The goal of portfolio optimization is to build a stock portfolio that yields the maximum possible return while maintaining the amount of risk you’re willing to carry.

Referring to our previous case study, let’s invoke the stochastic optimization algorithm and the corresponding code to create an optimized portfolio by testing 10,000 combinations of the following 20 dividend growth stocks:

Table of Contents

Input Data Preparation

Let’s define the following input parameters

Tickers:

benchmark_ = [“^GSPC”]

portfolio_ = [‘V’, ‘O’, ‘HD’, ‘MO’, ‘WM’,’NEE’,’PEP’,’CAT’,’UNH’,’MCD’,’XOM’,’UNP’,’CNQ’,’LMT’,’BLK’,’AAPL’,’MSFT’,’SBUX’,’ASML’,

‘COST’]

Dates:

start_date_ = “2022-01-01”

end_date_ = “2023-03-03”

trade_days_per_year = 252

Stochastic Simulations:

number_of_scenarios = 10000

Risk %:

delta_risk = 0.1

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and import the following libraries

import yfinance as yf

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import squarify

import seaborn as sb

Let’s download our stock and benchmark data

return_vector = []

risk_vector = []

distrib_vector = []

df = yf.download(benchmark_, start=start_date_, end=end_date_)

df2 = yf.download(portfolio_, start=start_date_, end=end_date_)

Clean Rows with No Values on both Benchmark and Portfolio

df = df.dropna(axis=0)

df2 = df2.dropna(axis=0)

Matching the Days

df = df[df.index.isin(df2.index)]

[*********************100%***********************] 1 of 1 completed [*********************100%***********************] 5 of 5 completed

df.tail()

df.shape

(292, 6)

df2.shape

(292, 120)

df.info()

<class 'pandas.core.frame.DataFrame'> DatetimeIndex: 292 entries, 2022-01-03 to 2023-03-02 Data columns (total 6 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Open 292 non-null float64 1 High 292 non-null float64 2 Low 292 non-null float64 3 Close 292 non-null float64 4 Adj Close 292 non-null float64 5 Volume 292 non-null int64 dtypes: float64(5), int64(1) memory usage: 16.0 KB

df2.columns

MultiIndex([('Adj Close', 'AAPL'),

('Adj Close', 'ASML'),

('Adj Close', 'BLK'),

('Adj Close', 'CAT'),

('Adj Close', 'CNQ'),

('Adj Close', 'COST'),

('Adj Close', 'HD'),

('Adj Close', 'LMT'),

('Adj Close', 'MCD'),

('Adj Close', 'MO'),

...

( 'Volume', 'MSFT'),

( 'Volume', 'NEE'),

( 'Volume', 'O'),

( 'Volume', 'PEP'),

( 'Volume', 'SBUX'),

( 'Volume', 'UNH'),

( 'Volume', 'UNP'),

( 'Volume', 'V'),

( 'Volume', 'WM'),

( 'Volume', 'XOM')],

length=120)

df.describe()

df2.describe().T

Portfolio/Benchmark Analysis

Analysis of Benchmark:

benchmark_vector = np.array(df[‘Close’])

Create our Daily Returns

benchmark_vector = np.diff(benchmark_vector)/benchmark_vector[1:]

Select or Final Return and Risk

benchmark_return = np.average(benchmark_vector)

benchmark_risk = np.std(benchmark_vector)

Add our Benchmark info to our lists

return_vector.append(benchmark_return)

risk_vector.append(benchmark_risk)

Analysis of Portfolio

portfolio_vector = np.array(df2[‘Close’])

Create a loop for the number of scenarios we want:

for i in range(number_of_scenarios):

#Create a random distribution that sums 1

# and is split by the number of stocks in the portfolio

random_distribution = np.random.dirichlet(np.ones(len(portfolio_)),size=1)

distrib_vector.append(random_distribution)

#Find the Closing Price for everyday of the portfolio

portfolio_matmul = np.matmul(random_distribution,portfolio_vector.T)

#Calculate the daily return

portfolio_matmul = np.diff(portfolio_matmul)/portfolio_matmul[:,1:]

#Select or Final Return and Risk

portfolio_return = np.average(portfolio_matmul, axis=1)

portfolio_risk = np.std(portfolio_matmul, axis=1)

#Add our Benchmark info to our lists

return_vector.append(portfolio_return[0])

risk_vector.append(portfolio_risk[0])

Create Risk Boundaries with the given delta_risk

min_risk = np.min(risk_vector)

max_risk = risk_vector[0]*(1+delta_risk)

risk_gap = [min_risk, max_risk]

Portfolio Return and Risk Couple

portfolio_array = np.column_stack((return_vector,risk_vector))[1:,]

Rule to create the best portfolio

If the criteria of minimum risk is satisfied then:

if np.where(((portfolio_array[:,1]<= max_risk)))[0].shape[0]>1:

min_risk_portfolio = np.where(((portfolio_array[:,1]<= max_risk)))[0]

best_portfolio_loc = portfolio_array[min_risk_portfolio]

max_loc = np.argmax(best_portfolio_loc[:,0])

best_portfolio = best_portfolio_loc[max_loc]

If the criteria of minimum risk is not satisfied then:

else:

min_risk_portfolio = np.where(((portfolio_array[:,1]== np.min(risk_vector[1:]))))[0]

best_portfolio_loc = portfolio_array[min_risk_portfolio]

max_loc = np.argmax(best_portfolio_loc[:,0])

best_portfolio = best_portfolio_loc[max_loc]

Let’s plot the summary of yearly portfolio average return vs standard deviation: portfolio scenarios, market proxy values, and best performer.

risk_gap = np.array(risk_gap)

best_portfolio[0] = np.array(best_portfolio[0])

x = np.array(risk_vector)

y = np.array(return_vector)*trade_days_per_year

fig, ax = plt.subplots(figsize=(20, 15))

plt.rc(‘axes’, titlesize=14) # Controls Axes Title

plt.rc(‘axes’, labelsize=14) # Controls Axes Labels

plt.rc(‘xtick’, labelsize=14) # Controls x Tick Labels

plt.rc(‘ytick’, labelsize=14) # Controls y Tick Labels

plt.rc(‘legend’, fontsize=14) # Controls Legend Font

plt.rc(‘figure’, titlesize=14) # Controls Figure Title

ax.scatter(x, y, alpha=0.5,

linewidths=0.1,

edgecolors=’black’, s=20,

label=’Portfolio Scenarios’

)

ax.scatter(x[0],

y[0],

color=’red’,

linewidths=1, s=180,

edgecolors=’black’,

label=’Market Proxy Values’)

ax.scatter(best_portfolio[1],

best_portfolio[0],

color=’green’,

linewidths=1, s=180,

edgecolors=’black’,

label=’Best Performer’)

ax.axvspan(min_risk,

max_risk,

color=’red’,

alpha=0.08,

label=’Accepted Risk Zone’)

ax.set_ylabel(“Yearly Portfolio Average Return (%)”,fontsize=14)

ax.set_xlabel(“Yearly Portfolio Standard Deviation”,fontsize=14)

ax.axhline(y=0, color=’black’,alpha=0.5)

ax = plt.gca()

ax.legend(loc=0)

vals = ax.get_yticks()

ax.set_yticklabels([‘{:,.2%}’.format(x) for x in vals])

plt.savefig(‘risk_optimizer2023.png’, dpi=300)

Output Data Visualization

let’s look at the Output Table of Distributions

portfolio_loc = np.where((portfolio_array[:,0]==(best_portfolio[0]/trade_days_per_year))&(portfolio_array[:,1]==(best_portfolio[1])))[0][0]

best_distribution = distrib_vector[portfolio_loc][0].tolist()

d = {“Stock Name”: portfolio_, “Stock % in Portfolio”: best_distribution}

output = pd.DataFrame(d)

output = output.sort_values(by=[“Stock % in Portfolio”],ascending=False)

output= output.style.format({“Stock % in Portfolio”: “{:.2%}”})

output

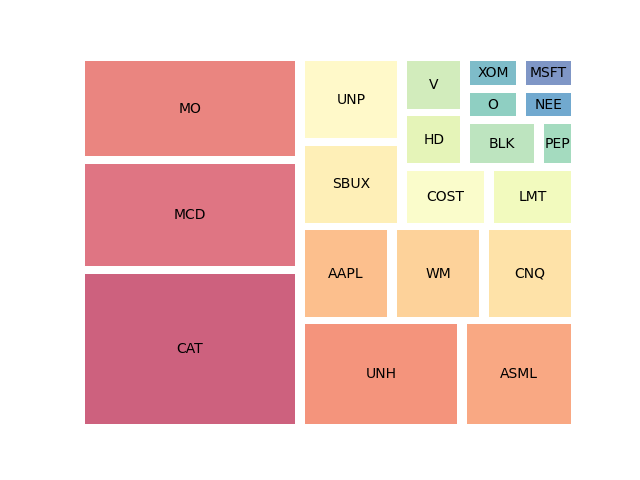

The can approximate this distribution by the squarify matrix proxy

episode_data =[20,14,13,10,7,5,5,5,5,5,3,3,2,2,2,1,1,1,1,1]

anime_names = [‘CAT’,’MCD’,’MO’,’UNH’,’ASML’,’AAPL’,’WM’,’CNQ’,’SBUX’,’UNP’,’COST’,’LMT’,’HD’,’V’,’BLK’,’PEP’,’O’,’XOM’,’NEE’,’MSFT’]

squarify.plot(episode_data, label=anime_names,color=sb.color_palette(“Spectral”,

len(episode_data)),alpha=.7,pad=2)

plt.axis(“off”)

plt.savefig(‘squarify20stocks.png’)

Summary

In this post, we have invoked the stochastic portfolio optimization algorithm to create a balanced portfolio of 20 dividend growth stocks suggested by @DrDividend47. Results allow us to spread our investment capital across a variety of assets. As a result, we can balance those assets in order to attain our desired min (risk) and max(reward) outcome whilst outperforming the benchmark index ^GSPC.

Explore More

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- Risk/Return POA – Dr. Dividend’s Positions

- Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

- Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

- Stock Portfolio Risk/Return Optimization

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment