- In this post, we will take a deep dive into issues around predictive uncertainties of Time Series Forecasting (TSF) models. Our final goal is to minimize decision-making risks.

- TSF is a prediction of what will occur in the future, and it is an uncertain process. Because of the uncertainty, the accuracy of a forecast is as important as the outcome predicted by the TSF model.

- In this study, we’ll examine various sources of TSF, explain common Time Series Analysis (TSA) techniques, and compare different statistical vs Machine Learning (ML) approaches to forecasting.

- The sources of time series data and thus business applications of interest are many: stock prices/returns, airline passengers, housing data, federal funds rate, CO2 concentration, meteorology, sales, oil production, livestock, hotel visitors, market sentiment, etc. The different sources produce observations at different levels of detail and accuracy.

- We will only consider time series that are observed at regular intervals of time (e.g., hourly, daily, weekly, monthly, quarterly, annually). Irregularly spaced time series can also occur, but are beyond the scope of this article.

Table of Contents

- Introduction

- Random Simulation Tests

- TSLA Stock 43 Days

- TSLA Stock 300 Days

- Housing in the United States

- Industrial Production

- Federal Funds Rate Data

- S&P 500 Absolute Returns

- Number of Airline Passengers- 1. Holt-Winters

- Number of Airline Passengers- 2. Prophet

- Average Temperature in India

- Monthly Sales Data Analysis

- QC Audit of Rossmann Stores

- Rossmann Sales Forecasting – 1. Prophet

- Rossmann Sales Forecasting – 2. SARIMA

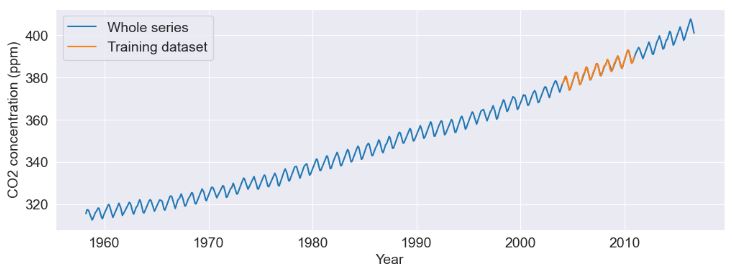

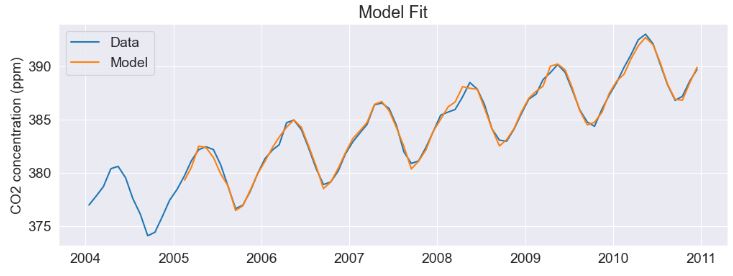

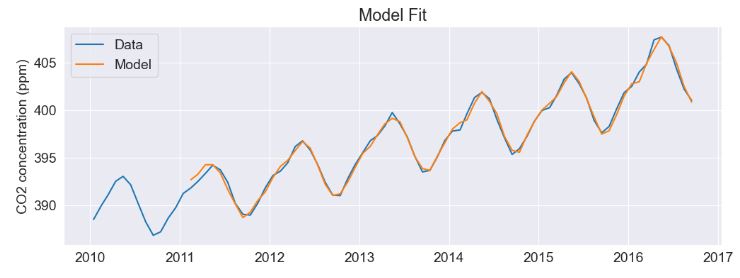

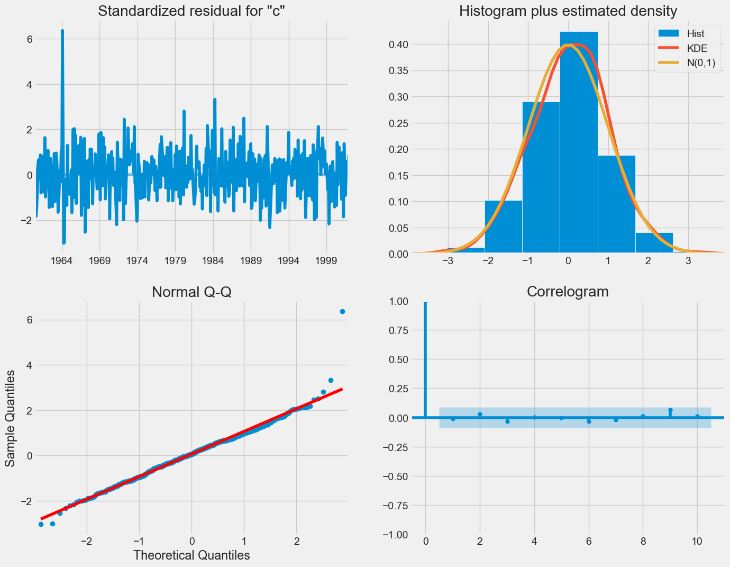

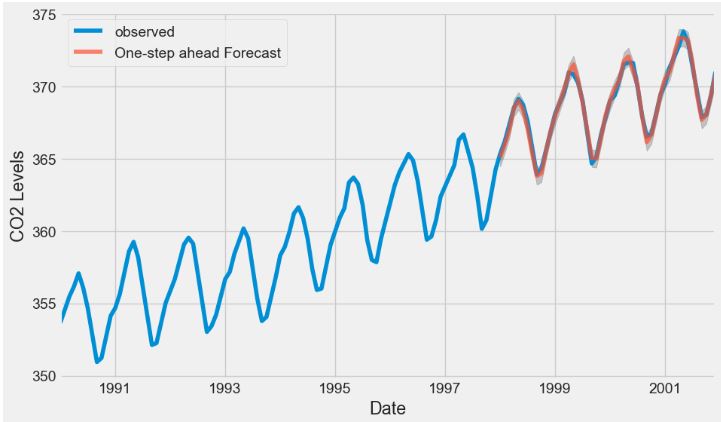

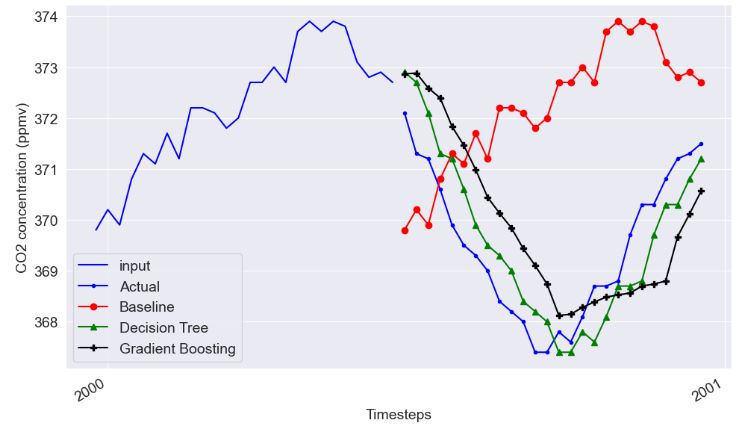

- CO2 Concentration Data – 1. SARIMA Predictions

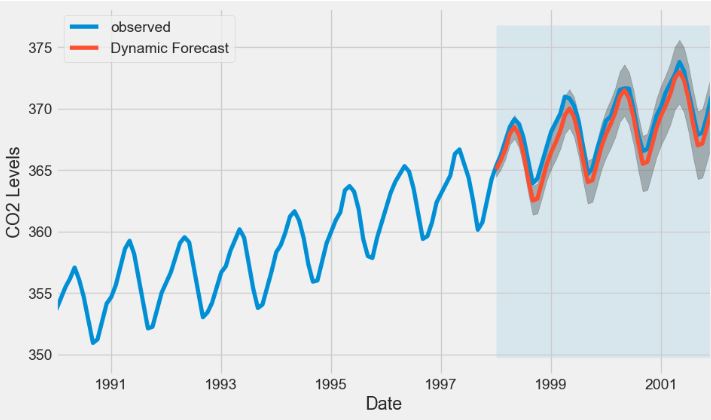

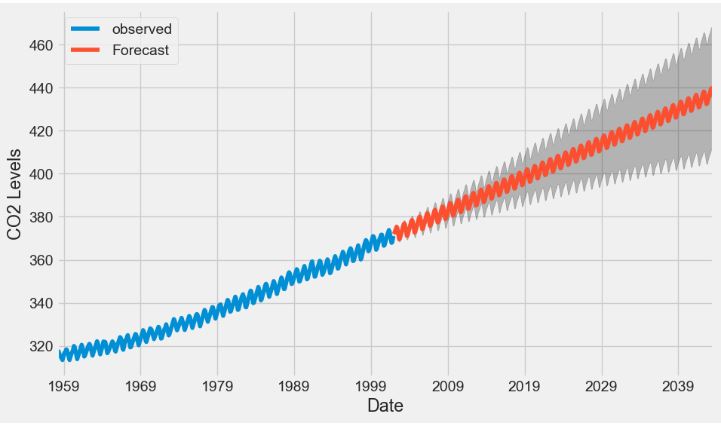

- CO2 Concentration Data – 2. ARIMA Dynamic Forecast

- CO2 Concentration Data – 3. ML Regression

- Unemployment/Interest Rate OLS

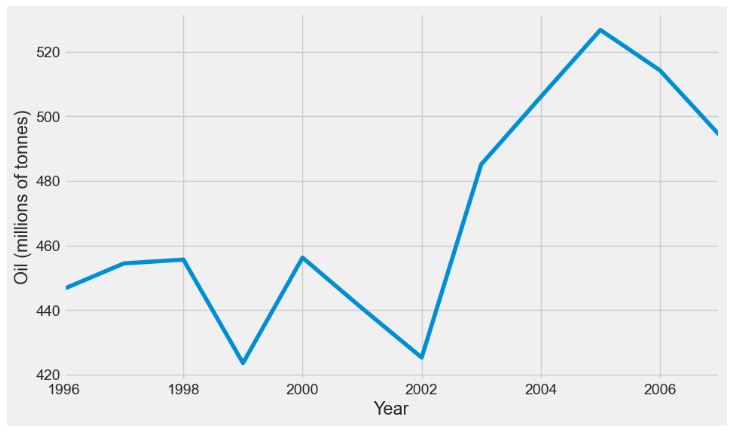

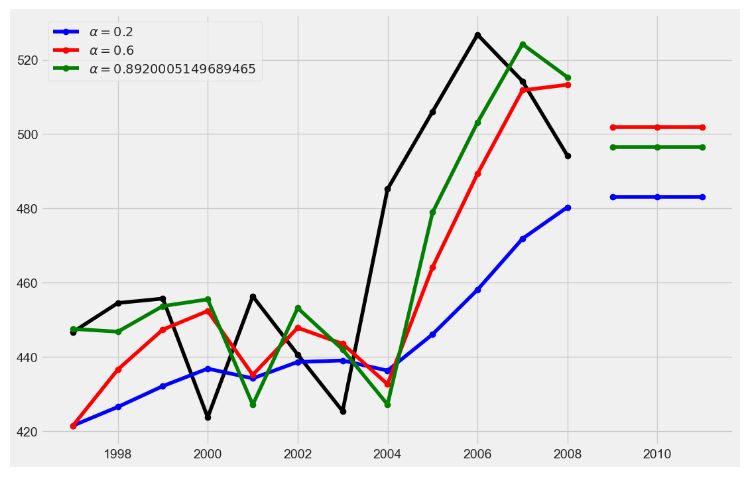

- Oil Production in Saudi Arabia

- Air Pollution & the Holt’s Method

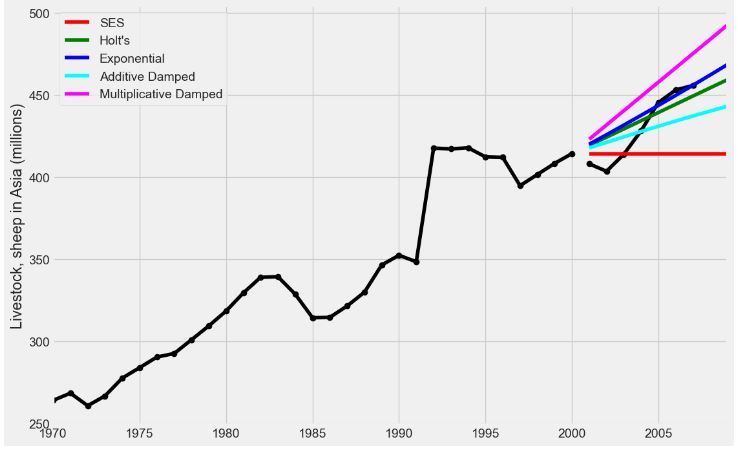

- Livestock, Sheep in Asia

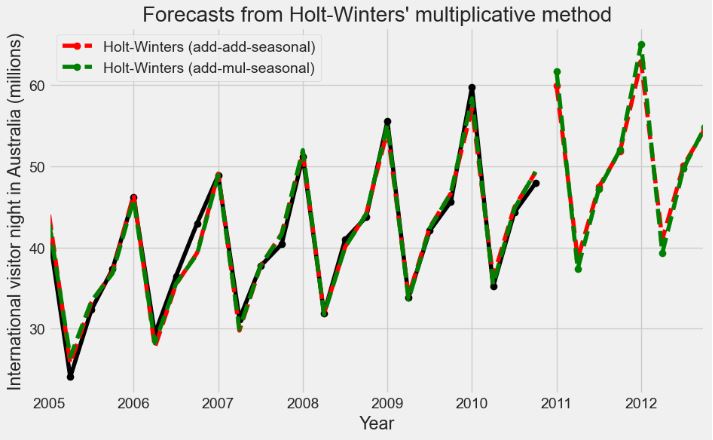

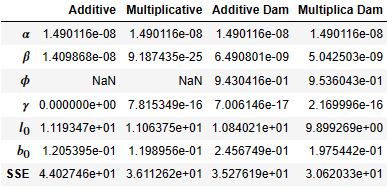

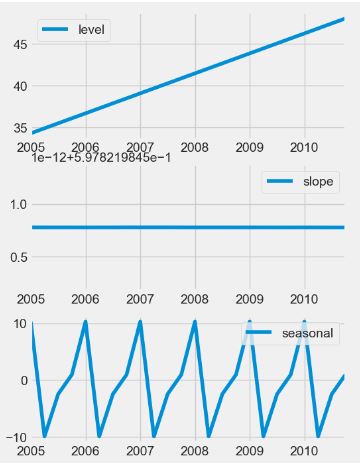

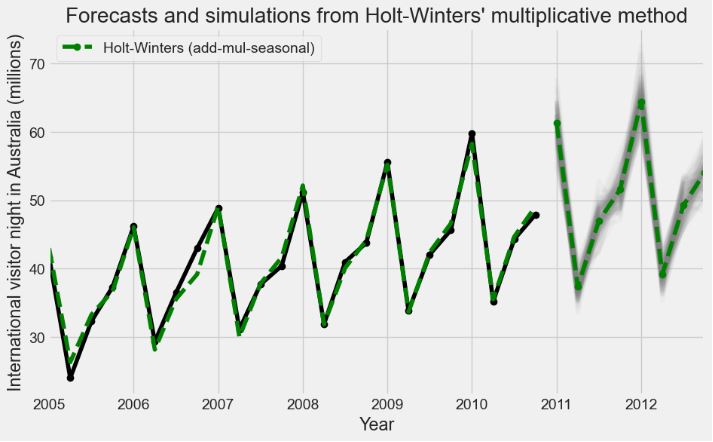

- International Visitor Nights in Australia

- Hourly Energy Demand Forecasting

- Stock Price Forecasting – 1. TSLA

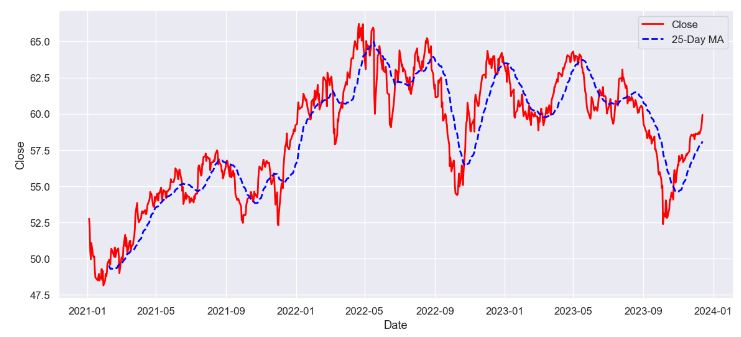

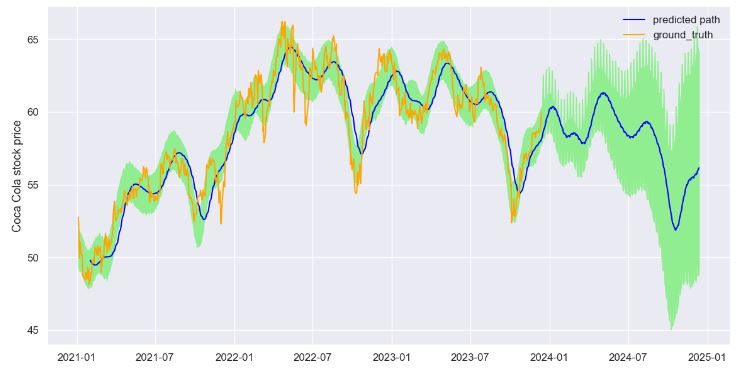

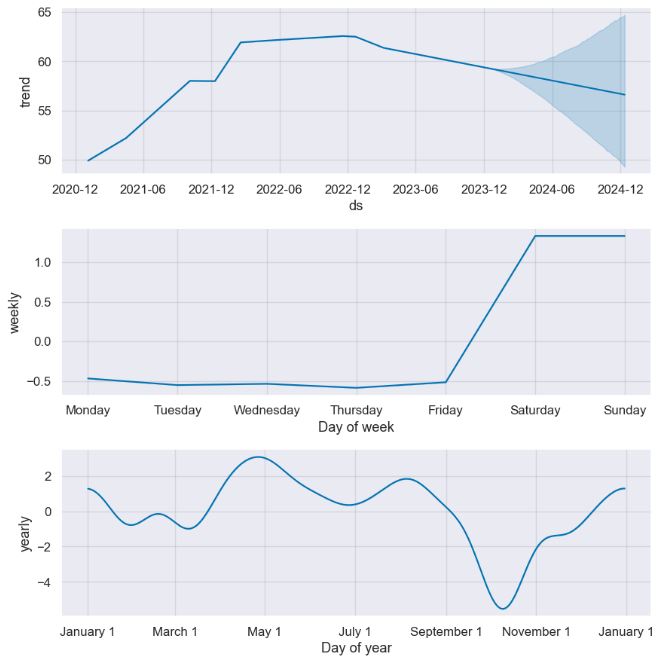

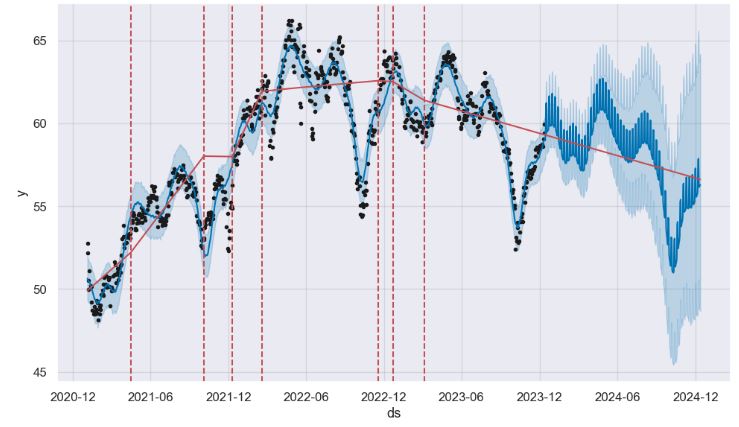

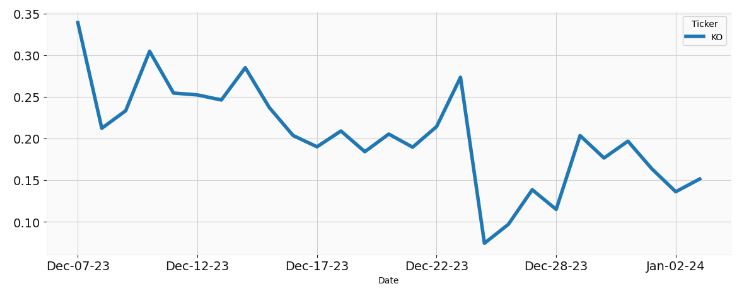

- Stock Price Forecasting – 2. KO

- FinTech Sentiment Analysis

- Discussion

- Conclusions

- Hands-On TSA(F) Tutorials

- Explore More

Introduction

- TSF is a data science technique that utilizes historical and current data to predict future values over a period of time or a specific point in the future. By analyzing data that we stored in the past, we can make informed decisions that can guide our business strategy and help us understand future trends.

- The most crucial step when considering TSF is understanding your data model and knowing which business questions need to be answered using this data.

- Here, TSA techniques come in handy. TSA isn’t about predicting the future; instead, it’s about understanding the past. It allows developers to decompose data into its constituent parts – trend, seasonality, and residual components. This can help identify any anomalies or shifts in the pattern over time.

- There are three types of TSF: univariate, bivariate, and multivariate forecasting.

- TSF can broadly be categorized into the following categories: statistical models, ML, and Deep Learning (DL).

- We will follow the following 4 steps of TSF: (1) Choosing the desired level of accuracy; (2) defining the business goal(s); (3) time series data mining and TSA; (4) how often model output needed.

- Some common business applications of TSF are predicting the weather, forecasting stock price changes, demand prediction, macro-economic planning, etc.

Random Simulation Tests

- We begin mastering TSF with Autoregressive (AR) Models.

- Let’s set the working directory YOURPATH, import key libraries, simulate stock data as a random sequence, and plot the data

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Generate a random time series data

np.random.seed(123)

n_samples = 100

time = pd.date_range('2023-01-01', periods=n_samples, freq='D')

data = np.random.normal(0, 1, n_samples).cumsum()

# Create a DataFrame with the time series data

df = pd.DataFrame({'Time': time, 'Data': data})

df.set_index('Time', inplace=True)

# Plot the time series data

plt.figure(figsize=(10, 4))

plt.plot(df.index, df['Data'])

plt.xlabel('Time')

plt.ylabel('Data')

plt.title('Example Time Series Data')

plt.show()

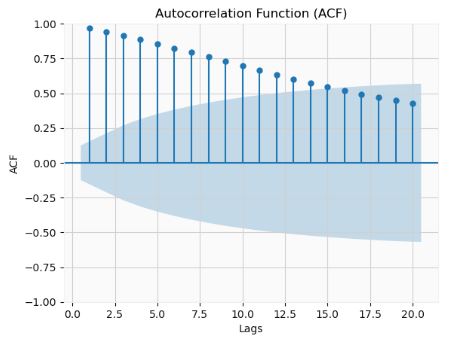

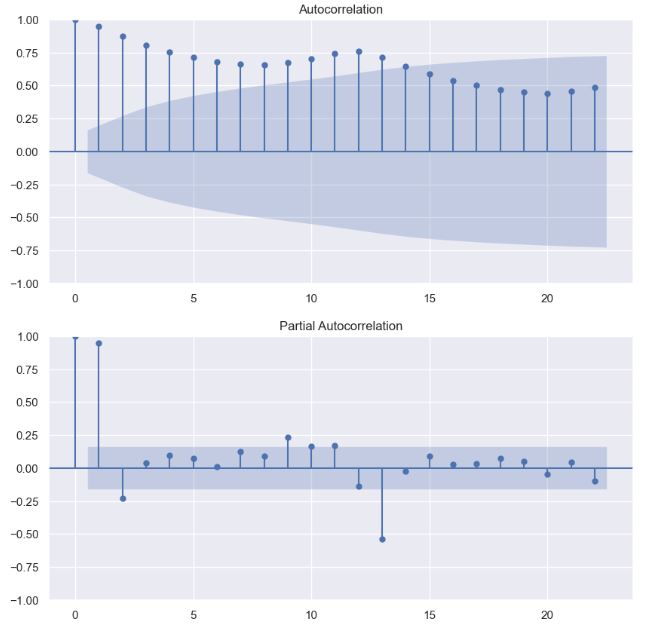

- Plotting ACF

from statsmodels.graphics.tsaplots import plot_acf

# ACF plot

plot_acf(df['Data'], lags=20, zero=False)

plt.xlabel('Lags')

plt.ylabel('ACF')

plt.title('Autocorrelation Function (ACF)')

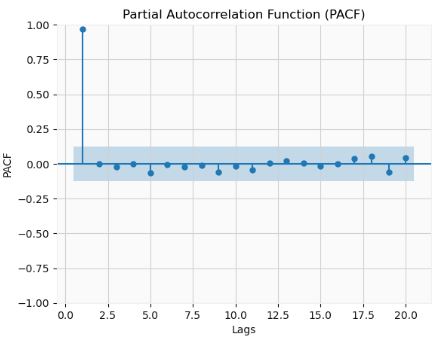

- Plotting PACF

from statsmodels.graphics.tsaplots import plot_pacf

plot_pacf(df['Data'], lags=20, zero=False)

plt.xlabel('Lags')

plt.ylabel('PACF')

plt.title('Partial Autocorrelation Function (PACF)')

- We can see that ACF is gradually declining with lags. The PACF has 1 significant lag and gradually falling ACF. This means that the data is and AR(1) process.

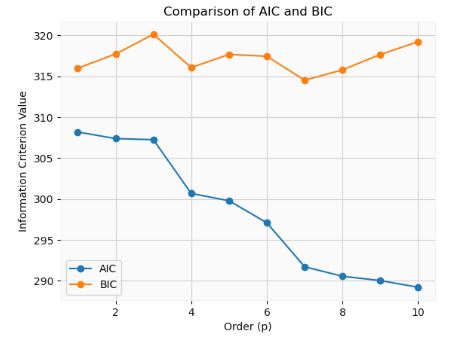

- Fitting AutoReg models with different orders and comparing AIC and BIC

from statsmodels.tsa.ar_model import AutoReg

max_order = 10

aic_values = []

bic_values = []

for p in range(1, max_order + 1):

model = AutoReg(data, lags=p)

result = model.fit()

aic_values.append(result.aic)

bic_values.append(result.bic)

# Plot AIC and BIC values

order = range(1, max_order + 1)

plt.plot(order, aic_values, marker='o', label='AIC')

plt.plot(order, bic_values, marker='o', label='BIC')

plt.xlabel('Order (p)')

plt.ylabel('Information Criterion Value')

plt.title('Comparison of AIC and BIC')

plt.legend()

plt.show()

- The model with the lowest AIC or BIC value is often considered the best-fitting model.

- By examining the Ljung-Box test results for different lags, we can determine the appropriate order (p)

import numpy as np

from statsmodels.tsa.ar_model import AutoReg

from statsmodels.stats.diagnostic import acorr_ljungbox

max_order = 10

p_values = []

for p in range(1, max_order + 1):

model = AutoReg(data, lags=p)

result = model.fit()

residuals = result.resid

result = acorr_ljungbox(residuals, lags=[p])

p_value = result.iloc[0,1]

p_values.append(p_value)

# Find the lag order with non-significant autocorrelation

threshold = 0.05

selected_order = np.argmax(np.array(p_values) < threshold) + 1

print("P Values: ", p_values)

print("Selected Order (p):", selected_order)

P Values: [0.6768877467795985, 0.9665450680852156, 0.2666153891802318, 0.9449353921040547, 0.9017991400094321, 0.9970732878539437, 0.9995994991323243, 0.9978831036372233, 0.986794476112608, 0.9813761718751872]

Selected Order (p): 1

- Cross-validation is another technique for determining the appropriate order (p)

import numpy as np

from statsmodels.tsa.ar_model import AutoReg

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import TimeSeriesSplit

np.random.seed(123)

data = np.random.normal(size=100)

max_order = 9

best_order = None

best_mse = np.inf

tscv = TimeSeriesSplit(n_splits=5)

for p in range(1, max_order + 1):

mse_scores = []

for train_index, test_index in tscv.split(data):

train_data, test_data = data[train_index], data[test_index]

model = AutoReg(train_data, lags=p)

result = model.fit()

predictions = result.predict(start=len(train_data), end=len(train_data) + len(test_data) - 1)

mse = mean_squared_error(test_data, predictions)

mse_scores.append(mse)

avg_mse = np.mean(mse_scores)

if avg_mse < best_mse:

best_mse = avg_mse

best_order = p

print("Best Lag Order (p):", best_order)

Best Lag Order (p): 3

- Here, we choose the lag order (p) that yields the best average performance across the folds.

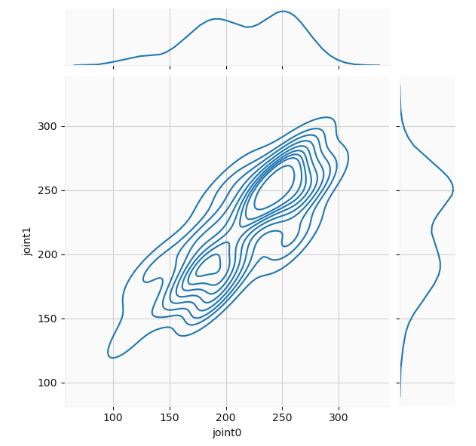

- Let’s look at a joint distribution of the time series data. If a time series is stationary, then its joint distribution with its lags should be time-invariant. In other words, the distribution should not change as the time index changes.

import seaborn as sns

lag = 10

# stack them into 2D arr

random_process=data1['Close']

joint = np.vstack([random_process[:-lag], random_process[lag:]])

joint0=joint[0]

joint1=joint[1]

df0 = pd.DataFrame({'joint0': joint[0], 'joint1': joint[1]})

sns.jointplot(data=df0, x='joint0', y='joint1', kind="kde")

- The joint distribution calculates the likelihood of two events occurring at the same time. A time series represents one possible outcome of a random process that can be completely characterized by its full joint probability distribution, which encompasses all possible combinations of values that the random process can take over an infinite period of time.

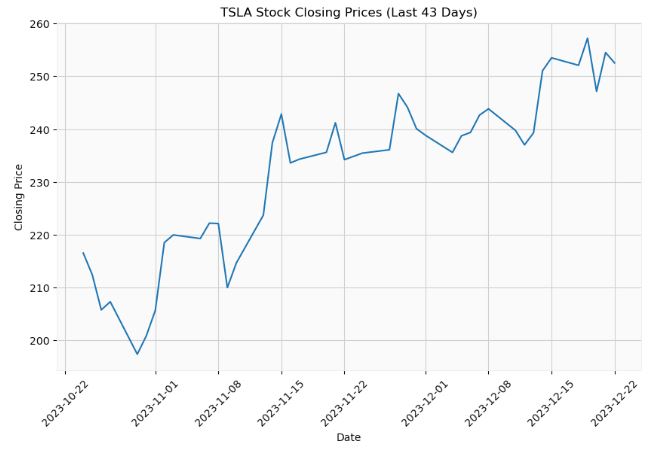

TSLA Stock 43 Days

- Let’s apply the above AR approach to the actual TSLA Stock Closing Prices (Last 43 Days)

import datetime

import numpy as np

import yfinance as yf

import matplotlib.pyplot as plt

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import TimeSeriesSplit

from statsmodels.tsa.ar_model import AutoReg

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.stats.diagnostic import acorr_ljungbox

ticker = "TSLA"

end_date = datetime.datetime.now().date()

start_date = end_date - datetime.timedelta(days=60)

data3 = yf.download(ticker, start=start_date, end=end_date)

closing_prices = data3["Close"]

print(len(closing_prices))

[*********************100%%**********************] 1 of 1 completed

43

plt.figure(figsize=(10, 6))

plt.plot(closing_prices)

plt.title("TSLA Stock Closing Prices (Last 43 Days)")

plt.xlabel("Date")

plt.ylabel("Closing Price")

plt.xticks(rotation=45)

plt.grid(True)

plt.show()

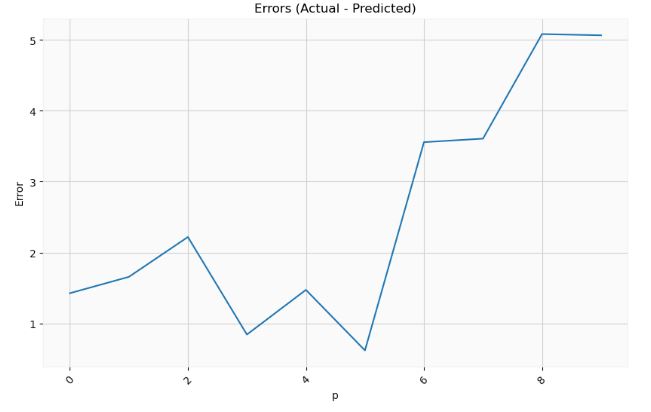

- Let’s create the 1-day AR(p) forecast as a function of p

n_test = 1

train_data = closing_prices[:len(closing_prices)-n_test]

test_data = closing_prices[len(closing_prices)-n_test:]

print(test_data)

Date

2023-12-22 252.539993

Name: Close, dtype: float64

error_list = []

for i in range(1,11):

model = AutoReg(train_data, lags=i)

model_fit = model.fit()

predicted_price = float(model_fit.predict(start=len(train_data), end=len(train_data)))

actual_price = test_data.iloc[0]

error_list.append(abs(actual_price - predicted_price))

plt.figure(figsize=(10, 6))

plt.plot(error_list)

plt.title("Errors (Actual - Predicted)")

plt.xlabel("p")

plt.ylabel("Error")

plt.xticks(rotation=45)

plt.grid(True)

plt.show()

- It is clear that the optimal p-value is p=5.

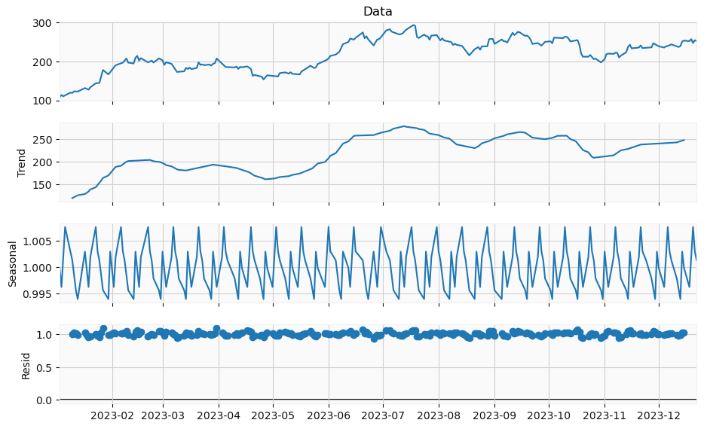

- Implementing the statsmodels seasonal decomposition of our time series data. This decomposition separates a time series into three distinct components: trend, seasonality, and residual (or irregular) component. Understanding these components helps in understanding underlying patterns in the data, forecasting, and making business or economic decisions.

import numpy as np

import pandas as pd

from statsmodels.tsa.seasonal import seasonal_decompose

y = pd.Series(df["Data"], df.index)

result = seasonal_decompose(y, model='multiplicative',period=10)

fig=result.plot()

fig.set_size_inches((10, 6))

- Performing the ADF test of stationarity

from statsmodels.tsa.stattools import adfuller

ts_stationary=pd.Series(data=y, index=df.index)

result = adfuller(ts_stationary)

print(result)

print('ADF Statistic: %f' % result[0])

print('p-value: %f' % result[1])

(-2.4007209950719894, 0.14153301655714257, 4, 241, {'1%': -3.4577787098622674, '5%': -2.873608704758507, '10%': -2.573201765981991}, 1549.8412743269414)

ADF Statistic: -2.400721

p-value: 0.141533

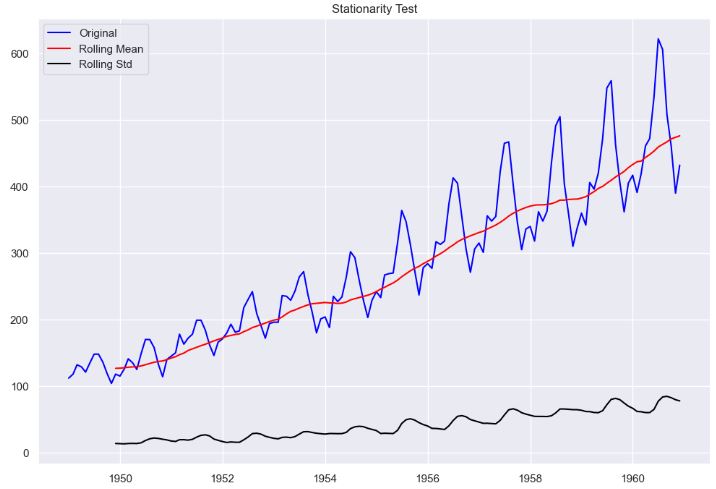

- Since the p-value is higher than 0.05 significance level, we can accept the null hypothesis, and the time series is not stationary.

- Let’s check the stability of the model over time by computing the rolling mean and variance

rolling_mean_s = ts_stationary.rolling(window=5).mean()

rolling_var_s = ts_stationary.rolling(window=5).var()

plt.plot(rolling_mean_s, label="Rolling Mean")

plt.plot(rolling_var_s, label="Rolling Variance")

plt.legend(loc="best")

plt.title("Rollings Stationary")

plt.show()

- Performing the KPSS test of stationarity. This test figures out if a time series is stationary around a mean or linear trend, or is non-stationary due to a unit root. A stationary time series is one where statistical properties – like the mean and variance – are constant over time.

from statsmodels.tsa.stattools import kpss

result = kpss(ts_stationary, regression='c')

print('KPSS Statistic: %f' % result[0])

print('p-value: %f' % result[1])

KPSS Statistic: 1.385231

p-value: 0.010000

- Here, a p-value of 0.01 (1%) would cause the null hypothesis to be rejected at an alpha level of 0.05 (5%).

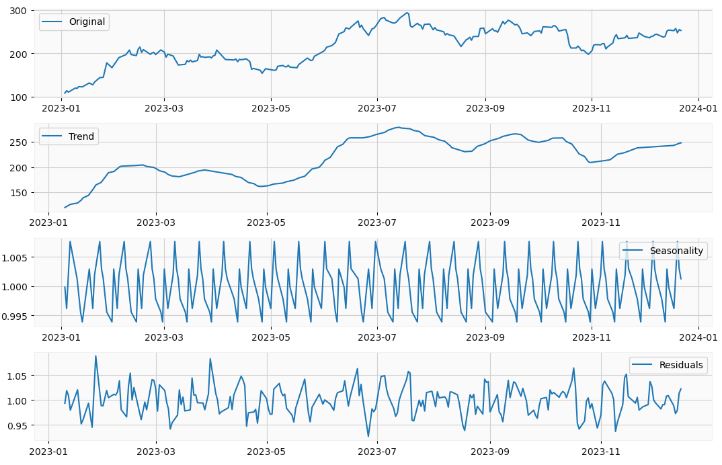

- Seasonal-Trend decomposition using LOESS (STL)

from statsmodels.tsa.seasonal import STL

result = STL(mydata, period=12, seasonal=7, robust=True).fit()

plt.figure(figsize=(11, 7))

plt.subplot(411)

plt.plot(mydata, label='Original')

plt.legend(loc='best')

plt.subplot(412)

plt.plot(result.trend, label='Trend')

plt.legend(loc='best')

plt.subplot(413)

plt.plot(result.seasonal,label='Seasonality')

plt.legend(loc='best')

plt.subplot(414)

plt.plot(result.resid, label='Residuals')

plt.legend(loc='best')

plt.tight_layout()

plt.show()

- Loess is not a decomposition method, but rather a smoothing method. The STL algorithm uses the Loess algorithm as a step in computing the seasonal decomposition.

TSLA Stock 300 Days

- Let’s use yfinance to download the TSLA stock data with days=300 and interval=’1h’

import ta

import talib

import yfinance as yf

import mplfinance as mpf

import matplotlib.pyplot as plt

from datetime import datetime, timedelta

ticker = "TSLA"

end_date = datetime.today().strftime('%Y-%m-%d')

start_date = (datetime.today() - timedelta(days=300)).strftime('%Y-%m-%d')

data = yf.download(ticker, start=start_date, end=end_date, interval='1h')

[*********************100%***********************] 1 of 1 completed

mpf.plot(data, type='candle', volume=True, style='yahoo')

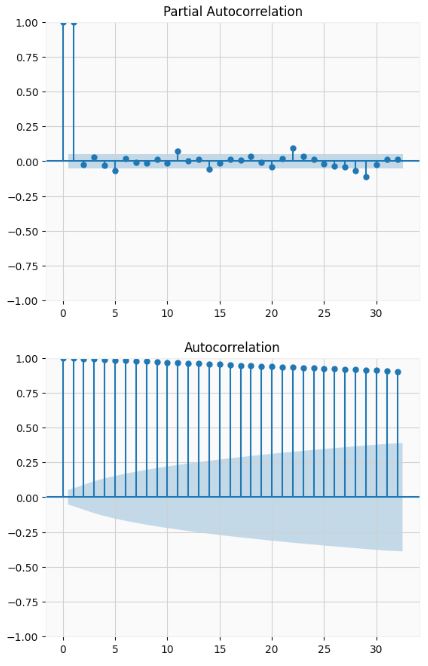

- Importing key libraries and plotting PACF/ACF of Close Price

from statsmodels.graphics.tsaplots import plot_pacf

from statsmodels.graphics.tsaplots import plot_acf

from statsmodels.tsa.statespace.sarimax import SARIMAX

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from statsmodels.tsa.stattools import adfuller

import matplotlib.pyplot as plt

from tqdm import tqdm_notebook

import numpy as np

import pandas as pd

from itertools import product

import warnings

warnings.filterwarnings('ignore')

%matplotlib inline

plot_pacf(data['Close']);

plot_acf(data['Close']);

- The ADF test confirms that the dataset is not stationary

# Augmented Dickey-Fuller test

ad_fuller_result = adfuller(data['Close'])

print(f'ADF Statistic: {ad_fuller_result[0]}')

print(f'p-value: {ad_fuller_result[1]}')

ADF Statistic: -1.5485859095622545

p-value: 0.5093544755020373

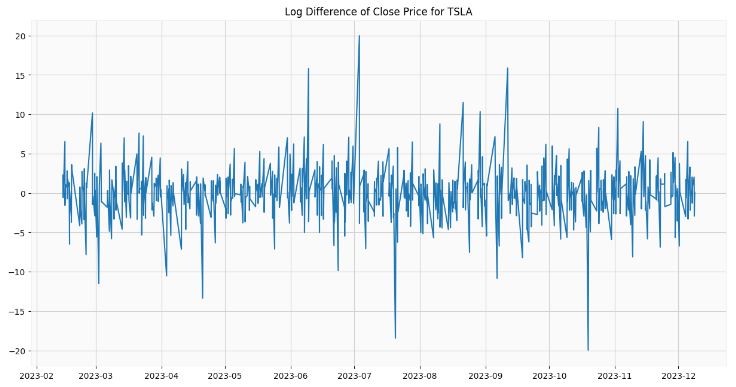

- Taking the log-domain 1st difference transformation to make the data stationary

data['data'] = np.log(data['Close'])

data['data'] = data['Close'].diff()

data = data.drop(data.index[0])

plt.figure(figsize=[15, 7.5]);

plt.plot(data['data'])

plt.title("Log Difference of Close Price for TSLA")

plt.show()

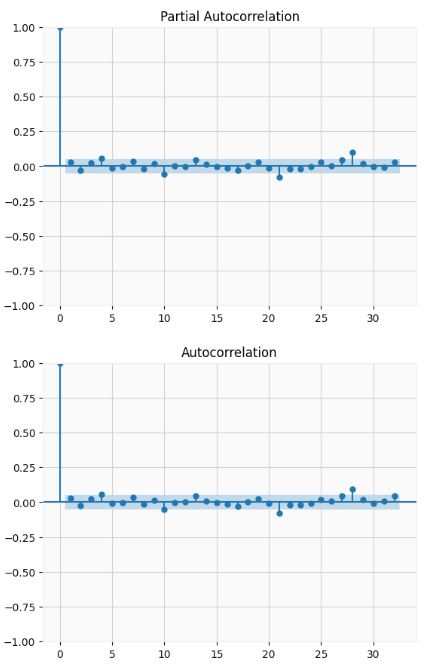

- Both the ADF test and PACF/ACF confirm that the transformed dataset is stationary

ad_fuller_result = adfuller(data['data'])

print(f'ADF Statistic: {ad_fuller_result[0]}')

print(f'p-value: {ad_fuller_result[1]}')

ADF Statistic: -17.738476868990166

p-value: 3.410415880267577e-30

plot_pacf(data['data']);

plot_acf(data['data']);

- Optimizing the SARIMAX model parameters

def optimize_SARIMA(parameters_list, d, D, s, exog):

"""

Return dataframe with parameters, corresponding AIC and SSE

parameters_list - list with (p, q, P, Q) tuples

d - integration order

D - seasonal integration order

s - length of season

exog - the exogenous variable

"""

results = []

for param in tqdm_notebook(parameters_list):

try:

model = SARIMAX(exog, order=(param[0], d, param[1]), seasonal_order=(param[2], D, param[3], s)).fit(disp=-1)

except:

continue

aic = model.aic

results.append([param, aic])

result_df = pd.DataFrame(results)

result_df.columns = ['(p,q)x(P,Q)', 'AIC']

#Sort in ascending order, lower AIC is better

result_df = result_df.sort_values(by='AIC', ascending=True).reset_index(drop=True)

return result_df

p = range(0, 4, 1)

d = 1

q = range(0, 4, 1)

P = range(0, 4, 1)

D = 1

Q = range(0, 4, 1)

s = 4

parameters = product(p, q, P, Q)

parameters_list = list(parameters)

print(len(parameters_list))

256

result_df = optimize_SARIMA(parameters_list, 1, 1, 4, data['data'])

result_df

0%| | 0/256 [00:00<?, ?it/s]

(p,q)x(P,Q) AIC

0 (3, 3, 0, 0) 14.000000

1 (1, 2, 0, 2) 6838.178237

2 (1, 2, 1, 1) 6838.344379

3 (0, 1, 2, 3) 6839.006923

4 (0, 1, 3, 3) 6839.726108

... ... ...

251 (2, 0, 0, 0) 8147.031496

252 (0, 0, 2, 0) 8201.217015

253 (1, 0, 0, 0) 8307.942745

254 (0, 0, 1, 0) 8362.245368

255 (0, 0, 0, 0) 8688.024189

256 rows × 2 columns

best_model = SARIMAX(data['data'], order=(3, 3, 0)).fit(dis=-1)

print(best_model.summary())

SARIMAX Results

==============================================================================

Dep. Variable: data No. Observations: 1450

Model: SARIMAX(3, 3, 0) Log Likelihood -4440.140

Date: Sun, 10 Dec 2023 AIC 8888.280

Time: 13:36:39 BIC 8909.389

Sample: 0 HQIC 8896.158

- 1450

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 -1.4624 0.020 -74.995 0.000 -1.501 -1.424

ar.L2 -1.1894 0.029 -41.353 0.000 -1.246 -1.133

ar.L3 -0.5277 0.023 -23.438 0.000 -0.572 -0.484

sigma2 27.0414 0.746 36.225 0.000 25.578 28.505

===================================================================================

Ljung-Box (L1) (Q): 82.80 Jarque-Bera (JB): 780.60

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 1.45 Skew: -0.07

Prob(H) (two-sided): 0.00 Kurtosis: 6.60

===================================================================================

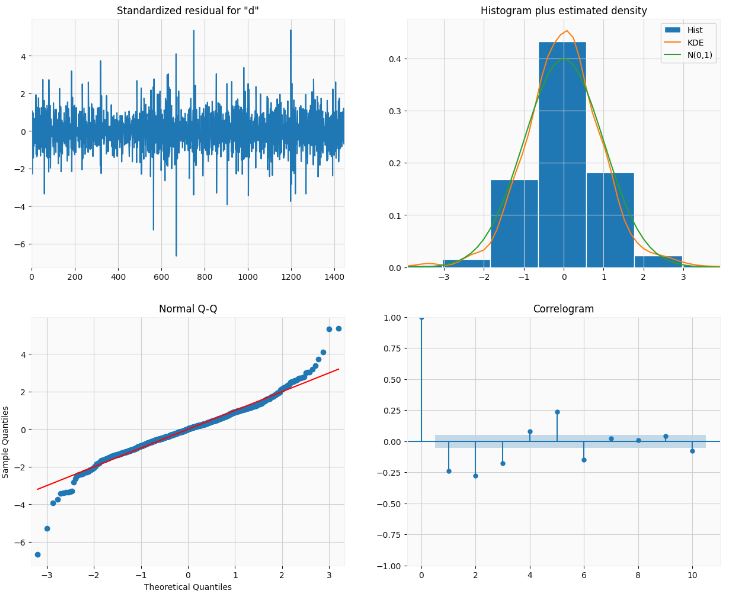

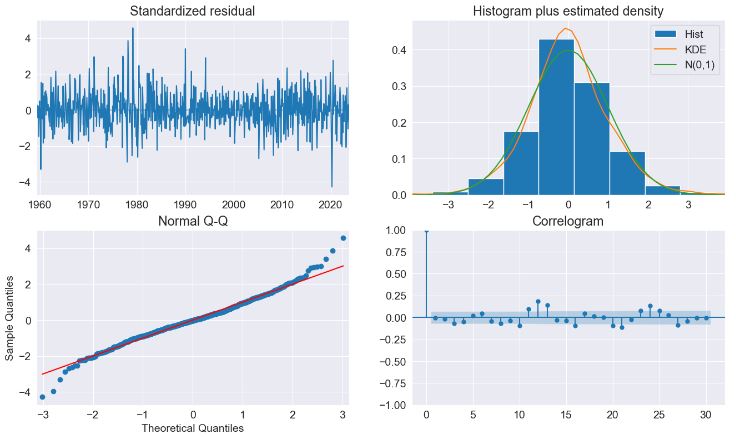

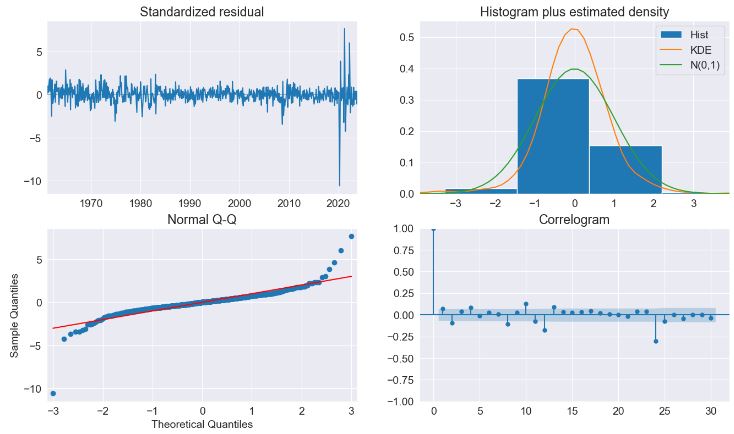

- Plotting the best SARIMAX model diagnostics

best_model.plot_diagnostics(figsize=(15,12));

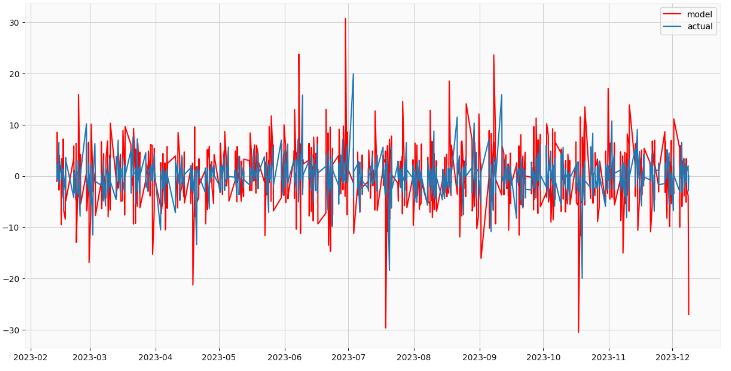

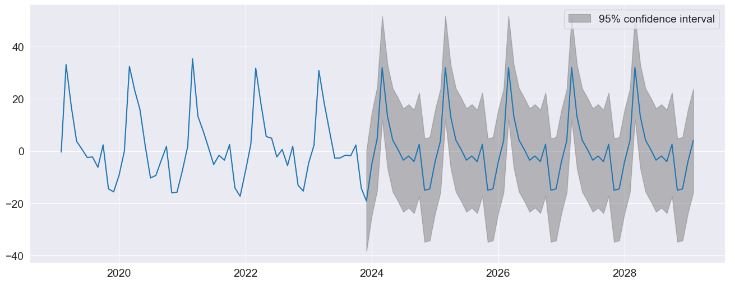

- Creating and plotting the best SARIMAX model forecast

data['arima_model'] = best_model.fittedvalues

data['arima_model'][:4+1] = np.NaN

forecast = best_model.predict(start=data.shape[0], end=data.shape[0] + 8)

forecast = data['arima_model'].append(forecast)

forecast1=forecast[9:]

df = pd.DataFrame({'Time': data.index, 'Data': forecast1})

df.set_index('Time', inplace=True)

plt.figure(figsize=(15, 7.5))

plt.plot(data.index,forecast1, color='r', label='model')

plt.plot(data.index,data['data'], label='actual')

plt.legend()

plt.show()

Housing in the United States

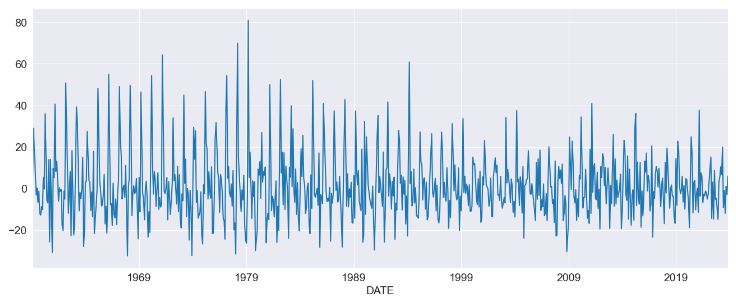

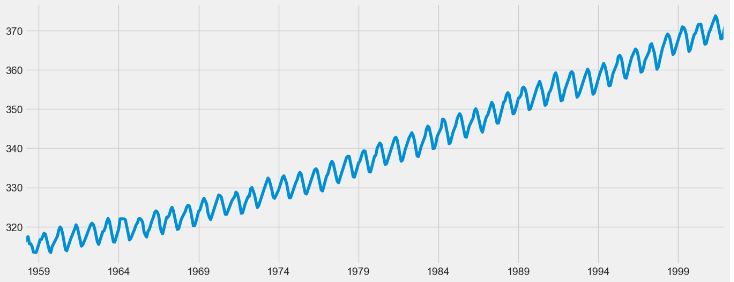

- Let’s apply the AR approach to the month-over-month growth rate in U.S. Housing

%matplotlib inline

import matplotlib.pyplot as plt

import pandas as pd

import pandas_datareader as pdr

import seaborn as sns

from statsmodels.tsa.api import acf, graphics, pacf

from statsmodels.tsa.ar_model import AutoReg, ar_select_order

sns.set_style("darkgrid")

pd.plotting.register_matplotlib_converters()

# Default figure size

sns.mpl.rc("figure", figsize=(16, 6))

sns.mpl.rc("font", size=14)

data = pdr.get_data_fred("HOUSTNSA", "1959-01-01", "2023-12-24")

housing = data.HOUSTNSA.pct_change().dropna()

# Scale by 100 to get percentages

housing = 100 * housing.asfreq("MS")

fig, ax = plt.subplots()

ax = housing.plot(ax=ax)

- Let’s examine the AutoReg Model Results

mod = AutoReg(housing, 3, old_names=False)

res = mod.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 778

Model: AutoReg(3) Log Likelihood -3198.885

Method: Conditional MLE S.D. of innovations 15.009

Date: Sat, 23 Dec 2023 AIC 6407.770

Time: 13:26:45 BIC 6431.034

Sample: 05-01-1959 HQIC 6416.720

- 11-01-2023

===============================================================================

coef std err z P>|z| [0.025 0.975]

-------------------------------------------------------------------------------

const 1.0998 0.543 2.027 0.043 0.036 2.163

HOUSTNSA.L1 0.1835 0.035 5.211 0.000 0.114 0.253

HOUSTNSA.L2 0.0080 0.036 0.223 0.823 -0.062 0.078

HOUSTNSA.L3 -0.1950 0.035 -5.549 0.000 -0.264 -0.126

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 0.9659 -1.3337j 1.6467 -0.1502

AR.2 0.9659 +1.3337j 1.6467 0.1502

AR.3 -1.8908 -0.0000j 1.8908 -0.5000

-----------------------------------------------------------------------------

sel = ar_select_order(housing, 13, old_names=False)

sel.ar_lags

res = sel.model.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 778

Model: AutoReg(13) Log Likelihood -2886.312

Method: Conditional MLE S.D. of innovations 10.528

Date: Sat, 23 Dec 2023 AIC 5802.624

Time: 13:26:51 BIC 5872.222

Sample: 03-01-1960 HQIC 5829.417

- 11-01-2023

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

const 1.4561 0.448 3.250 0.001 0.578 2.334

HOUSTNSA.L1 -0.2665 0.035 -7.710 0.000 -0.334 -0.199

HOUSTNSA.L2 -0.0833 0.031 -2.699 0.007 -0.144 -0.023

HOUSTNSA.L3 -0.0880 0.031 -2.861 0.004 -0.148 -0.028

HOUSTNSA.L4 -0.1724 0.031 -5.623 0.000 -0.233 -0.112

HOUSTNSA.L5 -0.0450 0.031 -1.447 0.148 -0.106 0.016

HOUSTNSA.L6 -0.0907 0.031 -2.963 0.003 -0.151 -0.031

HOUSTNSA.L7 -0.0715 0.031 -2.330 0.020 -0.132 -0.011

HOUSTNSA.L8 -0.1584 0.031 -5.174 0.000 -0.218 -0.098

HOUSTNSA.L9 -0.0898 0.031 -2.887 0.004 -0.151 -0.029

HOUSTNSA.L10 -0.1111 0.031 -3.627 0.000 -0.171 -0.051

HOUSTNSA.L11 0.1036 0.031 3.370 0.001 0.043 0.164

HOUSTNSA.L12 0.5028 0.031 16.303 0.000 0.442 0.563

HOUSTNSA.L13 0.2961 0.035 8.571 0.000 0.228 0.364

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 1.1036 -0.0000j 1.1036 -0.0000

AR.2 0.8751 -0.5032j 1.0095 -0.0831

AR.3 0.8751 +0.5032j 1.0095 0.0831

AR.4 0.5052 -0.8782j 1.0132 -0.1669

AR.5 0.5052 +0.8782j 1.0132 0.1669

AR.6 0.0126 -1.0588j 1.0589 -0.2481

AR.7 0.0126 +1.0588j 1.0589 0.2481

AR.8 -0.5285 -0.9382j 1.0768 -0.3316

AR.9 -0.5285 +0.9382j 1.0768 0.3316

AR.10 -0.9602 -0.5903j 1.1271 -0.4123

AR.11 -0.9602 +0.5903j 1.1271 0.4123

AR.12 -1.3050 -0.2611j 1.3309 -0.4686

AR.13 -1.3050 +0.2611j 1.3309 0.4686

------------------------------------------------------------------------------

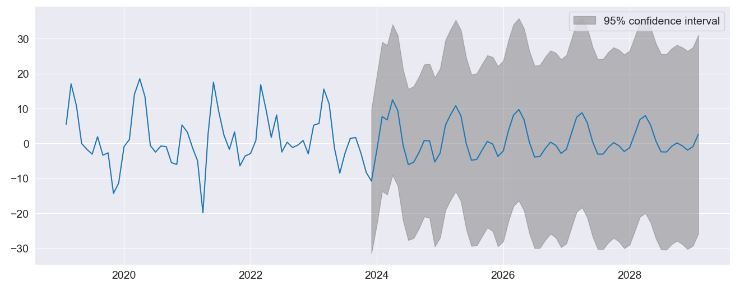

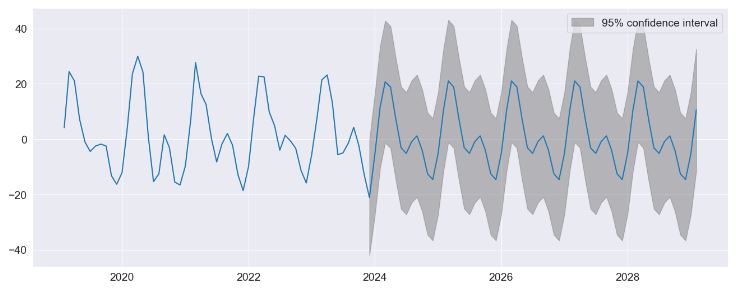

- Performing predictions to show the string seasonality captured by the model with 95% confidence interval

fig = res.plot_predict(720, 840)

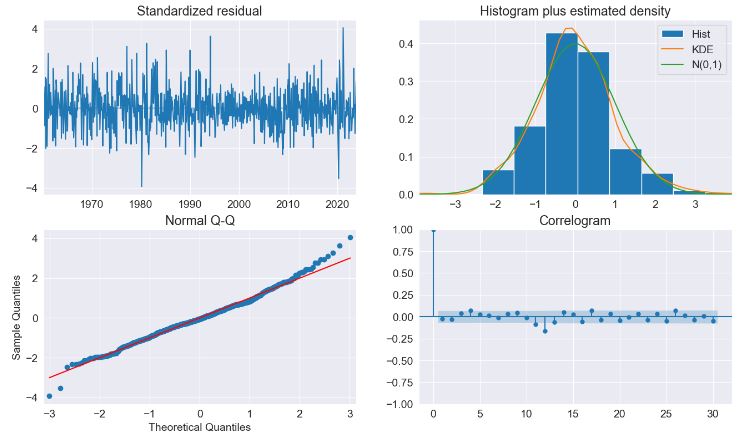

- The key diagnostics plot indicates that the model captures the key features in the data

fig = plt.figure(figsize=(16, 9))

fig = res.plot_diagnostics(fig=fig, lags=30)

- Testing model predictions with seasonal dummies

sel = ar_select_order(housing, 13, seasonal=True, old_names=False)

sel.ar_lags

res = sel.model.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 778

Model: Seas. AutoReg(2) Log Likelihood -2871.089

Method: Conditional MLE S.D. of innovations 9.786

Date: Sat, 23 Dec 2023 AIC 5772.178

Time: 13:27:10 BIC 5841.991

Sample: 04-01-1959 HQIC 5799.036

- 11-01-2023

===============================================================================

coef std err z P>|z| [0.025 0.975]

-------------------------------------------------------------------------------

const 1.5571 1.348 1.155 0.248 -1.085 4.199

s(2,12) 30.9672 1.806 17.149 0.000 27.428 34.506

s(3,12) 19.9295 2.332 8.545 0.000 15.358 24.501

s(4,12) 9.0602 2.561 3.537 0.000 4.040 14.080

s(5,12) 1.3026 2.041 0.638 0.523 -2.697 5.303

s(6,12) -4.5037 1.868 -2.411 0.016 -8.164 -0.843

s(7,12) -4.2775 1.806 -2.369 0.018 -7.816 -0.739

s(8,12) -6.3883 1.773 -3.604 0.000 -9.862 -2.914

s(9,12) -0.1806 1.781 -0.101 0.919 -3.670 3.309

s(10,12) -16.3239 1.790 -9.120 0.000 -19.832 -12.816

s(11,12) -19.4906 1.849 -10.542 0.000 -23.114 -15.867

s(12,12) -10.6999 1.771 -6.042 0.000 -14.171 -7.229

HOUSTNSA.L1 -0.2472 0.036 -6.903 0.000 -0.317 -0.177

HOUSTNSA.L2 -0.0994 0.036 -2.776 0.005 -0.170 -0.029

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -1.2430 -2.9173j 3.1710 -0.3141

AR.2 -1.2430 +2.9173j 3.1710 0.3141

-----------------------------------------------------------------------------

fig = res.plot_predict(720, 840)

fig = plt.figure(figsize=(16, 9))

fig = res.plot_diagnostics(lags=30, fig=fig)

- Implementing the Custom Deterministic Process. This allows for more complex deterministic terms to be constructed, for example one that includes seasonal components with two periods, or one that uses a Fourier series rather than seasonal dummies

from statsmodels.tsa.deterministic import DeterministicProcess

dp = DeterministicProcess(housing.index, constant=True, period=12, fourier=2)

mod = AutoReg(housing, 2, trend="n", seasonal=False, deterministic=dp)

res = mod.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 778

Model: AutoReg(2) Log Likelihood -2935.525

Method: Conditional MLE S.D. of innovations 10.633

Date: Sat, 23 Dec 2023 AIC 5887.049

Time: 13:29:17 BIC 5924.283

Sample: 04-01-1959 HQIC 5901.373

- 11-01-2023

===============================================================================

coef std err z P>|z| [0.025 0.975]

-------------------------------------------------------------------------------

const 1.6591 0.387 4.289 0.000 0.901 2.417

sin(1,12) 15.3251 0.818 18.732 0.000 13.722 16.929

cos(1,12) 4.8543 0.578 8.396 0.000 3.721 5.987

sin(2,12) 11.8657 0.605 19.628 0.000 10.681 13.051

cos(2,12) 0.0660 0.717 0.092 0.927 -1.339 1.471

HOUSTNSA.L1 -0.3403 0.036 -9.571 0.000 -0.410 -0.271

HOUSTNSA.L2 -0.1497 0.036 -4.212 0.000 -0.219 -0.080

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -1.1364 -2.3210j 2.5843 -0.3225

AR.2 -1.1364 +2.3210j 2.5843 0.3225

-----------------------------------------------------------------------------

fig = res.plot_predict(720, 840)

Industrial Production

- Let’s apply the AR forecasting to the industrial production index data

data = pdr.get_data_fred("INDPRO", "1959-01-01", "2023-12-24")

ind_prod = data.INDPRO.pct_change(12).dropna().asfreq("MS")

_, ax = plt.subplots(figsize=(16, 9))

ind_prod.plot(ax=ax)

sel = ar_select_order(ind_prod, 13, "bic", old_names=False)

res = sel.model.fit()

print(res.summary())

ind_prod.shape

(767,)

fig = res_glob.plot_predict(start=766, end=784)

res_ar5 = AutoReg(ind_prod, 5, old_names=False).fit()

predictions = pd.DataFrame(

{

"AR(5)": res_ar5.predict(start=766, end=784),

"AR(13)": res.predict(start=766, end=784),

"Restr. AR(13)": res_glob.predict(start=766, end=784),

}

)

_, ax = plt.subplots()

ax = predictions.plot(ax=ax)

AutoReg Model Results

==============================================================================

Dep. Variable: INDPRO No. Observations: 767

Model: AutoReg(13) Log Likelihood 2293.864

Method: Conditional MLE S.D. of innovations 0.012

Date: Sat, 23 Dec 2023 AIC -4557.727

Time: 13:28:11 BIC -4488.347

Sample: 02-01-1961 HQIC -4531.000

- 11-01-2023

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0015 0.001 2.940 0.003 0.001 0.003

INDPRO.L1 1.2122 0.034 35.403 0.000 1.145 1.279

INDPRO.L2 -0.3039 0.054 -5.589 0.000 -0.411 -0.197

INDPRO.L3 0.1038 0.055 1.889 0.059 -0.004 0.211

INDPRO.L4 0.0310 0.055 0.562 0.574 -0.077 0.139

INDPRO.L5 -0.0866 0.055 -1.578 0.115 -0.194 0.021

INDPRO.L6 0.0501 0.055 0.918 0.359 -0.057 0.157

INDPRO.L7 -0.0037 0.055 -0.067 0.946 -0.111 0.103

INDPRO.L8 -0.0894 0.054 -1.641 0.101 -0.196 0.017

INDPRO.L9 0.1202 0.055 2.205 0.027 0.013 0.227

INDPRO.L10 0.0097 0.055 0.177 0.859 -0.097 0.117

INDPRO.L11 -0.1255 0.054 -2.304 0.021 -0.232 -0.019

INDPRO.L12 -0.3056 0.053 -5.719 0.000 -0.410 -0.201

INDPRO.L13 0.3295 0.033 9.946 0.000 0.265 0.394

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 -1.0884 -0.3009j 1.1292 -0.4571

AR.2 -1.0884 +0.3009j 1.1292 0.4571

AR.3 -0.8108 -0.8184j 1.1520 -0.3743

AR.4 -0.8108 +0.8184j 1.1520 0.3743

AR.5 -0.2810 -1.0316j 1.0692 -0.2923

AR.6 -0.2810 +1.0316j 1.0692 0.2923

AR.7 0.2883 -1.0171j 1.0572 -0.2060

AR.8 0.2883 +1.0171j 1.0572 0.2060

AR.9 0.7786 -0.7401j 1.0743 -0.1210

AR.10 0.7786 +0.7401j 1.0743 0.1210

AR.11 1.0384 -0.2257j 1.0627 -0.0341

AR.12 1.0384 +0.2257j 1.0627 0.0341

AR.13 1.0771 -0.0000j 1.0771 -0.0000

------------------------------------------------------------------------------

- The diagnostics indicate the model captures most of the the dynamics in the data. The correlogram shows a patters at the seasonal frequency and so a more complete seasonal model (

SARIMAX) may be needed. Read more here. - Let’s produce 12-step-heard forecasts for the final 24 periods in the sample. Forecasts are produced using the

predictmethod from a results instance. The default produces static forecasts which are one-step forecasts. Producing multi-step forecasts requires usingdynamic=True.

import numpy as np

start = ind_prod.index[-24]

forecast_index = pd.date_range(start, freq=ind_prod.index.freq, periods=36)

cols = ["-".join(str(val) for val in (idx.year, idx.month)) for idx in forecast_index]

forecasts = pd.DataFrame(index=forecast_index, columns=cols)

for i in range(1, 24):

fcast = res_glob.predict(

start=forecast_index[i], end=forecast_index[i + 12], dynamic=True

)

forecasts.loc[fcast.index, cols[i]] = fcast

_, ax = plt.subplots(figsize=(16, 10))

ind_prod.iloc[-24:].plot(ax=ax, color="black", linestyle="--")

ax = forecasts.plot(ax=ax)

- Comparing to SARIMAX

from statsmodels.tsa.api import SARIMAX

sarimax_mod = SARIMAX(ind_prod, order=((1, 5, 12, 13), 0, 0), trend="c")

sarimax_res = sarimax_mod.fit()

print(sarimax_res.summary())

SARIMAX Results

=========================================================================================

Dep. Variable: INDPRO No. Observations: 767

Model: SARIMAX([1, 5, 12, 13], 0, 0) Log Likelihood 2282.426

Date: Sat, 23 Dec 2023 AIC -4552.853

Time: 13:29:05 BIC -4524.998

Sample: 01-01-1960 HQIC -4542.131

- 11-01-2023

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

intercept 0.0015 0.000 3.266 0.001 0.001 0.002

ar.L1 1.0263 0.009 112.105 0.000 1.008 1.044

ar.L5 -0.0306 0.014 -2.198 0.028 -0.058 -0.003

ar.L12 -0.4697 0.010 -49.317 0.000 -0.488 -0.451

ar.L13 0.4159 0.013 32.167 0.000 0.391 0.441

sigma2 0.0002 2.24e-06 67.499 0.000 0.000 0.000

===================================================================================

Ljung-Box (L1) (Q): 34.68 Jarque-Bera (JB): 18537.97

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 1.56 Skew: -0.98

Prob(H) (two-sided): 0.00 Kurtosis: 27.01

===================================================================================

sarimax_params = sarimax_res.params.iloc[:-1].copy()

sarimax_params.index = res_glob.params.index

params = pd.concat([res_glob.params, sarimax_params], axis=1, sort=False)

params.columns = ["AutoReg", "SARIMAX"]

params

AutoReg SARIMAX

const 0.001517 0.001471

INDPRO.L1 1.172634 1.026293

INDPRO.L2 -0.183711 -0.030650

INDPRO.L12 -0.417311 -0.469672

INDPRO.L13 0.370521 0.415866

Federal Funds Rate Data

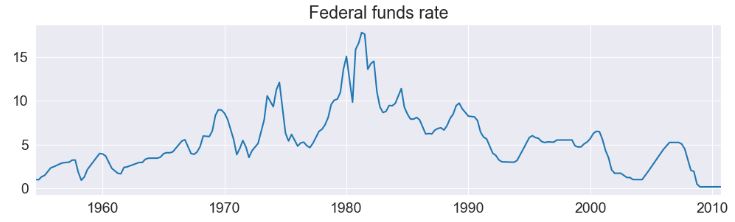

- Let’s look at an example of the use of Markov switching models in statsmodels to estimate dynamic regression models with changes in regime. Read the Stata Markov switching documentation here.

- Our first example deals with the Federal funds rate data

from statsmodels.tsa.regime_switching.tests.test_markov_regression import fedfunds

dta_fedfunds = pd.Series(

fedfunds, index=pd.date_range("1954-07-01", "2010-10-01", freq="QS")

)

# Plot the data

dta_fedfunds.plot(title="Federal funds rate", figsize=(12, 3))

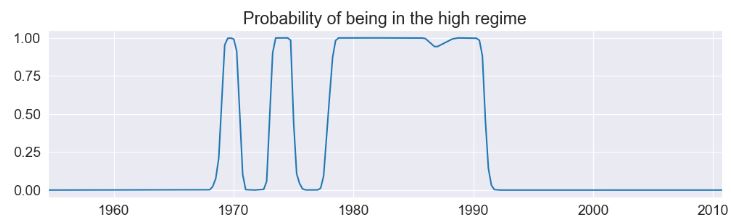

# Fit the model

# (a switching mean is the default of the MarkovRegession model)

mod_fedfunds = sm.tsa.MarkovRegression(dta_fedfunds, k_regimes=2)

res_fedfunds = mod_fedfunds.fit()

res_fedfunds.summary()

Markov Switching Model Results

Dep. Variable: y No. Observations: 226

Model: MarkovRegression Log Likelihood -508.636

Date: Sat, 23 Dec 2023 AIC 1027.272

Time: 13:29:47 BIC 1044.375

Sample: 07-01-1954 HQIC 1034.174

- 10-01-2010

Covariance Type: approx

Regime 0 parameters

coef std err z P>|z| [0.025 0.975]

const 3.7088 0.177 20.988 0.000 3.362 4.055

Regime 1 parameters

coef std err z P>|z| [0.025 0.975]

const 9.5568 0.300 31.857 0.000 8.969 10.145

Non-switching parameters

coef std err z P>|z| [0.025 0.975]

sigma2 4.4418 0.425 10.447 0.000 3.608 5.275

Regime transition parameters

coef std err z P>|z| [0.025 0.975]

p[0->0] 0.9821 0.010 94.443 0.000 0.962 1.002

p[1->0] 0.0504 0.027 1.876 0.061 -0.002 0.103

res_fedfunds.smoothed_marginal_probabilities[1].plot(

title="Probability of being in the high regime", figsize=(12, 3)

)

- The model suggests that the 1980’s was a time-period in which a high federal funds rate existed.

- From the estimated transition matrix we can calculate the expected duration of a low regime versus a high regime.

print(res_fedfunds.expected_durations)

[55.85400626 19.85506546]

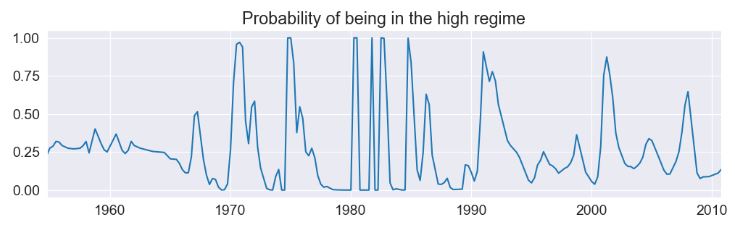

- The next example augments the previous model to include the lagged value of the federal funds rate

# Fit the model

mod_fedfunds2 = sm.tsa.MarkovRegression(

dta_fedfunds.iloc[1:], k_regimes=2, exog=dta_fedfunds.iloc[:-1]

)

res_fedfunds2 = mod_fedfunds2.fit()

res_fedfunds2.summary()

Markov Switching Model Results

Dep. Variable: y No. Observations: 225

Model: MarkovRegression Log Likelihood -264.711

Date: Sat, 23 Dec 2023 AIC 543.421

Time: 13:29:57 BIC 567.334

Sample: 10-01-1954 HQIC 553.073

- 10-01-2010

Covariance Type: approx

Regime 0 parameters

coef std err z P>|z| [0.025 0.975]

const 0.7245 0.289 2.510 0.012 0.159 1.290

x1 0.7631 0.034 22.629 0.000 0.697 0.829

Regime 1 parameters

coef std err z P>|z| [0.025 0.975]

const -0.0989 0.118 -0.835 0.404 -0.331 0.133

x1 1.0612 0.019 57.351 0.000 1.025 1.097

Non-switching parameters

coef std err z P>|z| [0.025 0.975]

sigma2 0.4783 0.050 9.642 0.000 0.381 0.576

Regime transition parameters

coef std err z P>|z| [0.025 0.975]

p[0->0] 0.6378 0.120 5.304 0.000 0.402 0.874

p[1->0] 0.1306 0.050 2.634 0.008 0.033 0.228

res_fedfunds2.smoothed_marginal_probabilities[0].plot(

title="Probability of being in the high regime", figsize=(12, 3)

)

- There are several things to notice from the summary output:

- The information criteria have decreased substantially, indicating that this model has a better fit than the previous model.

- The interpretation of the regimes, in terms of the intercept, have switched. Now the first regime has the higher intercept and the second regime has a lower intercept.

- Examining the smoothed probabilities of the high regime state, we now see quite a bit more variability.

- Finally, the expected durations of each regime have decreased quite a bit.

print(res_fedfunds2.expected_durations)

[2.76105188 7.65529154]

- Taylor rule with 2 or 3 regimes: Let’s include two additional exogenous variables – a measure of the output gap and a measure of inflation – to estimate a switching Taylor-type rule with both 2 and 3 regimes to see which fits the data better.

- Because the models can be often difficult to estimate, for the 3-regime model we employ a search over starting parameters to improve results, specifying 20 random search repetitions.

# Get the additional data

from statsmodels.tsa.regime_switching.tests.test_markov_regression import ogap, inf

dta_ogap = pd.Series(ogap, index=pd.date_range("1954-07-01", "2010-10-01", freq="QS"))

dta_inf = pd.Series(inf, index=pd.date_range("1954-07-01", "2010-10-01", freq="QS"))

exog = pd.concat((dta_fedfunds.shift(), dta_ogap, dta_inf), axis=1).iloc[4:]

# Fit the 2-regime model

mod_fedfunds3 = sm.tsa.MarkovRegression(dta_fedfunds.iloc[4:], k_regimes=2, exog=exog)

res_fedfunds3 = mod_fedfunds3.fit()

# Fit the 3-regime model

np.random.seed(12345)

mod_fedfunds4 = sm.tsa.MarkovRegression(dta_fedfunds.iloc[4:], k_regimes=3, exog=exog)

res_fedfunds4 = mod_fedfunds4.fit(search_reps=20)

res_fedfunds3.summary()

Markov Switching Model Results

Dep. Variable: y No. Observations: 222

Model: MarkovRegression Log Likelihood -229.256

Date: Sat, 23 Dec 2023 AIC 480.512

Time: 13:30:09 BIC 517.942

Sample: 07-01-1955 HQIC 495.624

- 10-01-2010

Covariance Type: approx

Regime 0 parameters

coef std err z P>|z| [0.025 0.975]

const 0.6555 0.137 4.771 0.000 0.386 0.925

x1 0.8314 0.033 24.951 0.000 0.766 0.897

x2 0.1355 0.029 4.609 0.000 0.078 0.193

x3 -0.0274 0.041 -0.671 0.502 -0.107 0.053

Regime 1 parameters

coef std err z P>|z| [0.025 0.975]

const -0.0945 0.128 -0.739 0.460 -0.345 0.156

x1 0.9293 0.027 34.309 0.000 0.876 0.982

x2 0.0343 0.024 1.429 0.153 -0.013 0.081

x3 0.2125 0.030 7.147 0.000 0.154 0.271

Non-switching parameters

coef std err z P>|z| [0.025 0.975]

sigma2 0.3323 0.035 9.526 0.000 0.264 0.401

Regime transition parameters

coef std err z P>|z| [0.025 0.975]

p[0->0] 0.7279 0.093 7.828 0.000 0.546 0.910

p[1->0] 0.2115 0.064 3.298 0.001 0.086 0.337

res_fedfunds4.summary()

Markov Switching Model Results

Dep. Variable: y No. Observations: 222

Model: MarkovRegression Log Likelihood -180.806

Date: Sat, 23 Dec 2023 AIC 399.611

Time: 13:30:11 BIC 464.262

Sample: 07-01-1955 HQIC 425.713

- 10-01-2010

Covariance Type: approx

Regime 0 parameters

coef std err z P>|z| [0.025 0.975]

const -1.0250 0.290 -3.531 0.000 -1.594 -0.456

x1 0.3277 0.086 3.812 0.000 0.159 0.496

x2 0.2036 0.049 4.152 0.000 0.107 0.300

x3 1.1381 0.081 13.977 0.000 0.978 1.298

Regime 1 parameters

coef std err z P>|z| [0.025 0.975]

const -0.0259 0.087 -0.298 0.765 -0.196 0.144

x1 0.9737 0.019 50.265 0.000 0.936 1.012

x2 0.0341 0.017 2.030 0.042 0.001 0.067

x3 0.1215 0.022 5.606 0.000 0.079 0.164

Regime 2 parameters

coef std err z P>|z| [0.025 0.975]

const 0.7346 0.130 5.632 0.000 0.479 0.990

x1 0.8436 0.024 35.198 0.000 0.797 0.891

x2 0.1633 0.025 6.515 0.000 0.114 0.212

x3 -0.0499 0.027 -1.835 0.067 -0.103 0.003

Non-switching parameters

coef std err z P>|z| [0.025 0.975]

sigma2 0.1660 0.018 9.240 0.000 0.131 0.201

Regime transition parameters

coef std err z P>|z| [0.025 0.975]

p[0->0] 0.7214 0.117 6.177 0.000 0.493 0.950

p[1->0] 4.001e-08 nan nan nan nan nan

p[2->0] 0.0783 0.038 2.079 0.038 0.004 0.152

p[0->1] 0.1044 0.095 1.103 0.270 -0.081 0.290

p[1->1] 0.8259 0.054 15.208 0.000 0.719 0.932

p[2->1] 0.2288 0.073 3.150 0.002 0.086 0.371

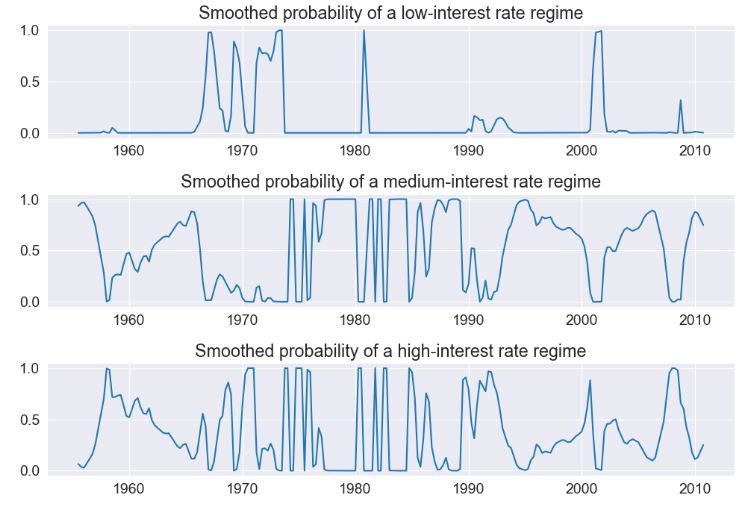

- Due to lower information criteria, we might prefer the 3-state model, with an interpretation of low-, medium-, and high-interest rate regimes. The smoothed probabilities of each regime are plotted below.

fig, axes = plt.subplots(3, figsize=(10, 7))

ax = axes[0]

ax.plot(res_fedfunds4.smoothed_marginal_probabilities[0])

ax.set(title="Smoothed probability of a low-interest rate regime")

ax = axes[1]

ax.plot(res_fedfunds4.smoothed_marginal_probabilities[1])

ax.set(title="Smoothed probability of a medium-interest rate regime")

ax = axes[2]

ax.plot(res_fedfunds4.smoothed_marginal_probabilities[2])

ax.set(title="Smoothed probability of a high-interest rate regime")

fig.tight_layout()

S&P 500 Absolute Returns

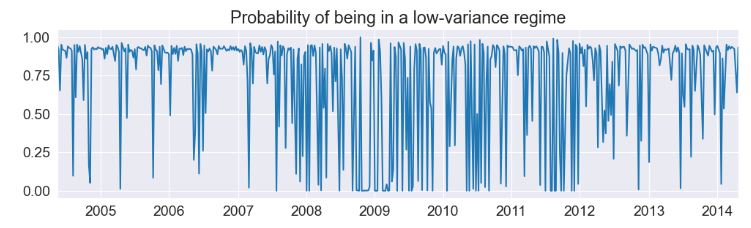

- Switching variances: We can also accommodate switching variances. The application is to absolute returns on S&P 500

from statsmodels.tsa.regime_switching.tests.test_markov_regression import areturns

dta_areturns = pd.Series(

areturns, index=pd.date_range("2004-05-04", "2014-5-03", freq="W")

)

# Plot the data

dta_areturns.plot(title="Absolute returns, S&P500", figsize=(12, 3))

# Fit the model

mod_areturns = sm.tsa.MarkovRegression(

dta_areturns.iloc[1:],

k_regimes=2,

exog=dta_areturns.iloc[:-1],

switching_variance=True,

)

res_areturns = mod_areturns.fit()

res_areturns.summary()

Markov Switching Model Results

Dep. Variable: y No. Observations: 520

Model: MarkovRegression Log Likelihood -745.798

Date: Sat, 23 Dec 2023 AIC 1507.595

Time: 13:30:35 BIC 1541.626

Sample: 05-16-2004 HQIC 1520.926

- 04-27-2014

Covariance Type: approx

Regime 0 parameters

coef std err z P>|z| [0.025 0.975]

const 0.7641 0.078 9.761 0.000 0.611 0.918

x1 0.0791 0.030 2.620 0.009 0.020 0.138

sigma2 0.3476 0.061 5.694 0.000 0.228 0.467

Regime 1 parameters

coef std err z P>|z| [0.025 0.975]

const 1.9728 0.278 7.086 0.000 1.427 2.518

x1 0.5280 0.086 6.155 0.000 0.360 0.696

sigma2 2.5771 0.405 6.357 0.000 1.783 3.372

Regime transition parameters

coef std err z P>|z| [0.025 0.975]

p[0->0] 0.7531 0.063 11.871 0.000 0.629 0.877

p[1->0] 0.6825 0.066 10.301 0.000 0.553 0.812

- The first regime is a low-variance regime and the second regime is a high-variance regime. Below we plot the probabilities of being in the low-variance regime. Between 2008 and 2012 there does not appear to be a clear indication of one regime guiding the economy.

res_areturns.smoothed_marginal_probabilities[0].plot(

title="Probability of being in a low-variance regime", figsize=(12, 3)

)

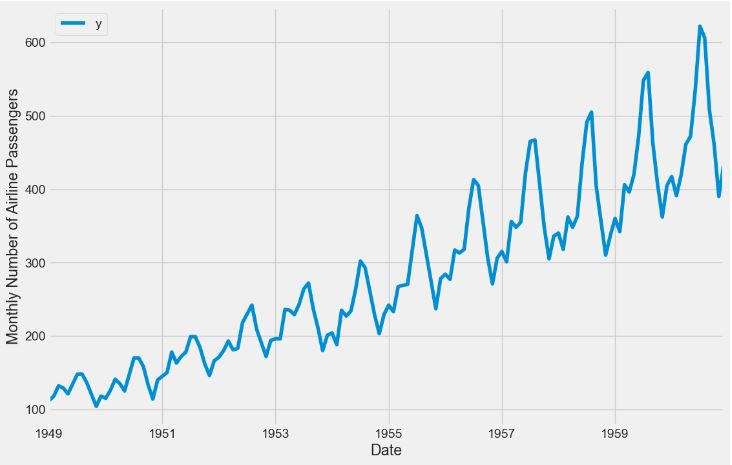

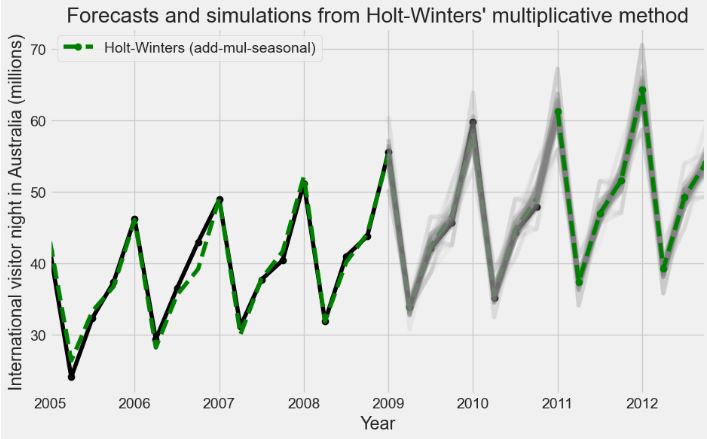

Number of Airline Passengers- 1. Holt-Winters

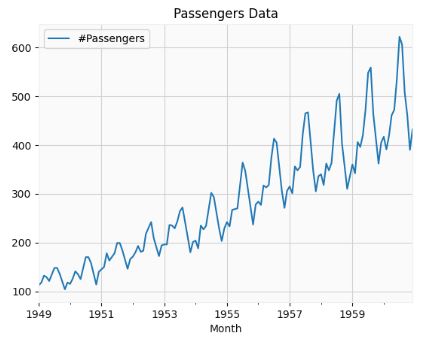

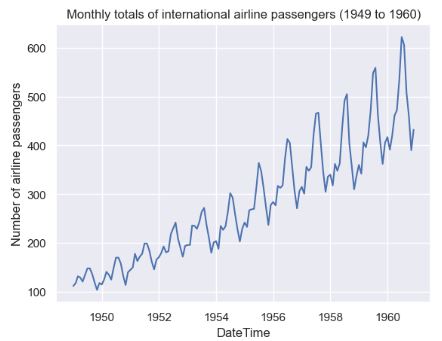

- Let’s apply the Holt-Winters Forecasting algorithm to the Airlines Passenger Data representing he number of International Airline Passengers (in thousands) between January 1949 to December 1960.

- Importing the key libraries and downloading the Kaggle dataset

# dataframe opertations - pandas

import pandas as pd

# plotting data - matplotlib

from matplotlib import pyplot as plt

# time series - statsmodels

# Seasonality decomposition

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.seasonal import seasonal_decompose

# holt winters

# single exponential smoothing

from statsmodels.tsa.holtwinters import SimpleExpSmoothing

# double and triple exponential smoothing

from statsmodels.tsa.holtwinters import ExponentialSmoothing

airline = pd.read_csv('AirPassengers.csv',index_col='Month', parse_dates=True)

# finding shape of the dataframe

print(airline.shape)

# having a look at the data

print(airline.head())

# plotting the original data

airline[['#Passengers']].plot(title='Passengers Data')

(144, 1)

#Passengers

Month

1949-01-01 112

1949-02-01 118

1949-03-01 132

1949-04-01 129

1949-05-01 121

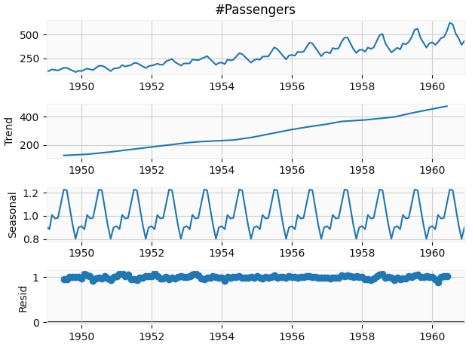

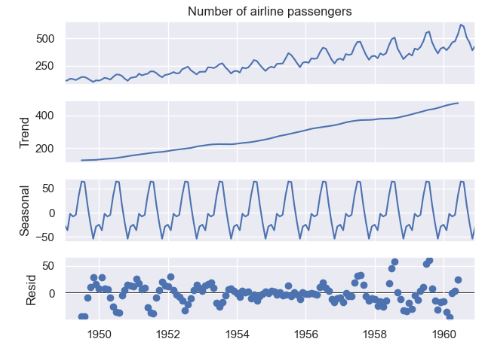

- Performing the seasonal decomposition of the input data

decompose_result = seasonal_decompose(airline['#Passengers'],model='multiplicative')

decompose_result.plot();

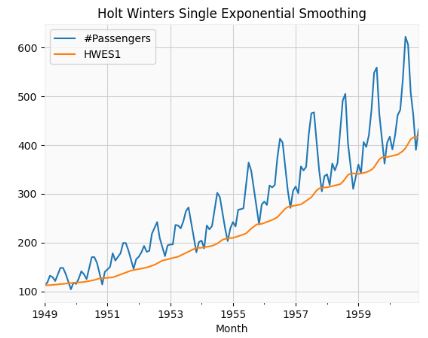

- Performing the Holt Winters (HW) Single Exponential Smoothing

# Set the frequency of the date time index as Monthly start as indicated by the data

airline.index.freq = 'MS'

# Set the value of Alpha and define m (Time Period)

m = 12

alpha = 1/(2*m)

airline['HWES1'] = SimpleExpSmoothing(airline['#Passengers']).fit(smoothing_level=alpha,optimized=False,use_brute=True).fittedvalues

airline[['#Passengers','HWES1']].plot(title='Holt Winters Single Exponential Smoothing');

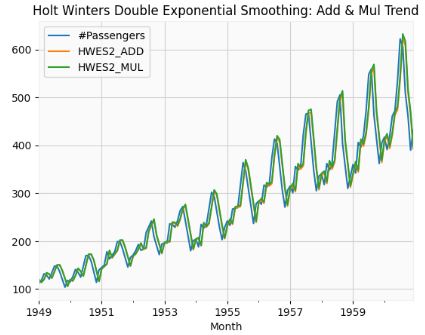

- Performing the HW Double Exponential Smoothing: Add & Mul Trend

airline['HWES2_ADD'] = ExponentialSmoothing(airline['#Passengers'],trend='add').fit().fittedvalues

airline['HWES2_MUL'] = ExponentialSmoothing(airline['#Passengers'],trend='mul').fit().fittedvalues

airline[['#Passengers','HWES2_ADD','HWES2_MUL']].plot(title='Holt Winters Double Exponential Smoothing: Add & Mul Trend');

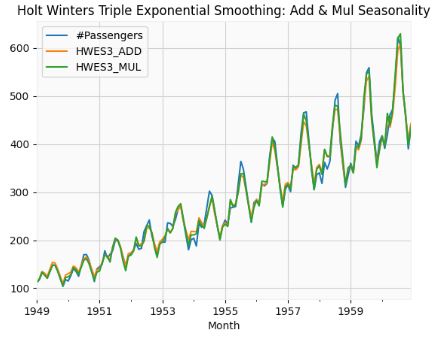

- Performing HW Triple Exponential Smoothing: Add & Mul Seasonality

airline['HWES3_ADD'] = ExponentialSmoothing(airline['#Passengers'],trend='add',seasonal='add',seasonal_periods=12).fit().fittedvalues

airline['HWES3_MUL'] = ExponentialSmoothing(airline['#Passengers'],trend='mul',seasonal='mul',seasonal_periods=12).fit().fittedvalues

airline[['#Passengers','HWES3_ADD','HWES3_MUL']].plot(title='Holt Winters Triple Exponential Smoothing: Add & Mul Seasonality');

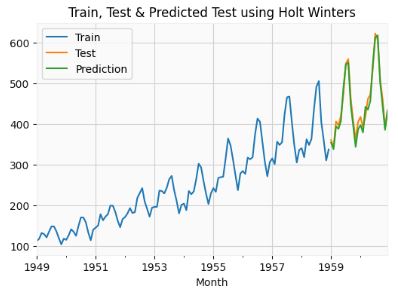

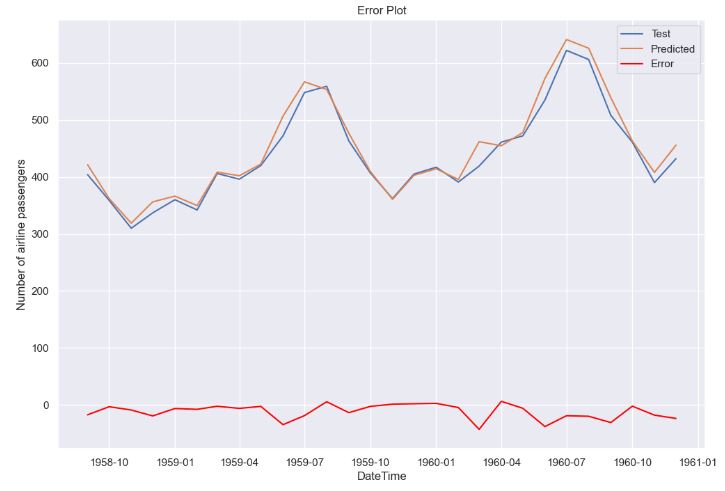

- Train, Test & Predicted Test using Holt Winters

# Split into train and test set

forecast_data=airline.copy()

train_airline = forecast_data[:120]

test_airline = forecast_data[120:]

fitted_model = ExponentialSmoothing(train_airline['#Passengers'],trend='mul',seasonal='mul',seasonal_periods=12).fit()

test_predictions = fitted_model.forecast(24)

train_airline['#Passengers'].plot(legend=True,label='Train')

test_airline['#Passengers'].plot(legend=True,label='Test',figsize=(6,4))

test_predictions.plot(legend=True,label='Prediction')

plt.title('Train, Test & Predicted Test using Holt Winters')

test_airline['#Passengers'].plot(legend=True,label='Test',figsize=(9,6))

test_predictions.plot(legend=True,label='Prediction',xlim=['1959–01–01','1961–01–01']);

- Let’s apply the low-code open-source python framework pytsal to the Airlines Passenger Data

!git clone https://github.com/KrishnanSG/pytsal.git

cd pytsal

from pytsal.dataset import load_airline

ts = load_airline()

print(ts.summary())

print('\n### Data ###\n')

print(ts)

name Monthly totals of international airline passen...

freq MS

target Number of airline passengers

type Univariate

phase Full

series_length 144

start 1949-01-01T00:00:00.000000000

end 1960-12-01T00:00:00.000000000

dtype: object

### Data ###

Date

1949-01-01 112.0

1949-02-01 118.0

1949-03-01 132.0

1949-04-01 129.0

1949-05-01 121.0

...

1960-08-01 606.0

1960-09-01 508.0

1960-10-01 461.0

1960-11-01 390.0

1960-12-01 432.0

Freq: MS, Name: Number of airline passengers, Length: 144, dtype: float64

- Performing the complete forecasting model setup & tuning

from pytsal.forecasting import *

model = setup(ts, 'holtwinter', eda=True, validation=True, find_best_model=True, plot_model_comparison=True)

INFO:pytsal.forecasting:Loading time series ...

INFO:pytsal.forecasting:Creating train test data

INFO:pytsal.forecasting:Initializing Visualizer ...

INFO:pytsal.visualization.eda:EDAVisualizer initialized

--- Time series summary ---

name Monthly totals of international airline passen...

freq MS

target Number of airline passengers

type Univariate

phase Full

series_length 144

start 1949-01-01T00:00:00.000000000

end 1960-12-01T00:00:00.000000000

dtype: object

"Monthly totals of international airline passengers (1949 to 1960)" dataset split with train size: 116 test size: 28

INFO:pytsal.visualization.eda:Constructed Time plot

INFO:pytsal.visualization.eda:Constructed decompose plot

INFO:pytsal.visualization.eda:Constructed seasonal plot

INFO:pytsal.visualization.eda:Constructed box plot

INFO:pytsal.visualization.eda:Constructed acf and pacf plot

INFO:pytsal.visualization.eda:Performing stationarity test

INFO:pytsal.visualization.eda:Test 1/2 ADF

INFO:pytsal.visualization.eda:

Test 2/2 KPSS

INFO:pytsal.visualization.eda:Tests completed

INFO:pytsal.visualization.eda:Performed stationary tests

INFO:pytsal.visualization.eda:EDAVisualizer completed

INFO:pytsal.forecasting:Initialize model tuning ...

INFO:pytsal.forecasting:Initializing comparison plot ...

Results of Dickey-Fuller Test:

Test Statistic 0.815369

p-value 0.991880

#Lags Used 13.000000

Number of Observations Used 130.000000

Critical Value 1% -3.481682

Critical Value 5% -2.884042

Critical Value 10% -2.578770

dtype: float64

KPSS Statistic: 0.09614984853532524

p-value: 0.1

num lags: 4

Critial Values:

10% : 0.119

5% : 0.146

2.5% : 0.176

1% : 0.216

ADF: p-value = 0.9919. The series is likely non-stationary.

KPSS: The series is deterministic trend stationary

9 tunable params available for <class 'pytsal.internal.containers.models.forecasting.HoltWinter'>

INFO:pytsal.forecasting:Tuning completed

###### TUNING SUMMARY #####

model_name args score aicc

8 HoltWinter {'trend': 'mul', 'seasonal': 'mul'} 13.053969 559.88

7 HoltWinter {'trend': 'mul', 'seasonal': 'add'} 15.790874 607.52

6 HoltWinter {'trend': 'add', 'seasonal': 'mul'} 20.691400 561.14

5 HoltWinter {'trend': 'add', 'seasonal': 'add'} 23.616991 608.54

4 HoltWinter {'trend': None, 'seasonal': 'mul'} 42.557011 509.11

2 HoltWinter {'trend': None, 'seasonal': 'add'} 52.697958 635.81

0 HoltWinter {'trend': None, 'seasonal': None} 91.816338 766.94

1 HoltWinter {'trend': 'add', 'seasonal': None} 121.201352 769.53

3 HoltWinter {'trend': 'mul', 'seasonal': None} 159.346430 770.16

Best model: {'trend': 'mul', 'seasonal': 'mul'} with score: 13.053969239269817

--- Model Summary ---

{'trend': 'mul', 'seasonal': 'mul'}

MAE 13.053969

MAPE 0.029033

RMSE 17.573640

AIC 552.826631

BIC 596.884074

AICC 559.878177

Name: Model metrics, dtype: float64

trained_model = finalize(ts, model)

INFO:pytsal.forecasting:Finalizing model (Training on complete data) ...

ExponentialSmoothing Model Results

========================================================================================

Dep. Variable: Number of airline passengers No. Observations: 144

Model: ExponentialSmoothing SSE 15805.297

Optimized: True AIC 708.553

Trend: Multiplicative BIC 756.070

Seasonal: Multiplicative AICC 714.025

Seasonal Periods: 12 Date: Tue, 02 Jan 2024

Box-Cox: False Time: 18:06:56

Box-Cox Coeff.: None

=================================================================================

coeff code optimized

---------------------------------------------------------------------------------

smoothing_level 0.2919245 alpha True

smoothing_trend 2.4068e-10 beta True

smoothing_seasonal 0.5678907 gamma True

initial_level 116.27509 l.0 True

initial_trend 1.0091534 b.0 True

initial_seasons.0 0.9510089 s.0 True

initial_seasons.1 1.0025536 s.1 True

initial_seasons.2 1.1168827 s.2 True

initial_seasons.3 1.0647580 s.3 True

initial_seasons.4 0.9955442 s.4 True

initial_seasons.5 1.0918944 s.5 True

initial_seasons.6 1.1934906 s.6 True

initial_seasons.7 1.1805039 s.7 True

initial_seasons.8 1.0707840 s.8 True

initial_seasons.9 0.9271625 s.9 True

initial_seasons.10 0.8131458 s.10 True

initial_seasons.11 0.9419461 s.11 True

---------------------------------------------------------------------------------

save_model(trained_model)

INFO:pytsal.forecasting:Model saved to trained_model.pytsal

'Model saved'

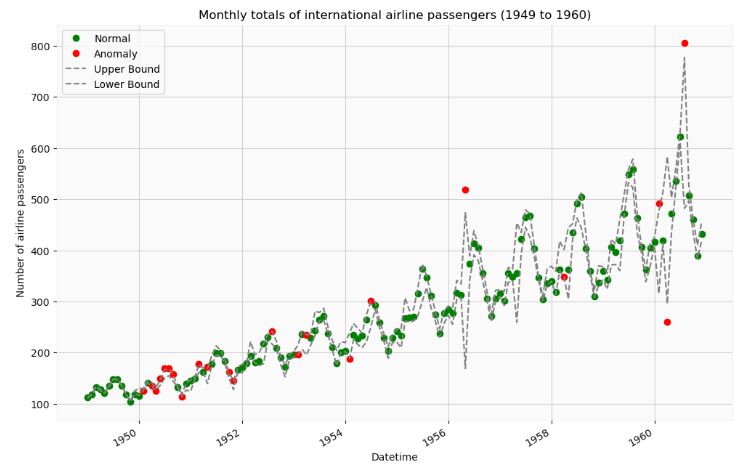

- The following example illustrates how the pytsal Holt-Winter’s model and the brutlag algorithm can be used to identify anomalies present in the above data.

import pytsal.forecasting as f

import pytsal.anomaly as ad

from pytsal.dataset import load_airline_with_anomaly

#1. Load data

ts_with_anomaly = load_airline_with_anomaly()

#print(ts_with_anomaly.summary())

#print('\n### Data ###\n')

#print(ts)

# 2.a Load model if exists

model = f.load_model()

# 2.b Create new model

if model is None:

ts = load_airline()

model = f.setup(ts, 'holtwinter', eda=False, validation=False, find_best_model=True, plot_model_comparison=False)

trained_model = f.finalize(ts, model)

f.save_model(trained_model)

model = f.load_model()

# 3. brutlag algorithm finds and returns the anomaly points

anomaly_points = ad.setup(ts_with_anomaly, model, 'brutlag')

INFO:pytsal.forecasting:Model loaded from trained_model.pytsal

INFO:pytsal.anomaly:Initializing anomaly detection algorithm ...

WARNING:pytsal.anomaly:This function in future release will be refactored. Hence use this with care expecting breaking changes in upcoming versions.

INFO:pytsal.anomaly:Performing brutlag anomaly detection ...

Difference between actual and predicted

actual predicted difference UB LB

Date

1949-01-01 112.0 111.590815 0.409185 111.892320 111.289311

1949-02-01 118.0 118.842908 -0.842908 119.463998 118.221818

1949-03-01 132.0 133.330735 -1.330735 134.311276 132.350193

1949-04-01 129.0 127.897958 1.102042 128.709989 127.085926

1949-05-01 121.0 120.982190 0.017810 120.995313 120.969068

... ... ... ... ... ...

1960-08-01 806.0 629.399412 176.600588 777.057362 481.741463

1960-09-01 508.0 511.998458 -3.998458 526.868422 497.128493

1960-10-01 461.0 448.033463 12.966537 461.492241 434.574685

1960-11-01 390.0 397.251316 -7.251316 410.319061 384.183570

1960-12-01 432.0 437.148457 -5.148457 455.348078 418.948837

[144 rows x 5 columns]

The data points classified as anomaly

observed expected

date

1950-02-01 126.0 128.061306

1950-04-01 135.0 138.507945

1950-05-01 125.0 129.102592

1950-06-01 149.0 142.209534

1950-07-01 170.0 158.282617

1950-08-01 170.0 161.586634

1950-09-01 158.0 150.451460

1950-11-01 114.0 117.015788

1951-03-01 178.0 169.289921

1951-05-01 172.0 154.496337

1951-10-01 162.0 155.498759

1951-11-01 146.0 136.398227

1952-08-01 242.0 229.327484

1953-02-01 196.0 205.796078

1953-04-01 235.0 215.252036

1954-02-01 188.0 213.333317

1954-07-01 302.0 274.823045

1956-05-01 518.0 321.263814

1958-04-01 348.0 374.880420

1960-02-01 491.0 395.803036

1960-04-01 261.0 439.297376

1960-08-01 806.0 629.399412

Number of Airline Passengers- 2. Prophet

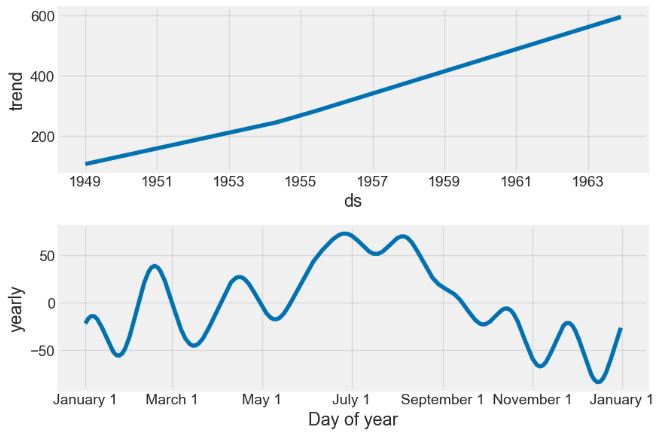

- In this section, we will apply the Prophet algorithm to the Airlines Passenger Data

- Preparing the input data

%matplotlib inline

import pandas as pd

from prophet import Prophet

import matplotlib.pyplot as plt

plt.style.use('fivethirtyeight')

df = pd.read_csv('AirPassengers.csv')

df['Month'] = pd.DatetimeIndex(df['Month'])

df = df.rename(columns={'Month': 'ds',

'#Passengers': 'y'})

ax = df.set_index('ds').plot(figsize=(12, 8))

ax.set_ylabel('Monthly Number of Airline Passengers')

ax.set_xlabel('Date')

plt.show()

- Fitting the model and making predictions

# set the uncertainty interval to 95% (the Prophet default is 80%)

my_model = Prophet(interval_width=0.95)

my_model.fit(df)

future_dates = my_model.make_future_dataframe(periods=36, freq='MS')

future_dates.tail()

ds

175 1963-08-01

176 1963-09-01

177 1963-10-01

178 1963-11-01

179 1963-12-01

forecast = my_model.predict(future_dates)

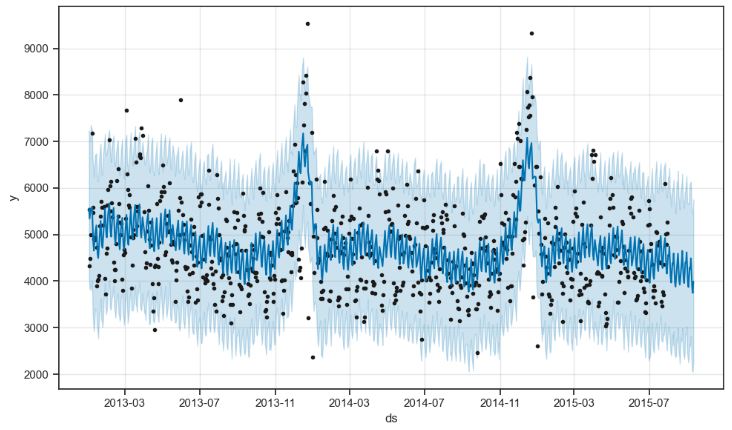

forecast[['ds', 'yhat', 'yhat_lower', 'yhat_upper']].tail()

my_model.plot(forecast,

uncertainty=True)

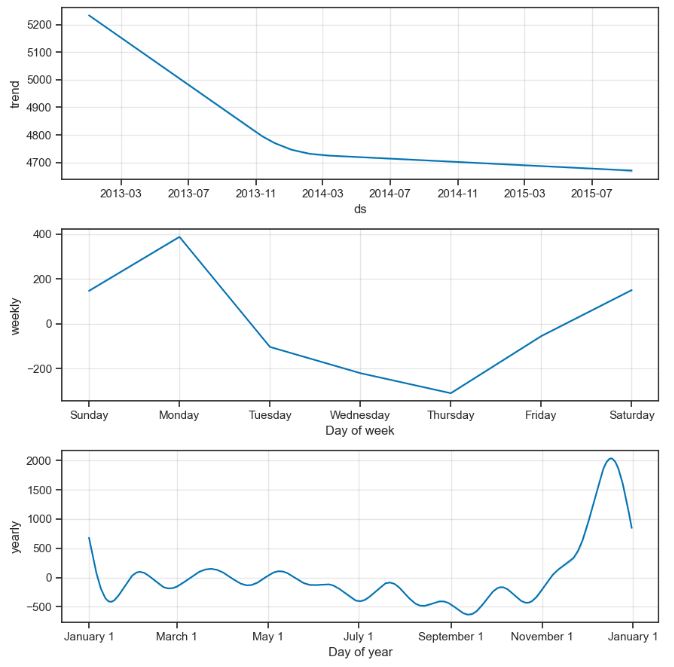

my_model.plot_components(forecast)

Average Temperature in India

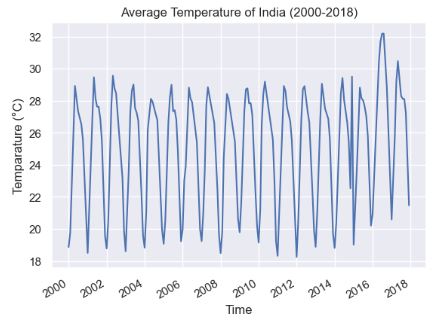

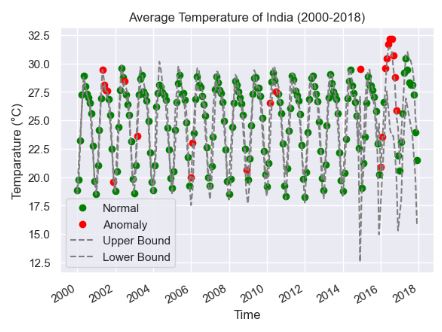

- Let’s apply the pytsal Holt-Winter’s model and the brutlag algorithm to the weather dataset that contains the India’s monthly average temperature (°C) from 2000-2018.

- Importing the input dataset

from time_series import TimeSeries

# Imports for data visualization

import matplotlib.pyplot as plt

import pandas as pd

from matplotlib.dates import DateFormatter

from matplotlib import dates as mpld

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

ts = TimeSeries('average_temp_india.csv', train_size=0.7)

plt.plot(ts.data.iloc[:,1].index,ts.data.iloc[:,1])

plt.gcf().autofmt_xdate()

plt.title("Average Temperature of India (2000-2018)")

plt.xlabel("Time")

plt.ylabel("Temparature (°C)")

plt.show()

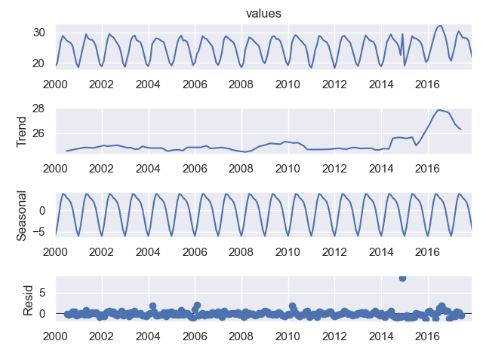

- Performing the additive seasonal decomposition of the above data

from statsmodels.tsa.seasonal import seasonal_decompose

seasonal_decompose(ts.data.iloc[:,1],model='additive',period=12).plot()

plt.show()

- Applying the anomaly detection algorithm to the temperature data

from time_series import TimeSeries

# Holt-Winters or Triple Exponential Smoothing model

from statsmodels.tsa.holtwinters import ExponentialSmoothing

# Imports for data visualization

import matplotlib.pyplot as plt

import pandas as pd

from matplotlib.dates import DateFormatter

from matplotlib import dates as mpld

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

ts = TimeSeries('average_temp_india.csv', train_size=0.7)

plt.plot(ts.data.iloc[:,1].index,ts.data.iloc[:,1])

plt.gcf().autofmt_xdate()

plt.title("Average Temperature of India (2000-2018)")

plt.xlabel("Time")

plt.ylabel("Temparature (°C)")

plt.show()

model = ExponentialSmoothing(

ts.train, trend='additive', seasonal='additive').fit()

prediction = model.predict(

start=ts.data.iloc[:, 1].index[0], end=ts.data.iloc[:, 1].index[-1])

"""Brutlag Algorithm"""

PERIOD = 12 # The given time series has seasonal_period=12

GAMMA = 0.3684211 # the seasonility component

SF = 1.96 # brutlag scaling factor for the confidence bands.

UB = [] # upper bound or upper confidence band

LB = [] # lower bound or lower confidence band

difference_array = []

dt = []

difference_table = {

"actual": ts.data.iloc[:, 1], "predicted": prediction, "difference": difference_array, "UB": UB, "LB": LB}

"""Calculatation of confidence bands using brutlag algorithm"""

for i in range(len(prediction)):

diff = ts.data.iloc[:, 1][i]-prediction[i]

if i < PERIOD:

dt.append(GAMMA*abs(diff))

else:

dt.append(GAMMA*abs(diff) + (1-GAMMA)*dt[i-PERIOD])

difference_array.append(diff)

UB.append(prediction[i]+SF*dt[i])

LB.append(prediction[i]-SF*dt[i])

print("\nDifference between actual and predicted\n")

difference = pd.DataFrame(difference_table)

print(difference)

"""Classification of data points as either normal or anomaly"""

normal = []

normal_date = []

anomaly = []

anomaly_date = []

for i in range(len(ts.data.iloc[:, 1].index)):

if (UB[i] <= ts.data.iloc[:, 1][i] or LB[i] >= ts.data.iloc[:, 1][i]) and i > PERIOD:

anomaly_date.append(ts.data.index[i])

anomaly.append(ts.data.iloc[:, 1][i])

else:

normal_date.append(ts.data.index[i])

normal.append(ts.data.iloc[:, 1][i])

anomaly = pd.DataFrame({"date": anomaly_date, "value": anomaly})

anomaly.set_index('date', inplace=True)

normal = pd.DataFrame({"date": normal_date, "value": normal})

normal.set_index('date', inplace=True)

print("\nThe data points classified as anomaly\n")

print(anomaly)

Difference between actual and predicted

actual predicted difference UB LB

2000-01-01 18.87 18.647206 0.222794 18.808087 18.486326

2000-02-01 19.78 20.668918 -0.888918 21.310810 20.027025

2000-03-01 23.22 24.025243 -0.805243 24.606713 23.443773

2000-04-01 27.27 26.716709 0.553291 27.116243 26.317175

2000-05-01 28.92 28.440959 0.479041 28.786877 28.095041

... ... ... ... ... ...

2017-08-01 28.12 27.387160 0.732840 30.254620 24.519699

2017-09-01 28.11 26.760501 1.349499 29.704445 23.816557

2017-10-01 27.24 25.312988 1.927012 28.594966 22.031011

2017-11-01 23.92 22.620502 1.299498 25.266893 19.974111

2017-12-01 21.47 19.868828 1.601172 23.898407 15.839248

[216 rows x 5 columns]

The data points classified as anomaly

value

date

2001-05-01 29.46

2001-06-01 28.13

2001-07-01 27.63

2001-08-01 27.62

2001-12-01 19.55

2002-07-01 28.47

2003-03-01 23.62

2006-01-01 19.96

2006-02-01 23.02

2008-12-01 20.62

2010-03-01 26.53

2010-07-01 27.55

2014-12-01 29.50

2016-01-01 20.92

2016-02-01 23.58

2016-04-01 29.56

2016-05-01 30.41

2016-06-01 31.70

2016-07-01 32.18

2016-08-01 32.19

2016-09-01 30.72

2016-10-01 28.81

2016-11-01 25.90

"""

Plotting the data points after classification as anomaly/normal.

Data points classified as anomaly are represented in red and normal in green.

"""

plt.plot(normal.index, normal, 'o', color='green')

plt.plot(anomaly.index, anomaly, 'o', color='red')

# Ploting brutlag confidence bands

plt.plot(ts.data.iloc[:, 1].index, UB, linestyle='--', color='grey')

plt.plot(ts.data.iloc[:, 1].index, LB, linestyle='--', color='grey')

# Formatting the graph

plt.legend(['Normal', 'Anomaly', 'Upper Bound', 'Lower Bound'])

plt.gcf().autofmt_xdate()

plt.title("Average Temperature of India (2000-2018)")

plt.xlabel("Time")

plt.ylabel("Temparature (°C)")

plt.show()

Monthly Sales Data Analysis

- Let’s apply the pytsal Holt-Winter’s model to the monthly total sales of a company from 2013-2016.

- Importing the input dataset

from time_series import TimeSeries

# Imports for data visualization

import matplotlib.pyplot as plt

from pandas.plotting import register_matplotlib_converters

from matplotlib.dates import DateFormatter

from matplotlib import dates as mpld

register_matplotlib_converters()

ts = TimeSeries('monthly_sales.csv', train_size=0.8)

print("Sales Data")

print(ts.data.describe())

print("Head and Tail of the time series")

print(ts.data.head(5).iloc[:,1])

print(ts.data.tail(5).iloc[:,1])

# Plot of raw time series data

plt.plot(ts.data.index,ts.data.sales)

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%Y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

plt.title("Sales Data Analysis (2013-2016)")

plt.xlabel("Time")

plt.ylabel("Sales")

plt.show()

Sales Data

sales

count 48.000000

mean 47858.351667

std 25221.124187

min 4519.890000

25% 29790.100000

50% 39339.515000

75% 65833.345000

max 118447.830000

Head and Tail of the time series

date

2013-01-01 14236.90

2013-02-01 4519.89

2013-03-01 55691.01

2013-04-01 28295.35

2013-05-01 23648.29

Name: sales, dtype: float64

date

2016-08-01 63120.89

2016-09-01 87866.65

2016-10-01 77776.92

2016-11-01 118447.83

2016-12-01 83829.32

Name: sales, dtype: float64

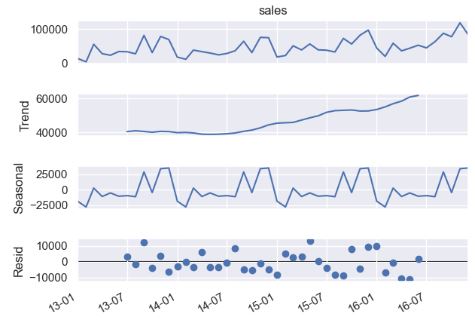

- Performing the seasonal decomposition of the above data

from statsmodels.tsa.seasonal import seasonal_decompose

result_add = seasonal_decompose(ts.data.iloc[:,1],period=12,model='additive')

result_add.plot()

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

result_mul = seasonal_decompose(ts.data.iloc[:,1],period=12,model='multiplicative')

result_mul.plot()

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

plt.show()

- model=’additive’

- model=’multiplicative’

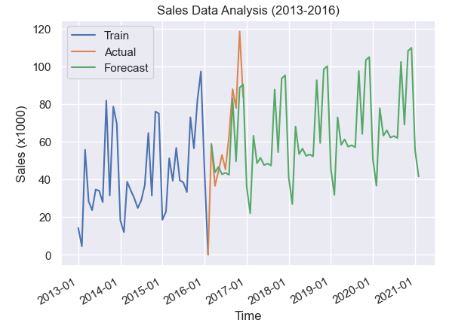

- Predicting the sales data with the Holt-Winter’s model

from statsmodels.tsa.holtwinters import ExponentialSmoothing

# Scaling down the data by a factor of 1000

ts.set_scale(1000)

# Training the model

model = ExponentialSmoothing(ts.train,trend='additive',seasonal='additive',seasonal_periods=12).fit(damping_slope=1)

plt.plot(ts.train.index,ts.train,label="Train")

plt.plot(ts.test.index,ts.test,label="Actual")

# Create a 5 year forecast

plt.plot(model.forecast(60),label="Forecast")

plt.legend(['Train','Actual','Forecast'])

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%Y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

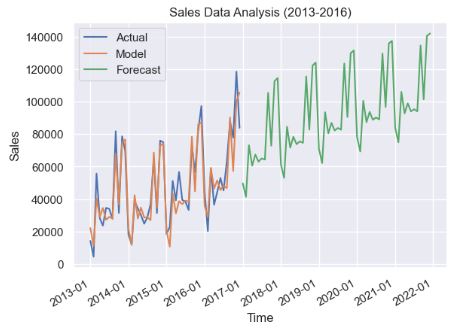

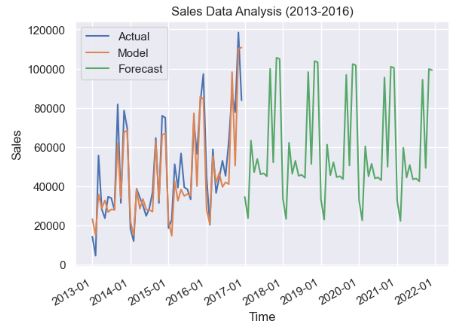

plt.title("Sales Data Analysis (2013-2016)")

plt.xlabel("Time")

plt.ylabel("Sales (x1000)")

plt.show()

- Backtesting the training data with the additive and multiplicative Holt-Winter’s (HW) models

from statsmodels.tsa.holtwinters import ExponentialSmoothing

ts = TimeSeries('monthly_sales.csv', train_size=0.8)

# Additive model

model_add = ExponentialSmoothing(ts.data.iloc[:,1],trend='additive',seasonal='additive',seasonal_periods=12,damped=True).fit(damping_slope=0.98)

prediction = model_add.predict(start=ts.data.iloc[:,1].index[0],end=ts.data.iloc[:,1].index[-1])

plt.plot(ts.data.iloc[:,1].index,ts.data.iloc[:,1],label="Train")

plt.plot(ts.data.iloc[:,1].index,prediction,label="Model")

plt.plot(model_add.forecast(60))

plt.legend(['Actual','Model','Forecast'])

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%Y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

plt.title("Sales Data Analysis (2013-2016)")

plt.xlabel("Time")

plt.ylabel("Sales")

plt.show()

# Multiplicative model

model_mul = ExponentialSmoothing(ts.data.iloc[:,1],trend='additive',seasonal='multiplicative',seasonal_periods=12,damped=True).fit()

prediction = model_mul.predict(start=ts.data.iloc[:,1].index[0],end=ts.data.iloc[:,1].index[-1])

plt.plot(ts.data.iloc[:,1].index,ts.data.iloc[:,1],label="Train")

plt.plot(ts.data.iloc[:,1].index,prediction,label="Model")

plt.plot(model_mul.forecast(60))

plt.legend(['Actual','Model','Forecast'])

plt.gcf().autofmt_xdate()

date_format = mpld.DateFormatter('%Y-%m')

plt.gca().xaxis.set_major_formatter(date_format)

plt.title("Sales Data Analysis (2013-2016)")

plt.xlabel("Time")

plt.ylabel("Sales")

plt.show()

- Additive HW model

- Multiplicative HW model

- Printing the HW model summary

print(model_add.summary())

ExponentialSmoothing Model Results

================================================================================

Dep. Variable: sales No. Observations: 48

Model: ExponentialSmoothing SSE 3839988196.858

Optimized: True AIC 907.482

Trend: Additive BIC 939.292

Seasonal: Additive AICC 934.624

Seasonal Periods: 12 Date: Sun, 10 Dec 2023

Box-Cox: False Time: 16:00:40

Box-Cox Coeff.: None

=================================================================================

coeff code optimized

---------------------------------------------------------------------------------

smoothing_level 0.1464286 alpha True

smoothing_trend 0.1464286 beta True

smoothing_seasonal 0.0001 gamma True

initial_level 41082.694 l.0 True

initial_trend -156.87900 b.0 True

damping_trend 0.9800000 phi False

initial_seasons.0 -18766.692 s.0 True

initial_seasons.1 -28179.421 s.1 True

initial_seasons.2 2468.4814 s.2 True

initial_seasons.3 -11199.301 s.3 True

initial_seasons.4 -5356.2134 s.4 True

initial_seasons.5 -10732.448 s.5 True

initial_seasons.6 -9770.2038 s.6 True

initial_seasons.7 -11438.903 s.7 True

initial_seasons.8 28700.401 s.8 True

initial_seasons.9 -4778.0170 s.9 True

initial_seasons.10 33978.828 s.10 True

initial_seasons.11 35073.489 s.11 True

---------------------------------------------------------------------------------

print(model_mul.summary())

ExponentialSmoothing Model Results

================================================================================

Dep. Variable: sales No. Observations: 48

Model: ExponentialSmoothing SSE 5306329076.722

Optimized: True AIC 923.006

Trend: Additive BIC 954.817

Seasonal: Multiplicative AICC 950.149

Seasonal Periods: 12 Date: Sun, 10 Dec 2023

Box-Cox: False Time: 16:00:40

Box-Cox Coeff.: None

=================================================================================

coeff code optimized

---------------------------------------------------------------------------------

smoothing_level 0.1464286 alpha True

smoothing_trend 0.0001 beta True

smoothing_seasonal 0.0001 gamma True

initial_level 41082.694 l.0 True

initial_trend -158.47980 b.0 True

damping_trend 0.9900000 phi True

initial_seasons.0 0.5674311 s.0 True

initial_seasons.1 0.3899121 s.1 True

initial_seasons.2 1.0435695 s.2 True

initial_seasons.3 0.7787636 s.3 True

initial_seasons.4 0.8913974 s.4 True

initial_seasons.5 0.7633235 s.5 True

initial_seasons.6 0.7722301 s.6 True

initial_seasons.7 0.7479818 s.7 True

initial_seasons.8 1.6619738 s.8 True

initial_seasons.9 0.8691594 s.9 True

initial_seasons.10 1.7613772 s.10 True

initial_seasons.11 1.7528805 s.11 True

---------------------------------------------------------------------------------

- One can see that IC(model_add)<IC(model_mul), where IC=AIC, BIC, and AICC. Recall that the smaller the IC value, the better the model fit.

"""

Conclusion of the analysis

--------------------------

From the model summary obtained it is clear that the sum of squared errors (SSE) for

the additive model (5088109579.122) < the SSE for the multiplicative(5235252441.242) model.

Hence the initial assumption that seasonality is roughly constant and therefore choosing

additive model was appropriate.

Note: The forecast made using multiplicative model seems to be unrealistic since the

variance between the high and low on an average is 100000 which is somewhat unexpected in

real world sales compared to 63000 incase of additive model.

"""

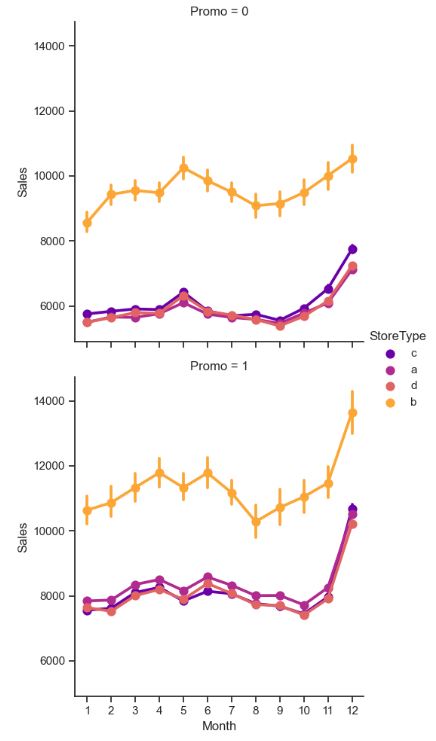

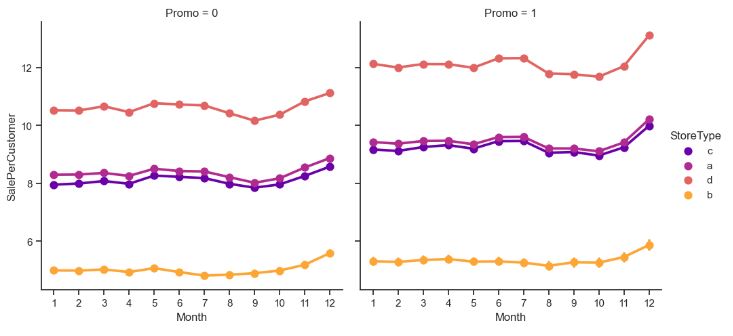

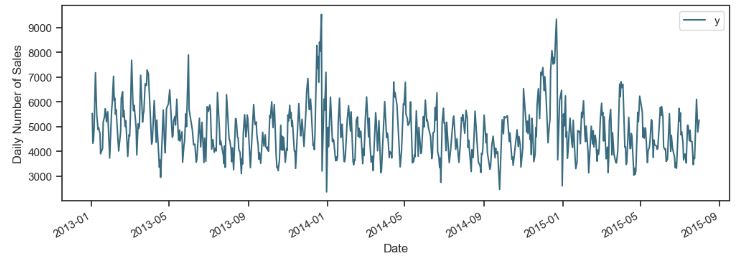

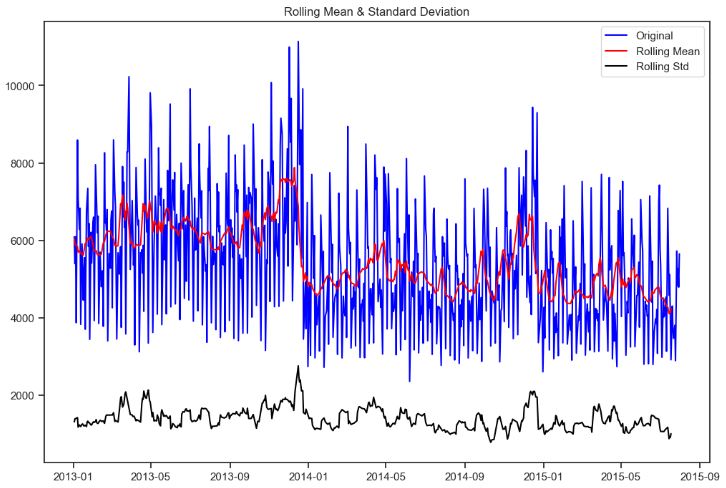

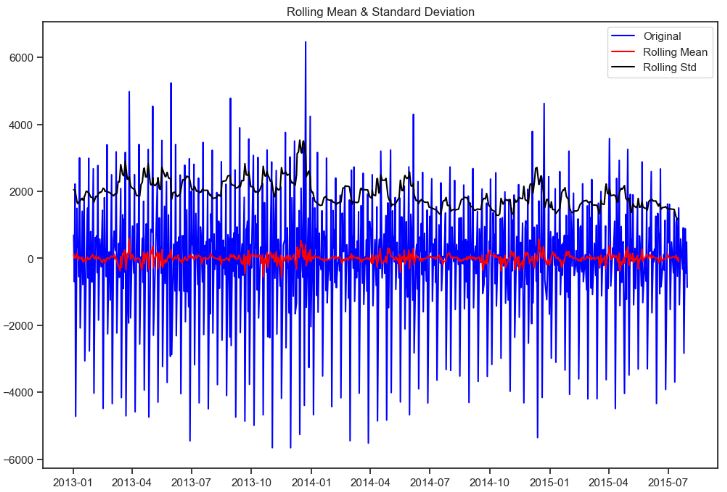

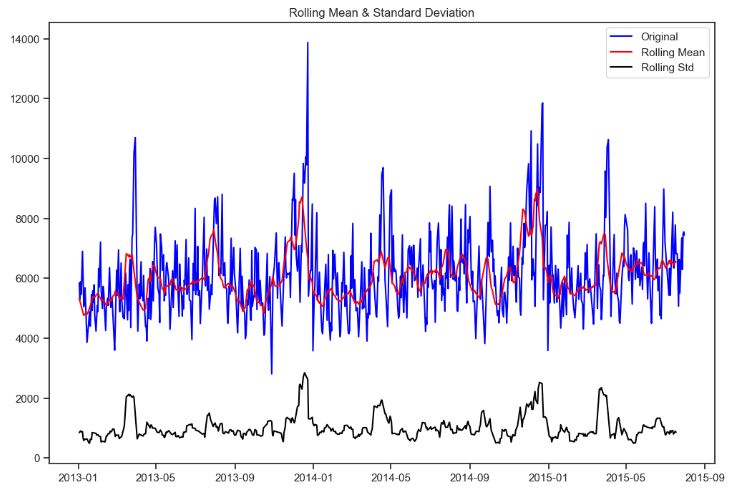

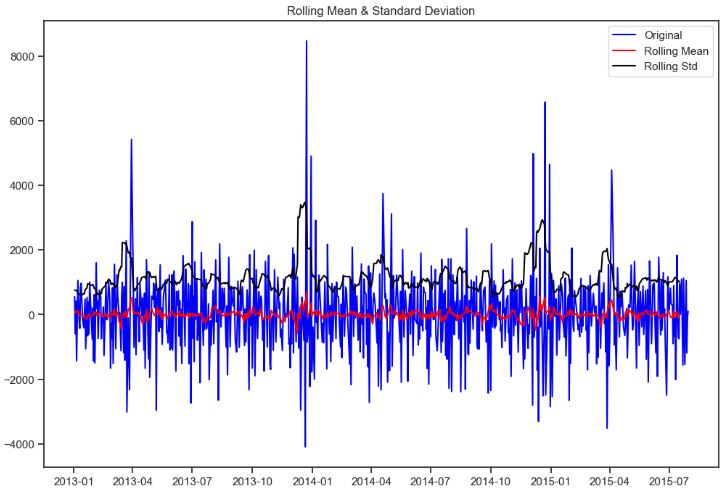

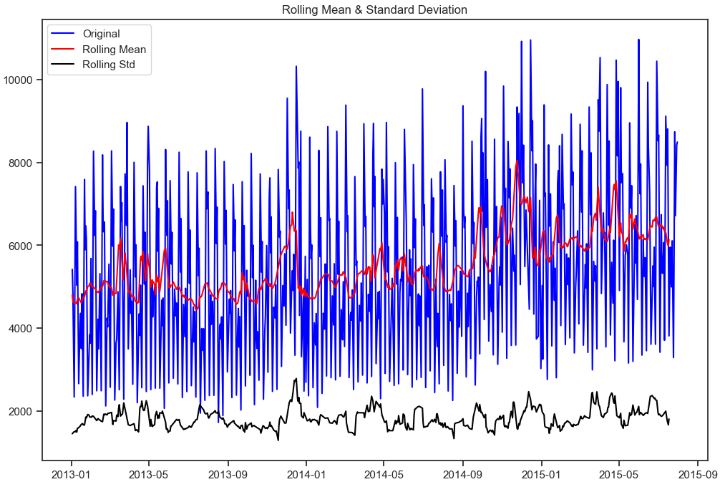

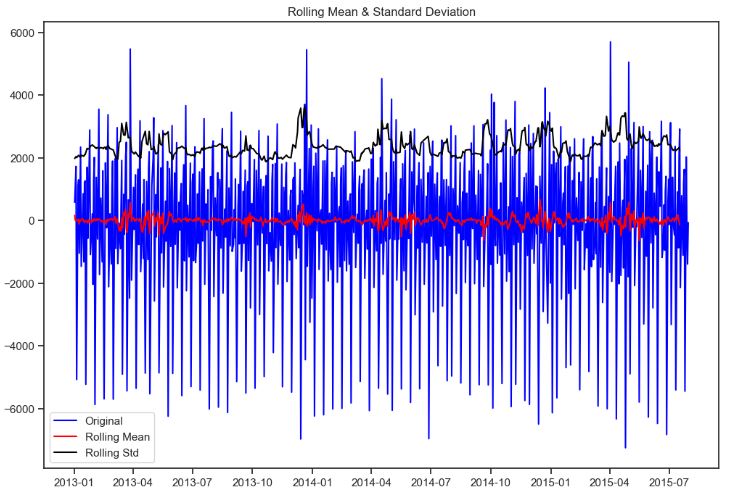

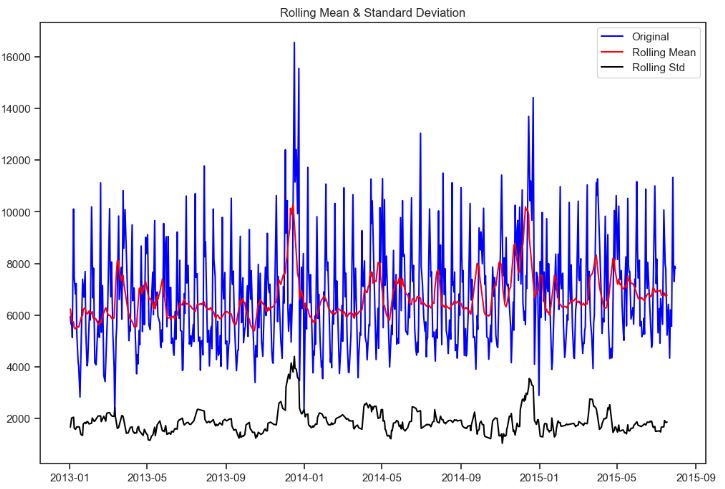

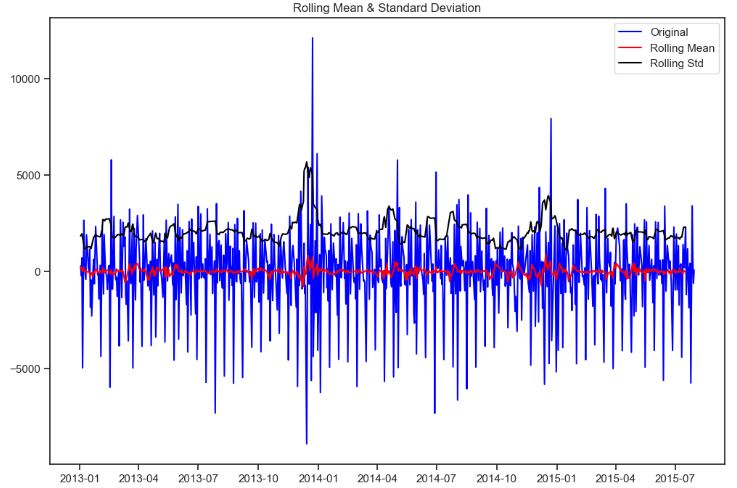

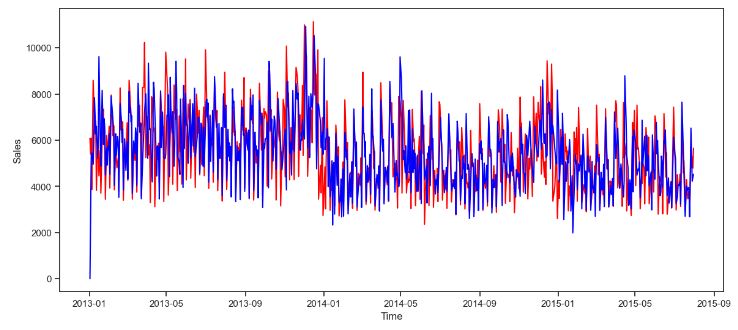

QC Audit of Rossmann Stores

- Let’s look at the Rossmann Store Sales representing historical sales data for 1,115 Rossmann stores. Our ultimate goal is to forecast the “Sales” column for the test set. Data challenge: some stores in the dataset were temporarily closed for refurbishment.

- Importing the key libraries

import warnings

warnings.filterwarnings("ignore")

# loading packages

# basic + dates

import numpy as np

import pandas as pd

from pandas import datetime

# data visualization

import matplotlib.pyplot as plt

import seaborn as sns # advanced vizs

%matplotlib inline

# statistics

#https://towardsdatascience.com/what-why-and-how-to-read-empirical-cdf-123e2b922480

from statsmodels.distributions.empirical_distribution import ECDF

# time series analysis

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

# prophet by Facebook

from prophet import Prophet

- Importing the train set and additional store data

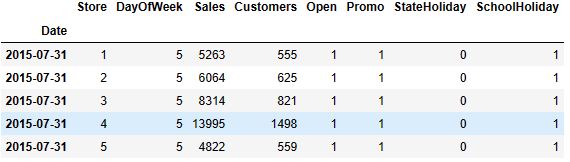

# importing train data to learn

train = pd.read_csv("train.csv",

parse_dates = True, low_memory = False, index_col = 'Date')

# additional store data

store = pd.read_csv("store.csv",

low_memory = False)

# time series as indexes

train.index

DatetimeIndex(['2015-07-31', '2015-07-31', '2015-07-31', '2015-07-31',

'2015-07-31', '2015-07-31', '2015-07-31', '2015-07-31',

'2015-07-31', '2015-07-31',

...

'2013-01-01', '2013-01-01', '2013-01-01', '2013-01-01',

'2013-01-01', '2013-01-01', '2013-01-01', '2013-01-01',

'2013-01-01', '2013-01-01'],

dtype='datetime64[ns]', name='Date', length=1017209, freq=None)

print(train.shape)

train.head()

(1017209, 8)

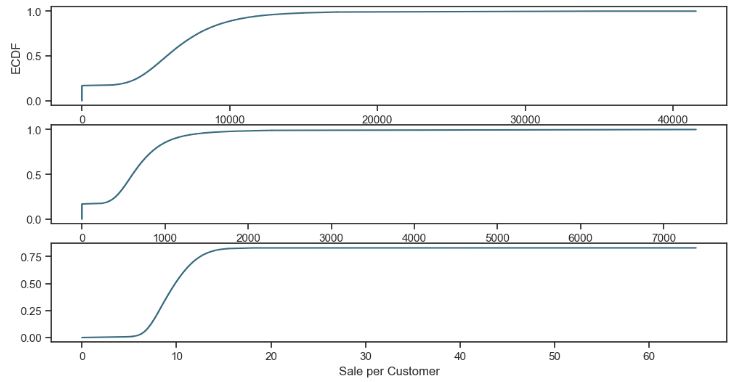

- Data editing, descriptive statistics, and plotting ECDF

# data extraction

train['Year'] = train.index.year

train['Month'] = train.index.month

train['Day'] = train.index.day

train['WeekOfYear'] = train.index.weekofyear

# adding new variable

train['SalePerCustomer'] = train['Sales']/train['Customers']

train['SalePerCustomer'].describe()

count 844340.000000

mean 9.493619

std 2.197494

min 0.000000

25% 7.895563

50% 9.250000

75% 10.899729

max 64.957854

Name: SalePerCustomer, dtype: float64

sns.set(style = "ticks")# to format into seaborn

c = '#386B7F' # basic color for plots

plt.figure(figsize = (12, 6))

plt.subplot(311)

cdf = ECDF(train['Sales'])

plt.plot(cdf.x, cdf.y, label = "statmodels", color = c);

plt.xlabel('Sales'); plt.ylabel('ECDF');

# plot second ECDF

plt.subplot(312)

cdf = ECDF(train['Customers'])

plt.plot(cdf.x, cdf.y, label = "statmodels", color = c);

plt.xlabel('Customers');

# plot second ECDF

plt.subplot(313)

cdf = ECDF(train['SalePerCustomer'])

plt.plot(cdf.x, cdf.y, label = "statmodels", color = c);

plt.xlabel('Sale per Customer');

- Checking open stores with zero sales

train[(train.Open==0)].shape

(172817, 13)

# opened stores with zero sales

zero_sales = train[(train.Open != 0) & (train.Sales == 0)]

print("In total: ", zero_sales.shape)