2022-01-04 MO

2022-01-05 MO

2022-01-06 MO

2022-01-07 MO

... ...

2023-03-30 MO

2023-03-31 MO

2023-04-03 MO

2023-04-04 MO

2023-04-05 MO

[316 rows x 7 columns], Open High Low Close Adj Close \

Date

2022-01-03 565.030029 567.469971 555.510010 566.710022 561.965271

2022-01-04 564.229980 568.719971 561.789978 564.229980 559.506042

2022-01-05 563.690002 565.049988 549.770020 549.919983 545.315857

2022-01-06 546.200012 553.520020 543.549988 549.799988 545.196899

2022-01-07 547.549988 548.369995 534.239990 536.179993 531.690857

... ... ... ... ... ...

2023-03-30 493.000000 495.739990 491.000000 491.480011 491.480011

2023-03-31 495.000000 498.359985 493.940002 496.869995 496.869995

2023-04-03 496.500000 499.200012 495.000000 497.029999 497.029999

2023-04-04 496.500000 502.579987 495.500000 497.730011 497.730011

2023-04-05 499.000000 504.130005 495.160004 497.130005 497.130005

Volume Label

Date

2022-01-03 2714100 COST

2022-01-04 2097500 COST

2022-01-05 2887500 COST

2022-01-06 2503100 COST

2022-01-07 2323900 COST

... ... ...

2023-03-30 1545500 COST

2023-03-31 2081300 COST

2023-04-03 1804700 COST

2023-04-04 1913300 COST

2023-04-05 1930600 COST

[316 rows x 7 columns], Open High Low Close Adj Close \

Date

2022-01-03 116.470001 117.800003 114.779999 116.680000 113.403084

2022-01-04 116.900002 117.050003 114.169998 114.239998 111.031593

2022-01-05 114.400002 114.959999 110.400002 110.440002 107.338318

2022-01-06 110.000000 111.879997 109.989998 111.139999 108.018661

2022-01-07 108.220001 109.709999 107.480003 107.570000 104.548920

... ... ... ... ... ...

2023-03-30 101.440002 101.699997 100.650002 101.320000 101.320000

2023-03-31 101.839996 104.279999 101.839996 104.129997 104.129997

2023-04-03 104.059998 104.940002 103.669998 104.849998 104.849998

2023-04-04 104.849998 105.010002 103.349998 104.000000 104.000000

2023-04-05 103.980003 105.699997 103.930000 104.900002 104.900002

Volume Label

Date

2022-01-03 5475700 SBUX

2022-01-04 8367600 SBUX

2022-01-05 8662300 SBUX

2022-01-06 6099900 SBUX

2022-01-07 11266400 SBUX

... ... ...

2023-03-30 4082600 SBUX

2023-03-31 6899300 SBUX

2023-04-03 3855400 SBUX

2023-04-04 3854400 SBUX

2023-04-05 5169900 SBUX

[316 rows x 7 columns], Open High Low Close Adj Close \

Date

2022-01-03 177.830002 182.880005 177.710007 182.009995 180.683868

2022-01-04 182.630005 182.940002 179.119995 179.699997 178.390701

2022-01-05 179.610001 180.169998 174.639999 174.919998 173.645538

2022-01-06 172.699997 175.300003 171.639999 172.000000 170.746826

2022-01-07 172.889999 174.139999 171.029999 172.169998 170.915588

... ... ... ... ... ...

2023-03-30 161.529999 162.470001 161.270004 162.360001 162.360001

2023-03-31 162.440002 165.000000 161.910004 164.899994 164.899994

2023-04-03 164.270004 166.289993 164.220001 166.169998 166.169998

2023-04-04 166.600006 166.839996 165.110001 165.630005 165.630005

2023-04-05 164.740005 165.050003 161.800003 163.759995 163.759995

Volume Label

Date

2022-01-03 104487900 AAPL

2022-01-04 99310400 AAPL

2022-01-05 94537600 AAPL

2022-01-06 96904000 AAPL

2022-01-07 86709100 AAPL

... ... ...

2023-03-30 49501700 AAPL

2023-03-31 68694700 AAPL

2023-04-03 56976200 AAPL

2023-04-04 46278300 AAPL

2023-04-05 51457200 AAPL

[316 rows x 7 columns], Open High Low Close Adj Close \

Date

2022-01-03 354.679993 356.589996 353.029999 354.359985 343.132660

2022-01-04 355.529999 363.540009 355.209991 361.989990 350.520935

2022-01-05 363.000000 364.000000 357.869995 358.140015 346.792938

2022-01-06 360.000000 361.239990 357.549988 358.000000 346.657349

2022-01-07 359.079987 362.989990 358.149994 360.140015 348.729553

... ... ... ... ... ...

2023-03-30 474.540009 475.799988 471.730011 473.179993 473.179993

2023-03-31 474.190002 475.350006 471.029999 472.730011 472.730011

2023-04-03 473.000000 487.899994 472.750000 486.619995 486.619995

2023-04-04 485.589996 490.630005 484.750000 488.540009 488.540009

2023-04-05 488.000000 493.829987 487.029999 489.989990 489.989990

Volume Label

Date

2022-01-03 1205700 LMT

2022-01-04 1361100 LMT

2022-01-05 1682200 LMT

2022-01-06 1368800 LMT

2022-01-07 1634600 LMT

... ... ...

2023-03-30 950300 LMT

2023-03-31 1409600 LMT

2023-04-03 1656700 LMT

2023-04-04 1081100 LMT

2023-04-05 1305500 LMT

[316 rows x 7 columns]]

TechIndicator = copy.deepcopy(data)

Relative Strength Index (RSI)

- The relative strength index (RSI) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of a security’s recent price changes to evaluate overvalued or undervalued conditions in the price of that security.

- The RSI is displayed as an oscillator (a line graph) on a scale of zero to 100.

- An asset is usually considered overbought when the RSI is above 70 and oversold when it is below 30.

def rsi(values):

up = values[values>0].mean()

down = -1*values[values<0].mean()

return 100 * up / (up + down)

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘Momentum_1D’] = (TechIndicator[stock][‘Close’]-TechIndicator[stock][‘Close’].shift(1)).fillna(0)

TechIndicator[stock][‘RSI_14D’] = TechIndicator[stock][‘Momentum_1D’].rolling(center=False, window=14).apply(rsi).fillna(0)

TechIndicator[0].tail(5)

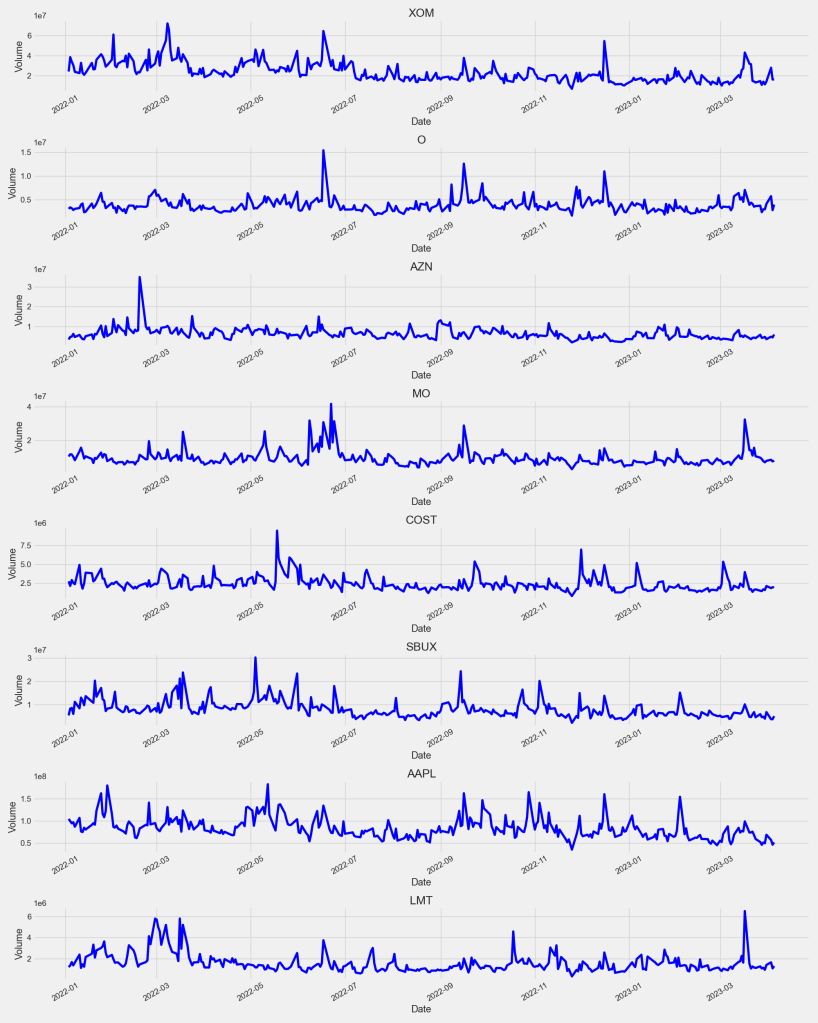

Volume

- Trading volume is a measure of how much a given financial asset has traded in a period of time. For stocks, volume is measured in the number of shares traded. For futures and options, volume is based on how many contracts have changed hands. Traders look to volume to determine liquidity and combine changes in volume with technical indicators to make trading decisions.

- Volume measures the number of shares traded in a stock or contracts traded in futures or options.

- Volume can indicate market strength, as rising markets on increasing volume are typically viewed as strong and healthy.

- When prices fall on increasing volume, the trend is gathering strength to the downside.

- When prices reach new highs (or no lows) on decreasing volume, watch out—a reversal might be taking shape.

- On-balance volume (OBV) and the Klinger oscillator are examples of charting tools that are based on volume.

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘Volume_plain’] = TechIndicator[stock][‘Volume’].fillna(0)

TechIndicator[0].tail()

Bollinger Bands (BB)

- Bollinger Bands® is a technical analysis tool to generate oversold or overbought signals and was developed by John Bollinger.

- Three lines compose Bollinger Bands: A simple moving average, or the middle band, and an upper and lower band.

- The upper and lower bands are typically 2 standard deviations +/- from a 20-day simple moving average and can be modified.

- When the price continually touches the upper Bollinger Band, it can indicate an overbought signal.

- If the price continually touches the lower band it can indicate an oversold signal.

def bbands(price, length=30, numsd=2):

“”” returns average, upper band, and lower band”””

#ave = pd.stats.moments.rolling_mean(price,length)

ave = price.rolling(window = length, center = False).mean()

#sd = pd.stats.moments.rolling_std(price,length)

sd = price.rolling(window = length, center = False).std()

upband = ave + (sdnumsd) dnband = ave – (sdnumsd)

return np.round(ave,3), np.round(upband,3), np.round(dnband,3)

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘BB_Middle_Band’], TechIndicator[stock][‘BB_Upper_Band’], TechIndicator[stock][‘BB_Lower_Band’] = bbands(TechIndicator[stock][‘Close’], length=20, numsd=1)

TechIndicator[stock][‘BB_Middle_Band’] = TechIndicator[stock][‘BB_Middle_Band’].fillna(0)

TechIndicator[stock][‘BB_Upper_Band’] = TechIndicator[stock][‘BB_Upper_Band’].fillna(0)

TechIndicator[stock][‘BB_Lower_Band’] = TechIndicator[stock][‘BB_Lower_Band’].fillna(0)

TechIndicator[0].tail()

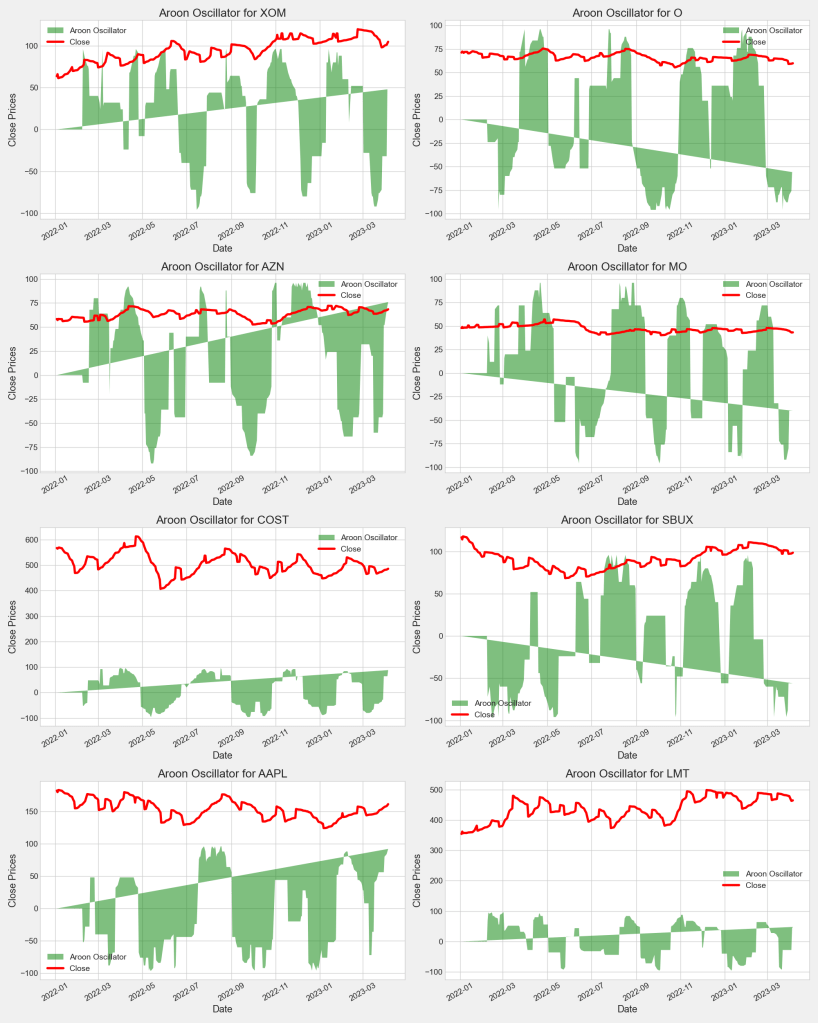

Aroon Oscillator (AO)

The Aroon indicator is a technical indicator that is used to identify trend changes in the price of an asset, as well as the strength of that trend.

- The Aroon indicator is composed of two lines. An up line which measures the number of periods since a High, and a down line which measures the number of periods since a Low.

- The indicator is typically applied to 25 periods of data, so the indicator is showing how many periods it has been since a 25-period high or low.

- When the Aroon Up is above the Aroon Down, it indicates bullish price behavior.

- When the Aroon Down is above the Aroon Up, it signals bearish price behavior.

- Crossovers of the two lines can signal trend changes. For example, when Aroon Up crosses above Aroon Down it may mean a new uptrend is starting.

- The indicator moves between zero and 100.

def aroon(df, tf=25):

aroonup = []

aroondown = []

x = tf

while x< len(df.index):

aroon_up = ((df[‘High’][x-tf:x].tolist().index(max(df[‘High’][x-tf:x])))/float(tf))100 aroon_down = ((df[‘Low’][x-tf:x].tolist().index(min(df[‘Low’][x-tf:x])))/float(tf))100

aroonup.append(aroon_up)

aroondown.append(aroon_down)

x+=1

return aroonup, aroondown

for stock in range(len(TechIndicator)):

listofzeros = [0] * 25

up, down = aroon(TechIndicator[stock])

aroon_list = [x – y for x, y in zip(up,down)]

if len(aroon_list)==0:

aroon_list = [0] * TechIndicator[stock].shape[0]

TechIndicator[stock][‘Aroon_Oscillator’] = aroon_list

else:

TechIndicator[stock][‘Aroon_Oscillator’] = listofzeros+aroon_list

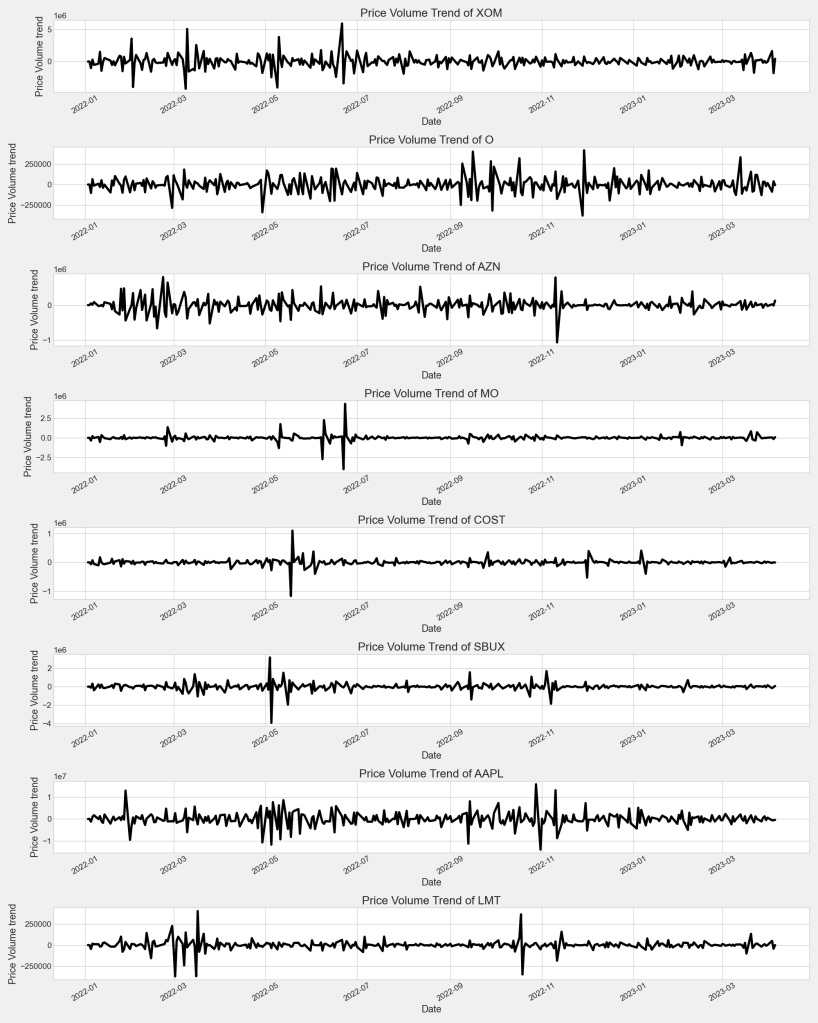

Price Volume Trend (PVT)

The PVT indicator helps determine a security’s price direction and strength of price change. The indicator consists of a cumulative volume line that adds or subtracts a multiple of the percentage change in a share prices’ trend and current volume, depending upon the security’s upward or downward movements.

for stock in range(len(TechIndicator)):

TechIndicator[stock][“PVT”] = (TechIndicator[stock][‘Momentum_1D’]/ TechIndicator[stock][‘Close’].shift(1))*TechIndicator[stock][‘Volume’]

TechIndicator[stock][“PVT”] = TechIndicator[stock][“PVT”]-TechIndicator[stock][“PVT”].shift(1)

TechIndicator[stock][“PVT”] = TechIndicator[stock][“PVT”].fillna(0)

TechIndicator[0].tail()

Acceleration Bands (AB)

The Acceleration Bands measure volatility over a user-defined number of bars (default is often the past 20 bars). They are plotted using a simple moving average as the midpoint, with the upper and lower bands being of equal distance from the midpoint, similar to Bollinger Bands.

def abands(df):

#df[‘AB_Middle_Band’] = pd.rolling_mean(df[‘Close’], 20)

df[‘AB_Middle_Band’] = df[‘Close’].rolling(window = 20, center=False).mean()

# High * ( 1 + 4 * (High – Low) / (High + Low))

df[‘aupband’] = df[‘High’] * (1 + 4 * (df[‘High’]-df[‘Low’])/(df[‘High’]+df[‘Low’]))

df[‘AB_Upper_Band’] = df[‘aupband’].rolling(window=20, center=False).mean()

# Low *(1 – 4 * (High – Low)/ (High + Low))

df[‘adownband’] = df[‘Low’] * (1 – 4 * (df[‘High’]-df[‘Low’])/(df[‘High’]+df[‘Low’]))

df[‘AB_Lower_Band’] = df[‘adownband’].rolling(window=20, center=False).mean()

for stock in range(len(TechIndicator)):

abands(TechIndicator[stock])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

columns2Drop = [‘Momentum_1D’, ‘aupband’, ‘adownband’]

for stock in range(len(TechIndicator)):

TechIndicator[stock] = TechIndicator[stock].drop(labels = columns2Drop, axis=1)

TechIndicator[0].head()

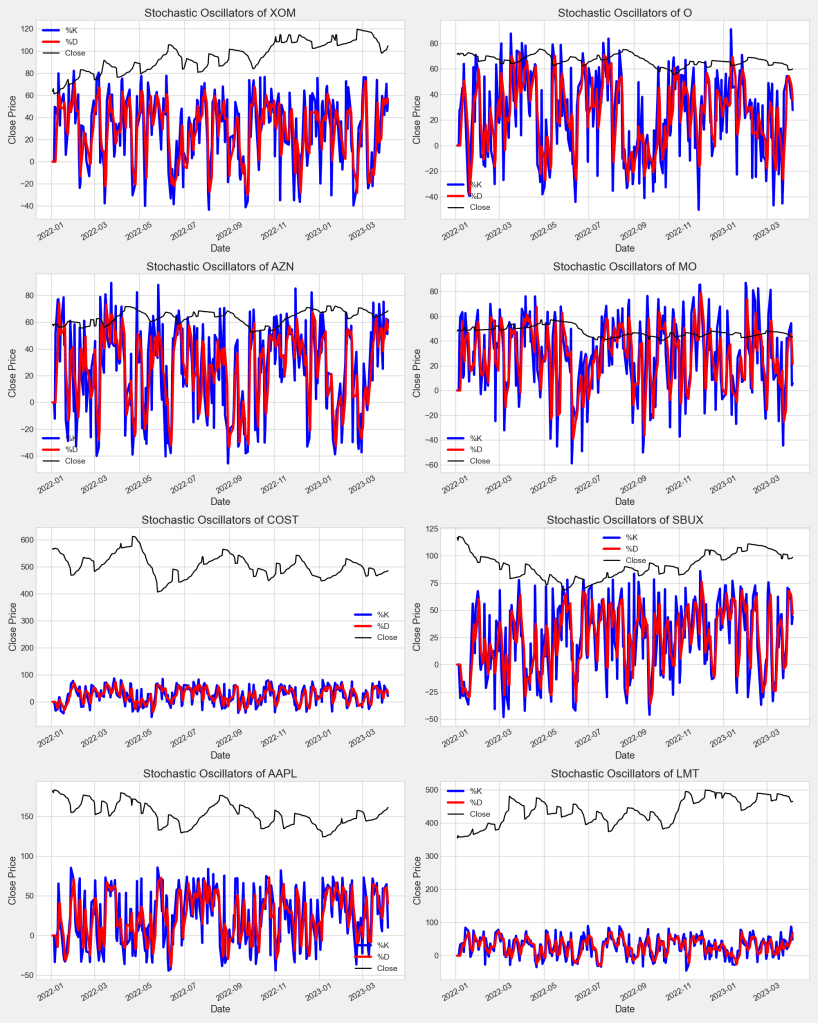

Stochastic Oscillator (%K and %D)

A stochastic oscillator is a momentum indicator comparing a particular closing price of a security to a range of its prices over a certain period of time. The sensitivity of the oscillator to market movements is reducible by adjusting that time period or by taking a moving average of the result. It is used to generate overbought and oversold trading signals, utilizing a 0–100 bounded range of values.

- Stochastics are a favored technical indicator because they are easy to understand and have a relatively high degree of accuracy.

- It falls into the class of technical indicators known as oscillators.

- The indicator provides buy and sell signals for traders to enter or exit positions based on momentum.

- Stochastics are used to show when a stock has moved into an overbought or oversold position.

- it is beneficial to use stochastics in conjunction with other tools like the relative strength index (RSI) to confirm a signal.

def STOK(df, n):

df[‘STOK’] = ((df[‘Close’] – df[‘Low’].rolling(window=n, center=False).mean()) / (df[‘High’].rolling(window=n, center=False).max() – df[‘Low’].rolling(window=n, center=False).min())) * 100

df[‘STOD’] = df[‘STOK’].rolling(window = 3, center=False).mean()

for stock in range(len(TechIndicator)):

STOK(TechIndicator[stock], 4)

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

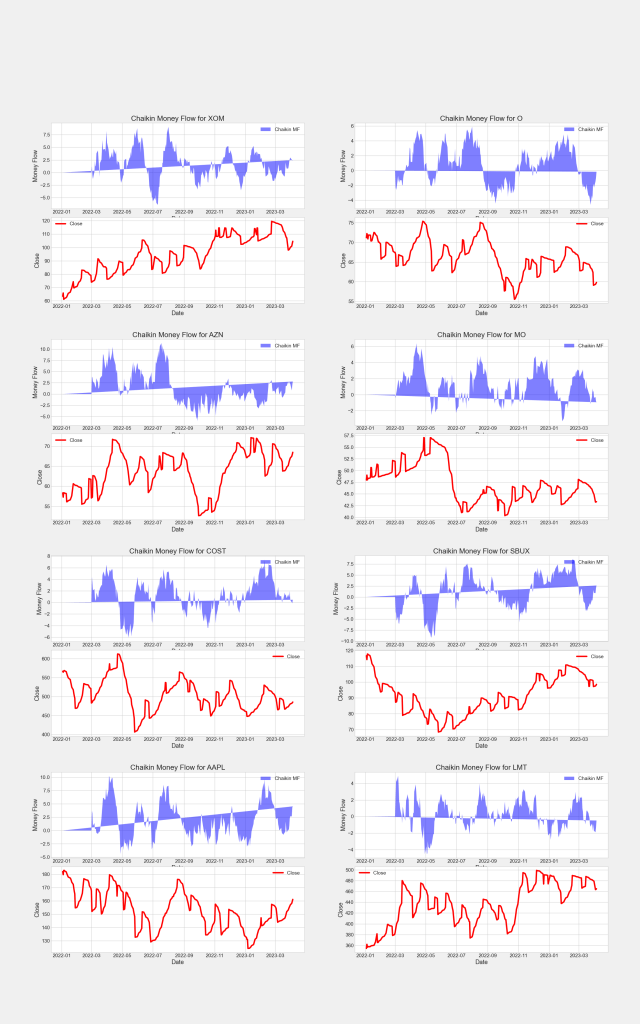

Chaikin Money Flow (CMFlow)

- The Chaikin Indicator applies MACD to the accumulation-distribution line rather than to the closing price.

- It is an oscillator technical indicator for spotting trends and reversals.

- A cross above the accumulation-distribution line indicates that market players are accumulating shares, securities, or contracts, which is typically bullish.

To calculate the Chaikin oscillator, subtract a 10-day exponential moving average (EMA) of the accumulation-distribution line from a 3-day EMA of the accumulation-distribution line. This measures momentum predicted by oscillations around the accumulation-distribution line.

def CMFlow(df, tf):

CHMF = []

MFMs = []

MFVs = []

x = tf

while x < len(df.index):

PeriodVolume = 0

volRange = df['Volume'][x-tf:x]

for eachVol in volRange:

PeriodVolume += eachVol

MFM = ((df['Close'][x] - df['Low'][x]) - (df['High'][x] - df['Close'][x])) / (df['High'][x] - df['Low'][x])

MFV = MFM*PeriodVolume

MFMs.append(MFM)

MFVs.append(MFV)

x+=1

y = tf

while y < len(MFVs):

PeriodVolume = 0

volRange = df['Volume'][x-tf:x]

for eachVol in volRange:

PeriodVolume += eachVol

consider = MFVs[y-tf:y]

tfsMFV = 0

for eachMFV in consider:

tfsMFV += eachMFV

tfsCMF = tfsMFV/PeriodVolume

CHMF.append(tfsCMF)

y+=1

return CHMF

for stock in range(len(TechIndicator)):

listofzeros = [0] * 40

CHMF = CMFlow(TechIndicator[stock], 20)

if len(CHMF)==0:

CHMF = [0] * TechIndicator[stock].shape[0]

TechIndicator[stock][‘Chaikin_MF’] = CHMF

else:

TechIndicator[stock][‘Chaikin_MF’] = listofzeros+CHMF

TechIndicator[0].tail()

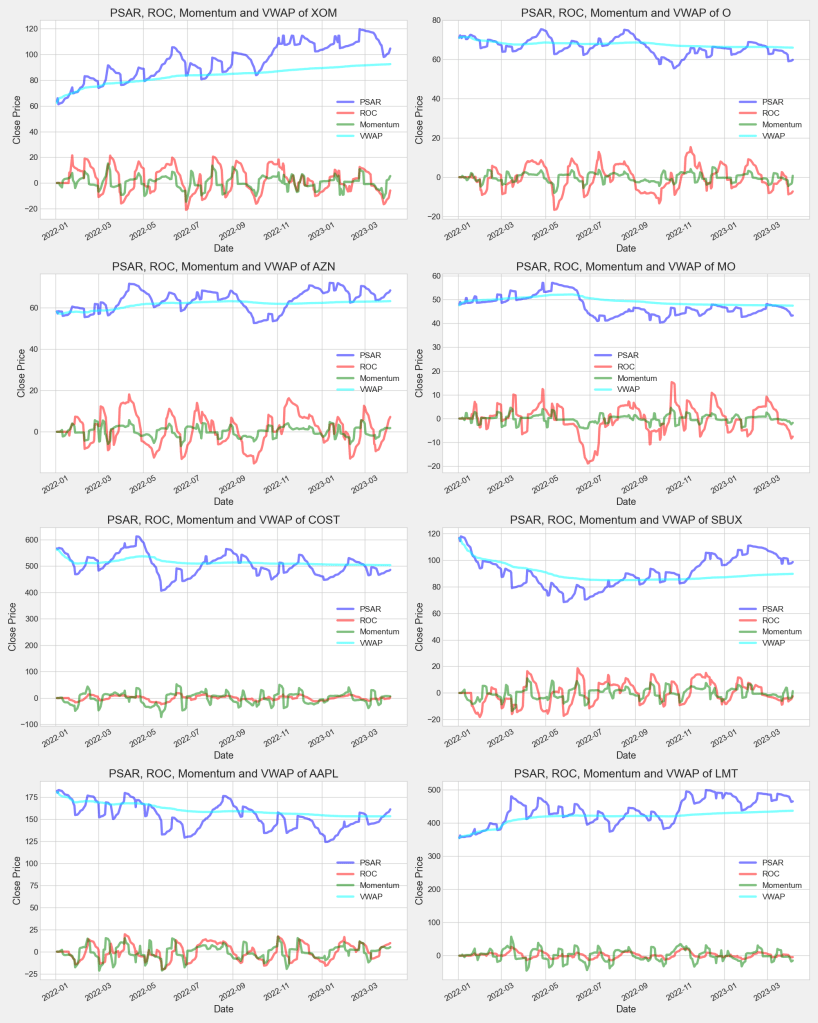

Parabolic SAR (PSAR)

- The parabolic SAR indicator appears on a chart as a series of dots, either above or below an asset’s price, depending on the direction the price is moving. A dot is placed below the price when it is trending upward, and above the price when it is trending downward.

- A reversal occurs when these dots flip, but a reversal signal in the SAR does not necessarily mean a reversal in the price. A PSAR reversal only means that the price and indicator have crossed.

def psar(df, iaf = 0.02, maxaf = 0.2):

length = len(df)

dates = (df.index)

high = (df[‘High’])

low = (df[‘Low’])

close = (df[‘Close’])

psar = df[‘Close’][0:len(df[‘Close’])]

psarbull = [None] * length

psarbear = [None] * length

bull = True

af = iaf

ep = df[‘Low’][0]

hp = df[‘High’][0]

lp = df[‘Low’][0]

for i in range(2,length):

if bull:

psar[i] = psar[i – 1] + af * (hp – psar[i – 1])

else:

psar[i] = psar[i – 1] + af * (lp – psar[i – 1])

reverse = False

if bull:

if df[‘Low’][i] < psar[i]: bull = False reverse = True psar[i] = hp lp = df[‘Low’][i] af = iaf else: if df[‘High’][i] > psar[i]:

bull = True

reverse = True

psar[i] = lp

hp = df[‘High’][i]

af = iaf

if not reverse:

if bull:

if df[‘High’][i] > hp:

hp = df[‘High’][i]

af = min(af + iaf, maxaf)

if df[‘Low’][i – 1] < psar[i]: psar[i] = df[‘Low’][i – 1] if df[‘Low’][i – 2] < psar[i]: psar[i] = df[‘Low’][i – 2] else: if df[‘Low’][i] < lp: lp = df[‘Low’][i] af = min(af + iaf, maxaf) if df[‘High’][i – 1] > psar[i]:

psar[i] = df[‘High’][i – 1]

if df[‘High’][i – 2] > psar[i]:

psar[i] = df[‘High’][i – 2]

if bull:

psarbull[i] = psar[i]

else:

psarbear[i] = psar[i]

df[‘psar’] = psar

for stock in range(len(TechIndicator)):

psar(TechIndicator[stock])

TechIndicator[0].tail()

Price Rate of Change (ROC)

The Price Rate of Change (ROC) is a momentum-based technical indicator that measures the percentage change in price between the current price and the price a certain number of periods ago. The ROC indicator is plotted against zero, with the indicator moving upwards into positive territory if price changes are to the upside, and moving into negative territory if price changes are to the downside.

- The Price Rate of Change (ROC) oscillator is an unbounded momentum indicator used in technical analysis set against a zero-level midpoint.

- A rising ROC above zero typically confirms an uptrend while a falling ROC below zero indicates a downtrend.

- When the price is consolidating, the ROC will hover near zero. In this case, it is important traders watch the overall price trend since the ROC will provide little insight except for confirming the consolidation.

# ROC = [(Close – Close n periods ago) / (Close n periods ago)] * 100

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘ROC’] = ((TechIndicator[stock][‘Close’] – TechIndicator[stock][‘Close’].shift(12))/(TechIndicator[stock][‘Close’].shift(12)))*100

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

Volume Weighted Average Price (VWAP)

- The VWAP is a technical analysis indicator used on intraday charts that resets at the start of every new trading session.

- It’s a trading benchmark that represents the average price a security has traded at throughout the day, based on both volume and price.

- VWAP appears as a single line on intraday charts.

- It looks similar to a moving average line, but smoother.

- VWAP represents a view of price action throughout a single day’s trading session.

- Retail and professional traders may use VWAP to help them determine intraday price trends.

- VWAP typically is most useful to short-term traders.

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘VWAP’] = np.cumsum(TechIndicator[stock][‘Volume’] * (TechIndicator[stock][‘High’] + TechIndicator[stock][‘Low’])/2) / np.cumsum(TechIndicator[stock][‘Volume’])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

Momentum

Momentum measures the rate of the rise or fall in stock prices. For trending analysis, momentum is a useful indicator of strength or weakness in the issue’s price. History has shown that momentum is far more useful during rising markets than falling markets because markets rise more often than they fall.

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘Momentum’] = TechIndicator[stock][‘Close’] – TechIndicator[stock][‘Close’].shift(4)

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

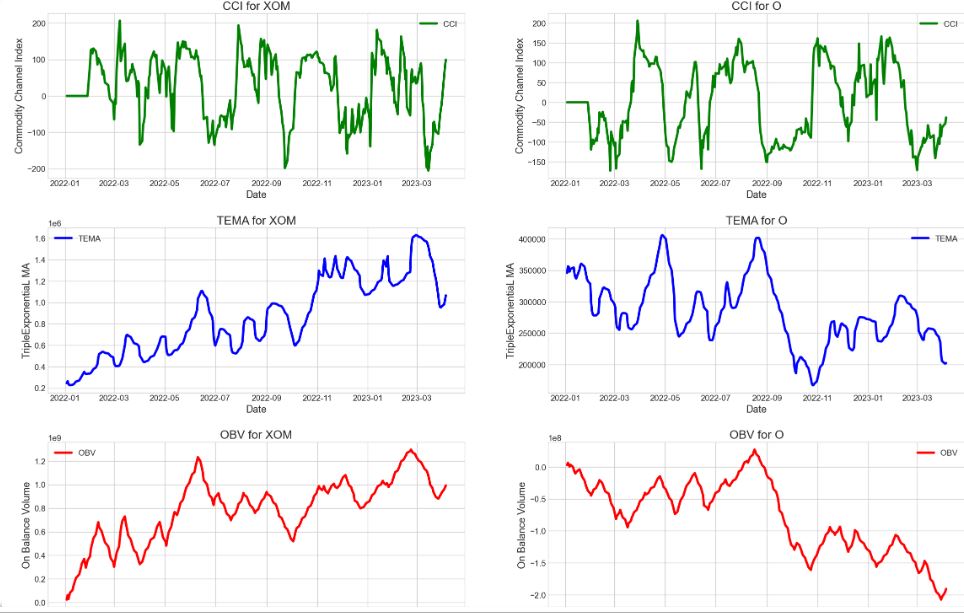

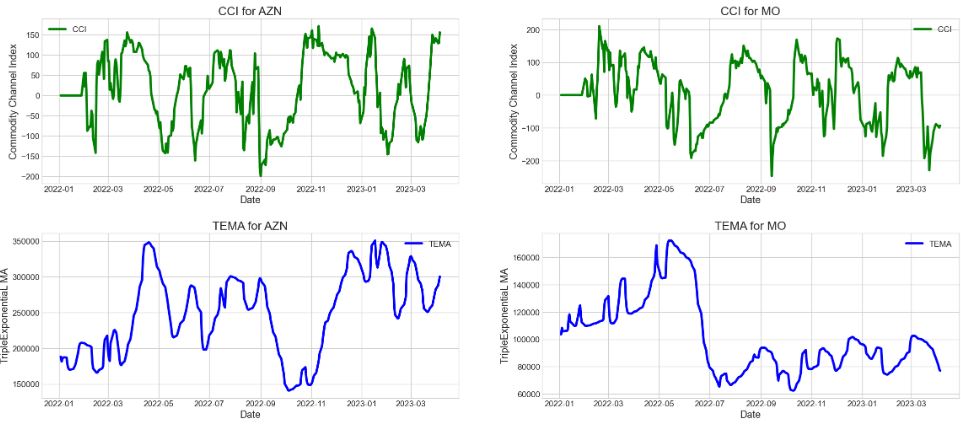

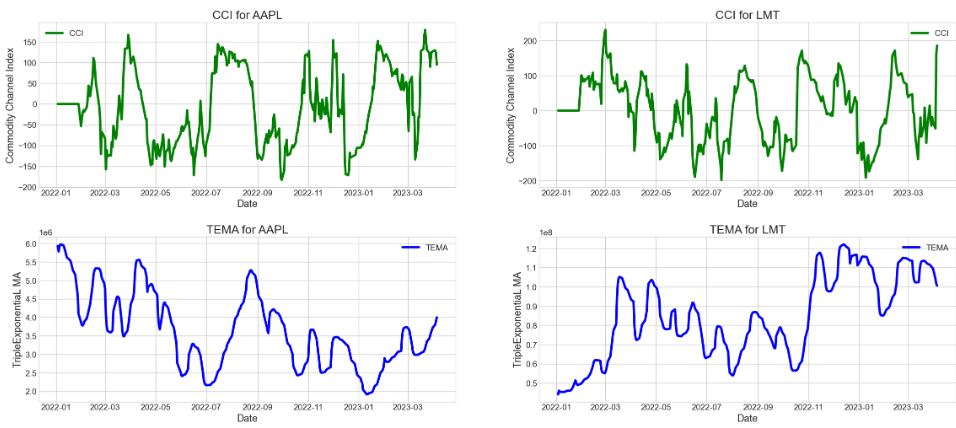

Commodity Channel Index (CCI)

- The Commodity Channel Index (CCI) is a technical indicator that measures the difference between the current price and the historical average price.

- When the CCI is above zero, it indicates the price is above the historic average. Conversely, when the CCI is below zero, the price is below the historic average.

- The CCI is an unbounded oscillator, meaning it can go higher or lower indefinitely. For this reason, overbought and oversold levels are typically determined for each individual asset by looking at historical extreme CCI levels where the price reversed from.

def CCI(df, n, constant):

TP = (df[‘High’] + df[‘Low’] + df[‘Close’]) / 3

CCI = pd.Series((TP – TP.rolling(window=n, center=False).mean()) / (constant * TP.rolling(window=n, center=False).std())) #, name = ‘CCI_’ + str(n))

return CCI

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘CCI’] = CCI(TechIndicator[stock], 20, 0.015)

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[0].tail()

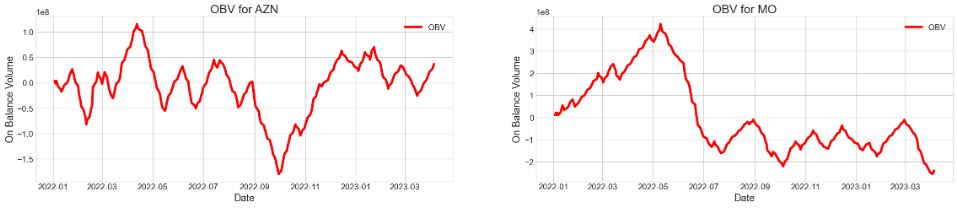

On Balance Volume (OBV)

On-balance volume (OBV) is a technical trading momentum indicator that uses volume flow to predict changes in stock price.

- OBV shows crowd sentiment that can predict a bullish or bearish outcome.

- Comparing relative action between price bars and OBV generates more actionable signals than the green or red volume histograms commonly found at the bottom of price charts.

for stock in range(len(TechIndicator)):

new = (TechIndicator[stock][‘Volume’] * (~TechIndicator[stock][‘Close’].diff().le(0) * 2 -1)).cumsum()

TechIndicator[stock][‘OBV’] = new

TechIndicator[5].tail()

Keltner Channels (KCH)

- Keltner Channels are volatility-based bands that are placed on either side of an asset’s price and can aid in determining the direction of a trend.

- The exponential moving average (EMA) of a Keltner Channel is typically 20 periods, although this can be adjusted if desired.

- The upper and lower bands are typically set two times the average true range (ATR) above and below the EMA, although the multiplier can also be adjusted based on personal preference.

- Price reaching the upper Keltner Channel band is bullish, while reaching the lower band is bearish.

- The angle of the Keltner Channel also aids in identifying the trend direction. The price may also oscillate between the upper and lower Keltner Channel bands, which can be interpreted as resistance and support levels.

def KELCH(df, n):

KelChM = pd.Series(((df[‘High’] + df[‘Low’] + df[‘Close’]) / 3).rolling(window =n, center=False).mean(), name = ‘KelChM_’ + str(n))

KelChU = pd.Series(((4 * df[‘High’] – 2 * df[‘Low’] + df[‘Close’]) / 3).rolling(window =n, center=False).mean(), name = ‘KelChU_’ + str(n))

KelChD = pd.Series(((-2 * df[‘High’] + 4 * df[‘Low’] + df[‘Close’]) / 3).rolling(window =n, center=False).mean(), name = ‘KelChD_’ + str(n))

return KelChM, KelChD, KelChU

for stock in range(len(TechIndicator)):

KelchM, KelchD, KelchU = KELCH(TechIndicator[stock], 14)

TechIndicator[stock][‘Kelch_Upper’] = KelchU

TechIndicator[stock][‘Kelch_Middle’] = KelchM

TechIndicator[stock][‘Kelch_Down’] = KelchD

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[5].tail()

Triple Exponential Moving Average (TEMA)

- The triple exponential moving average (TEMA) uses multiple EMA calculations and subtracts out the lag to create a trend following indicator that reacts quickly to price changes.

- The TEMA indicator can help identify trend direction, signal potential short-term trend changes or pullbacks, and provide support or resistance.

- When the price is above the TEMA it helps confirm an uptrend; when the price is below the TEMA it helps confirm a downtrend.

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘EMA’] = TechIndicator[stock][‘Close’].ewm(span=3,min_periods=0,adjust=True,ignore_na=False).mean()

TechIndicator[stock] = TechIndicator[stock].fillna(0)

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘TEMA’] = (3 * TechIndicator[stock][‘EMA’] – 3 * TechIndicator[stock][‘EMA’] * TechIndicator[stock][‘EMA’]) + (TechIndicator[stock][‘EMA’]TechIndicator[stock][‘EMA’]TechIndicator[stock][‘EMA’])

TechIndicator[5].tail()

Normalized Average True Range (NATR)

- The average true range (ATR) is a market volatility indicator used in technical analysis.

- It is typically derived from the 14-day simple moving average of a series of true range indicators.

- The ATR was initially developed for use in commodities markets but has since been applied to all types of securities.

- ATR shows investors the average range prices swing for an investment over a specified period.

- True Range = Highest of (HIgh – low, abs(High – previous close), abs(low – previous close))

- Average True Range = 14 day MA of True Range

- Normalized Average True Range = ATR / Close * 100

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘HL’] = TechIndicator[stock][‘High’] – TechIndicator[stock][‘Low’]

TechIndicator[stock][‘absHC’] = abs(TechIndicator[stock][‘High’] – TechIndicator[stock][‘Close’].shift(1))

TechIndicator[stock][‘absLC’] = abs(TechIndicator[stock][‘Low’] – TechIndicator[stock][‘Close’].shift(1))

TechIndicator[stock][‘TR’] = TechIndicator[stock][[‘HL’,’absHC’,’absLC’]].max(axis=1)

TechIndicator[stock][‘ATR’] = TechIndicator[stock][‘TR’].rolling(window=14).mean()

TechIndicator[stock][‘NATR’] = (TechIndicator[stock][‘ATR’] / TechIndicator[stock][‘Close’]) *100

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[5].tail()

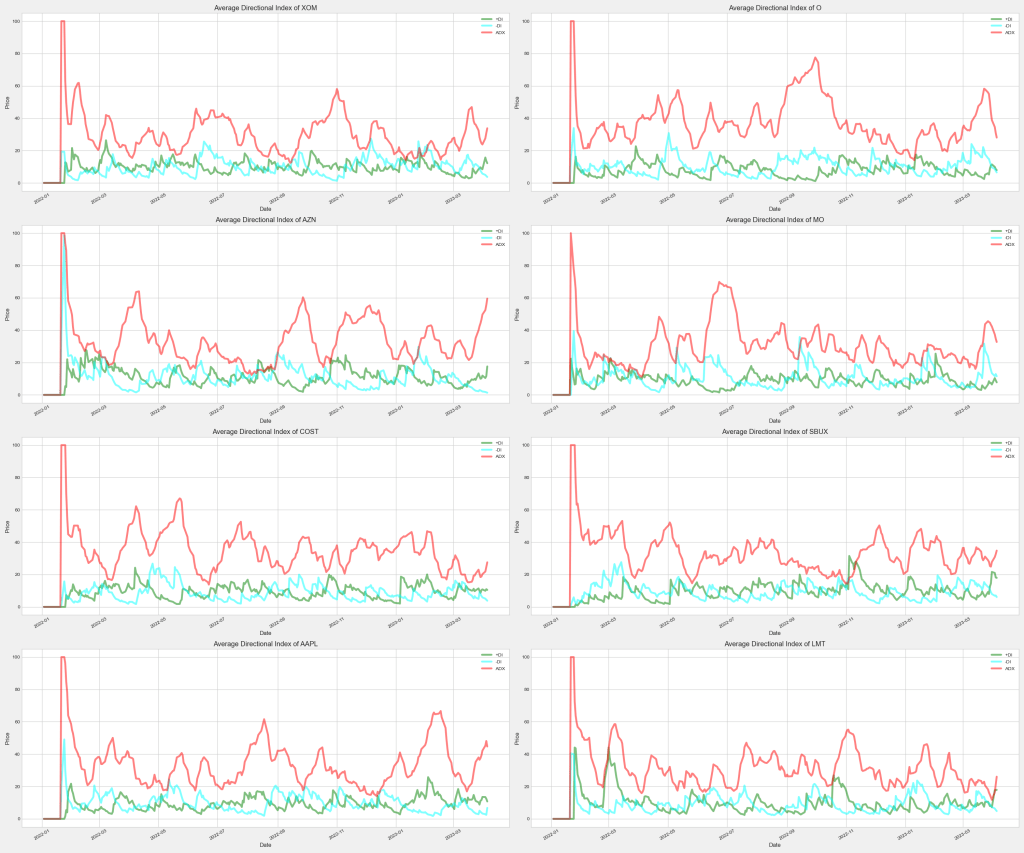

Average Directional Movement Index (ADX)

The average directional index (ADX) helps traders see the trend direction as well as the strength of that trend. The Positive Directional Indicator (+DI) is one of the lines in the Average Directional Index (ADX) indicator and is used to measure the presence of an uptrend.

- The ADX is now used in several markets by technical traders to judge the strength of a trend.

- The ADX makes use of a positive (+DI) and negative (-DI) directional indicator in addition to the trendline.

- The trend has strength when ADX is above 25; the trend is weak or the price is trendless when ADX is below 20, according to Wilder.

- Non-trending doesn’t mean the price isn’t moving. It may not be, but the price could also be making a trend change or is too volatile for a clear direction to be present.

def DMI(df, period):

df[‘UpMove’] = df[‘High’] – df[‘High’].shift(1)

df[‘DownMove’] = df[‘Low’].shift(1) – df[‘Low’]

df[‘Zero’] = 0

df['PlusDM'] = np.where((df['UpMove'] > df['DownMove']) & (df['UpMove'] > df['Zero']), df['UpMove'], 0)

df['MinusDM'] = np.where((df['UpMove'] < df['DownMove']) & (df['DownMove'] > df['Zero']), df['DownMove'], 0)

df['plusDI'] = 100 * (df['PlusDM']/df['ATR']).ewm(span=period,min_periods=0,adjust=True,ignore_na=False).mean()

df['minusDI'] = 100 * (df['MinusDM']/df['ATR']).ewm(span=period,min_periods=0,adjust=True,ignore_na=False).mean()

df['ADX'] = 100 * (abs((df['plusDI'] - df['minusDI'])/(df['plusDI'] + df['minusDI']))).ewm(span=period,min_periods=0,adjust=True,ignore_na=False).mean()

for stock in range(len(TechIndicator)):

DMI(TechIndicator[stock], 14)

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[5].tail()

columns2Drop = [‘UpMove’, ‘DownMove’, ‘ATR’, ‘PlusDM’, ‘MinusDM’, ‘Zero’, ‘EMA’, ‘HL’, ‘absHC’, ‘absLC’, ‘TR’]

for stock in range(len(TechIndicator)):

TechIndicator[stock] = TechIndicator[stock].drop(labels = columns2Drop, axis=1)

TechIndicator[2].head()

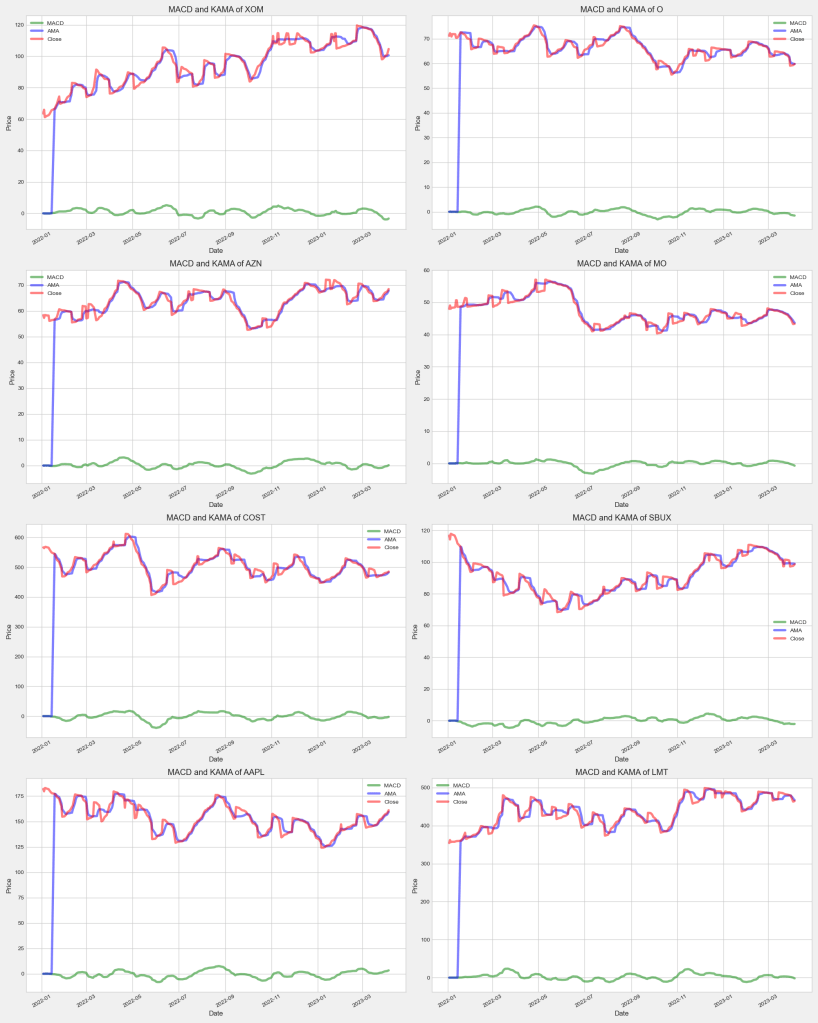

MACD

- Moving average convergence/divergence (MACD, or MAC-D) is a trend-following momentum indicator that shows the relationship between two exponential moving averages (EMAs) of a security’s price. The MACD line is calculated by subtracting the 26-period EMA from the 12-period EMA.

- The result of that calculation is the MACD line. A nine-day EMA of the MACD line is called the signal line, which is then plotted on top of the MACD line, which can function as a trigger for buy or sell signals.

- Traders may buy the security when the MACD line crosses above the signal line and sell—or short—the security when the MACD line crosses below the signal line. MACD indicators can be interpreted in several ways, but the more common methods are crossovers, divergences, and rapid rises/falls.

- MACD is best used with daily periods, where the traditional settings of 26/12/9 days is the norm.

- MACD triggers technical signals when the MACD line crosses above the signal line (to buy) or falls below it (to sell).

- MACD can help gauge whether a security is overbought or oversold, alerting traders to the strength of a directional move, and warning of a potential price reversal.

- MACD can also alert investors to bullish/bearish divergences (e.g., when a new high in price is not confirmed by a new high in MACD, and vice versa), suggesting a potential failure and reversal.

- After a signal line crossover, it is recommended to wait for three or four days to confirm that it is not a false move.

for stock in range(len(TechIndicator)):

TechIndicator[stock][’26_ema’] = TechIndicator[stock][‘Close’].ewm(span=26,min_periods=0,adjust=True,ignore_na=False).mean()

TechIndicator[stock][’12_ema’] = TechIndicator[stock][‘Close’].ewm(span=12,min_periods=0,adjust=True,ignore_na=False).mean()

TechIndicator[stock][‘MACD’] = TechIndicator[stock][’12_ema’] – TechIndicator[stock][’26_ema’]

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[2].tail()

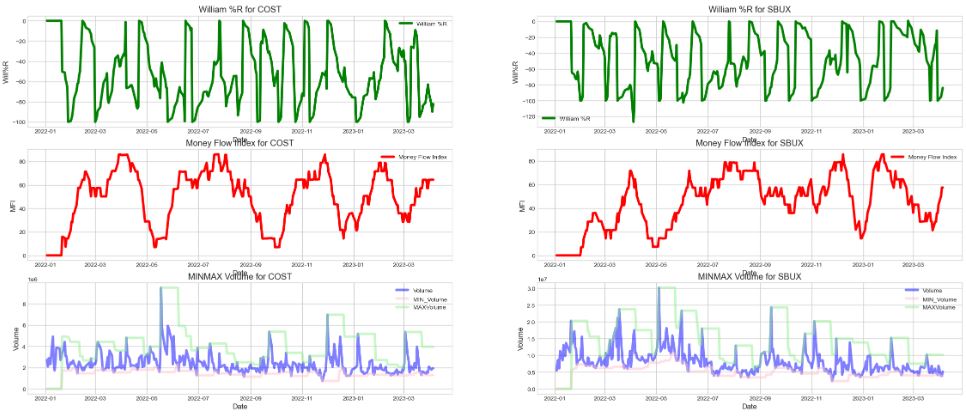

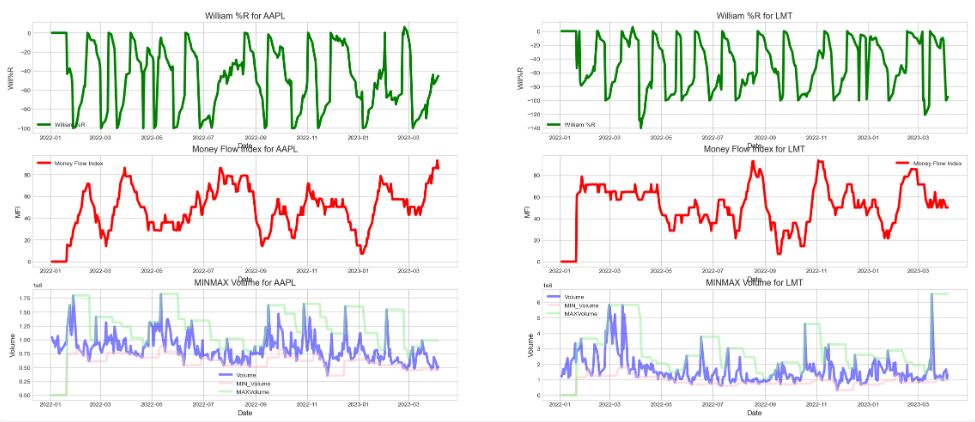

Money Flow Index (MFI)

Money flow is calculated by averaging the high, low and closing prices, and multiplying by the daily volume. Comparing that result with the number for the previous day tells traders whether money flow was positive or negative for the current day. Positive money flow indicates that prices are likely to move higher, while negative money flow suggests prices are about to fall.

Typical Price = (High + Low + Close)/3

Raw Money Flow = Typical Price x Volume

The money flow is divided into positive and negative money flow.

- Positive money flow is calculated by adding the money flow of all the days where the typical price is higher than the previous day’s typical price.

- Negative money flow is calculated by adding the money flow of all the days where the typical price is lower than the previous day’s typical price.

- If typical price is unchanged then that day is discarded.

- Money Flow Ratio = (14-period Positive Money Flow)/(14-period Negative Money Flow)

- Money Flow Index = 100 – 100/(1 + Money Flow Ratio)

def MFI(df):

# typical price

df[‘tp’] = (df[‘High’]+df[‘Low’]+df[‘Close’])/3

#raw money flow

df[‘rmf’] = df[‘tp’] * df[‘Volume’]

# positive and negative money flow

df['pmf'] = np.where(df['tp'] > df['tp'].shift(1), df['tp'], 0)

df['nmf'] = np.where(df['tp'] < df['tp'].shift(1), df['tp'], 0)

# money flow ratio

df['mfr'] = df['pmf'].rolling(window=14,center=False).sum()/df['nmf'].rolling(window=14,center=False).sum()

df['Money_Flow_Index'] = 100 - 100 / (1 + df['mfr'])

for stock in range(len(TechIndicator)):

MFI(TechIndicator[stock])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[2].tail()

Ichimoku Cloud

- The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

- The Ichimoku Cloud is composed of five lines or calculations, two of which comprise a cloud where the difference between the two lines is shaded in.

- The lines include a nine-period average, a 26-period average, an average of those two averages, a 52-period average, and a lagging closing price line.

- The cloud is a key part of the indicator. When the price is below the cloud, the trend is down. When the price is above the cloud, the trend is up.

- The above trend signals are strengthened if the cloud is moving in the same direction as the price. For example, during an uptrend, the top of the cloud is moving up, or during a downtrend, the bottom of the cloud is moving down.

- Turning Line = ( Highest High + Lowest Low ) / 2, for the past 9 days

- Standard Line = ( Highest High + Lowest Low ) / 2, for the past 26 days

- Leading Span 1 = ( Standard Line + Turning Line ) / 2, plotted 26 days ahead of today

- Leading Span 2 = ( Highest High + Lowest Low ) / 2, for the past 52 days, plotted 26 days ahead of today

- Cloud = Shaded Area between Span 1 and Span 2

def ichimoku(df):

# Turning Line

period9_high = df[‘High’].rolling(window=9,center=False).max()

period9_low = df[‘Low’].rolling(window=9,center=False).min()

df[‘turning_line’] = (period9_high + period9_low) / 2

# Standard Line

period26_high = df['High'].rolling(window=26,center=False).max()

period26_low = df['Low'].rolling(window=26,center=False).min()

df['standard_line'] = (period26_high + period26_low) / 2

# Leading Span 1

df['ichimoku_span1'] = ((df['turning_line'] + df['standard_line']) / 2).shift(26)

# Leading Span 2

period52_high = df['High'].rolling(window=52,center=False).max()

period52_low = df['Low'].rolling(window=52,center=False).min()

df['ichimoku_span2'] = ((period52_high + period52_low) / 2).shift(26)

# The most current closing price plotted 22 time periods behind (optional)

df['chikou_span'] = df['Close'].shift(-22) # 22 according to investopedia

for stock in range(len(TechIndicator)):

ichimoku(TechIndicator[stock])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[2].tail()

William %R (WillR)

Williams %R, also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way.

- Williams %R moves between zero and -100.

- A reading above -20 is overbought.

- A reading below -80 is oversold.

- An overbought or oversold reading doesn’t mean the price will reverse. Overbought simply means the price is near the highs of its recent range, and oversold means the price is in the lower end of its recent range.

- Can be used to generate trade signals when the price and the indicator move out of overbought or oversold territory.

- %R = -100 * ( ( Highest High – Close) / ( Highest High – Lowest Low ) )

def WillR(df):

highest_high = df[‘High’].rolling(window=14,center=False).max()

lowest_low = df[‘Low’].rolling(window=14,center=False).min()

df[‘WillR’] = (-100) * ((highest_high – df[‘Close’]) / (highest_high – lowest_low))

for stock in range(len(TechIndicator)):

WillR(TechIndicator[stock])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[2].tail()

MINMAX

def MINMAX(df):

df[‘MIN_Volume’] = df[‘Volume’].rolling(window=14,center=False).min()

df[‘MAX_Volume’] = df[‘Volume’].rolling(window=14,center=False).max()

for stock in range(len(TechIndicator)):

MINMAX(TechIndicator[stock])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[2].tail()

Adaptive Moving Average (KAMA)

Developed by Perry Kaufman, Kaufman’s Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low. KAMA will adjust when the price swings widen and follow prices from a greater distance. This trend-following indicator can be used to identify the overall trend, time turning points and filter price movements.

def KAMA(price, n=10, pow1=2, pow2=30):

”’ kama indicator ”’

”’ accepts pandas dataframe of prices ”’

absDiffx = abs(price - price.shift(1) )

ER_num = abs( price - price.shift(n) )

ER_den = absDiffx.rolling(window=n,center=False).sum()

ER = ER_num / ER_den

sc = ( ER*(2.0/(pow1+1)-2.0/(pow2+1.0))+2/(pow2+1.0) ) ** 2.0

answer = np.zeros(sc.size)

N = len(answer)

first_value = True

for i in range(N):

if sc[i] != sc[i]:

answer[i] = np.nan

else:

if first_value:

answer[i] = price[i]

first_value = False

else:

answer[i] = answer[i-1] + sc[i] * (price[i] - answer[i-1])

return answer

for stock in range(len(TechIndicator)):

TechIndicator[stock][‘KAMA’] = KAMA(TechIndicator[stock][‘Close’])

TechIndicator[stock] = TechIndicator[stock].fillna(0)

TechIndicator[4].tail()

columns2Drop = [’26_ema’, ’12_ema’,’tp’,’rmf’,’pmf’,’nmf’,’mfr’]

for stock in range(len(TechIndicator)):

TechIndicator[stock] = TechIndicator[stock].drop(labels = columns2Drop, axis=1)

TechIndicator[2].head()

Visualization of Technical Indicators

%matplotlib inline

from matplotlib.dates import DateFormatter

Relative Strength Index

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

TechIndicator[i][‘mydate’]=pd.to_datetime(TechIndicator[i].index)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘RSI_14D’])

ax.set_title(str(TechIndicator[i][‘Label’][0]))

ax.set_xlabel(“Date”)

ax.set_ylabel(“Relative Strength Index”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizrsiplot.png’)

Volume Plain

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(8,1,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Volume_plain’], ‘b’)

ax.set_title(str(TechIndicator[i][‘Label’][0]))

ax.set_xlabel(“Date”)

ax.set_ylabel(“Volume”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizvolumeplain.png’)

Bollinger Bands

plt.style.use(‘fivethirtyeight’)

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.fill_between(TechIndicator[i][‘mydate’], TechIndicator[i][‘BB_Upper_Band’], TechIndicator[i][‘BB_Lower_Band’], color=’grey’, label=”Band Range”)

# Plot Adjust Closing Price and Moving Averages

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], color=’red’, lw=2, label=”Close”)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘BB_Middle_Band’], color=’black’, lw=2, label=”Middle Band”)

ax.set_title(“Bollinger Bands for ” + str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Prices”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizbollingerbands.png’)

Aroon Oscillator

plt.style.use(‘seaborn-whitegrid’)

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.fill(TechIndicator[i][‘mydate’], TechIndicator[i][‘Aroon_Oscillator’],’g’, alpha = 0.5, label = “Aroon Oscillator”)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], ‘r’, label=”Close”)

ax.set_title(“Aroon Oscillator for ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Prices”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizaroonoscillator.png’)

Summary

Price Volume Trend

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(8,1,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘PVT’], ‘black’)

ax.set_title(“Price Volume Trend of ” +str(TechIndicator[i][‘Label’][0]))

ax.set_xlabel(“Date”)

ax.set_ylabel(“Price Volume trend”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizpricevolumetrend.png’)

Acceleration Band

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.fill_between(TechIndicator[i][‘mydate’], TechIndicator[i][‘AB_Upper_Band’], TechIndicator[i][‘AB_Lower_Band’], color=’grey’, label = “Band-Range”)

# Plot Adjust Closing Price and Moving Averages

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], color=’red’, lw=2, label = “Close”)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘AB_Middle_Band’], color=’black’, lw=2, label=”Middle_Band”)

ax.set_title(“Acceleration Bands for ” + str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Prices”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizaccelerationband.png’)

Stochastic Oscillator

plt.style.use(‘seaborn-whitegrid’)

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘STOK’], ‘blue’, label=”%K”)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘STOD’], ‘red’, label=”%D”)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], color=’black’, lw=2, label = “Close”)

ax.set_title(“Stochastic Oscillators of ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Price”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizstochasticoscillator.png’)

Chaikin Money Flow

import matplotlib.gridspec as gridspec

fig = plt.figure(figsize=(25,40))

outer = gridspec.GridSpec(4, 2, wspace=0.2, hspace=0.2)

for i in range(8):

inner = gridspec.GridSpecFromSubplotSpec(2, 1,

subplot_spec=outer[i], wspace=0.1, hspace=0.1)

for j in range(2):

ax = plt.Subplot(fig, inner[j])

if j==0:

t = ax.fill(TechIndicator[i]['mydate'], TechIndicator[i]['Chaikin_MF'],'b', alpha = 0.5, label = "Chaikin MF")

ax.set_title("Chaikin Money Flow for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("Money Flow")

else:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['Close'], 'r', label="Close")

t = ax.set_ylabel("Close")

ax.legend()

ax.set_xlabel("Date")

fig.add_subplot(ax)

fig.tight_layout()

plt.savefig(‘vizchaikinmoneyflow.png’)

Parabolic SAR, Rate of Change, Momentum and VWAP

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘psar’], ‘blue’, label=”PSAR”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘ROC’], ‘red’, label=”ROC”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Momentum’], ‘green’, label=”Momentum”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘VWAP’], ‘cyan’, label=”VWAP”, alpha = 0.5)

ax.set_title(“PSAR, ROC, Momentum and VWAP of ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Price”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizpsar.png’)

Commodity Channel Index, Triple Exponential Moving Average On Balance Volume

fig = plt.figure(figsize=(25,80))

outer = gridspec.GridSpec(4, 2, wspace=0.2, hspace=0.2)

for i in range(8):

inner = gridspec.GridSpecFromSubplotSpec(3, 1,

subplot_spec=outer[i], wspace=0.3, hspace=0.3)

for j in range(3):

ax = plt.Subplot(fig, inner[j])

if j==0:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['CCI'], 'green', label="CCI")

t = ax.set_title("CCI for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("Commodity Channel Index")

elif j == 1:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['TEMA'], 'blue', label="TEMA")

t = ax.set_title("TEMA for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("TripleExponentiaL MA")

else:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['OBV'], 'red', label="OBV")

t = ax.set_title("OBV for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("On Balance Volume")

ax.legend()

ax.set_xlabel("Date")

fig.add_subplot(ax)

fig.tight_layout()

plt.savefig(‘vizccitema.png’)

Normalized Average True Range (NATR)

plt.style.use(‘ggplot’)

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘NATR’], ‘red’, label=”NATR”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], ‘cyan’, label=”Close”, alpha = 0.5)

ax.set_title(“NATR of ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Price”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘viznatr.png’)

Keltner Channels

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.fill_between(TechIndicator[i][‘mydate’], TechIndicator[i][‘Kelch_Upper’], TechIndicator[i][‘Kelch_Down’],

color=’blue’, label = “Band-Range”, alpha = 0.5)

# Plot Adjust Closing Price and Moving Averages

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], color=’red’, label = “Close”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Kelch_Middle’], color=’black’, label=”Middle_Band”, alpha = 0.5)

ax.set_title(“Keltner Channels for ” + str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Close Prices”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizkeltner.png’)

Average Directional Index

plt.style.use(‘seaborn-whitegrid’)

fig = plt.figure(figsize=(30,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘plusDI’], ‘green’, label=”+DI”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘minusDI’], ‘cyan’, label=”-DI”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘ADX’], ‘red’, label=”ADX”, alpha = 0.5)

ax.set_title(“Average Directional Index of ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Price”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizadi.png’)

MACD vs KAMA

plt.style.use(‘seaborn-whitegrid’)

fig = plt.figure(figsize=(20,25))

for i in range(8):

ax = plt.subplot(4,2,i+1)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘MACD’], ‘green’, label=”MACD”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘KAMA’], ‘blue’, label=”AMA”, alpha = 0.5)

ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘Close’], ‘red’, label=”Close”, alpha = 0.5)

ax.set_title(“MACD and KAMA of ” +str(TechIndicator[i][‘Label’][0]))

ax.legend()

ax.set_xlabel(“Date”)

ax.set_ylabel(“Price”)

plt.xticks(rotation=30)

fig.tight_layout()

plt.savefig(‘vizmacdkama.png’)

William %R, Money Flow

fig = plt.figure(figsize=(25,50))

outer = gridspec.GridSpec(4, 2, wspace=0.2, hspace=0.2)

for i in range(8):

inner = gridspec.GridSpecFromSubplotSpec(3, 1,

subplot_spec=outer[i], wspace=0.2, hspace=0.2)

for j in range(3):

ax = plt.Subplot(fig, inner[j])

if j==0:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['WillR'], 'green', label="William %R")

t = ax.set_title("William %R for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("Will%R")

elif j ==1:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['Money_Flow_Index'], 'red', label="Money Flow Index")

t = ax.set_title("Money Flow Index for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("MFI")

else:

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['Volume'], 'blue', label="Volume", alpha = 0.5)

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['MIN_Volume'], 'pink', label="MIN_Volume", alpha = 0.5)

t = ax.plot(TechIndicator[i]['mydate'], TechIndicator[i]['MAX_Volume'], 'lightgreen', label="MAXVolume", alpha = 0.5)

t = ax.set_title("MINMAX Volume for " +str(TechIndicator[i]['Label'][0]))

t = ax.set_ylabel("Volume")

ax.legend()

#ax.set_title("CCI, TEMA, OBV for " +str(techindi2[i]['Label'][0]))

ax.set_xlabel("Date")

fig.add_subplot(ax)

fig.tight_layout()

plt.savefig(‘vizwilr.png’)

Ichimoku Cloud

fig = plt.figure(figsize=(20,25)) for i in range(8): ax = plt.subplot(4,2,i+1) ax.fill_between(TechIndicator[i][‘mydate’], TechIndicator[i][‘ichimoku_span1’], TechIndicator[i][‘ichimoku_span2′], color=’blue’, label = “ichimoku cloud”, alpha = 0.5) # Plot Adjust Closing Price and Moving Averages ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘turning_line’], color=’red’, label = “Tenkan-sen”, alpha = 0.4) ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘standard_line’], color=’cyan’, label=”Kijun-sen”, alpha = 0.3) ax.plot(TechIndicator[i][‘mydate’], TechIndicator[i][‘chikou_span’], color=’green’, label=”Chikou-span”, alpha = 0.2) ax.set_title(“Ichimoku for ” + str(TechIndicator[i][‘Label’][0])) ax.legend() ax.set_xlabel(“Date”) ax.set_ylabel(“Prices”) plt.xticks(rotation=30) fig.tight_layout() plt.savefig(‘vizishimoku.png’)

Summary

- In general, technical indicators fit into five categories: trend, mean reversion, relative strength, volume, and momentum.

- Leading indicators attempt to predict where the price is headed while lagging indicators offer a historical report of background conditions that resulted in the current price being where it is.

- Most popular technical indicators include simple moving averages (SMAs), exponential moving averages (EMAs), bollinger bands, stochastics, and on-balance volume (OBV).

- Seven of the best indicators for day trading are:

- On-balance volume (OBV)

- Accumulation/distribution line

- Average directional index

- Aroon oscillator

- Moving average convergence divergence (MACD)

- Relative strength index (RSI)

- Stochastic oscillator

Bottom Line: The most experienced traders are those that have a strong understanding of technical stock indicators, which makes them better equipped to navigate complex and fast-paced financial markets.

Internal Links

- Predicting the JPM Stock Price and Breakouts with Auto ARIMA, FFT, LSTM and Technical Trading Indicators

- The Donchian Channel vs Buy-and-Hold Breakout Trading Systems – $MO Use-Case

- XOM SMA-EMA-RSI Golden Crosses ’22

- The CodeX-Aroon Auto-Trading Approach – the AAPL Use Case

- A TradeSanta’s Quick Guide to Best Swing Trading Indicators

- The Qullamaggie’s OXY Swing Breakouts

- Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

- Algorithmic Trading using Monte Carlo Predictions and 62 AI-Assisted Trading Technical Indicators (TTI)

- Predicting Trend Reversal in Algorithmic Trading using Stochastic Oscillator in Python

- Basic Stock Price Analysis in Python

Continue Exploring

- Technical indicators for trading stocks

- Python for stock analysis

- How to Build Stock Technical Indicators with Python

- Mean Reversion Trading Strategy Using Python

Infographic

Embed Socials

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment