- This is a continuation of the previous ML-centered case study focused on predicting rolling volatility of the NVIDIA stock.

- Today our ultimate objective is to optimize NVIDIA moving average (MVA) crossovers in terms of balanced returns and drawdowns as compared to the simple RNN mean reversal trading strategies.

- Recall that MVA Cross is an indicator that shows when a trend is changing in the short-term and getting either weaker or stronger. We will focus on the very popular and straightforward dual MVA crossover trading strategy that uses two moving averages to predict market trends and entry/exit points.

- Mean reversion in trading theorizes that prices tend to return to average levels, and extreme price moves are hard to sustain for extended periods.

- The predictive modelling study explained how using RNNs in a mean reversion strategy can improve its performance. RNNs are particularly useful for modelling sequences of events where the output of one event is fed back into the network as input for the next event.

Stock Data Preparation

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

- Importing the basic Python libraries

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

import plotly.graph_objs as go

import seaborn as sns

- Downloading the 10Y NVIDIA stock dataset

#Download ticker price data from yfinance

tick = 'NVDA'

ticker = yf.Ticker(tick)

ticker_history = ticker.history(period='10y')

- Calculating MVAs and cumulative returns

#Calculate 10 and 20 days moving averages

ticker_history['ma10'] = ticker_history['Close'].rolling(window=10).mean()

ticker_history['ma20'] = ticker_history['Close'].rolling(window=20).mean()

#Create a column with buy and sell signals

ticker_history['signal'] = 0.0

ticker_history['signal'] = np.where(ticker_history['ma10'] > ticker_history['ma20'], 1.0, 0.0)

#Calculate daily returns for the ticker

ticker_history['returns'] = ticker_history['Close'].pct_change()

#Calculate strategy returns

ticker_history['strategy_returns'] = ticker_history['signal'].shift(1) * ticker_history['returns']

#Calculate cumulative returns for the ticker and the strategy

ticker_history['cumulative_returns'] = (1 + ticker_history['returns']).cumprod()

ticker_history['cumulative_strategy_returns'] = (1 + ticker_history['strategy_returns']).cumprod()

#Print the cumulative strategy returns at the last date

ticker_history['cumulative_strategy_returns'][-1]

19.665081883053688

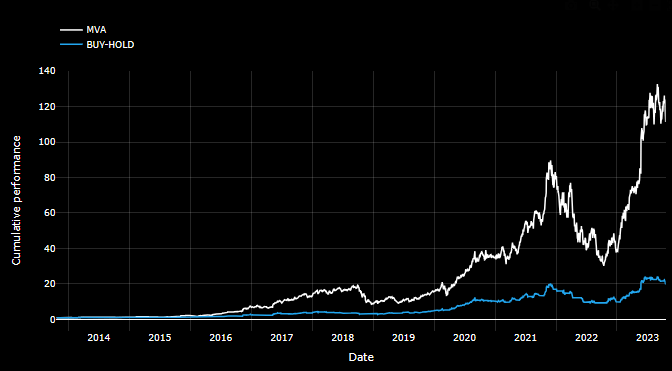

- Invoking Plotly to compare cumulative returns of MVA and Buy-Hold trading strategies

fig = go.Figure()

fig.add_trace(go.Scatter(x=ticker_history.index, y=ticker_history['cumulative_returns'], name='MVA',

line=dict(color='white', width=2)))

fig.add_trace(go.Scatter(x=ticker_history.index, y=ticker_history['cumulative_strategy_returns'], name='BUY-HOLD',

line=dict(color='#22a7f0', width=2)))

fig.update_layout(title=(''),

xaxis_title='Date',

yaxis_title='Cumulative performance',

font=dict(color='white'),

paper_bgcolor='black',

plot_bgcolor='black',

legend=dict(x=0, y=1.2, bgcolor='rgba(0,0,0,0)'),

yaxis=dict(gridcolor='rgba(255,255,255,0.2)'),

xaxis=dict(gridcolor='rgba(255,255,255,0.2)'))

fig.update_xaxes(showgrid=True, ticklabelmode="period")

fig.update_yaxes(showgrid=True)

fig.show()

- Calculating the maximum cumulative returns and the current drawdown of the strategy returns in relation to the maximum cumulative returns

#Calculate the maximum cumulative returns of the strategy so far

ticker_history['cumulative_strategy_max'] = ticker_history['cumulative_strategy_returns'].cummax()

#Calculate the current drawdown of the strategy returns in relation to the maximum cumulative returns

ticker_history['cumulative_strategy_drawdown'] = (ticker_history['cumulative_strategy_returns'] / ticker_history['cumulative_strategy_max']) - 1

#Print the current drawdown

print('The current drawdown of the strategy is:', ticker_history['cumulative_strategy_drawdown'][-1])

The current drawdown of the strategy is: -0.1868066793178107

- Calculating mean fast/slow 10-20 MVAs and strategy returns

#Define base slow and fast moving averages

fast_ma = 10

slow_ma = 20

#Calculate the moving averages for the strategy

ticker_history['fast_ma'] = ticker_history['Close'].rolling(window=fast_ma).mean()

ticker_history['slow_ma'] = ticker_history['Close'].rolling(window=slow_ma).mean()

#Create a column with buy and sell signals

ticker_history['signal'] = np.where(ticker_history['fast_ma'] > ticker_history['slow_ma'], 1.0, 0.0)

# Calculate daily ticker and strategy returns

ticker_history['returns'] = ticker_history['Close'].pct_change()

ticker_history['strategy_returns'] = ticker_history['signal'].shift(1) * ticker_history['returns']

Heatmap of MVA Returns

- Preparing data for heatmaps of returns

# Define two lists of fast and slow moving average values to be used as index and columns for a returns matrix

fast_ma_range = [5, 7, 9, 10, 20, 21, 30, 40, 50, 100]

slow_ma_range = [7, 9, 10, 20, 21, 30, 40, 50, 100, 200]

# Create a DataFrame with the index and columns as the fast and slow moving average values, respectively

# The DataFrame will be used to store returns data for different combinations of the moving averages

returns_matrix = pd.DataFrame(index=fast_ma_range, columns=slow_ma_range)

# Iterate through all combinations of fast and slow moving average values

for fast_ma in fast_ma_range:

for slow_ma in slow_ma_range:

# Calculate the fast and slow moving averages of the stock's closing price

ticker_history['fast_ma'] = ticker_history['Close'].rolling(window=fast_ma).mean()

ticker_history['slow_ma'] = ticker_history['Close'].rolling(window=slow_ma).mean()

# Generate a signal to buy (1.0) or sell (0.0) based on the relative positions of the two moving averages

ticker_history['signal'] = np.where(ticker_history['fast_ma'] > ticker_history['slow_ma'], 1.0, 0.0)

# Calculate the daily returns of the stock and the strategy

ticker_history['strategy_returns'] = ticker_history['signal'].shift(1) * ticker_history['returns']

# Calculate the cumulative returns of the strategy

cumulative_strategy_returns = (1 + ticker_history['strategy_returns']).cumprod()

# Add the cumulative returns of the strategy to the returns matrix

returns_matrix.loc[fast_ma, slow_ma] = cumulative_strategy_returns[-1]

# Make a copy of the returns_matrix and convert index and columns to string type

values = returns_matrix.copy()

values.index = values.index.astype(str)

values.columns = values.columns.astype(str)

# Convert values to float type

values = values.astype(float)

# Change the style of the plot and set the default color scheme

plt.style.use('dark_background')

sns.set_palette("bright")

# Create a heatmap with the provided values, including annotations, using the RdYlGn color map

sns.heatmap(values, annot=True, cmap='RdYlGn')

# Add labels to the axes

plt.xlabel('Slow Moving Average', fontsize=12, color='white')

plt.ylabel('Fast Moving Average', fontsize=12, color='white')

# Add a title to the plot

plt.title('Heatmap of Returns', fontsize=16, color='white')

# Increase the font size to 0.8 and change the color to white for all text elements

sns.set(font_scale=0.8, rc={'text.color':'white', 'axes.labelcolor':'white', 'xtick.color':'white', 'ytick.color':'white'})

# Change the background color of the plot to black

fig = plt.gcf()

fig.set_facecolor('#000000')

# Display the plot

plt.show()

Heatmap of MVA Drawdowns

- Preparing data for heatmaps of drawdowns

# Define two lists of fast and slow moving average values to be used as index and columns for a returns matrix

fast_ma_range = [5, 7, 9, 10, 20, 21, 30, 40, 50, 100]

slow_ma_range = [7, 9, 10, 20, 21, 30, 40, 50, 100, 200]

# Create a DataFrame with the index and columns as the fast and slow moving average values, respectively

# The DataFrame will be used to store returns data for different combinations of the moving averages

dd_matrix = pd.DataFrame(index=fast_ma_range, columns=slow_ma_range)

# Loop through different values for fast and slow moving averages

for fast_ma in fast_ma_range:

for slow_ma in slow_ma_range:

# Calculate the moving averages for the strategy

ticker_history['fast_ma'] = ticker_history['Close'].rolling(window=fast_ma).mean()

ticker_history['slow_ma'] = ticker_history['Close'].rolling(window=slow_ma).mean()

# Create a binary signal column for buy/sell signals

ticker_history['signal'] = np.where(ticker_history['fast_ma'] > ticker_history['slow_ma'], 1.0, 0.0)

# Calculate daily returns for the ticker and the strategy

ticker_history['strategy_returns'] = ticker_history['signal'].shift(1) * ticker_history['returns']

# Calculate cumulative returns for the strategy

ticker_history['cumulative_strategy_returns'] = (1 + ticker_history['strategy_returns']).cumprod()

# Calculate maximum cumulative returns for the strategy

ticker_history['cumulative_strategy_max'] = ticker_history['cumulative_strategy_returns'].cummax()

# Calculate the drawdown for the strategy

ticker_history['cumulative_strategy_drawdown'] = (ticker_history['cumulative_strategy_returns'] / ticker_history['cumulative_strategy_max']) - 1

# Add drawdown to the matrix of drawdowns

dd_matrix.loc[fast_ma, slow_ma] = ticker_history['cumulative_strategy_drawdown'][-1]

# Make a copy of the drawdown matrix and convert the index and columns to string type

values_dd = dd_matrix.copy()

values_dd.index = values_dd.index.astype(str)

values_dd.columns = values_dd.columns.astype(str)

# Convert values to float type

values_dd = values_dd.astype(float)

# Change the style of the plot and set the default color scheme

plt.style.use('dark_background')

sns.set_palette("bright")

# Create a heatmap with the provided values, including annotations, using the RdYlGn color map

sns.heatmap(values_dd, annot=True, cmap='RdYlGn')

# Add labels to the axes

plt.xlabel('Slow Moving Average', fontsize=12, color='white')

plt.ylabel('Fast Moving Average', fontsize=12, color='white')

# Add a title to the plot

plt.title('Heatmap of Drawdowns', fontsize=16, color='white')

# Increase the font size to 0.8 and change the color to white for all text elements

sns.set(font_scale=0.8, rc={'text.color':'white', 'axes.labelcolor':'white', 'xtick.color':'white', 'ytick.color':'white'})

# Change the background color of the plot to black

fig = plt.gcf()

fig.set_facecolor('#000000')

# Display the plot

plt.show()

Predicted RNN Trading Strategy Returns

- Downloading 15-min NVDA data from yfinance

import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

from keras.layers import Dense, SimpleRNN, Dropout

from keras.optimizers import Adam

# Download 15-minute NVDA data from yfinance

nvd = yf.Ticker('NVDA')

data = nvd.history(interval='15m', start='2023-10-03', end='2023-10-17')

# Reset the index to make 'Date' a regular column

data = data.reset_index()

data.tail()

- Implementing the RNN price prediction model

scaler = MinMaxScaler(feature_range=(0, 1))

scaled_data = scaler.fit_transform(data['Close'].values.reshape(-1, 1))

# Create training and testing datasets

def create_dataset(scaled_data, lookback=160):

X, y = [], []

for i in range(lookback, len(scaled_data)):

X.append(scaled_data[i - lookback:i, 0])

y.append(scaled_data[i, 0])

return np.array(X), np.array(y)

lookback = 160

train_ratio = 0.95

train_size = int(len(scaled_data) * train_ratio)

train_data = scaled_data[:train_size]

test_data = scaled_data[train_size - lookback:]

X_train, y_train = create_dataset(train_data, lookback)

X_test, y_test = create_dataset(test_data, lookback)

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

# Build the RNN model

model = Sequential()

model.add(SimpleRNN(50, return_sequences=True, input_shape=(X_train.shape[1], 1)))

model.add(Dropout(0.2))

model.add(SimpleRNN(50, return_sequences=True))

model.add(Dropout(0.2))

model.add(SimpleRNN(50))

model.add(Dropout(0.2))

model.add(Dense(1))

model.compile(optimizer=Adam(lr=0.001), loss='mean_squared_error')

# Train the model

model.fit(X_train, y_train, epochs=100, batch_size=64)

# Make predictions

predicted_prices = model.predict(X_test)

predicted_prices = scaler.inverse_transform(predicted_prices)

# Evaluate the model

rmse = np.sqrt(np.mean((predicted_prices - y_test)**2))

print('Root Mean Squared Error:', rmse)

# Plotting the predicted against the actual

num_test_points = len(X_test)

test_datetime_values = data.iloc[-num_test_points:, 0]

# Inverse transform the actual prices (y_test)

actual_prices = scaler.inverse_transform(y_test.reshape(-1, 1))

# Plot actual and predicted stock prices

fig=plt.figure(figsize=(12, 5))

import matplotlib as mpl

mpl.rcParams['text.color'] = 'blue'

mpl.rcParams.update({'font.size': 22})

mpl.rcParams['xtick.labelcolor'] = 'blue'

mpl.rcParams['xtick.color'] = 'blue'

mpl.rcParams['ytick.labelcolor'] = 'blue'

mpl.rcParams['ytick.color'] = 'blue'

plt.plot(test_datetime_values, actual_prices, label='Actual Prices',lw=4)

plt.plot(test_datetime_values, predicted_prices, label='Predicted Prices',lw=4)

font1 = {'family':'sans-serif','color':'blue','size':20}

plt.xlabel('Datetime',fontdict = font1)

plt.ylabel('Stock Prices',fontdict = font1)

plt.title('NVDA Stock Price Prediction')

plt.rcParams.update({'text.color': "blue",

'axes.labelcolor': "blue"})

plt.legend()

SMALL_SIZE = 16

MEDIUM_SIZE = 16

BIGGER_SIZE = 16

plt.rc('font', size=SMALL_SIZE) # controls default text sizes

plt.rc('axes', titlesize=SMALL_SIZE) # fontsize of the axes title

plt.rc('axes', labelsize=MEDIUM_SIZE) # fontsize of the x and y labels

plt.rc('xtick', labelsize=SMALL_SIZE) # fontsize of the tick labels

plt.rc('ytick', labelsize=SMALL_SIZE) # fontsize of the tick labels

plt.rc('legend', fontsize=SMALL_SIZE) # legend fontsize

plt.rc('figure', titlesize=BIGGER_SIZE) # fontsize of the figure

plt.grid(c='black')

plt.show()

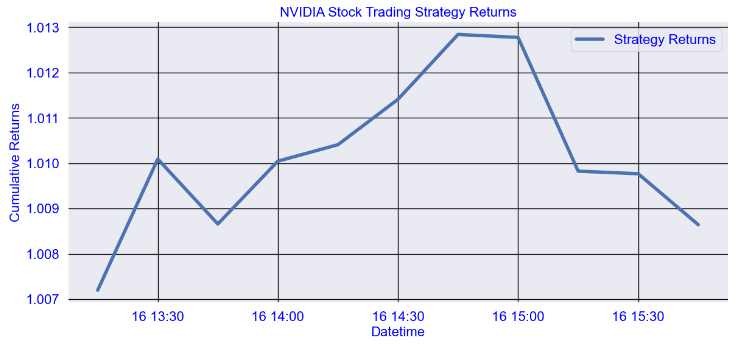

- Plotting cumulative RNN strategy returns

# Calculate the percentage change in predicted prices

predicted_pct_change = np.diff(predicted_prices.reshape(-1)) / predicted_prices[:-1].reshape(-1)

# Get the actual prices corresponding to the predicted_prices in the test set

actual_prices_test = actual_prices[-len(predicted_prices) + 1:]

# Calculate the percentage change in actual prices

actual_pct_change = np.diff(actual_prices_test.reshape(-1)) / actual_prices_test[:-1].reshape(-1)

# Truncate the longer array if the lengths are not equal

if len(predicted_pct_change) != len(actual_pct_change):

min_len = min(len(predicted_pct_change), len(actual_pct_change))

predicted_pct_change = predicted_pct_change[:min_len]

actual_pct_change = actual_pct_change[:min_len]

# Create a trading strategy based on the predicted percentage change

strategy_returns = np.where(predicted_pct_change > 0, 1, -1) * actual_pct_change

# Calculate the cumulative returns

cumulative_returns = (1 + strategy_returns).cumprod()

# Plot the cumulative returns

import matplotlib as mpl

mpl.rcParams['text.color'] = 'blue'

plt.figure(figsize=(14, 6))

plt.plot(data['Datetime'].iloc[-len(cumulative_returns):], cumulative_returns, label='Strategy Returns',lw=4)

plt.xlabel('Datetime')

plt.ylabel('Cumulative Returns')

plt.title('NVIDIA Stock Trading Strategy Returns')

plt.legend()

plt.grid(c='black')

plt.show()

- Predicting RNN mean reversion strategy returns

import yfinance as yf

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import LSTM, Dense, Dropout

from tensorflow.keras.layers import SimpleRNN

# Download 15-minute NVIDIA data from yfinance

tesla = yf.download('NVDA', start='2023-10-03', end='2023-10-17', interval='15m')

# Reset the index

tesla.reset_index(inplace=True)

# Preprocess data

data = tesla[['Close']]

scaler = MinMaxScaler(feature_range=(0, 1))

scaled_data = scaler.fit_transform(data)

# Create a Function that generates 'good' data for the process

def create_dataset(data, lookback):

features, targets = [], []

for i in range(lookback, len(data)):

features.append(data[i-lookback:i])

targets.append(data[i, 0])

return np.array(features), np.array(targets)

lookback = 60

mean_reversion_features, mean_reversion_targets = create_dataset(scaled_data, lookback)

# Split data into train and test

train_size = int(len(mean_reversion_features) * 0.8)

X_train_mean_reversion, y_train_mean_reversion = mean_reversion_features[:train_size], mean_reversion_targets[:train_size]

X_test_mean_reversion, y_test_mean_reversion = mean_reversion_features[train_size:], mean_reversion_targets[train_size:]

X_train_mean_reversion = X_train_mean_reversion.reshape((X_train_mean_reversion.shape[0], X_train_mean_reversion.shape[1], 1))

X_test_mean_reversion = X_test_mean_reversion.reshape((X_test_mean_reversion.shape[0], X_test_mean_reversion.shape[1], 1))

def create_rnn_model(lookback):

model = Sequential()

model.add(SimpleRNN(units=50, return_sequences=True, input_shape=(lookback, 1)))

model.add(SimpleRNN(units=50, return_sequences=False))

model.add(Dense(units=25))

model.add(Dense(units=1))

model.compile(optimizer='adam', loss='mean_squared_error')

return model

mean_reversion_rnn = create_rnn_model(lookback)

# Train the model

mean_reversion_rnn.fit(X_train_mean_reversion, y_train_mean_reversion, epochs=5, batch_size=32)

# Generate predictions

y_test_mean_reversion = mean_reversion_rnn.predict(X_test_mean_reversion)

# Calculate the z-score of predicted mean reversion values

z_scores = (y_test_mean_reversion - y_test_mean_reversion.mean()) / y_test_mean_reversion.std()

# Define z-score threshold for buy and sell signals

z_threshold = 1

# Generate trading signals

mean_reversion_signals = np.where(z_scores > z_threshold, -1, np.where(z_scores < -z_threshold, 1, 0))

last_train_index = tesla.index[train_size + lookback - 1]

returns = np.diff(tesla.loc[last_train_index + 1:, 'Close'].values) * mean_reversion_signals.flatten()[:-1]

# Calculate cumulative returns

cumulative_returns = np.cumsum(returns)

# Plot cumulative returns

plt.figure(figsize=(14, 6))

plt.plot(tesla.loc[last_train_index + 2:, 'Datetime'].values, cumulative_returns, label='Mean Reversion Strategy Returns',lw=4)

plt.xlabel('Datetime')

plt.ylabel('Cumulative Returns')

plt.legend()

plt.grid(c='black')

plt.show()

Summary

- The 10Y MVA optimized strategy 40-200 yields cumulative return of 130% and max drawdown of -16%. The choice of different MVAs can affect the results of the MVA strategy. In addition, commissions should be added to the analysis, as well as the effect of slippage.

- The 14-day RNN mean reversion strategy cumulative return is 3%. There are significant plateau periods in both the actual data (when the markets are closed) and the model returns for the same reason.

Explore More

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment