Referring to the Pup’s Weekday Dig #58 (Jun 8, 2022), let’s look at the following top three updated alerts:

- $RRC – Triggered yesterday

- $CCJ – Big move yesterday on news. Shares of uranium companies are trading higher following a report the US is seeking $4.3 billion to buy enriched uranium from domestic sources

- $STNG – an additional target.

Range Resources Corp (RRC) 36.00 -1.02 (-2.76%) 06/08/22 [NYSE]

Previous Close37.02

Volume4,599,400

Avg Vol4,742,895

Stochastic %K90.48%

Weighted Alpha+121.50

5-Day Change+0.76 (+2.16%)

52-Week Range

Range Resources Corporation is a natural gas exploration and production company headquartered in Fort Worth, Texas. It operates in the Marcellus Formation, where it is one of the largest land owners.

Cameco Corp (CCJ) 27.31 +0.31 (+1.15%) 06/09/22 [NYSE]

Previous Close27.00

Volume11,364,700

Avg Vol7,281,920

Stochastic %K77.74%

Weighted Alpha+32.30

5-Day Change+3.03 (+12.48%)

52-Week Range

Cameco Corporation is the world’s largest publicly traded uranium company, based in Saskatoon, Saskatchewan, Canada. In 2015, it was the world’s second largest uranium producer, accounting for 18% of world production.

Scorpio Tankers Inc (STNG)

37.33 +0.67 (+1.83%) 06/08/22 [NYSE]

Previous Close36.66

Volume1,463,400

Avg Vol1,616,785

Stochastic %K93.31%

Weighted Alpha+136.30

5-Day Change+2.51 (+7.21%)

52-Week Range11.02 – 37.71

Scorpio Tankers Inc. is a tanker shipping company founded by Emanuele A. Lauro on 1 July 2009. It is an international provider in the transportation of refined petroleum products. Scorpio Tankers is headquartered in Monaco and trades on the New York Stock Exchange.

In this post, we select these three stocks to discuss the most basic stock price analysis in Python that consists of stock prices, stock volume, market capitalization, 50/200-day moving average, scattered X-plot matrix, and stock volatility or standard deviation as a measure of risk.

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

and import/install Python libraries of interest

import pandas as pd

import datetime

import numpy as np

import matplotlib.pyplot as plt

from pandas.plotting import scatter_matrix

!pip install yfinance

import yfinance as yf

%matplotlib inline

Let’s import the stock data from Yahoo Finance

start = “2020-06-07”

end = ‘2022-06-07’

tcs = yf.download(‘RRC’,start,end)

infy = yf.download(‘CCJ’,start,end)

wipro = yf.download(‘STNG’,start,end)

[*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed

Let’s create the stock price chart

tcs[‘Open’].plot(label = ‘RRC’, figsize = (15,7))

infy[‘Open’].plot(label = “CCJ”)

wipro[‘Open’].plot(label = ‘STING’)

plt.title(‘Stock Prices of RRC, CCJ and STNG’)

plt.savefig(“pupstocks3.jpg”)

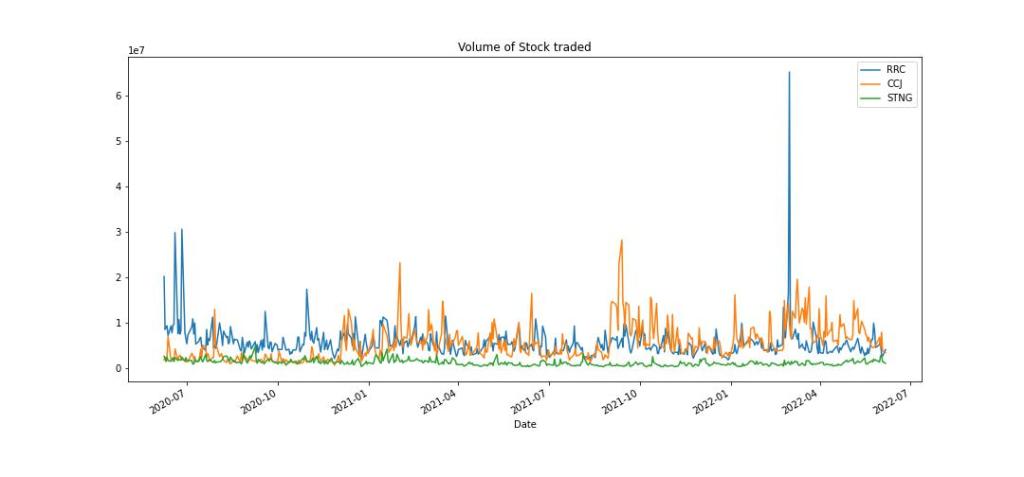

Let’s plot the volume

Let’s look at the market capitalization chart

tcs[‘MarktCap’] = tcs[‘Open’] * tcs[‘Volume’]

infy[‘MarktCap’] = infy[‘Open’] * infy[‘Volume’]

wipro[‘MarktCap’] = wipro[‘Open’] * wipro[‘Volume’]

tcs[‘MarktCap’].plot(label = ‘RRC’, figsize = (15,7))

infy[‘MarktCap’].plot(label = ‘CCJ’)

wipro[‘MarktCap’].plot(label = ‘STNG’)

plt.title(‘Market Cap’)

plt.legend()

plt.savefig(“pupmcap3.jpg”)

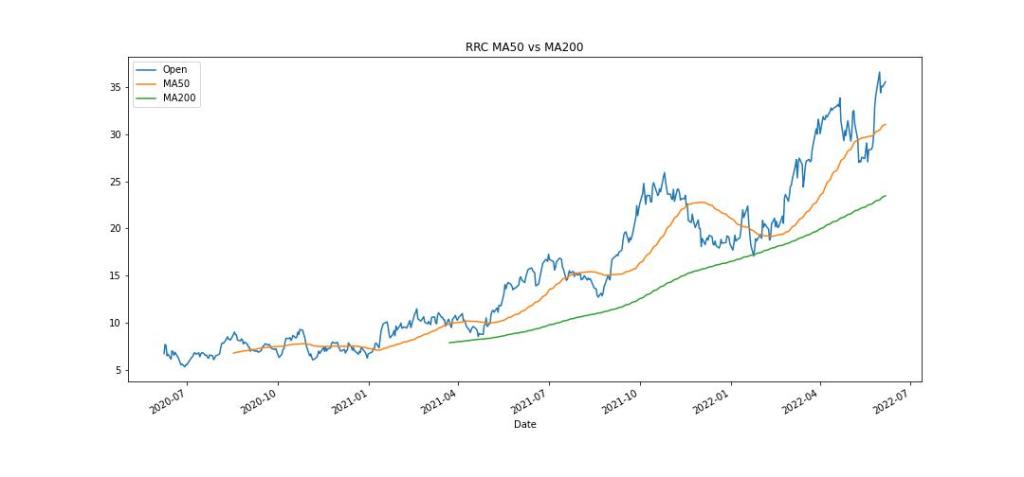

Let’s compare moving averages (MAs) for RRC

tcs[‘MA50’] = tcs[‘Open’].rolling(50).mean()

tcs[‘MA200’] = tcs[‘Open’].rolling(200).mean()

tcs[‘Open’].plot(figsize = (15,7))

tcs[‘MA50’].plot(label = “MA50”)

tcs[‘MA200’].plot(label = “MA200”)

plt.title(‘RRC MA50 vs MA200’)

plt.legend()

plt.savefig(“puprrc.jpg”)

By plotting a 200-day and 50-day moving average on your chart, a buy signal occurs when the 50-day crosses above the 200-day. A sell signal occurs when the 50-day drops below the 200-day.

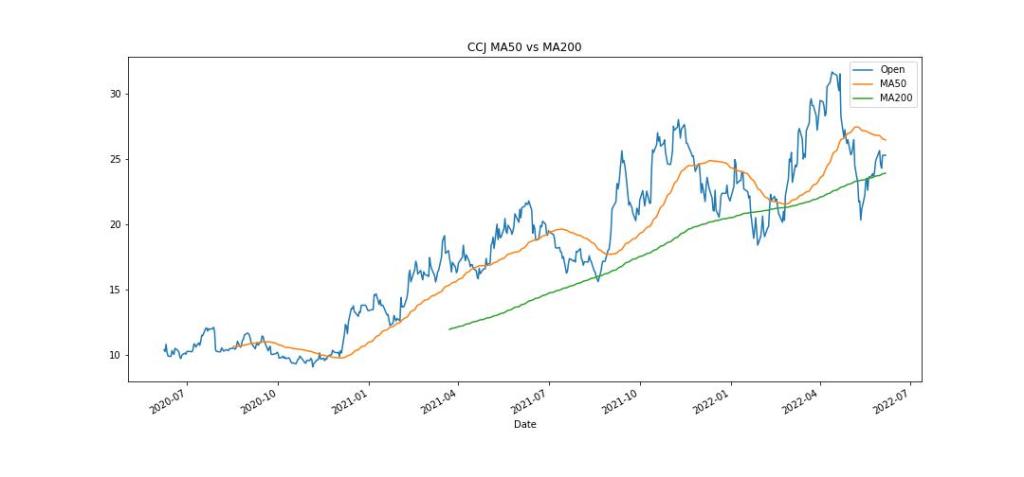

Let’s compare MAs for CCJ

infy[‘MA50’] = infy[‘Open’].rolling(50).mean()

infy[‘MA200’] = infy[‘Open’].rolling(200).mean()

infy[‘Open’].plot(figsize = (15,7))

infy[‘MA50’].plot(label = “MA50”)

infy[‘MA200’].plot(label = “MA200”)

plt.title(‘CCJ MA50 vs MA200’)

plt.legend()

plt.savefig(“pupccj.jpg”)

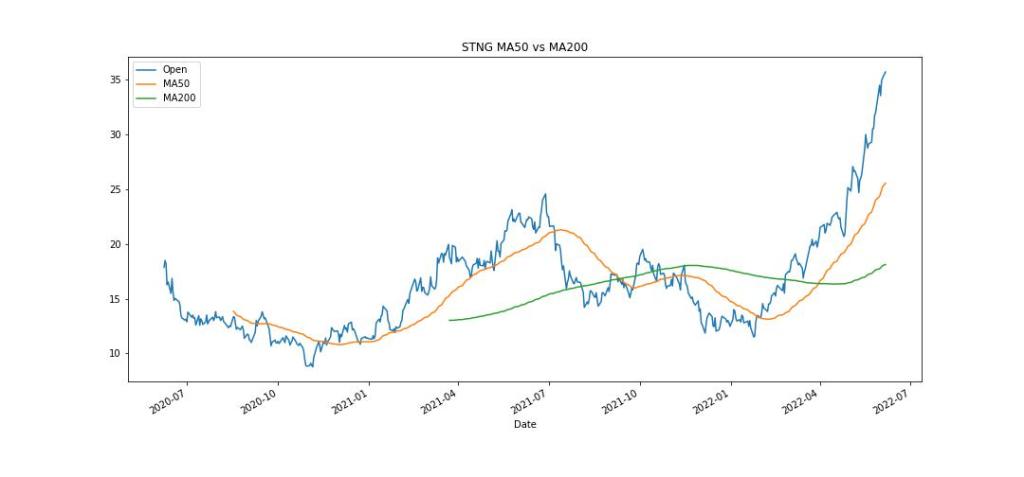

Let’s compare MAs for STNG

wipro[‘MA50’] = wipro[‘Open’].rolling(50).mean()

wipro[‘MA200’] = wipro[‘Open’].rolling(200).mean()

wipro[‘Open’].plot(figsize = (15,7))

wipro[‘MA50’].plot(label = “MA50”)

wipro[‘MA200’].plot(label = “MA200”)

plt.title(‘STNG MA50 vs MA200’)

plt.legend()

plt.savefig(“pupstng.jpg”)

These three MAs plots show a buy signal for RRC/CCJ and a sell signal for STNG.

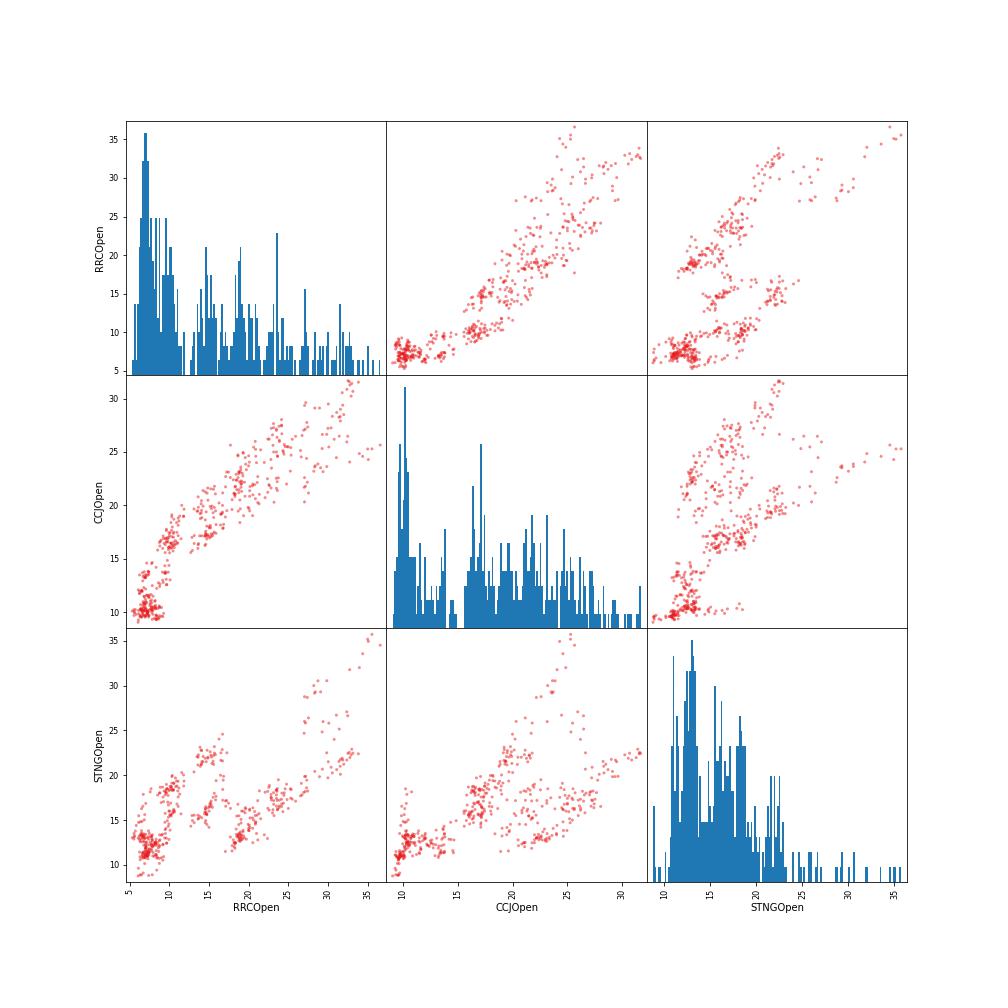

Let’s look at the scattered matrix X-plot of our 3 stocks

data = pd.concat([tcs[‘Open’],infy[‘Open’],wipro[‘Open’]],axis = 1)

data.columns = [‘RRCOpen’,’CCJOpen’,’STNGOpen’]

scatter_matrix(data, figsize = (14,14), hist_kwds= {‘bins’:150},color=’#e41a1c’)

plt.savefig(“pupxplot.jpg”)

The above graph is the combination of histograms for each stock (3 diagonal charts) and a sequence of X-plot taking two stocks at a time (off-diagonal charts). We can see a linear correlation between RRC and CCJ.

Finally, let’s compare volatility or STDEV of our selected stocks by plotting their histograms

tcs[‘returns’] = (tcs[‘Close’]/tcs[‘Close’].shift(1)) -1

infy[‘returns’] = (infy[‘Close’]/infy[‘Close’].shift(1))-1

wipro[‘returns’] = (wipro[‘Close’]/wipro[‘Close’].shift(1)) – 1

tcs[‘returns’].hist(bins = 100, label = ‘RRC’, alpha = 0.5, figsize = (15,7))

infy[‘returns’].hist(bins = 100, label = ‘CCJ’, alpha = 0.5)

wipro[‘returns’].hist(bins = 100, label = ‘STNG’, alpha = 0.5)

plt.legend()

plt.savefig(“pupstdv3.jpg”)

It is clear that our stocks have the same degree of volatility = STDEV = risk.

The above analysis represents a basic automated decision support workflow that can be used to optimize the Risk-to-Reward Ratio in real time.

Leave a comment