- Today the focus is on risk assessment of top blue chips (NVDA, ORCL, AMD, AAPL, INTC, AMZN, GE, XOM, TSLA, MSFT, WMT, PG, KO, JNJ, BAC, NKE, HON, GS, and ^GSPC) using the IQR-based real-time volatility ranking algorithm and the corresponding Python functions.

- The objective is to determine market regimes using standard deviation (STD) of log-domain stock prices. It allows us to assess how values in a dataset are distributed around the mean.

- Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

- Consider the class Levels

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

class Levels:

def run(self):

df = self.read_file()

df = self.calc_std_dev_levels(df)

self.plot_levels(df)

def read_file(self):

filename = 'data.csv'

df = pd.read_csv(filename, names=['receive_timestamp', 'price'])

df['receive_timestamp'] = pd.to_datetime(df['receive_timestamp'])

df.set_index('receive_timestamp', inplace=True)

return df

def calc_std_dev_levels(self, df):

#log price

df['price'] = df['price'].apply(np.log)

#price difference

df['price_diff'] = df['price'].diff()

#std dev

df['std_dev'] = df['price_diff'].rolling(window=100).std()

#use rolling mean to find 'zones' of volatility

df['std_dev_ma'] = df['std_dev'].rolling(3000).mean()

#thresholds between levels

std_dev_ma_threshold_1 = df['std_dev_ma'].quantile(0.2)

std_dev_ma_threshold_2 = df['std_dev_ma'].quantile(0.4)

std_dev_ma_threshold_3 = df['std_dev_ma'].quantile(0.6)

std_dev_ma_threshold_4 = df['std_dev_ma'].quantile(0.8)

# Initialize 'signal' column with zeros

df['levels'] = 0

#assign levels based on average std dev

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_1), 'levels'] = 1

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_2), 'levels'] = 2

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_3), 'levels'] = 3

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_4), 'levels'] = 4

return df

def plot_levels(self, df):

fig, ax = plt.subplots()

colors = {

0:'grey',

1:'green',

2: 'blue',

3: 'red',

4: 'black'

}

scatter = ax.scatter(

np.reshape(df.index, -1),

np.reshape(df['price'], -1),

c=np.reshape(df['levels'].apply(lambda x: colors[x]), -1),

s=10,

linewidths=1

)

# Create proxy artists for legend

legend_labels = [f'Level {level}' for level in colors.keys()]

legend_handles = [mpatches.Patch(color=colors[level], label=label) for level, label in enumerate(legend_labels)]

# Create a legend

ax.legend(handles=legend_handles, title='Levels')

plt.title('std dev levels')

plt.xlabel('Date')

plt.ylabel('Price')

plt.grid(True)

plt.show()

- Let’s test this class using the high-volatility segment data.csv

if __name__ == '__main__':

v = Levels()

v.run()

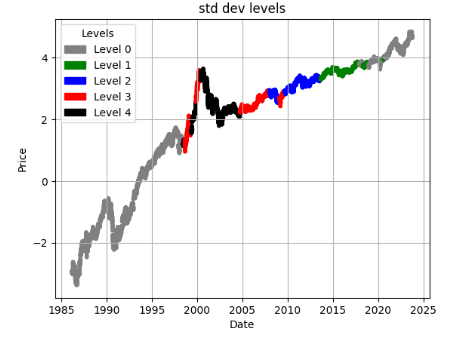

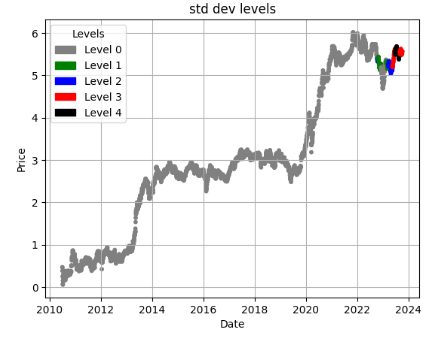

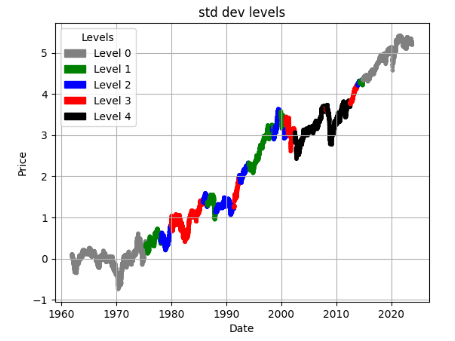

- Let’s take a closer look at the output

- Clearly, we can create a price chart and mark our levels. The faster the price changes, the higher the volatility and STD. Level 0 will correspond to the lowest volatility, with each subsequent group representing higher volatility. Gray and green zones represent low volatility, while red and black indicate the most volatile segments.

- Let’s replace the above class with the following two functions

# Importing Libraries

# Data Handling

import pandas as pd

import numpy as np

# Financial Data Analysis

import yfinance as yf

# Data Visualization

import plotly.express as px

import plotly.graph_objs as go

import plotly.subplots as sp

from plotly.subplots import make_subplots

import plotly.figure_factory as ff

import plotly.io as pio

from IPython.display import display

from plotly.offline import init_notebook_mode

# Statistics & Mathematics

import scipy.stats as stats

import statsmodels as sm

from scipy.stats import shapiro, skew

import math

# Hiding warnings

import warnings

warnings.filterwarnings("ignore")

def load_and_preprocess(ticker):

'''

This function takes in a ticker symbol, which is used to

retrieve historical data from Yahoo Finance.

The attributes 'Returns', and the Adjusted Low, High, and Open

are created.

NaNs are filled with 0s

'''

df = yf.download(ticker)

df['Returns'] = df['Adj Close'].pct_change(1)

df['Adj Low'] = df['Low'] - (df['Close'] - df['Adj Close'])

df['Adj High'] = df['High'] - (df['Close'] - df['Adj Close'])

df['Adj Open'] = df['Open'] - (df['Close'] - df['Adj Close'])

df = df.fillna(0)

return df

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

def plot_levels(df):

#log price

df['price'] = df['Adj Close'].apply(np.log)

#price difference

df['price_diff'] = df['price'].diff()

#std dev

df['std_dev'] = df['price_diff'].rolling(window=100).std()

#use rolling mean to find 'zones' of volatility

df['std_dev_ma'] = df['std_dev'].rolling(3000).mean()

#thresholds between levels

std_dev_ma_threshold_1 = df['std_dev_ma'].quantile(0.2)

std_dev_ma_threshold_2 = df['std_dev_ma'].quantile(0.4)

std_dev_ma_threshold_3 = df['std_dev_ma'].quantile(0.6)

std_dev_ma_threshold_4 = df['std_dev_ma'].quantile(0.8)

# Initialize 'signal' column with zeros

df['levels'] = 0

#assign levels based on average std dev

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_1), 'levels'] = 1

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_2), 'levels'] = 2

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_3), 'levels'] = 3

df.loc[(df['std_dev_ma'] > std_dev_ma_threshold_4), 'levels'] = 4

fig, ax = plt.subplots()

colors = {

0:'grey',

1:'green',

2: 'blue',

3: 'red',

4: 'black'

}

scatter = ax.scatter(

np.reshape(df.index, -1),

np.reshape(df['price'], -1),

c=np.reshape(df['levels'].apply(lambda x: colors[x]), -1),

s=10,

linewidths=1

)

# Create proxy artists for legend

legend_labels = [f'Level {level}' for level in colors.keys()]

legend_handles = [mpatches.Patch(color=colors[level], label=label) for level, label in enumerate(legend_labels)]

# Create a legend

ax.legend(handles=legend_handles, title='Levels')

plt.title('std dev levels')

plt.xlabel('Date')

plt.ylabel('Price')

plt.grid(True)

plt.show()

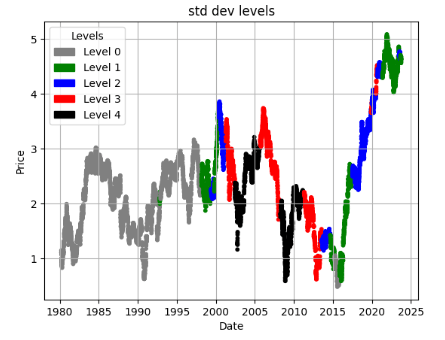

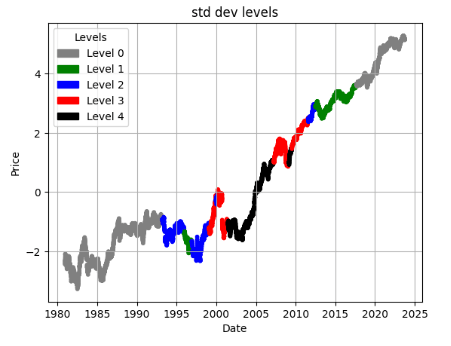

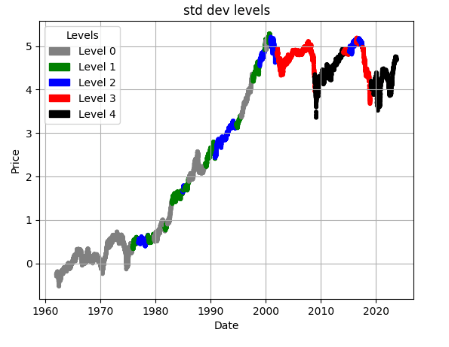

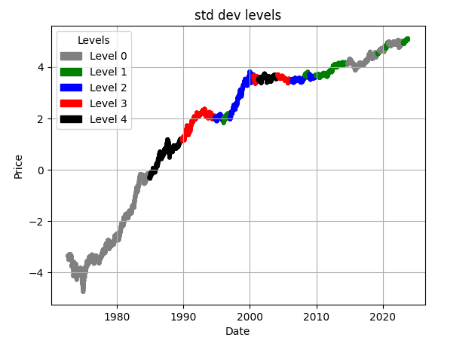

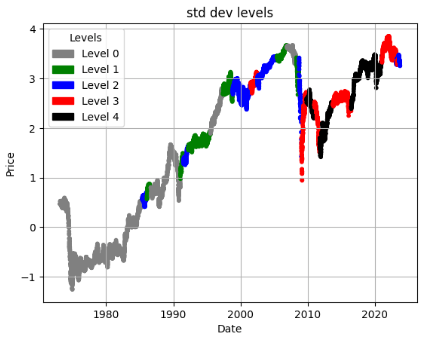

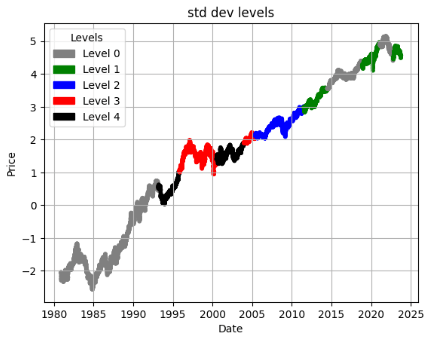

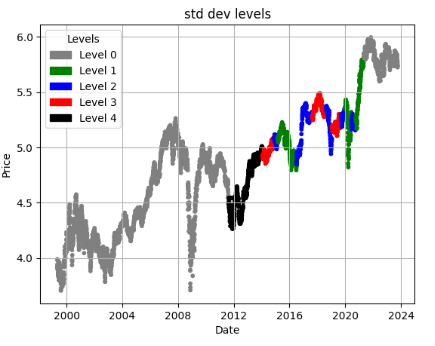

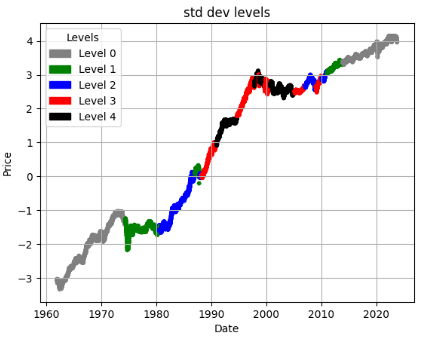

- Now, we can examine price := (log Adj Close price) charts of stocks and mark their STD levels as follows

ticker = 'NVDA'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'ORCL'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'AMD'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'XOM'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'AAPL'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'INTC'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'AMZN'

df = load_and_preprocess(ticker) # Loading and Transforming Dataframe

plot_levels(df)

ticker = 'GE'

df = load_and_preprocess(ticker) # Loading and Transforming Dataframe

plot_levels(df)

ticker = 'TSLA'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'MSFT'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'WMT'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'PG'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'JNJ'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'BAC'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = '^GSPC'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'NKE'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'HON'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'GS'

df = load_and_preprocess(ticker)

plot_levels(df)

ticker = 'KO'

df = load_and_preprocess(ticker)

plot_levels(df)

Summary

- These plots can be interpreted in various ways: (1) you can enable or disable your trading/investment strategies using the proposed IQR-based market’s volatility levels 0-4; (2) traders or investors can determine the distance from the mean price at which they place their orders.

- On a risk-adjusted basis, low-to-moderate volatility stocks (NVDA, ORCL, INTC, AMZN, AAPL, PG, HON, KO, and JNJ) can be superior investments in 2023 and beyond.

- Highly volatile stocks (XOM, GE, BAC, TSLA, and ^GSPC) offer the most profit potential but are equally susceptible to losses in Q4’23: traders can take advantage of short-term strategies to trade the momentum. Highly volatile stocks can earn profits for a short lock-in period.

- Taking a long-term investment view well beyond 2023 is important for stocks with moderate volatility levels such as AMD, MSFT, WMT, NKE, and GS.

Explore More

- Blue-Chip Stock Portfolios for Quant Traders

- Multiple-Criteria Technical Analysis of Blue Chips in Python

- Are Blue Chips Perfect for This Bear Market?

- Advanced Integrated Data Visualization (AIDV) in Python – 1. Stock Technical Indicators

- Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

- 360-Deg Revision of Risk Aware Investing after SVB Collapse – 1. The Financial Sector

- Portfolio max(Return/Risk) Stochastic Optimization of 20 Dividend Growth Stocks

- The Zacks Market Outlook Nov ’22 – Energy

- The CodeX-Aroon Auto-Trading Approach – the AAPL Use Case

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- S&P 500 Algorithmic Trading with FBProphet

- Inflation-Resistant Stocks to Buy

- Risk-Return Analysis and LSTM Price Predictions of 4 Major Tech Stocks in 2023

One-Time

Monthly

Yearly

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

€5.00

€15.00

€100.00

Or enter a custom amount

€

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment