Featured Photo by @Nate_Dumlao at @unsplash

This post was inspired by the Qullamaggie’s trading journey and its application to the TSLA swing breakouts. Read more about breakouts here.

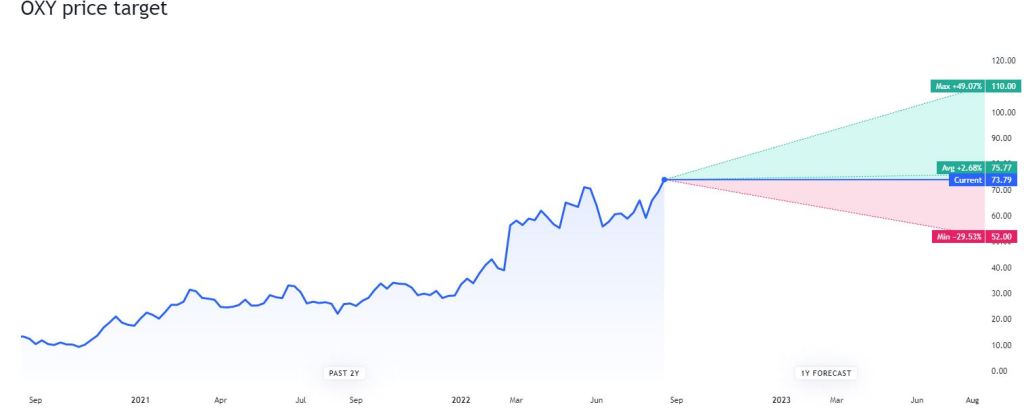

Our current goal is to extend the above breakout analysis to the $OXY stock.

Motivation

- Occidental Petroleum: The Next Merger Arbitrage Play?

- Protecting Life’s Work: Buffett’s Acquisition Of Occidental Petroleum

- Buffett Buying Occidental: Other Oil Stocks Are More Compelling, Lessons From Buffett’s Railroad Buy

- Occidental Petroleum: Buffett Will Not Get My Shares This Cheap

- Occidental Petroleum among Energy/Material gainers

OXY advanced price chart: candlesticks, trading volume, Bollinger bands, Awesome Oscillator (AO), and Chaikin Oscillator.

1D

5D

The summary of Occidental Petroleum Corporation is based on the most popular technical indicators, such as Moving Averages, Oscillators and Pivots.

OXY technical analysis

| Name | Value | Action |

|---|---|---|

| Relative Strength Index (14) | 65.42 | Neutral |

| Stochastic %K (14, 3, 3) | 79.62 | Neutral |

| Commodity Channel Index (20) | 165.12 | Neutral |

| Average Directional Index (14) | 33.40 | Neutral |

| Awesome Oscillator | 9.95 | Neutral |

| Momentum (10) | 18.11 | Buy |

| MACD Level (12, 26) | 5.36 | Buy |

| Stochastic RSI Fast (3, 3, 14, 14) | 45.74 | Neutral |

| Williams Percent Range (14) | −5.11 | Neutral |

| Bull Bear Power | 13.54 | Neutral |

| Ultimate Oscillator (7, 14, 28) | 65.77 | Neutral |

| Name | Value | Action |

|---|---|---|

| Exponential Moving Average (10) | 65.43 | Buy |

| Simple Moving Average (10) | 63.40 | Buy |

| Exponential Moving Average (20) | 61.64 | Buy |

| Simple Moving Average (20) | 62.90 | Buy |

| Exponential Moving Average (30) | 57.77 | Buy |

| Simple Moving Average (30) | 58.97 | Buy |

| Exponential Moving Average (50) | 51.24 | Buy |

| Simple Moving Average (50) | 47.96 | Buy |

| Exponential Moving Average (100) | 43.37 | Buy |

| Simple Moving Average (100) | 35.35 | Buy |

| Exponential Moving Average (200) | 43.63 | Buy |

| Simple Moving Average (200) | 38.43 | Buy |

| Ichimoku Base Line (9, 26, 52, 26) | 56.54 | Neutral |

| Volume Weighted Moving Average (20) | 62.64 | Buy |

| Hull Moving Average (9) | 70.74 | Buy |

E2E Workflow

The E2E algorithm is implemented as a sequence of the following steps:

- trend_filter

Take in a pandas series and output a binary array to indicate if a stock

fits the growth criteria (1) or not (0)

Parameters

———-

prices : pd.core.series.Series

The prices we are using to check for growth

growth_4_min : float, optional

The minimum 4 week growth. The default is 25

growth_12_min : float, optional

The minimum 12 week growth. The default is 50

growth_24_min : float, optional

The minimum 24 week growth. The default is 80

Returns

——-

np.array

A binary array showing the positions where the growth criteria is met

- explicit_heat_smooth

Smoothen out a time series using a explicit finite difference method.

Parameters

———-

prices : np.array

The price to smoothen

t_end : float

The time at which to terminate the smootheing (i.e. t = 2)

Returns

——-

P : np.array

The smoothened time-series

Time spacing, must be < 1 for numerical stability

Set up the initial condition

Solve the finite difference scheme for the next time-step

Add the fixed boundary conditions since the above solves the interior points only

- check_consolidation

Smoothen the time-series and check for consolidation, see the

docstring of find_consolidation for the parameters

- find_consolidation

Return a binary array to indicate whether each of the data-points are

classed as consolidating or not

Parameters

———-

prices : np.array

The price time series to check for consolidation

days_to_smooth : int, optional

The length of the time-series to smoothen (days). The default is 50.

perc_change_days : int, optional

The days back to % change compare against (days). The default is 5.

perc_change_thresh : float, optional

The range trading % criteria for consolidation. The default is 0.015.

check_days : int, optional

This says the number of lookback days to check for any consolidation.

If any days in check_days back is consolidating, then the last data

point is said to be consolidating. The default is 5.

Returns

——-

res : np.array

The binary array indicating consolidation (1) or not (0)

- We download the Yahoofinance $OXY data and call the above functions

- Data visualizations using matplotlib scatter plot – original Close price + Volume size (red) vs breakouts (green).

Results

Set working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

Import libraries

import numpy as np

import pandas as pd

import yfinance as yf

Define functions

def trend_filter(prices: pd.core.series.Series,

growth_4_min: float = 25.,

growth_12_min: float = 50.,

growth_24_min: float = 80.) -> np.array:

”’

Take in a pandas series and output a binary array to indicate if a stock

fits the growth criteria (1) or not (0)

Parameters

———-

prices : pd.core.series.Series

The prices we are using to check for growth

growth_4_min : float, optional

The minimum 4 week growth. The default is 25

growth_12_min : float, optional

The minimum 12 week growth. The default is 50

growth_24_min : float, optional

The minimum 24 week growth. The default is 80

Returns

——-

np.array

A binary array showing the positions where the growth criteria is met

”’

growth_func = lambda x: 100*(x.values[-1]/x.min() - 1)

growth_4 = df['Close'].rolling(20).apply(growth_func) > growth_4_min

growth_12 = df['Close'].rolling(60).apply(growth_func) > growth_12_min

growth_24 = df['Close'].rolling(120).apply(growth_func) > growth_24_min

return np.where(

growth_4 | growth_12 | growth_24,

1,

0,

)

if name == ‘main‘:

df = yf.download('OXY')

df.loc[:, 'trend_filter'] = trend_filter(df['Close'])

df.dropna()

[*********************100%***********************] 1 of 1 completed

df_trending = df[df[‘trend_filter’] == 1]

def explicit_heat_smooth(prices: np.array,

t_end: float = 5.0) -> np.array:

”’

Smoothen out a time series using a explicit finite difference method.

Parameters

———-

prices : np.array

The price to smoothen

t_end : float

The time at which to terminate the smootheing (i.e. t = 2)

Returns

——-

P : np.array

The smoothened time-series

”’

k = 0.1 # Time spacing, must be < 1 for numerical stability

# Set up the initial condition

P = prices

t = 0

while t < t_end:

# Solve the finite difference scheme for the next time-step

P = k*(P[2:] + P[:-2]) + P[1:-1]*(1-2*k)

# Add the fixed boundary conditions since the above solves the interior

# points only

P = np.hstack((

np.array([prices[0]]),

P,

np.array([prices[-1]]),

))

t += k

return P

def check_consolidation(prices: np.array,

perc_change_days: int,

perc_change_thresh: float,

check_days: int) -> int:

”’

Smoothen the time-series and check for consolidation, see the

docstring of find_consolidation for the parameters

”’

# Find the smoothed representation of the time series

prices = explicit_heat_smooth(prices)

# Perc change of the smoothed time series to perc_change_days days prior

perc_change = prices[perc_change_days:]/prices[:-perc_change_days] - 1

consolidating = np.where(np.abs(perc_change) < perc_change_thresh, 1, 0)

# Provided one entry in the last n days passes the consolidation check,

# we say that the financial instrument is in consolidation on the end day

if np.sum(consolidating[-check_days:]) > 0:

return 1

else:

return 0

def find_consolidation(prices: np.array,

days_to_smooth: int = 50,

perc_change_days: int = 5,

perc_change_thresh: float = 0.015,

check_days: int = 5) -> np.array:

”’

Return a binary array to indicate whether each of the data-points are

classed as consolidating or not

Parameters

———-

prices : np.array

The price time series to check for consolidation

days_to_smooth : int, optional

The length of the time-series to smoothen (days). The default is 50.

perc_change_days : int, optional

The days back to % change compare against (days). The default is 5.

perc_change_thresh : float, optional

The range trading % criteria for consolidation. The default is 0.015.

check_days : int, optional

This says the number of lookback days to check for any consolidation.

If any days in check_days back is consolidating, then the last data

point is said to be consolidating. The default is 5.

Returns

——-

res : np.array

The binary array indicating consolidation (1) or not (0)

”’

res = np.full(prices.shape, np.nan)

for idx in range(days_to_smooth, prices.shape[0]):

res[idx] = check_consolidation(

prices = prices[idx-days_to_smooth:idx],

perc_change_days = perc_change_days,

perc_change_thresh = perc_change_thresh,

check_days = check_days,

)

return res

Let’s proceed with main

if name == ‘main‘:

df = yf.download('TSLA')

df.loc[:, 'consolidating'] = find_consolidation(df['Close'].values)

df.dropna()

[*********************100%***********************] 1 of 1 completed

df = yf.download(‘TSLA’)

df.loc[:, ‘consolidating’] = find_consolidation(df[‘Close’].values)

df.loc[:, ‘trend_filter’] = trend_filter(df[‘Close’])

df.loc[:, ‘filtered’] = np.where(

df[‘consolidating’] + df[‘trend_filter’] == 2,

True,

False,

)

[*********************100%***********************] 1 of 1 completed

Our dataframe df looks as follows

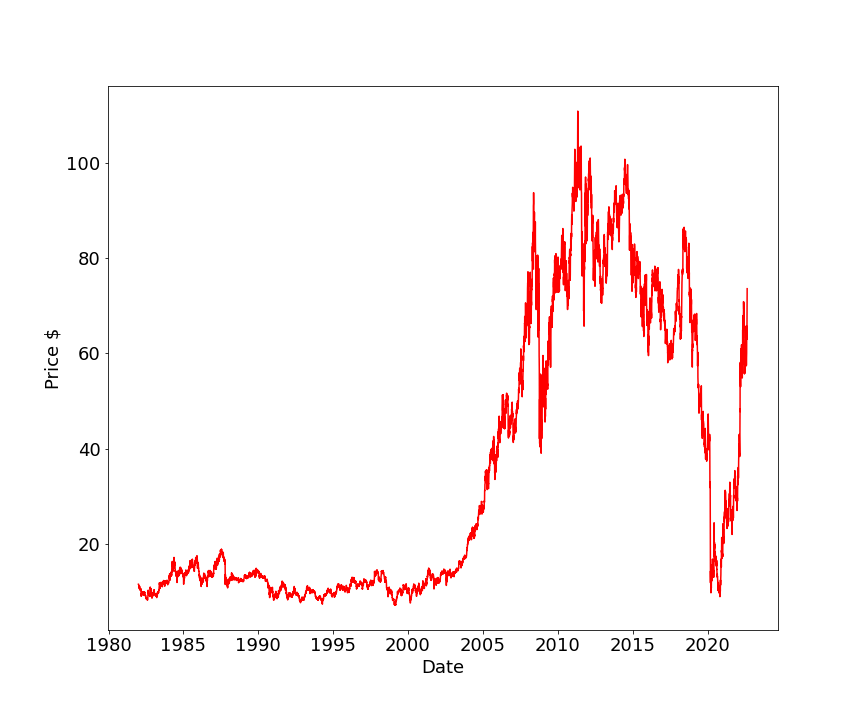

<class 'pandas.core.frame.DataFrame'> DatetimeIndex: 3051 entries, 2010-06-29 to 2022-08-10 Data columns (total 9 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Open 3051 non-null float64 1 High 3051 non-null float64 2 Low 3051 non-null float64 3 Close 3051 non-null float64 4 Adj Close 3051 non-null float64 5 Volume 3051 non-null int64 6 consolidating 3001 non-null float64 7 trend_filter 3051 non-null int32 8 filtered 3051 non-null bool dtypes: bool(1), float64(6), int32(1), int64(1) memory usage: 205.6 KB

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

import pandas as pd

df.index = pd.DatetimeIndex(data=df.index, tz=’US/Eastern’)

import matplotlib

plt.figure(figsize=(12,10))

matplotlib.rcParams.update({‘font.size’: 18})

import matplotlib.pyplot as plt

plt.plot(dft.DateTime,df.Close, ‘r’)

plt.xlabel(“Date”)

plt.ylabel(“Price $”)

plt.savefig(‘tslaprice.png’)

plt.figure(figsize=(12,10))

scal=5e5

plt.scatter(df0.index, df0[“Close”],color=’red’,s=df0[“Volume”]/scal,alpha=0.4)

plt.scatter(df1.index, df1[“Close”],color=’green’,s=df1[“Volume”]/scal,alpha=0.4)

plt.xlabel(“Date”)

plt.ylabel(“Price $”)

plt.legend([“Close” , “Filtered”], facecolor=’bisque’,

loc=’upper center’, bbox_to_anchor=(0.5, -0.08),

ncol=2)

plt.grid()

plt.show()

plt.savefig(‘oxypriceswingfilter.png’)

Conclusions

print(df.loc[‘2021-01-01 00:00:00-04:00′:’2022-08-22 00:00:00-04:00’])

Adj Close Volume consolidating trend_filter \

Date

2021-01-04 00:00:00-05:00 17.351271 18497800 0.0 1

2021-01-05 00:00:00-05:00 19.101311 37293800 1.0 1

2021-01-06 00:00:00-05:00 19.886841 37156400 1.0 1

2021-01-07 00:00:00-05:00 20.453615 24299300 1.0 1

2021-01-08 00:00:00-05:00 19.966389 18277900 0.0 1

... ... ... ... ...

2022-08-16 00:00:00-04:00 63.509998 16662200 1.0 0

2022-08-17 00:00:00-04:00 62.970001 14889800 1.0 0

2022-08-18 00:00:00-04:00 64.879997 16818000 1.0 0

2022-08-19 00:00:00-04:00 71.290001 79840900 0.0 0

2022-08-22 00:00:00-04:00 69.029999 47888500 0.0 0

filtered

Date

2021-01-04 00:00:00-05:00 False

2021-01-05 00:00:00-05:00 True

2021-01-06 00:00:00-05:00 True

2021-01-07 00:00:00-05:00 True

2021-01-08 00:00:00-05:00 False

... ...

2022-08-16 00:00:00-04:00 False

2022-08-17 00:00:00-04:00 False

2022-08-18 00:00:00-04:00 False

2022-08-19 00:00:00-04:00 False

2022-08-22 00:00:00-04:00 False

We focus on the “True” trading signals and ignore “False”.

The above scatter plot and the table help identify the setups. You need to have a watchlist ready before the market open. You should also probably have alerts set, and know how many shares you want to buy.

A swing trader can use the daily chart to find these setups, but it also works on the weekly chart and the intraday (1- and 5-minute) charts.

Read More

QULLAMAGGIE

OXY Stock Update Wednesday, 25 May 2022

OXY Stock Analysis, Thursday, 23 June 2022

Track All Markets with TradingView

Predicting Trend Reversal in Algorithmic Trading using Stochastic Oscillator in Python

S&P 500 Algorithmic Trading with FBProphet

Leave a comment