In this post, we will apply the Guillen’s asset rebalancing algorithm (cf. the Python code) to the following risk-aware portfolio:

stocks = [‘SPY‘, ‘XOM‘, ‘ABBV‘, ‘AZN‘, ‘LMT‘]

The initial portfolio value to be allocated is

portfolio_value = 10**6

and the weight allocation per asset is

weights = [0.15 , 0.30, 0.40, 0.075, 0.075]

Conventionally, our benchmark is S&P500

benchmark = ‘^GSPC’

The time factors are as follows:

Start date 2013-01-02

End date 2023-03-17

In-sample months 83

Out-of-sample months 38

Download Input Data

Let’s set the working directory

import os os.chdir(‘YOURPATH’)

os. getcwd()

and

import the libraries

import yfinance as yf

import pandas as pd

import numpy as np

import pyfolio as py

import plotly.graph_objs as go

from plotly.subplots import make_subplots

import warnings

warnings.filterwarnings(“ignore”)

followed by the above-mentioned user input parameters.

Let’s download the data

stock_data = yf.download(stocks, start=start_date)[‘Adj Close’]

stock_data = stock_data.dropna()

stock_data = stock_data.reindex(columns=stocks)

stock_prices = stock_data[stocks].values

[*********************100%***********************] 5 of 5 completed

and define the shares dataframe

shares_df = pd.DataFrame(index=[stock_data.index[0]])

for s,w in zip(stocks, weights):

shares_df[s + ‘_shares’] = np.floor((portfolio_value * np.array(w)) / stock_data[s][0])

shares_df

Rebalancing Engine Run

- Initialize variables

balance_year = stock_data.index[0].year # Since we rebalance based on year

signal = False

count = 0 # for loop count purpose

Store previous values in a dictionary

prev_values = {}

- Calculate portfolio value for the first day by mult. shares * price per asset at t=0

portfolio_value = sum([shares_df.loc[stock_data.index[0], s + ‘_shares’] * stock_data.loc[stock_data.index[0], s] for s in stocks])

for day in stock_data.index:

count += 1

if day == stock_data.index[0]:

shares_df.loc[day] = shares_df.loc[day] # First day

# Store initial values as previous values

for col in shares_df.columns:

prev_values[col] = shares_df.loc[day, col]

elif day.year != balance_year: # THIS IS OUR SIGNAL

signal = True

# calculate new shares based on the new portfolio value and weights

new_shares = [np.floor((portfolio_value * w) / stock_data[s][day]) for s,w in zip(stocks, weights)]

shares_df.loc[day, :] = new_shares

balance_year = day.year

count += 1

# print(f'Rebalance: {day.date()}, count: {count}') # uncomment to debug days 😉

# Store new values as previous values

for col in shares_df.columns:

prev_values[col] = shares_df.loc[day, col]

else:

signal = False

# Use previous values if it is not a rebalancing date

shares_df.loc[day, :] = [prev_values[col] for col in shares_df.columns]

# print(f'Not rebalance, regular day: {day.date()}') # uncomment to debug days 😉

# Calculate asset values and portfolio value for the current day

asset_values = [shares_df.loc[day, s + '_shares'] * stock_data.loc[day, s] for s in stocks]

portfolio_value = sum(asset_values)

stock_data.loc[day, 'Signal'] = signal

stock_data.loc[day, 'Portfolio_Value'] = portfolio_value

# Add shares to stock data frame to have all together

for s in stocks:

stock_data.loc[day, s + '_shares'] = shares_df.loc[day, s + '_shares']

stock_data.loc[day, s + '_value'] = shares_df.loc[day, s + '_shares'] * stock_data.loc[day, s]

Calculate log returns for portfolio

stock_data[‘Portfolio_Value_rets’] = np.log(stock_data[‘Portfolio_Value’] / stock_data[‘Portfolio_Value’].shift(1))

Calculate log returns for each stock and asset weight

for stock in stocks:

stock_data[f'{stock}_rets’] = np.log(stock_data[stock] / stock_data[stock].shift(1))

stock_data[stock + ‘_weight’] = stock_data[stock + ‘_value’] / stock_data[‘Portfolio_Value’]

Benchmark data download and return

start_date_benchmark = stock_data.index[0]

benchmark_data = yf.download(benchmark, start=start_date_benchmark)

benchmark_data = benchmark_data.dropna()

benchmark_data[‘benchmark_rets’] = np.log(benchmark_data[‘Adj Close’] / benchmark_data[‘Adj Close’].shift(1))

benchmark_data[‘benchmark_rets’] = benchmark_data[‘benchmark_rets’].dropna()

[*********************100%***********************] 1 of 1 completed

Data timezone UTC unification for pyfolio valuation

stock_data.index = stock_data.index.tz_localize(‘UTC’)

benchmark_data.index = benchmark_data.index.tz_localize(‘UTC’)

live_date = pd.Timestamp(live_date, tz=’UTC’)

Output Data Visualization

from IPython.core.display import display, HTML

display(HTML(“”))

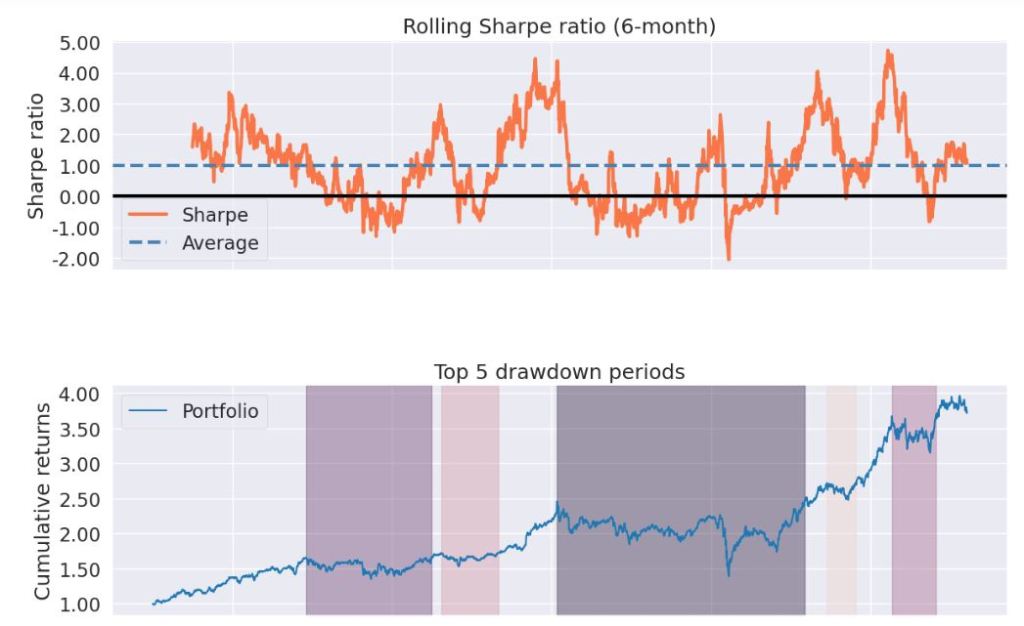

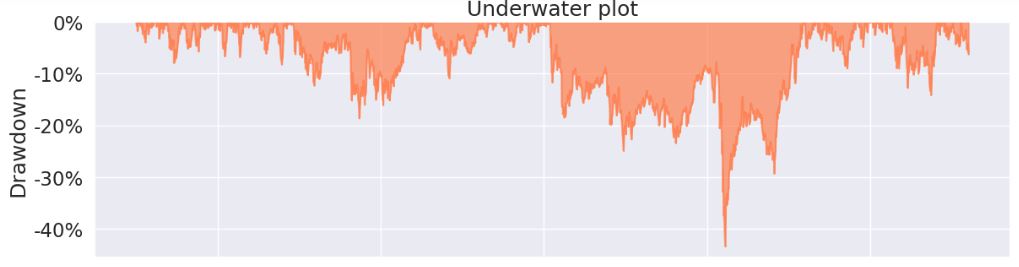

py.create_full_tear_sheet(stock_data[‘Portfolio_Value_rets’], benchmark_rets = benchmark_data[‘benchmark_rets’], live_start_date = live_date)

2014 2016 2018 2020 2022

Summary

We have implemented the following portfolio rebalancing strategy in Python:

- Define the assets, weights, and initial capital for investment.

- Select the benchmark and relevant dates.

- Assign initial capital to each asset based on desired weights.

- Implement the rebalancing engine based on monthly, yearly, daily, or signal-based triggers.

- Monitor the portfolio’s performance numerically or visually and extract insights.

Our output out-of-sample data are as follows:

- Return at End date (2023-03-17): 3.5+/- 2 %

- Annual return 17.3%

- Cumulative returns 66.6%

- Annual volatility 23.4%

- Max drawdown -38.6%

- Calmar ratio 0.45

- Sharpe ratio 0.8

- Omega ratio 1.16

- Sortino ratio 1.09

- Alpha 0.15

- Beta 0.72

- 4 stress events

- 5 drawdown periods

Explore More

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- Risk/Return POA – Dr. Dividend’s Positions

- Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

- Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

- Stock Portfolio Risk/Return Optimization

- Stock Market ’22 Round Up & ’23 Outlook: Zacks Strategy vs Seeking Alpha Tactics

- XOM SMA-EMA-RSI Golden Crosses ’22

- Python Technical Analysis for BioTech – Get Buy Alerts on ABBV in 2023

- A Comparative Analysis of The 3 Best Global Growth Stocks in Q1’23 – 2. AZN

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment