This project was inspired by the Qullamaggie’s breakout strategy for swing traders implemented as a simple stock scanner in Python. We will download the TSLA historical data from Yahoo finance.

Let’s set the working directory YOURPATH and import libraries

import os

os.chdir(‘YOURPATH’)

os. getcwd()

import numpy as np

import pandas as pd

import yfinance as yf

import seaborn as sns

import matplotlib.pyplot as plt

import matplotlib

Let’s define and call the following functions:

def trend_filter(prices: pd.core.series.Series,

growth_4_min: float = 25.,

growth_12_min: float = 50.,

growth_24_min: float = 80.) -> np.array:

”’

Take in a pandas series and output a binary array to indicate if a stock

fits the growth criteria (1) or not (0)

Parameters

———-

prices : pd.core.series.Series

The prices we are using to check for growth

growth_4_min : float, optional

The minimum 4 week growth. The default is 25

growth_12_min : float, optional

The minimum 12 week growth. The default is 50

growth_24_min : float, optional

The minimum 24 week growth. The default is 80

Returns

——-

np.array

A binary array showing the positions where the growth criteria is met

”’

growth_func = lambda x: 100*(x.values[-1]/x.min() - 1)

growth_4 = df['Close'].rolling(20).apply(growth_func) > growth_4_min

growth_12 = df['Close'].rolling(60).apply(growth_func) > growth_12_min

growth_24 = df['Close'].rolling(120).apply(growth_func) > growth_24_min

return np.where(

growth_4 | growth_12 | growth_24,

1,

0,

)

if name == ‘main‘:

df = yf.download('TSLA')

df.loc[:, 'trend_filter'] = trend_filter(df['Close'])

df.dropna()

[*********************100%***********************] 1 of 1 completed

df_trending = df[df[‘trend_filter’] == 1]

def explicit_heat_smooth(prices: np.array,

t_end: float = 5.0) -> np.array:

”’

Smoothen out a time series using a explicit finite difference method.

Parameters

———-

prices : np.array

The price to smoothen

t_end : float

The time at which to terminate the smootheing (i.e. t = 2)

Returns

——-

P : np.array

The smoothened time-series

”’

k = 0.1 # Time spacing, must be < 1 for numerical stability

# Set up the initial condition

P = prices

t = 0

while t < t_end:

# Solve the finite difference scheme for the next time-step

P = k*(P[2:] + P[:-2]) + P[1:-1]*(1-2*k)

# Add the fixed boundary conditions since the above solves the interior

# points only

P = np.hstack((

np.array([prices[0]]),

P,

np.array([prices[-1]]),

))

t += k

return P

def check_consolidation(prices: np.array,

perc_change_days: int,

perc_change_thresh: float,

check_days: int) -> int:

”’

Smoothen the time-series and check for consolidation, see the

docstring of find_consolidation for the parameters

”’

# Find the smoothed representation of the time series

prices = explicit_heat_smooth(prices)

# Perc change of the smoothed time series to perc_change_days days prior

perc_change = prices[perc_change_days:]/prices[:-perc_change_days] - 1

consolidating = np.where(np.abs(perc_change) < perc_change_thresh, 1, 0)

# Provided one entry in the last n days passes the consolidation check,

# we say that the financial instrument is in consolidation on the end day

if np.sum(consolidating[-check_days:]) > 0:

return 1

else:

return 0

def find_consolidation(prices: np.array,

days_to_smooth: int = 50,

perc_change_days: int = 5,

perc_change_thresh: float = 0.015,

check_days: int = 5) -> np.array:

”’

Return a binary array to indicate whether each of the data-points are

classed as consolidating or not

Parameters

———-

prices : np.array

The price time series to check for consolidation

days_to_smooth : int, optional

The length of the time-series to smoothen (days). The default is 50.

perc_change_days : int, optional

The days back to % change compare against (days). The default is 5.

perc_change_thresh : float, optional

The range trading % criteria for consolidation. The default is 0.015.

check_days : int, optional

This says the number of lookback days to check for any consolidation.

If any days in check_days back is consolidating, then the last data

point is said to be consolidating. The default is 5.

Returns

——-

res : np.array

The binary array indicating consolidation (1) or not (0)

”’

res = np.full(prices.shape, np.nan)

for idx in range(days_to_smooth, prices.shape[0]):

res[idx] = check_consolidation(

prices = prices[idx-days_to_smooth:idx],

perc_change_days = perc_change_days,

perc_change_thresh = perc_change_thresh,

check_days = check_days,

)

return res

if name == ‘main‘:

df = yf.download('TSLA')

df.loc[:, 'consolidating'] = find_consolidation(df['Close'].values)

df.dropna()

[*********************100%***********************] 1 of 1 completed

Let’s check the content of our data frame df

df.info()

class 'pandas.core.frame.DataFrame'> DatetimeIndex: 3051 entries, 2010-06-29 to 2022-08-10 Data columns (total 9 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Open 3051 non-null float64 1 High 3051 non-null float64 2 Low 3051 non-null float64 3 Close 3051 non-null float64 4 Adj Close 3051 non-null float64 5 Volume 3051 non-null int64 6 consolidating 3001 non-null float64 7 trend_filter 3051 non-null int32 8 filtered 3051 non-null bool dtypes: bool(1), float64(6), int32(1), int64(1) memory usage: 205.6 KB

Let’s look at the date index

df.index = pd.DatetimeIndex(data=df.index, tz=’US/Eastern’) # naive–> aware

df.index

DatetimeIndex(['2010-06-29 00:00:00-04:00', '2010-06-30 00:00:00-04:00',

'2010-07-01 00:00:00-04:00', '2010-07-02 00:00:00-04:00',

'2010-07-06 00:00:00-04:00', '2010-07-07 00:00:00-04:00',

'2010-07-08 00:00:00-04:00', '2010-07-09 00:00:00-04:00',

'2010-07-12 00:00:00-04:00', '2010-07-13 00:00:00-04:00',

...

'2022-07-28 00:00:00-04:00', '2022-07-29 00:00:00-04:00',

'2022-08-01 00:00:00-04:00', '2022-08-02 00:00:00-04:00',

'2022-08-03 00:00:00-04:00', '2022-08-04 00:00:00-04:00',

'2022-08-05 00:00:00-04:00', '2022-08-08 00:00:00-04:00',

'2022-08-09 00:00:00-04:00', '2022-08-10 00:00:00-04:00'],

dtype='datetime64[ns, US/Eastern]', name='Date', length=3051, freq=None)

dft = pd.DataFrame({‘DateTime’: df.index})

dft.DateTime

0 2010-06-29 00:00:00-04:00

1 2010-06-30 00:00:00-04:00

2 2010-07-01 00:00:00-04:00

3 2010-07-02 00:00:00-04:00

4 2010-07-06 00:00:00-04:00

...

3046 2022-08-04 00:00:00-04:00

3047 2022-08-05 00:00:00-04:00

3048 2022-08-08 00:00:00-04:00

3049 2022-08-09 00:00:00-04:00

3050 2022-08-10 00:00:00-04:00

Name: DateTime, Length: 3051, dtype: datetime64[ns, US/Eastern]

Selecting rows based on condition

df1 = df[df[‘filtered’] > 0]

df0 = df[df[‘filtered’] < 1]

dft1 = pd.DataFrame({‘DateTime’: df1.index})

dft0 = pd.DataFrame({‘DateTime’: df0.index})

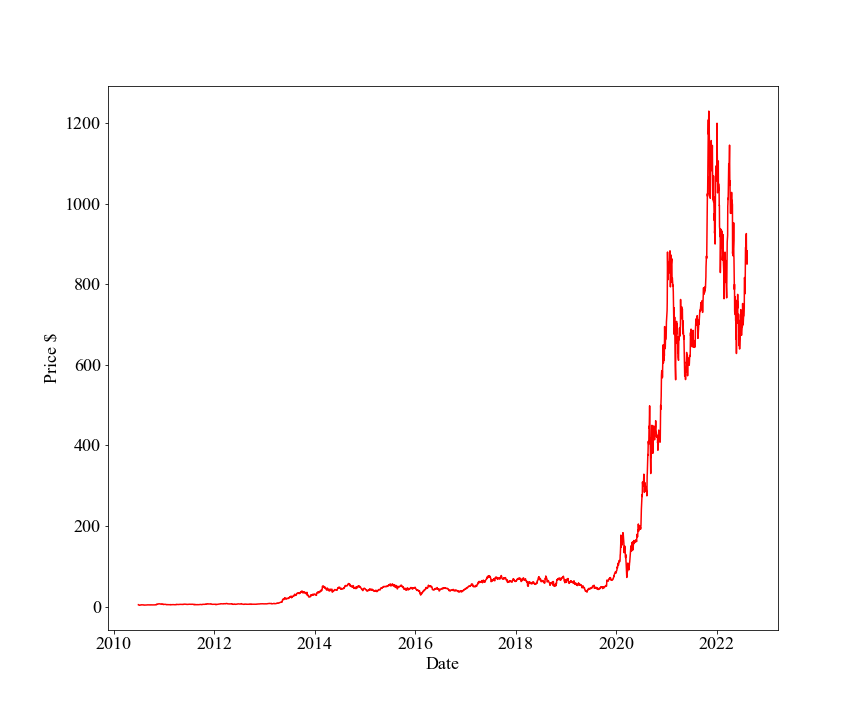

Let’s plot the TSLA stock price 2010-2022

plt.figure(figsize=(12,10))

matplotlib.rcParams.update({‘font.size’: 18})

import matplotlib.pyplot as plt

plt.plot(dft.DateTime,df.Close, ‘r’)

plt.xlabel(“Date”)

plt.ylabel(“Price $”)

plt.savefig(‘tslaprice.png’)

Let’s display the original close price (red) vs filtered data or breakouts (green) as the following composite scatter plot

plt.figure(figsize=(12,10))

scal=5e5

plt.scatter(df0.index, df0[“Close”],color=’red’,s=df0[“Volume”]/scal,alpha=0.4)

plt.scatter(df1.index, df1[“Close”],color=’green’,s=df1[“Volume”]/scal,alpha=0.4)

plt.xlabel(“Date”)

plt.ylabel(“Price $”)

plt.legend([“Close” , “Filtered”], facecolor=’bisque’,

loc=’upper center’, bbox_to_anchor=(0.5, -0.08),

ncol=2)

plt.grid()

plt.show()

plt.savefig(‘tslapriceswingfilter.png’)

This is done by using the following breakout parameters:

- Time-series days to smoothen = 50 days

- How many days back to percentage check = 5 (i.e. percentage change of the recent day to 5 days ago, to see if it’s rangebound).

- The threshold % to define a rangebound data-point = 1.5%

- The number of days to check for consolidation = 5

The above plot shows the “filtered” price where we observe consolidation that meets the growth criteria at a given date/time. This scanner is very simple and efficient in that it can be applied to a 1000’s of stocks to identify potential consolidation/breakout patterns of interest to swing traders.

Read More

Regarding Qullamaggies’s video named ‘My scanning process and scans’

Any Really Successful traders using KQ’s Methods? (self.qullamaggie)

submitted 3 months ago byFickle-Jury-5844

Stock Day Trading, Swing Trading & Investing 3-Course Bundle

The Ultimate 3-Course Stock Trading Bundle For Day Trading, Swing Trading, & Investing In The Stock Market!

Swing Trading: What It Is & How It Works

Day Trading vs. Swing Trading: What’s the Difference?

Track All Markets with TradingView

Macroaxis Wealth Optimization

Upswing Resilient Investor Guide

Leave a comment