Featured Image by D koi on Unsplash

Following the Garcia’s exercise on how to create a portfolio testing 10,000 combinations of stocks, let’s implement the end-to-end Python stock optimization workflow that minimizes the Risk/Return ratio with respect to a market benchmark. Such a stand alone workflow consists of the following steps:

- Import Python Libraries of interest

- Set Up Key Variables (Portfolio, Benchmark, Start/End Date, etc.)

- Download, Select and Clean YahooFinance Stock Data

- Portfolio Analysis: Scenarios vs market Benchmark

- Select the Best Portfolio Scenario

- Plot Average Stock Return vs Standard Deviation

Let’s set up the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and import the following libraries

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

Let’s define our key variables

benchmark_ = [“^GSPC”,]

portfolio_ = [‘AAPL’, ‘MSFT’, ‘BRK-B’, ‘SPGI’, ‘BLK’, ‘IWDA.L’, ‘ULVR.L’, ‘SNOW’, ‘DTE.DE’, ‘UGAS.MI’, ‘EUNL.DE’, ‘EXXT.DE’, ‘GOOG’, ‘AMZN’, ‘SHOP’, ‘VOW.DE’,’MC.PA’, ‘DAX’, ‘ABNB’, ‘BX’, ‘COST’, ‘JNJ’,’NKE’, ‘PYPL’, ‘QCOM’, ‘WM’]

start_date_ = “2021-01-01”

end_date_ = “2022-09-23”

number_of_scenarios = 10000

Initialization of key vectors:

return_vector = []

risk_vector = []

distrib_vector = []

Let’s download input stock data

df = yf.download(benchmark_, start=start_date_, end=end_date_)

df2 = yf.download(portfolio_, start=start_date_, end=end_date_)

Let’s clean rows with No Values on both Benchmark and Portfolio

df = df.dropna(axis=0)

df2 = df2.dropna(axis=0)

while matching the days

df = df[df.index.isin(df2.index)]

[*********************100%***********************] 1 of 1 completed [*********************100%***********************] 26 of 26 completed

Let’s check the content of above data frames

Let’s edit the benchmark data

benchmark_vector = np.array(df[‘Close’])

by creating our daily returns

benchmark_vector = np.diff(benchmark_vector)/benchmark_vector[1:]

benchmark_return = np.average(benchmark_vector)

benchmark_risk = np.std(benchmark_vector)

and modify our return and risk vectors

return_vector.append(benchmark_return)

risk_vector.append(benchmark_risk)

Let’s perform our portfolio analysis

portfolio_vector = np.array(df2[‘Close’])

Let’s iterate through the number of pre-defined scenarios

for i in range(number_of_scenarios):

#Create a random distribution that sums 1

# and is split by the number of stocks in the portfolio

random_distribution = np.random.dirichlet(np.ones(len(portfolio_)),size=1)

distrib_vector.append(random_distribution)

#Find the Closing Price for everyday of the portfolio

portfolio_matmul = np.matmul(random_distribution,portfolio_vector.T)

#Calculate the daily return

portfolio_matmul = np.diff(portfolio_matmul)/portfolio_matmul[:,1:]

#Select or Final Return and Risk

portfolio_return = np.average(portfolio_matmul, axis=1)

portfolio_risk = np.std(portfolio_matmul, axis=1)

#Add our Benchmark info to our lists

return_vector.append(portfolio_return[0])

risk_vector.append(portfolio_risk[0])

Let’s define the risk boundaries

delta_risk = 0.1

min_risk = np.min(risk_vector)

max_risk = risk_vector[0]*(1+delta_risk)

risk_gap = [min_risk, max_risk]

Let’s merge the portfolio return and risk

portfolio_array = np.column_stack((return_vector,risk_vector))[1:,]

and define the rule to create the best portfolio

If the criteria of min risk is satisfied then:

if np.where(((portfolio_array[:,1]<= max_risk)))[0].shape[0]>1:

min_risk_portfolio = np.where(((portfolio_array[:,1]<= max_risk)))[0]

best_portfolio_loc = portfolio_array[min_risk_portfolio]

max_loc = np.argmax(best_portfolio_loc[:,0])

best_portfolio = best_portfolio_loc[max_loc]

Otherwise, if the criteria of min risk is not satisfied, then:

else:

min_risk_portfolio = np.where(((portfolio_array[:,1]== np.min(risk_vector[1:]))))[0]

best_portfolio_loc = portfolio_array[min_risk_portfolio]

max_loc = np.argmax(best_portfolio_loc[:,0])

best_portfolio = best_portfolio_loc[max_loc]

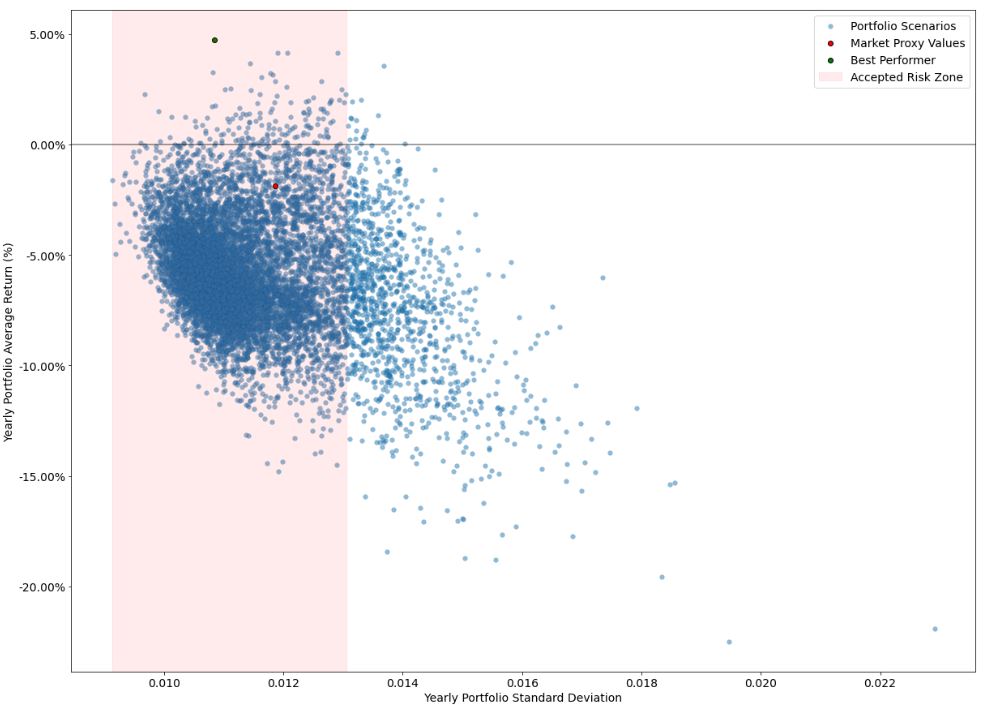

The Visual Representation is

trade_days_per_year = 252

risk_gap = np.array(risk_gap)trade_days_per_year best_portfolio[0] = np.array(best_portfolio[0])trade_days_per_year

x = np.array(risk_vector)

y = np.array(return_vector)*trade_days_per_year

fig, ax = plt.subplots(figsize=(20, 15))

plt.rc(‘axes’, titlesize=14) # Controls Axes Title

plt.rc(‘axes’, labelsize=14) # Controls Axes Labels

plt.rc(‘xtick’, labelsize=14) # Controls x Tick Labels

plt.rc(‘ytick’, labelsize=14) # Controls y Tick Labels

plt.rc(‘legend’, fontsize=14) # Controls Legend Font

plt.rc(‘figure’, titlesize=14) # Controls Figure Title

ax.scatter(x, y, alpha=0.5,

linewidths=0.1,

edgecolors=’black’,

label=’Portfolio Scenarios’

)

ax.scatter(x[0],

y[0],

color=’red’,

linewidths=1,

edgecolors=’black’,

label=’Market Proxy Values’)

ax.scatter(best_portfolio[1],

best_portfolio[0],

color=’green’,

linewidths=1,

edgecolors=’black’,

label=’Best Performer’)

ax.axvspan(min_risk,

max_risk,

color=’red’,

alpha=0.08,

label=’Accepted Risk Zone’)

ax.set_ylabel(“Yearly Portfolio Average Return (%)”,fontsize=14)

ax.set_xlabel(“Yearly Portfolio Standard Deviation”,fontsize=14)

ax.axhline(y=0, color=’black’,alpha=0.5)

ax = plt.gca()

ax.legend(loc=0)

vals = ax.get_yticks()

ax.set_yticklabels([‘{:,.2%}’.format(x) for x in vals])

plt.savefig(‘risk_optimizer.png’, dpi=300)

This plot shows the market performing (red dot) and then the maximum return at the minimum risk. That means if you would’ve held that portfolio between start and end date, you would’ve had a better portfolio than the market benchmark.

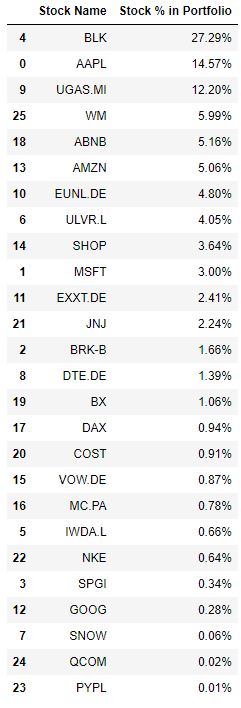

Let’s look at the output table of distributions

portfolio_loc = np.where((portfolio_array[:,0]==(best_portfolio[0]/trade_days_per_year))&(portfolio_array[:,1]==(best_portfolio[1])))[0][0]

best_distribution = distrib_vector[portfolio_loc][0].tolist()

d = {“Stock Name”: portfolio_, “Stock % in Portfolio”: best_distribution}

output = pd.DataFrame(d)

output = output.sort_values(by=[“Stock % in Portfolio”],ascending=False)

output= output.style.format({“Stock % in Portfolio”: “{:.2%}”})

output

The above portfolio optimization script is the efficient way to assess whether investment goals and outcomes have been met.

Explore More

Leave a comment