Featured Photo by Pixabay

Contents:

- Zacks Market Research

- Seeking Alpha Insights

- Summary

- Explore More

- Pages

- Embed Socials

- Macroaxis Infographic

Zacks Market Research

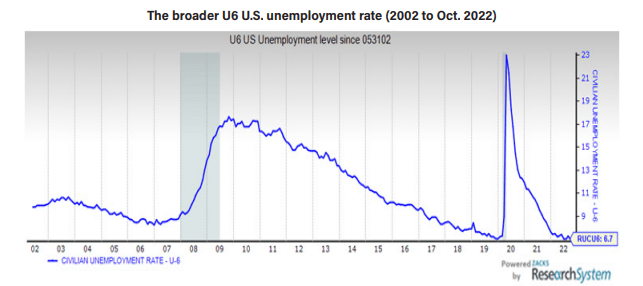

2022 has been a strong year for jobs:

Commodity markets:

- Not giving energy bulls help, no related industrial commodities from May 2022 show upside in forward 12M (Copper -0.3% Aluminum +6.9%, Nickel -4.1%).

- Keeping the virus under control (in China) remains critical. Shutdowns destroy demand for commodities. Mobility raises oil demand via transportation needs.

Energy:

- From domestic energy sources, U.S. oil rig counts are stable. Baker Hughes counted 768 on Oct. 28th (+224 from a year earlier), 767 on July 29th, 673 on April 1st, 430 on April 1st, 2021 and 351 rigs on Dec. 30th, 2020.

• Recent share price charts show bullishness on U.S. majors, XOM and CVX. A COVID share price low got put in March 2020 ~$32. XOM was $97 on June 1st and $90 on May 4th. XOM was $94 on Aug. 1st and $92 on Oct. 4th, 2022. This time, XOM was $112 on Nov. 2nd. Pre-COVID, shares traded ~$75.

Global Investments:

In the Zacks October 2022 Chief Investment Officer (CIO) survey, the CIOs made it fairly clear how they felt about investing outside the US. Answer: not great.

- Of major concern to many investors is the ongoing impact of the war in Ukraine, particularly on commodity markets, and also the downstream effects of monetary policy tightening in developed countries around the world.

- A persistently strong US dollar is also impacting the outlook for developing economies in particular.

- South Korea and Taiwan were the CIO’s top country ETF ideas, which may be translated as a nod to advanced technology and semiconductors. Outside of Asia, Brazil, Canada, Australia got identified as “OK” ETF long ideas

Corporate High Yield and Investment Grade Bonds:

In our OCT 2022 poll, CIOs thought High Yield (HY) spreads will remain stable or expand. Investment Grade (IG) spreads should expand or remain stable too. No credit spread tightening is envisioned, given the building recession fears.

Municipal Bonds:

Note: In our latest poll done in OCT 2022, CIOs were neutral on Munis.

State tax efficient munis always look excellent for older income investors. Having written that, all bond classes get pressured by rising rates. Plan to hold to maturity (on 5-year paper?). U.S. rates are rising markedly. Now, their budgets are benefitting from full employment, everywhere, along with the U.S. economy.

We see three major insights outlined:

- The small-cap Russell growth stock index remains undervalued relative to the S&P 500 index by -10.1%.

- This long U.S. small-cap consolidation period is now running to 22 months.

- Late last year, we did get a short-lived runup in small-cap land. The broad blended small-cap RUT index peaked on Nov. 8th, 2021 at 2,458.

So, look ahead 12 months. Expect an unpredictable recovery by Russell 2000 (RUT) growth stocks. Their cumulative 3-yr return stands at +10.06%, with an annualized return of +3.07%

For the 4 quarters of 2022, Zacks sees:

* For Q1-2022, S&P500 EPS growth was +9.8%; revenue grew +13.7%.

* For Q2-2022, S&P500 EPS growth was +7.2%; revenue grew +13.9%.

* For Q3-2022, S&P500 EPS growth should be +2.0%; revenue should grow +10.7%.

* For Q4-2022, S&P500 EPS growth should be -2.5%; revenue should grow +5.4%

Underlying U.S. macro fundamentals?

- U.S. private sector jobs went up +239K in OCT (+210K were Leisure/Hospitality).

- Annual pay was up +7.7% y/y, according to the ADP® Nat’l Employment Report.

3 Key Areas of Focus for Investors in 2023:

- How inflation and expected inflation influence global central bank policy

- Whether the U.S. jobs market can remain relatively strong and provide consumers with a buffer against slowing growth

- Whether U.S. corporate earnings come in better than expected—which is to say, not fall off an ‘earnings cliff.’

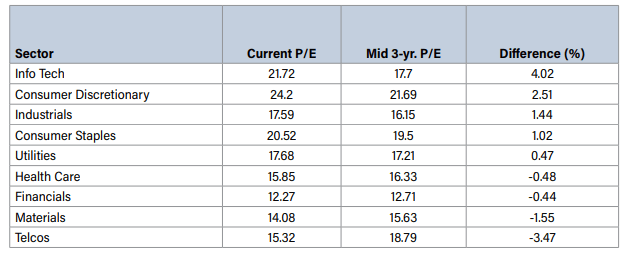

A table (below) studies these S&P500 sector forward 12-month P/E ratios, as of Oct. 31st, 2022. I list 9 S&P500 sectors. This list excludes Energy and Real Estate.

- The bullish groups? Note the largest S&P500 sector P/E differences in Info Tech (4.02), Consumer Discretionary (2.51), Industrials (1.44), and Staples (1.02).

- Utilities (0.47), Health Care (-0.48%), and Financials (-0.44) are fairly priced.

- Finally, Materials (-1.55) and Telcos (-3.47), nobody wants.

Zacks Rank S&P500 Sector Picks

- Energy stays the top sector, remaining firmly at Very Attractive. Top industries here are Oil Misc., Coal, Oil Drillers, and Oil & Gas Integrated.

- Financials moved up to Attractive from Very Attractive. Banks & Thrifts and Insurance remain the best. 2023 recession worry, and Fed rate hiking remains relevant.

- Health Care stays a Market Weight. Medical Care looks relatively better.

- Consumer Staples went to Market Weight from Very Attractive. Agri-business stood out.

- Info Tech stayed Unattractive. Computer Software-Services is the standout. Semis look terrible.

- Communications Services stays at Market Weight. Telco Equipment and Telco Services look about the same now. Market Weight for both.

- Industrials fell to Unattractive from Market Weight. Pollution control is the best. Metal Fabricating and Machinery are OK.

- Consumer Discretionary fell to Very Unattractive from Unattractive. Leisure Services looks the best. Nonfood Retail was solid.

- Materials fell to Very Unattractive from Unattractive. Building Products look the best, at market weight.

- Utilities stay Very Unattractive. Utilities-Electric Power look best.

Small Cap, Mid Cap, and Large Cap stocks

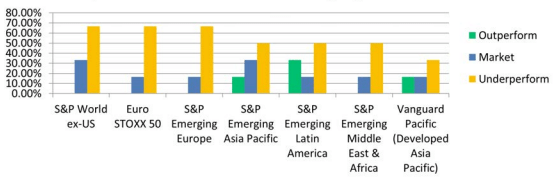

- The likeliest Large Cap return is (+5% to +10%) in 12 months. Large Cap Value indexes Out Perform. Large Cap Growth indexes Under Perform.

• The likeliest Mid Cap return is (+5 to +15%) in 12 months. Mid Cap Value indexes Out Perform. Mid Cap Growth indexes Under Perform.

• The likeliest Small Cap return is (+10% to +15%) in 12 months. Small Cap Value indexes Out Perform. Small Cap Growth indexes Under Perform.

Commodities vs Gold

In October 2022, CIOs were bearish on Commodities and bullish or market weight on Gold. In Nov. 2019, CIOs were bearish on Gold.

Setting U.S. returns expectations for 2023

For bulls, seven of 16 Zacks S&P500 sectors show strong Q3-22 earnings estimates:

• Oil/Energy (+128.9%)

• Transportation (+58.9%)

• Consumer Discretionary (+27.4%)

• Autos (+34.5%)

• Construction (+24.5%)

• Industrial Products (+17.8%)

• Business Services (+7.9%)

With S&P500 Q3 earnings growth at +2.0%, two Zacks sectors roughly align 1-for-1:

• Consumer Staples (+0.5%)

• Conglomerates (+2.3%)

For bears, seven Zacks S&P500 sectors show weak earnings growth.

• Medical (-3.8%)

• Finance (-8.2%)

• Utilities (-8.4%)

• Retail/Wholesale (-8.5%)

• Technology (-14.6%)

• Basic Materials (-21.8%)

• Aerospace (-51.3%)

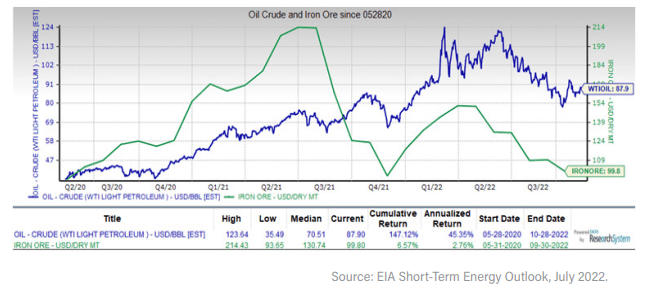

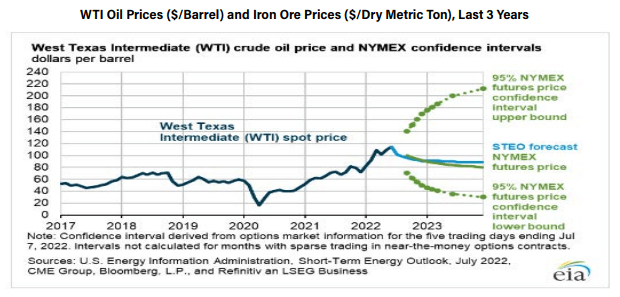

WTI Oil

Zacks Consensus looks for $86.60 a WTI barrel and $91.06 a Brent barrel in June 2023.

What Produces 2023 Optimism?

1. Bulls celebrate 95% vaccine efficacy, and bivalent booster shots.

2. With an experienced U.S. administration, public health, trade, military advisory, and diplomatic cooperation are stronger across states and countries.

3. We could see a Fed Powell pause, albeit a more delayed one. We have dovish European and Japanese central banks.

4.There is the arrival of $1T in “Infrastructure” funds to factor in.

Seeking Alpha Insights

2022 Overview:

- 2022 was exceptionally volatile in the markets, with all major indexes heading towards ending the year in the red.

- Trouble is brewing in Europe again, but not only on the border of Ukraine and Russia. A flare-up in the Balkans is threatening the stability of the continent, with the epicenter of the conflict taking place in northern Kosovo.

2022 Review: Major Asset Classes

2022 Review: U.S. Equity Risk Factors

A December That Will Be Painful To Remember

- December 2022 is set to be a standout exception as one of the worst last months of the year for the U.S. benchmark index since 1957.

- The Bloomberg bond indexes have also been a travesty for 2022. Treasuries are down -11.97%, IG Corporates down -15.15%, HY bonds down -10.35%, MBS down -11.09% and munis are down -8.28%.

- During the last decade, the borrowing costs were relatively cheap, as the Fed kept interest rates quite low. This, however, is no longer the case as the Fed ratchets up interest rates in their continuing battle with inflation.

Wed, Dec 28, 2:04 PM

- Tesla (TSLA) has slid out of the list of the top 10 U.S. companies by market cap after logging its seventh straight decline on Tuesday. Shares plunged over 11% to under $110, bringing the YTD losses for the company led by Elon Musk to nearly 73%.

- All the Big Tech giants, which Tesla is often compared to, have been battered this year as the central bank implemented a series of severe interest rate hikes to counter inflationary pressures. Meta Platforms (META) is down 65% YTD, while Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL) and Microsoft (MSFT) are off between 30-50% in 2022.

- Solana drops further on concerns that large holders will sell

Dec. 27, 2022 6:45 AM ET

Dec. 26, 2022 2:07 PM ET

Sat, Dec 24, 2:39 PM

- More than 2,300 readers responded to this week’s Wall Street Breakfast poll. Asked where they would deploy most of their investing capital in 2023, a vast majority of readers said “stocks.”

- More than 62% of respondents will tilt most of their investments to equities (SPY) (QQQ) (IWM) (URTH), according to the results. For the more risk-averse, cash (SPRXX) at 17.5% was a favorite over bonds (TBT) (TLT) (SHY) (JNK) (LQD) (BNDW) at 12.2%, indicating that those investors are skeptical of Fed rate cuts coming next year.

- The latest Summary of Economic Projections “shows the ‘median’ FOMCer expects short rates to rise to 5.1%, and remain there for the entirety of 2023, inflation to remain hundreds of basis points above target through the end of next year, the yield curve to remain in inversion for two more years (given the current level of long rates) and the unemployment rate to ‘only’ rise 110 bps from recent trough to prospective peak,” MKM strategist and economist Michael Darda wrote in a note (emphasis his).

- Rounding out the results, 5.4% said they will put most of their capital to work in commodities (USO) (GLD) (DBC), nudging out crypto (BTC-USD) (ETH-USD) (OTC:GBTC) at 2.7%.

Ideas:

- Lumen Technologies: A Win-Win For Income Investors

- Suncor Energy: Share Buybacks To Accelerate As Debt Paydown Ends

- Citigroup: Why Its Stock Could 8x

- Spotify: Making Profits On Thin Profit Margins

- Vonovia: My #1 Recession Pick With 8% Dividend Yield

Dividends:

ETFs/Portfolio

- Battle Of The Preferred CEFs: Sell PFD, Buy FLC

- Which Of The Stocks In Your Portfolio Will Go To Zero In 2023?

- 60/40 Portfolio Set To Outperform Over The Next Decade

- U.S. Stocks Poised For Positive 2023, So Says History

- The Stock Market And The U.S. Economy In The Coming Two Weeks

REITs:

Prologis: Near The Top Of My Watchlist For 2023

NewLake Capital: A Fat Yield From An Industry That’s Suffering

Global Medical REIT: A Small Cap REIT To Own For 2023

Sell Alert: 2 REITs To Sell Before 2023

2023 US/Global Outlook

- Israel Teva Pharmaceutical: 2023 Could Finally Be The Stock’s Breakout Year

- Belgium KBC Group: Expect Special Dividends In 2023

- Greece GasLog Partners: A Big Year Ahead In 2023

- UK BP: The Bull Run Can Continue

- It Is What It Is, Intel Is My Rebound Bet For 2023

- Xerox: A Contrarian Pick For 2023

- Cisco Systems: Surprisingly Resilient

- The S&P 500 Is At Risk Of A -30% Decline In 2023

- Gold And Silver Are Setting Up For A Strong Advance In 2023 (Technical Analysis)

- Liquidity Is Vanishing: What Will It Mean For Markets In 2023?

Summary

SeekingAlpha:

- 2022 was exceptionally volatile in the markets, with all major indexes heading towards ending the year in the red.

- Trouble is brewing in Europe again, but not only on the border of Ukraine and Russia.

- Looking beyond fundamental and technical analysis or charting, historical results point to a positive year for US stocks in 2023.

- Energy Is Still A Strong Play In 2023

- S&P 500 2023 Outlook: Stay Alive In The First Half To Climb The Wall Of Worry In The Second

Zacks:

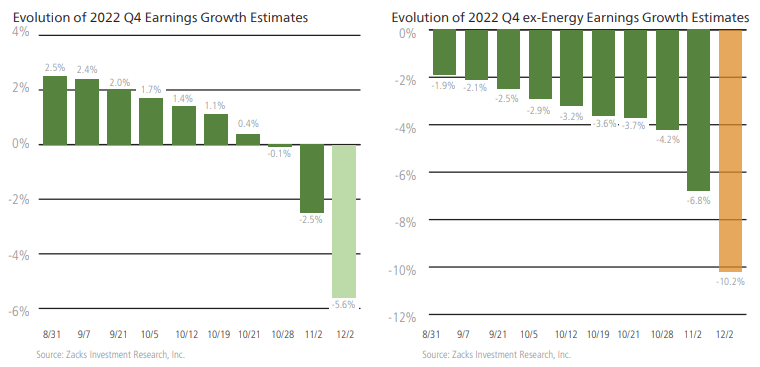

- 2022 Q4 earnings are expected to be down -5.6% on +4.3% higher revenues:

- Area of Focus #1: Global central banks and by extension,

global monetary policy.

- Area of Focus #2: How the labor market and U.S. consumers could make or break the economy

- Area of Focus #3: How corporate earnings may respond along the way.

Bottom Line for Investors:

- Importantly, some of the key sectors that are in the path of the Fed’s

tightening cycle like Construction, Retail, Discretionary, and even Technology have already shaved ~20% off their 2023 estimates since mid-April. - We are not saying that estimates don’t need to fall any further. But rather that the bulk of the cuts are likely behind us, particularly if the coming economic downturn is a lot less problematic than many seem to assume or fear – which we believe it will be.

Explore More

The Zacks Market Outlook Nov ’22 – Energy

USDTUSD | Tether USD Analysis 6 Nov ’22

Zacks Investment Research Update Q4’22

The Zacks Steady Investor – A Quick Look

Towards min(Risk/Reward) – SeekingAlpha August Bear Market Update

Zacks Insights into this High Inflation/Rising Rate Market

SeekingAlpha Risk/Reward July Rundown

Zacks Insights into the Commodity Bull Market

Are Blue-Chips Perfect for This Bear Market?

Inflation-Resistant Stocks to Buy

Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

A Weekday Market Research Update

Pages

Embed Socials

Macroaxis Infographic

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment