Featured Image by TradingView.com

In this article, we will implement the CodeX-Aroon auto-trading strategy to examine the AAPL stock 2022 in terms of stock trends, trading signals, positions, backtesting, and benchmarking against SPY ETF.

Contents:

Aroon Indicator

The Aroon Indicator (often referred to as Aroon Up Down) is a range bound, technical indicator that is actually a set of two separate measurements designed to measure how many periods have passed since price has recorded an n-period high or low with “n” being a number of periods set at the trader’s discretion. For example a 25 Day (long-term) Aroon-Up will take the number of days since price last recorded a 25 day high and then calculate a number between 0 and 100. A 25 Day Aroon-Down will do the same thing except is will calculate a number based of the number of days since a 25 day low. This number is intended to quantify the strength of a trend (if there is one). The closer the number is to 100, the stronger the trend. Aroon is not only good at identifying trends, it is also a useful tool for identifying periods of consolidation.

Auto-Trading

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and import the key libraries

import pandas as pd

import numpy as np

import requests

import matplotlib.pyplot as plt

from math import floor

from termcolor import colored as cl

plt.style.use(‘fivethirtyeight’)

plt.rcParams[‘figure.figsize’] = (20, 10)

We need to define the following user parameters

myticker=’AAPL’

mydate=’2022-01-01′

myamount=10000

mywin=25

Let’s get the AAPL historical data using the API key linked to the user account on twelvedata.com

def get_historical_data(symbol, start_date):

api_key = ‘API key’

api_url = f’https://api.twelvedata.com/time_series?symbol={symbol}&interval=1day&outputsize=5000&apikey={api_key}’

raw_df = requests.get(api_url).json()

df = pd.DataFrame(raw_df[‘values’]).iloc[::-1].set_index(‘datetime’).astype(float)

df = df[df.index >= start_date]

df.index = pd.to_datetime(df.index)

return df

tsla = get_historical_data(myticker, mydate)

tsla

let’s calculate the Aroon up/down indicators

def get_aroon(symbol, lookback, start_date):

api_key = ‘API key’

api_url = f’https://api.twelvedata.com/aroon?symbol={symbol}&interval=1day&time_period={lookback}&outputsize=5000&apikey={api_key}’

raw_df = requests.get(api_url).json()

df = pd.DataFrame(raw_df[‘values’]).iloc[::-1].set_index(‘datetime’).astype(float)

df = df[df.index >= start_date]

df.index = pd.to_datetime(df.index)

aroon_up = df[‘aroon_up’]

aroon_down = df[‘aroon_down’]

return aroon_up, aroon_down

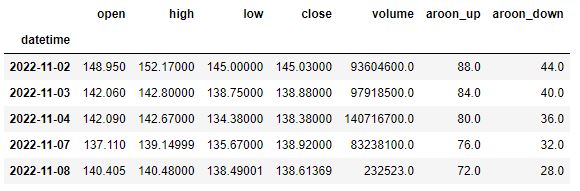

tsla[‘aroon_up’], tsla[‘aroon_down’] = get_aroon(myticker, mywin, mydate)

tsla.tail()

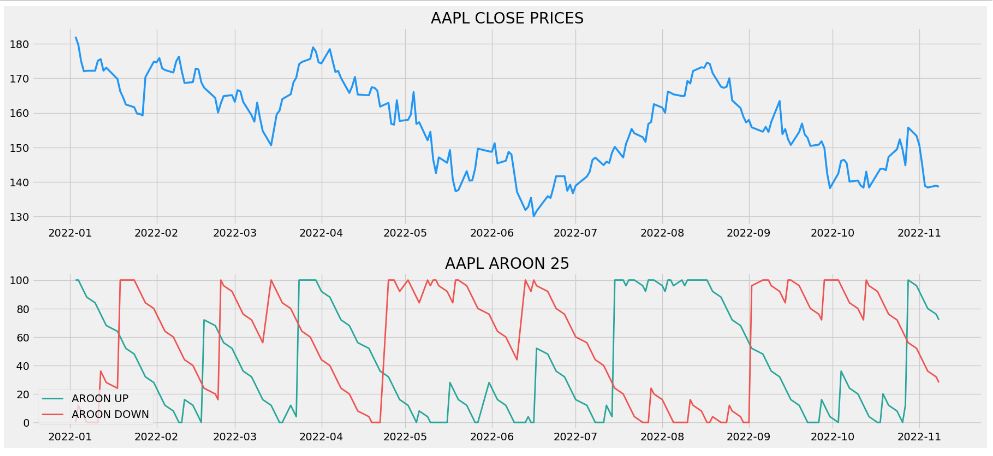

Let’s plot these 2 indicators below the closing price

ax1 = plt.subplot2grid((11,1), (0,0), rowspan = 5, colspan = 1)

ax2 = plt.subplot2grid((11,1), (6,0), rowspan = 4, colspan = 1)

ax1.plot(tsla[‘close’], linewidth = 2.5, color = ‘#2196f3’)

ax1.set_title(‘AAPL CLOSE PRICES’)

ax2.plot(tsla[‘aroon_up’], color = ‘#26a69a’, linewidth = 2, label = ‘AROON UP’)

ax2.plot(tsla[‘aroon_down’], color = ‘#ef5350’, linewidth = 2, label = ‘AROON DOWN’)

ax2.legend()

ax2.set_title(‘AAPL AROON 25’)

plt.show()

Let’s implement the Aroon trading strategy using the above plots

def implement_aroon_strategy(prices, up, down):

buy_price = []

sell_price = []

aroon_signal = []

signal = 0

for i in range(len(prices)):

if up[i] >= 70 and down[i] <= 30:

if signal != 1:

buy_price.append(prices[i])

sell_price.append(np.nan)

signal = 1

aroon_signal.append(signal)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

aroon_signal.append(0)

elif up[i] <= 30 and down[i] >= 70:

if signal != -1:

buy_price.append(np.nan)

sell_price.append(prices[i])

signal = -1

aroon_signal.append(signal)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

aroon_signal.append(0)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

aroon_signal.append(0)

return buy_price, sell_price, aroon_signal

buy_price, sell_price, aroon_signal = implement_aroon_strategy(tsla[‘close’], tsla[‘aroon_up’], tsla[‘aroon_down’])

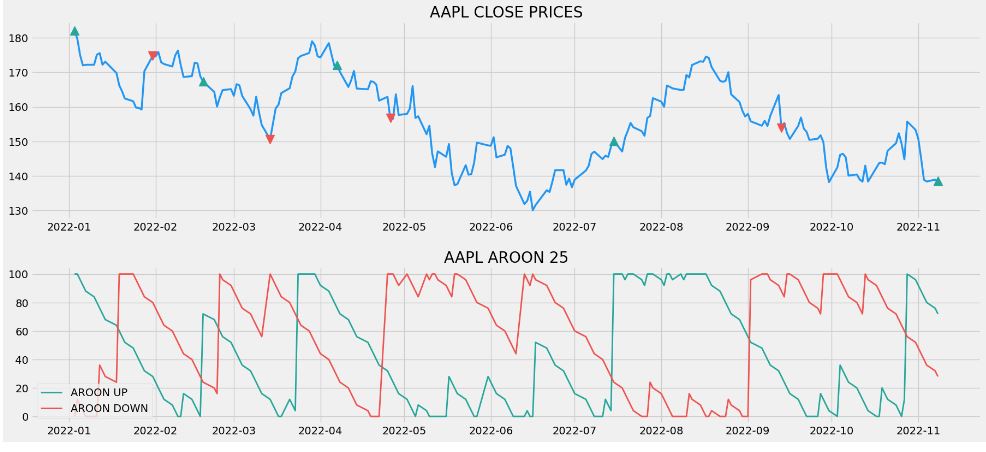

Let’s plot the result

ax1 = plt.subplot2grid((11,1), (0,0), rowspan = 5, colspan = 1)

ax2 = plt.subplot2grid((11,1), (6,0), rowspan = 4, colspan = 1)

ax1.plot(tsla[‘close’], linewidth = 2.5, color = ‘#2196f3’)

ax1.plot(tsla.index, buy_price, marker = ‘^’, color = ‘#26a69a’, markersize = 12)

ax1.plot(tsla.index, sell_price, marker = ‘v’, color = ‘#ef5350’, markersize = 12)

ax1.set_title(‘AAPL CLOSE PRICES’)

ax2.plot(tsla[‘aroon_up’], color = ‘#26a69a’, linewidth = 2, label = ‘AROON UP’)

ax2.plot(tsla[‘aroon_down’], color = ‘#ef5350’, linewidth = 2, label = ‘AROON DOWN’)

ax2.legend()

ax2.set_title(‘AAPL AROON 25’)

plt.show()

We are ready to create our position

position = []

for i in range(len(aroon_signal)):

if aroon_signal[i] > 1:

position.append(0)

else:

position.append(1)

for i in range(len(tsla[‘close’])):

if aroon_signal[i] == 1:

position[i] = 1

elif aroon_signal[i] == -1:

position[i] = 0

else:

position[i] = position[i-1]

aroon_up = tsla[‘aroon_up’]

aroon_down = tsla[‘aroon_down’]

close_price = tsla[‘close’]

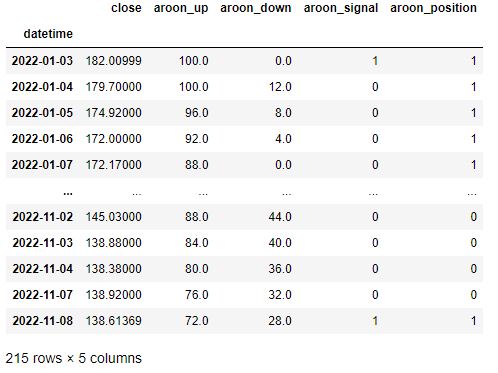

aroon_signal = pd.DataFrame(aroon_signal).rename(columns = {0:’aroon_signal’}).set_index(tsla.index)

position = pd.DataFrame(position).rename(columns = {0:’aroon_position’}).set_index(tsla.index)

frames = [close_price, aroon_up, aroon_down, aroon_signal, position]

strategy = pd.concat(frames, join = ‘inner’, axis = 1)

strategy

This list indicates 1 if we hold the stock or 0 if we don’t hold the stock. Our position will remain 0 until some changes in the trading signal occur. The Aroon indicator trading signal may also represent a sell signal (-1).

Let’s implement the backtesting process for our trading strategy

tsla_ret = pd.DataFrame(np.diff(tsla[‘close’])).rename(columns = {0:’returns’})

aroon_strategy_ret = []

for i in range(len(tsla_ret)):

returns = tsla_ret[‘returns’][i]*strategy[‘aroon_position’][i]

aroon_strategy_ret.append(returns)

aroon_strategy_ret_df = pd.DataFrame(aroon_strategy_ret).rename(columns = {0:’aroon_returns’})

investment_value = myamount

number_of_stocks = floor(investment_value/tsla[‘close’][-1])

aroon_investment_ret = []

for i in range(len(aroon_strategy_ret_df[‘aroon_returns’])):

returns = number_of_stocks*aroon_strategy_ret_df[‘aroon_returns’][i]

aroon_investment_ret.append(returns)

aroon_investment_ret_df = pd.DataFrame(aroon_investment_ret).rename(columns = {0:’investment_returns’})

total_investment_ret = round(sum(aroon_investment_ret_df[‘investment_returns’]), 2)

profit_percentage = floor((total_investment_ret/investment_value)*100)

print(cl(‘Profit gained from the Aroon strategy by investing $10k in AAPL: {}’.format(total_investment_ret), attrs = [‘bold’]))

print(cl(‘Profit percentage of the Aroon strategy : {}%’.format(profit_percentage), attrs = [‘bold’]))

Profit gained from the Aroon strategy by investing $10k in AAPL: -2561.76 Profit percentage of the Aroon strategy : -26%

Let’s see how well our trading strategy performs against a benchmark (SPY ETF)

def get_benchmark(start_date, investment_value):

spy = get_historical_data(‘SPY’, start_date)[‘close’]

benchmark = pd.DataFrame(np.diff(spy)).rename(columns = {0:’benchmark_returns’})

investment_value = investment_value

number_of_stocks = floor(investment_value/spy[-1])

benchmark_investment_ret = []

for i in range(len(benchmark['benchmark_returns'])):

returns = number_of_stocks*benchmark['benchmark_returns'][i]

benchmark_investment_ret.append(returns)

benchmark_investment_ret_df = pd.DataFrame(benchmark_investment_ret).rename(columns = {0:'investment_returns'})

return benchmark_investment_ret_df

benchmark = get_benchmark(mydate, myamount)

investment_value = myamount

total_benchmark_investment_ret = round(sum(benchmark[‘investment_returns’]), 2)

benchmark_profit_percentage = floor((total_benchmark_investment_ret/investment_value)*100)

print(cl(‘Benchmark profit by investing $10k : {}’.format(total_benchmark_investment_ret), attrs = [‘bold’]))

print(cl(‘Benchmark Profit percentage : {}%’.format(benchmark_profit_percentage), attrs = [‘bold’]))

print(cl(‘Aroon Strategy profit is {}% higher than the Benchmark Profit’.format(profit_percentage – benchmark_profit_percentage), attrs = [‘bold’]))

Benchmark profit by investing $10k : -2533.7 Benchmark Profit percentage : -26% Aroon Strategy profit is 0% higher than the Benchmark Profit

We can see that our Aroon indicator trading strategy has outperformed the SPY ETF by 0%.

Summary

- The Aroon indicator is composed of two lines. An up line which measures the number of periods since a High, and a down line which measures the number of periods since a Low.

- The indicator is typically applied to 25 periods of data, so the indicator is showing how many periods it has been since a 25-period high or low.

- When the Aroon Up is above the Aroon Down, it indicates bullish price behavior (cf. 2022-04, -08, -11)

- When the Aroon Down is above the Aroon Up, it signals bearish price behavior (cf. 2022-02, -03, -05, -06, -09, -10).

- Crossovers of the two lines can signal trend changes. For example, when Aroon Up crosses above Aroon Down it may mean a new uptrend is starting.

- The road ahead: this indicator should be incorporated into the comprehensive investment/trading risk management and portfolio optimization workflows.

Explore More

Algorithmic Trading with Aroon Indicator in Python

Investment Risk Management Study

Supervised ML/AI Stock Prediction using Keras LSTM Models

Upswing Resilient Investor Guide

ML/AI Regression for Stock Prediction – AAPL Use Case

Short-Term Stock Market Price Prediction using Deep Learning Models

AAPL Stock Technical Analysis 2 June 2022

Stock Forecasting with FBProphet

Predicting Trend Reversal in Algorithmic Trading using Stochastic Oscillator in Python

S&P 500 Algorithmic Trading with FBProphet

Track All Markets with TradingView

Basic Stock Price Analysis in Python

Bear Market Similarity Analysis using Nasdaq 100 Index Data

Are Blue-Chips Perfect for This Bear Market?

Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

Macroaxis AI Investment Opportunity

Zacks Insights into this High Inflation/Rising Rate Market

Towards min(Risk/Reward) – SeekingAlpha August Bear Market Update

The Qullamaggie’s OXY Swing Breakouts

Stock Portfolio Risk/Return Optimization

Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

A TradeSanta’s Quick Guide to Best Swing Trading Indicators

Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

DJI Market State Analysis using the Cruz Fitting Algorithm

Zacks Investment Research Update Q4’22

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Leave a comment