The goal of the here presented pilot study is to develop and test an end-to-end Python-3 script in Jupyter that implements algorithmic trading (aka automated trading, black-box trading, or algo-trading). Thanks to high-level automation and integration of multiple tasks, the script can simultaneously analyze hundreds of technical indicators, run simulations and forecasts, perform real-time technical analysis and generate trading signals and alerts at a speed and frequency that is impossible for a human trader.

Trading Technical Indicators (tti) is an open source Python library for Technical Analysis of trading indicators within the realm of Algorithmic Trading, using traditional methods and machine learning algorithms.

PyPI TTI – this is where Traditional Technical Analysis and AI are met:

- Calculate technical indicators (62 indicators supported).

- Produce graphs for any technical indicator.

- Get trading signals for each indicator.

- Trading simulation based on trading signals.

- Machine Learning integration for prices prediction.

Let’s begin with the Monte Carlo simulation to find the best data fit and predict future stock prices.

Let’s import the relevant libraries

import numpy as np

from datetime import datetime

import pandas_datareader as pdr

from scipy.stats import norm

Let’s define some parameters

days_to_test = 30 #Days for our best fit test

days_to_predict = 1 #How many days in the future we want to go

simulations = 1000 #How many simulations to run

ticker = ‘BAC’ #Our stock ticker name

Bank of America Corp is our stock of interest.

Let’s read the historical stock data from Yahoo Finance

data = pdr.get_data_yahoo([ticker],

start=datetime(1990, 1, 1),

end=datetime.today().strftime(‘%Y-%m-%d’))[‘Close’]

Let’s calculate several key parameters

daily_return = np.log(1 + data[ticker].pct_change())

average_daily_return = daily_return.mean()

variance = daily_return.var()

drift = average_daily_return – (variance/2)

standard_deviation = daily_return.std()

and make predictions

predictions = np.zeros(days_to_test+days_to_predict)

predictions[0] = data[ticker][-days_to_test]

pred_collection = np.ndarray(shape=(simulations,days_to_test+days_to_predict))

for j in range(0,simulations):

for i in range(1,days_to_test+days_to_predict):

random_value = standard_deviation * norm.ppf(np.random.rand())

predictions[i] = predictions[i-1] * np.exp(drift + random_value)

pred_collection[j] = predictions

differences = np.array([])

for k in range(0,simulations):

difference_arrays = np.subtract(data[ticker].values[-days_to_test:],pred_collection[k][:-1])

difference_values = np.sum(np.abs(difference_arrays))

differences = np.append(differences,difference_values)

best_fit = np.argmin(differences)

future_price = pred_collection[best_fit][-1]

type(future_price)

numpy.float64

print(future_price)

31.845747517762227

print(predictions)

[37.45000076 37.27929377 36.76698951 35.60097048 35.43851925 34.00310714 33.55056974 32.5020387 32.17673994 32.40621735 31.96776456 32.07664156 33.27317133 33.49117672 31.69846963 33.4838012 36.3412071 35.703381 35.55212438 35.384061 34.26848077 35.62129531 35.02340644 33.75911575 34.37497056 34.79596405 33.18222406 32.12827983 31.67886237 31.50734121 30.4862908 ]

print(predictions.shape)

(31,)

print(data.shape)

(8180, 1)

dataraw=data[ticker].values[-(days_to_test+days_to_predict):]

print(dataraw.shape)

(31,)

Let’s plot predictions and raw data

from matplotlib import pyplot as plt

from matplotlib.pyplot import figure

figure(figsize=(8, 6), dpi=80)

plt.plot(dataraw,label=’Raw Data’,linewidth=2)

plt.plot(predictions,label=’Predicted Data’,linewidth=2)

plt.xlabel(“Days”)

plt.ylabel(“Price”)

plt.legend()

print(dataraw[30])

31.920000076293945

We can see that the difference between predictions and raw data is only 0.25%

Let’s plot the historical data

plt.plot(data,linewidth=2)

Next, we will look at the available trading indicators and the tti.indicators usage examples.

Let’s install the TTI library

!pip install tti

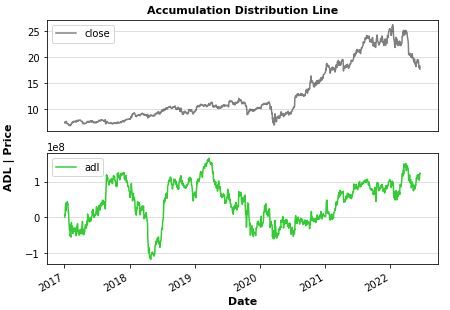

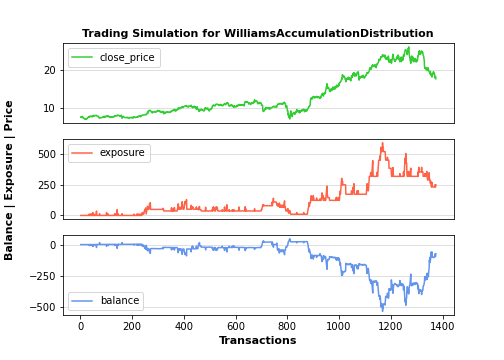

Let’s begin with the A/D indicator

from tti.indicators import AccumulationDistributionLine

The accumulation/distribution indicator (A/D) is a cumulative indicator that uses volume and price to assess whether a stock is being accumulated or distributed. The A/D measure seeks to identify divergences between the stock price and the volume flow. This provides insight into how strong a trend is. If the price is rising but the indicator is falling, then it suggests that buying or accumulation volume may not be enough to support the price rise and a price decline could be forthcoming.

Let’s import the relevant libraries

import pandas as pd

import datetime

import numpy as np

import matplotlib.pyplot as plt

from pandas.plotting import scatter_matrix

!pip install yfinance

import yfinance as yf

%matplotlib inline

Let’s consider the following Indian stocks as an example

start = “2017-01-01”

end = ‘2022-6-17’

tcs = yf.download(‘TCS’,start,end)

infy = yf.download(‘INFY’,start,end)

wipro = yf.download(‘WIPRO.NS’,start,end)

[*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed [*********************100%***********************] 1 of 1 completed

TCS = Tata Consultancy Services Limited

INFY = Infosys Ltd

WIPRO = Wipro Limited

Let’s select INFY as an example

df=infy

adl_indicator = AccumulationDistributionLine(input_data=df)

Get indicator’s calculated data

print(‘\nTechnical Indicator data:\n’, adl_indicator.getTiData())

echnical Indicator data:

adl

Date

2017-01-03 1220076

2017-01-04 7429572

2017-01-05 5938753

2017-01-06 27622113

2017-01-09 38246447

... ...

2022-06-10 107633755

2022-06-13 104228143

2022-06-14 110571789

2022-06-15 124032379

2022-06-16 122503296

[1374 rows x 1 columns]

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-16:’, adl_indicator.getTiValue(‘2022-06-16’))

Technical Indicator value at 2022-06-16: [122503296]

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, adl_indicator.getTiValue())

Most recent Technical Indicator value: [122503296]

Get signal from indicator

print(‘\nTechnical Indicator signal:’, adl_indicator.getTiSignal())

Technical Indicator signal: ('buy', -1)

Show the Graph for the calculated Technical Indicator

adl_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

adl_indicator.getTiGraph().savefig(‘../TTI/example_AccumulationDistributionLine.png’)

print(‘\nGraph for the calculated ADL indicator data, saved.’)

Graph for the calculated ADL indicator data, saved.

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

adl_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_AccumulationDistributionLine.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Simulation Data:

signal open_trading_action stock_value exposure \

Date

2017-01-03 hold none 7.37 0.0

2017-01-04 buy long 7.565 7.565

2017-01-05 buy long 7.51 15.075

2017-01-06 buy long 7.41 22.485

2017-01-09 buy long 7.48 22.555

... ... ... ... ...

2022-06-10 buy long 18.33 1399.507497

2022-06-13 buy long 17.85 1417.357497

2022-06-14 buy long 18.24 1417.747497

2022-06-15 buy long 18.290001 1417.797498

2022-06-16 buy long 17.67 1435.467498

portfolio_value earnings balance

Date

2017-01-03 0.0 0.0 0.0

2017-01-04 7.565 0.0 7.565

2017-01-05 15.02 0.0 15.02

2017-01-06 22.23 0.0 22.23

2017-01-09 22.44 0.07 22.51

... ... ... ...

2022-06-10 -384.929998 199.284986 -185.645012

2022-06-13 -357.000008 199.284986 -157.715022

2022-06-14 -364.799995 199.674985 -165.12501

2022-06-15 -365.800018 199.724987 -166.075032

2022-06-16 -335.730001 199.724987 -136.005015

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 955, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 392, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 1435.47, 'last_open_long_positions': 29, 'last_open_short_positions': 48, 'last_portfolio_value': -335.73, 'last_earnings': 199.72, 'final_balance': -136.01}

Graph for the executed trading signal simulation, saved.

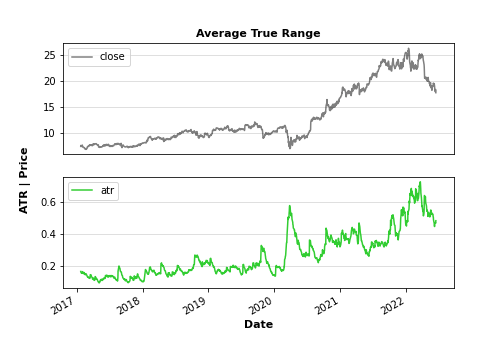

We Can Calculate the Average True Range (ATR) Easy with Pandas DataFrames. This is an important volatility indicator.

For example, consider $NFLX since 2020-1-1

import numpy as np

import pandas_datareader as pdr

import datetime as dt

start = dt.datetime(2020, 1, 1)

data = pdr.get_data_yahoo(“NFLX”, start)

high_low = data[‘High’] – data[‘Low’]

high_close = np.abs(data[‘High’] – data[‘Close’].shift())

low_close = np.abs(data[‘Low’] – data[‘Close’].shift())

ranges = pd.concat([high_low, high_close, low_close], axis=1)

true_range = np.max(ranges, axis=1)

atr = true_range.rolling(14).sum()/14

The ATR plot (blue curve) vs the original stock price (orange curve) is as follows

import matplotlib.pyplot as plt

fig, ax = plt.subplots()

atr.plot(ax=ax)

data[‘Close’].plot(ax=ax, secondary_y=True, alpha=0.3)

plt.show()

Let’s see how ATR can be computed using TTI by considering $INFY

from tti.indicators import AverageTrueRange

atr_indicator = AverageTrueRange(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-16:’, atr_indicator.getTiValue(‘2022-06-16’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, atr_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, atr_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

atr_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

atr_indicator.getTiGraph().savefig(‘../TTI/example_ATR.png’)

print(‘\nGraph for the calculated ATR indicator data, saved.’)

Technical Indicator value at 2022-06-16: [0.4831]

Most recent Technical Indicator value: [0.4831]

Technical Indicator signal: ('buy', -1)

Graph for the calculated ATR indicator data, saved.

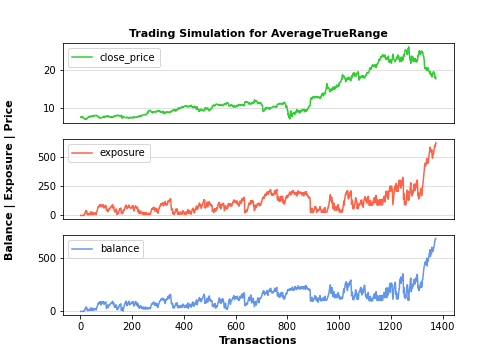

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

atr_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_ATR.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 buy long 18.33 587.754999 458.249998

2022-06-13 buy long 17.85 605.604999 464.10001

2022-06-14 buy long 18.24 605.994998 474.239994

2022-06-15 buy long 18.290001 606.045 475.540024

2022-06-16 buy long 17.67 623.715 477.090002

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 207.524981 665.774979

2022-06-13 207.524981 671.624991

2022-06-14 207.91498 682.154974

2022-06-15 207.964982 683.505005

2022-06-16 207.964982 685.054984

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 1289, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 71, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 623.71, 'last_open_long_positions': 28, 'last_open_short_positions': 1, 'last_portfolio_value': 477.09, 'last_earnings': 207.96, 'final_balance': 685.05}

Graph for the executed trading signal simulation, saved.

Recall that the average true range (ATR) is a market volatility indicator used in technical analysis. It is typically derived from the 14-day simple moving average of a series of true range indicators. The ATR was originally developed for use in commodities markets but has since been applied to all types of securities.

Let’s look at the Bollinger Bands (BB) to Gauge Trends. These bands are a trading tool used to determine entry and exit points for a trade.

from tti.indicators import BollingerBands

bb_indicator = BollingerBands(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, bb_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, bb_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, bb_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

bb_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

bb_indicator.getTiGraph().savefig(‘../TTI/example_BB.png’)

print(‘\nGraph for the calculated BB indicator data, saved.’)

Technical Indicator value at 2022-06-15: [18.7665, 19.6881, 17.8449]

Most recent Technical Indicator value: [18.711, 19.749, 17.673]

Technical Indicator signal: ('buy', -1)

Graph for the calculated BB indicator data, saved.

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

bb_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_BB.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 206.519999 -36.66

2022-06-13 buy long 17.85 224.369999 -17.85

2022-06-14 hold none 18.24 206.519999 -36.48

2022-06-15 hold none 18.290001 206.519999 -36.580002

2022-06-16 buy long 17.67 224.189999 -17.67

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 24.760002 -11.899998

2022-06-13 24.760002 6.910001

2022-06-14 25.150001 -11.329998

2022-06-15 25.150001 -11.430001

2022-06-16 25.150001 7.480001

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 65, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 106, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 224.19, 'last_open_long_positions': 5, 'last_open_short_positions': 6, 'last_portfolio_value': -17.67, 'last_earnings': 25.15, 'final_balance': 7.48}

Graph for the executed trading signal simulation, saved.

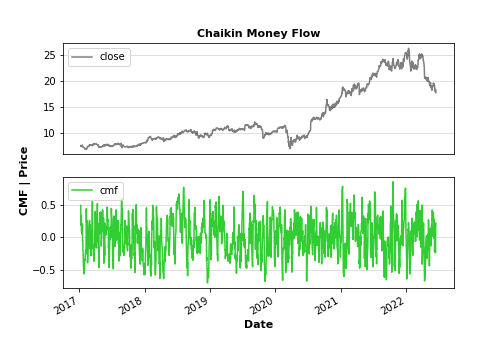

The Chaikin Money Flow (CMF) is an indicator created by Marc Chaikin in the 1980s to monitor the accumulation and distribution of a stock over a specified period. The default CMF period is 21 days. The indicator readings range between +1 and -1.

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, cmf_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, cmf_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, cmf_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

cmf_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

cmf_indicator.getTiGraph().savefig(‘../TTI/example_CMF.png’)

print(‘\nGraph for the calculated CMF indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

cmf_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_CMF.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [0.1354]

Most recent Technical Indicator value: [0.2206]

Technical Indicator signal: ('buy', -1)

Graph for the calculated CMF indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 buy long 18.33 260.900001 -54.99

2022-06-13 buy long 17.85 278.750001 -35.700001

2022-06-14 hold none 18.24 260.900001 -54.719999

2022-06-15 hold none 18.290001 260.900001 -54.870003

2022-06-16 buy long 17.67 278.570001 -35.34

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 55.725003 0.735003

2022-06-13 55.725003 20.025002

2022-06-14 56.115003 1.395003

2022-06-15 56.115003 1.245

2022-06-16 56.115003 20.775002

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 160, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 218, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 278.57, 'last_open_long_positions': 6, 'last_open_short_positions': 8, 'last_portfolio_value': -35.34, 'last_earnings': 56.12, 'final_balance': 20.78}

Graph for the executed trading signal simulation, saved.

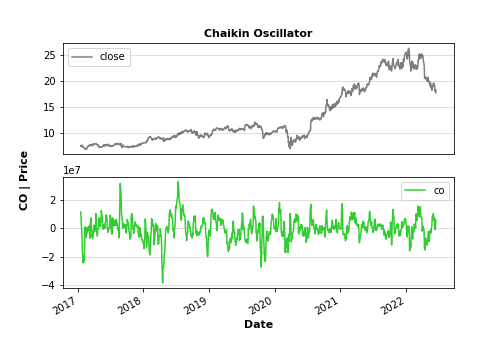

Let’s look at the Chaikin Oscillator. The Chaikin Oscillator (CO) is the difference between the 3-day and 10-day EMAs of the A/D Line discussed above. Like other momentum indicators, this indicator is designed to anticipate directional changes in the A/D Line by measuring the momentum behind the movements. A momentum change is the first step to a trend change. Anticipating trend changes in the A/D Line can help chartists anticipate trend changes in the underlying security. The CO generates signals with crosses above/below the zero line or with bullish/bearish divergences.

from tti.indicators import ChaikinOscillator

co_indicator = ChaikinOscillator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, co_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, co_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, co_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

co_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

co_indicator.getTiGraph().savefig(‘../TTI/example_CO.png’)

print(‘\nGraph for the calculated CO indicator data, saved.’)

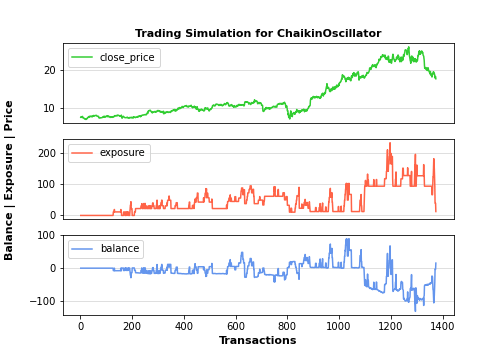

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

co_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_CO.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [4952520.5672]

Most recent Technical Indicator value: [5958499.6774]

Technical Indicator signal: ('hold', 0)

Graph for the calculated CO indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 sell short 18.33 93.449999 -73.32

2022-06-13 hold none 17.85 39.135 -35.700001

2022-06-14 hold none 18.24 39.135 -36.48

2022-06-15 hold none 18.290001 39.135 -36.580002

2022-06-16 hold none 17.67 12.375 -17.67

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 32.400006 -40.919994

2022-06-13 32.910004 -2.789997

2022-06-14 32.910004 -3.569995

2022-06-15 32.910004 -3.669998

2022-06-16 33.080004 15.410004

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 162, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 74, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 12.38, 'last_open_long_positions': 0, 'last_open_short_positions': 1, 'last_portfolio_value': -17.67, 'last_earnings': 33.08, 'final_balance': 15.41}

Graph for the executed trading signal simulation, saved.

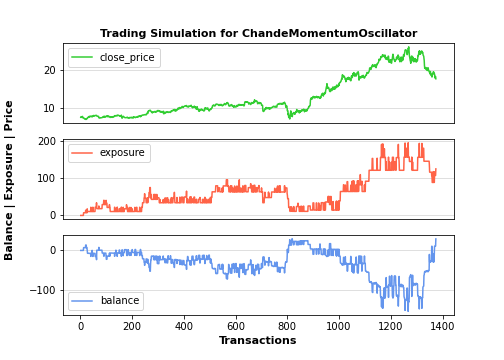

The Chande momentum oscillator (CMO) is a technical indicator that uses momentum to identify relative strength or weakness in a market:

- The chosen time frame greatly affects signals generated by the indicator.

- Pattern recognition often generates more reliable signals than absolute oscillator levels.

- Overbought-oversold indicators are less effective in strongly trending markets.

from tti.indicators import ChandeMomentumOscillator

cmo_indicator = ChandeMomentumOscillator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, cmo_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, cmo_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, cmo_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

cmo_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

cmo_indicator.getTiGraph().savefig(‘../TTI/example_CMO.png’)

print(‘\nGraph for the calculated CMO indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

cmo_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_CMO.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [-49.7142]

Most recent Technical Indicator value: [-57.8947]

Technical Indicator signal: ('buy', -1)

Graph for the calculated CMO indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 107.789999 -18.33

2022-06-13 hold none 17.85 107.789999 -17.85

2022-06-14 hold none 18.24 107.789999 -18.24

2022-06-15 hold none 18.290001 107.789999 -18.290001

2022-06-16 buy long 17.67 125.459999 0.0

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 29.255002 10.925003

2022-06-13 29.255002 11.405002

2022-06-14 29.255002 11.015003

2022-06-15 29.255002 10.965002

2022-06-16 29.255002 29.255002

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 76, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 121, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 125.46, 'last_open_long_positions': 3, 'last_open_short_positions': 3, 'last_portfolio_value': 0.0, 'last_earnings': 29.26, 'final_balance': 29.26}

Graph for the executed trading signal simulation, saved.

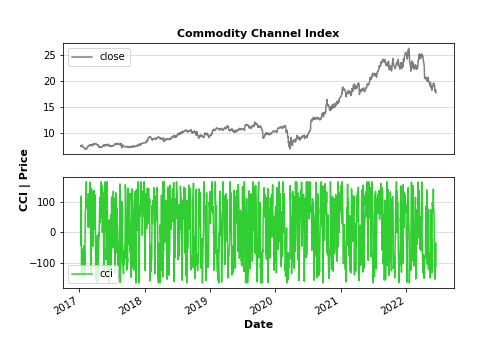

The Commodity Channel Index (CCI) is a technical indicator that measures the difference between the current price and the historical average price. When the CCI is above zero, it indicates the price is above the historic average. Conversely, when the CCI is below zero, the price is below the historic average.

from tti.indicators import CommodityChannelIndex

cci_indicator = CommodityChannelIndex(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, cci_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, cci_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, cci_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

cci_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

cci_indicator.getTiGraph().savefig(‘../TTI/example_CCI.png’)

print(‘\nGraph for the calculated CCI indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

cci_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_CCI.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [-34.6475]

Most recent Technical Indicator value: [-112.9162]

Technical Indicator signal: ('buy', -1)

Graph for the calculated CCI indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 buy long 18.33 334.484997 54.99

2022-06-13 buy long 17.85 352.334997 71.400002

2022-06-14 hold none 18.24 334.484997 54.719999

2022-06-15 hold none 18.290001 334.484997 54.870003

2022-06-16 buy long 17.67 352.154997 70.68

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 76.254998 131.244998

2022-06-13 76.254998 147.655

2022-06-14 76.644998 131.364997

2022-06-15 76.644998 131.515

2022-06-16 76.644998 147.324998

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 198, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 282, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 352.15, 'last_open_long_positions': 11, 'last_open_short_positions': 7, 'last_portfolio_value': 70.68, 'last_earnings': 76.64, 'final_balance': 147.32}

Graph for the executed trading signal simulation, saved.

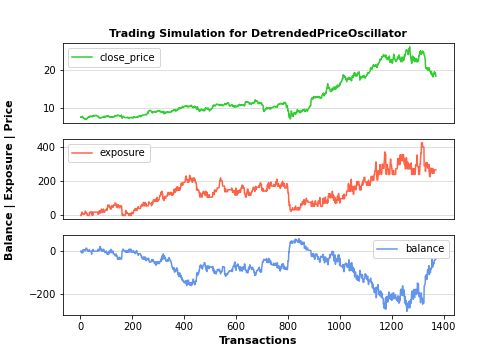

The detrended price oscillator (DPO) is an indicator in technical analysis that attempts to eliminate the long-term trends in prices by using a displaced moving average so it does not react to the most current price action. This allows the indicator to show intermediate overbought and oversold levels effectively.

from tti.indicators import DetrendedPriceOscillator

dpo_indicator = DetrendedPriceOscillator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, dpo_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, dpo_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, dpo_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

dpo_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

dpo_indicator.getTiGraph().savefig(‘../TTI/example_DPO.png’)

print(‘\nGraph for the calculated DPO indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

dpo_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_DPO.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: None

Most recent Technical Indicator value: [0.12]

Technical Indicator signal: ('hold', 0)

Graph for the calculated DPO indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 sell short 7.41 11.115 -7.41

2017-01-09 buy long 7.48 18.595 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 264.75 -91.65

2022-06-13 NaN NaN NaN NaN NaN

2022-06-14 NaN NaN NaN NaN NaN

2022-06-15 NaN NaN NaN NaN NaN

2022-06-16 NaN NaN NaN NaN NaN

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 -7.41

2017-01-09 0.0 0.0

... ... ...

2022-06-10 55.260003 -36.389997

2022-06-13 NaN NaN

2022-06-14 NaN NaN

2022-06-15 NaN NaN

2022-06-16 NaN NaN

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1370, 'number_of_buy_signals': 224, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 226, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 18.33, 'last_exposure': 264.75, 'last_open_long_positions': 4, 'last_open_short_positions': 9, 'last_portfolio_value': -91.65, 'last_earnings': 55.26, 'final_balance': -36.39}

Graph for the executed trading signal simulation, saved.

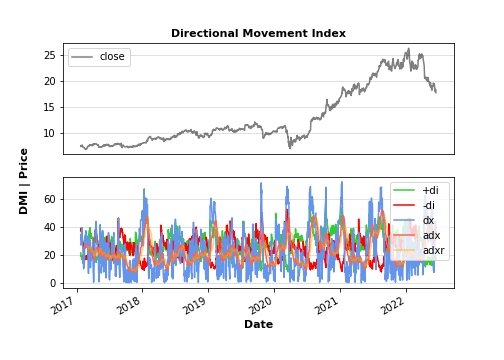

Let’s look at the indicator that identifies in which direction the price of an asset is moving:

- The directional movement index (DMI) is a technical indicator that measures both the strength and direction of a price movement and is intended to reduce false signals.

- The DMI utilizes two standard indicators, one negative (-DM) and one positive (+DN), in conjunction with a third, the average directional index (ADX), which is non-directional but shows momentum.

- The larger the spread between the two primary lines, the stronger the price trend. If +DI is way above -DI the price trend is strongly up. If -DI is way above +DI then the price trend is strongly down.

- ADX measures the strength of the trend, either up or down; a reading above 25 indicates a strong trend.

from tti.indicators import DirectionalMovementIndex

dmi_indicator = DirectionalMovementIndex(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, dmi_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, dmi_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, dmi_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

dmi_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

dmi_indicator.getTiGraph().savefig(‘../TTI/example_dmi.png’)

print(‘\nGraph for the calculated dmi indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

dmi_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_dmi.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [18.2314, 38.9129, 36.1917, 31.9486, 36.8952]

Most recent Technical Indicator value: [16.3714, 39.3787, 41.2687, 32.6143, 36.6857]

Technical Indicator signal: ('hold', 0)

Graph for the calculated dmi indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 37.649999 -36.66

2022-06-13 hold none 17.85 37.649999 -35.700001

2022-06-14 hold none 18.24 37.649999 -36.48

2022-06-15 hold none 18.290001 37.649999 -36.580002

2022-06-16 hold none 17.67 37.649999 -35.34

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 8.490003 -28.169997

2022-06-13 8.490003 -27.209998

2022-06-14 8.490003 -27.989996

2022-06-15 8.490003 -28.089999

2022-06-16 8.490003 -26.849997

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 27, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 30, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 37.65, 'last_open_long_positions': 0, 'last_open_short_positions': 2, 'last_portfolio_value': -35.34, 'last_earnings': 8.49, 'final_balance': -26.85}

Graph for the executed trading signal simulation, saved.

Let’s look at the double exponential moving average (DEMA). This is a technical indicator that was devised to reduce the lag in the results produced by a traditional moving average. Technical traders use it to lessen the amount of “noise” that can distort the movements on a price chart:

from tti.indicators import DoubleExponentialMovingAverage

dema_indicator = DoubleExponentialMovingAverage(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, dema_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, dema_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, dema_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

dema_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

dema_indicator.getTiGraph().savefig(‘../TTI/example_dema.png’)

print(‘\nGraph for the calculated dema indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

dema_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_dema.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [18.1512] Most recent Technical Indicator value: [17.8323] Technical Indicator signal: ('buy', -1)

Graph for the calculated dema indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 buy long 18.33 437.709995 366.599998

2022-06-13 buy long 17.85 455.559996 374.850008

2022-06-14 hold none 18.24 437.709995 364.799995

2022-06-15 hold none 18.290001 437.709995 365.800018

2022-06-16 buy long 17.67 455.379995 371.070002

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 100.444993 467.044991

2022-06-13 100.444993 475.295001

2022-06-14 100.834992 465.634988

2022-06-15 100.834992 466.635011

2022-06-16 100.834992 471.904994

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 672, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 0, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 455.38, 'last_open_long_positions': 21, 'last_open_short_positions': 0, 'last_portfolio_value': 371.07, 'last_earnings': 100.83, 'final_balance': 471.9}

Graph for the executed trading signal simulation, saved.

Let’s look at the Ease of Movement indicator that shows the relationship between price and volume, and it’s often used to assess the strength of an underlying trend:

- Ease of Movement calculates how easily a price can move up or down.

- The calculation subtracts yesterday’s average price from today’s average price and divides the difference by volume.

from tti.indicators import EaseOfMovement

eom_indicator = EaseOfMovement(input_data=df,period=1, fill_missing_values=False)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, eom_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, eom_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, eom_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

eom_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

eom_indicator.getTiGraph().savefig(‘../TTI/example_eom.png’)

print(‘\nGraph for the calculated eom indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

eom_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_eom.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [-0.0, -0.0]

Most recent Technical Indicator value: [-0.0001, -0.0001]

Technical Indicator signal: ('hold', 0)

Graph for the calculated eom indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 131.235002 0.0

2022-06-13 hold none 17.85 131.235002 0.0

2022-06-14 buy long 18.24 149.475002 18.24

2022-06-15 hold none 18.290001 131.235002 0.0

2022-06-16 hold none 17.67 131.235002 0.0

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 23.25 23.25

2022-06-13 23.25 23.25

2022-06-14 23.25 41.49

2022-06-15 23.300001 23.300001

2022-06-16 23.300001 23.300001

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 41, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 39, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 131.24, 'last_open_long_positions': 3, 'last_open_short_positions': 3, 'last_portfolio_value': 0.0, 'last_earnings': 23.3, 'final_balance': 23.3}

Graph for the executed trading signal simulation, saved.

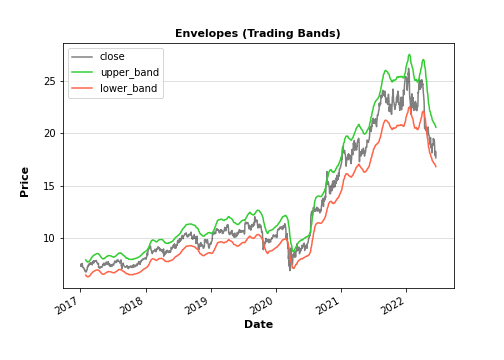

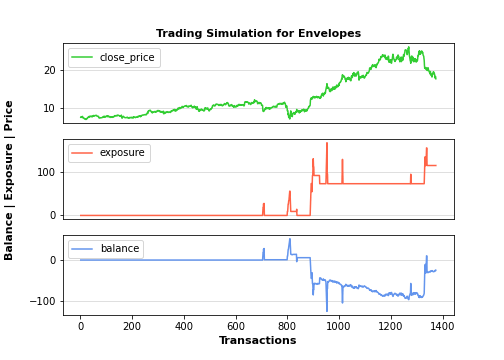

Let’s look at the Envelopes (ENV) indicator. ENV is a tool that attempts to identify the upper and lower bands of a trading range. It does this by plotting two moving average envelopes on a price chart, one shifted up to a certain distance above the price and the other shifted below.

from tti.indicators import Envelopes

env_indicator = Envelopes(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, env_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, env_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, env_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

env_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

env_indicator.getTiGraph().savefig(‘../TTI/example_env.png’)

print(‘\nGraph for the calculated env indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

env_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_env.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [20.6431, 16.8898]

Most recent Technical Indicator value: [20.5821, 16.8399]

Technical Indicator signal: ('hold', 0)

Graph for the calculated env indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 114.934999 -36.66

2022-06-13 hold none 17.85 114.934999 -35.700001

2022-06-14 hold none 18.24 114.934999 -36.48

2022-06-15 hold none 18.290001 114.934999 -36.580002

2022-06-16 hold none 17.67 114.934999 -35.34

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 10.68 -25.98

2022-06-13 10.68 -25.02

2022-06-14 10.68 -25.799999

2022-06-15 10.68 -25.900002

2022-06-16 10.68 -24.66

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 28, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 19, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 114.93, 'last_open_long_positions': 2, 'last_open_short_positions': 4, 'last_portfolio_value': -35.34, 'last_earnings': 10.68, 'final_balance': -24.66}

Graph for the executed trading signal simulation, saved.

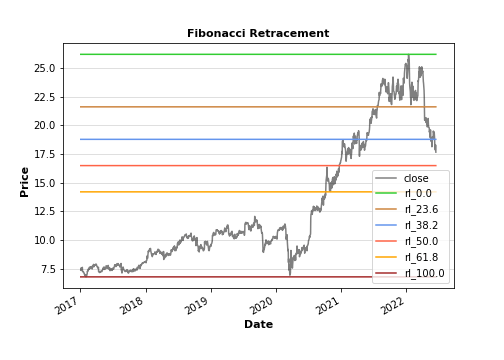

In finance, Fibonacci retracement is a method of technical analysis for determining support and resistance levels. It is named after the Fibonacci sequence of numbers, whose ratios provide price levels to which markets tend to retrace a portion of a move, before a trend continues in the original direction.

Fibonacci retracement levels—stemming from the Fibonacci sequence—are horizontal lines that indicate where support and resistance are likely to occur.

Each level is associated with a percentage. The percentage is how much of a prior move the price has retraced. The Fibonacci retracement levels are 23.6%, 38.2%, 61.8%, and 78.6%. While not officially a Fibonacci ratio, 50% is also used.

The indicator is useful because it can be drawn between any two significant price points, such as a high and a low. The indicator will then create the levels between those two points.

Suppose the price of a stock rises $10 and then drops $2.36. In that case, it has retraced 23.6%, which is a Fibonacci number. Fibonacci numbers are found throughout nature. Therefore, many traders believe that these numbers also have relevance in financial markets:

from tti.indicators import FibonacciRetracement

fr_indicator = FibonacciRetracement(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, fr_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, fr_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, fr_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

fr_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

fr_indicator.getTiGraph().savefig(‘../TTI/example_fr.png’)

print(‘\nGraph for the calculated fr indicator data, saved.’)

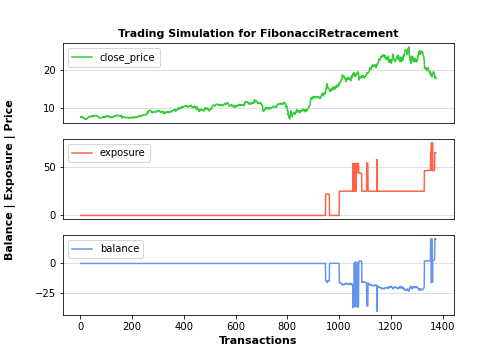

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

fr_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_fr.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [26.2, 21.6204, 18.7873, 16.4975, 14.2077, 6.795]

Most recent Technical Indicator value: [26.2, 21.6204, 18.7873, 16.4975, 14.2077, 6.795]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fr indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 buy long 18.33 64.39 18.33

2022-06-13 hold none 17.85 64.39 17.85

2022-06-14 hold none 18.24 64.39 18.24

2022-06-15 hold none 18.290001 64.39 18.290001

2022-06-16 hold none 17.67 64.39 17.67

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 3.020002 21.350002

2022-06-13 3.020002 20.870003

2022-06-14 3.020002 21.260002

2022-06-15 3.020002 21.310003

2022-06-16 3.020002 20.690002

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 8, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 10, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 64.39, 'last_open_long_positions': 2, 'last_open_short_positions': 1, 'last_portfolio_value': 17.67, 'last_earnings': 3.02, 'final_balance': 20.69}

Graph for the executed trading signal simulation, saved.

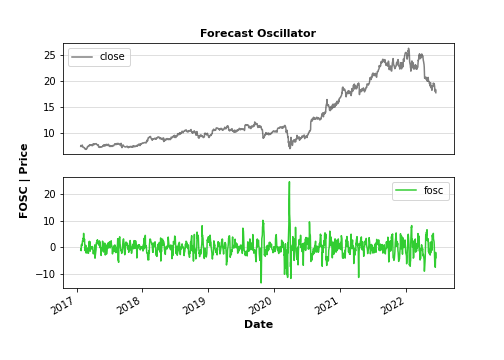

Let’s look at the Forecast Oscillator (FO) that compares actual price with the value returned by the Time Series Forecast study. It is calculated as percentage ratio of the difference between the Close price and previous bar’s Time Series Forecast value to the Close price. The Forecast Oscillator and therefore the time series forecast are based on linear regression. The time series forecast indicator is equal to the sum of two other indicators: the linear regression and the linear regression slope.

from tti.indicators import ForecastOscillator

fo_indicator = ForecastOscillator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, fo_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, fo_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, fo_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

fo_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

fo_indicator.getTiGraph().savefig(‘../TTI/example_fo.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

fo_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_fo.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [-1.9798]

Most recent Technical Indicator value: [-3.9943]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 152.354999 -36.66

2022-06-13 hold none 17.85 152.354999 -35.700001

2022-06-14 hold none 18.24 152.354999 -36.48

2022-06-15 hold none 18.290001 152.354999 -36.580002

2022-06-16 hold none 17.67 152.354999 -35.34

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 49.379995 12.719995

2022-06-13 49.379995 13.679995

2022-06-14 49.379995 12.899996

2022-06-15 49.379995 12.799994

2022-06-16 49.379995 14.039995

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 153, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 152, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 152.35, 'last_open_long_positions': 3, 'last_open_short_positions': 5, 'last_portfolio_value': -35.34, 'last_earnings': 49.38, 'final_balance': 14.04}

Graph for the executed trading signal simulation, saved.

Let’s look at the Ichimoku cloud (IMC) trading that attempts to identify a probable direction of price. It helps the trader determine the most suitable time to enter and exit the market by providing you with the trend direction. It gives you reliable support and resistance levels and the strength of these market signals:

from tti.indicators import IchimokuCloud

imc_indicator = IchimokuCloud(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, imc_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, imc_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, imc_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

imc_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

imc_indicator.getTiGraph().savefig(‘../TTI/example_imc.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

imc_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_imc.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [18.7, 18.94, 21.335, 22.46]

Most recent Technical Indicator value: [18.62, 18.685, 21.1425, 22.365]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 0.0 0.0

2022-06-13 hold none 17.85 0.0 0.0

2022-06-14 hold none 18.24 0.0 0.0

2022-06-15 hold none 18.290001 0.0 0.0

2022-06-16 hold none 17.67 0.0 0.0

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 0.79 0.79

2022-06-13 0.79 0.79

2022-06-14 0.79 0.79

2022-06-15 0.79 0.79

2022-06-16 0.79 0.79

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 5, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 1, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 0.0, 'last_open_long_positions': 0, 'last_open_short_positions': 0, 'last_portfolio_value': 0.0, 'last_earnings': 0.79, 'final_balance': 0.79}

Graph for the executed trading signal simulation, saved.

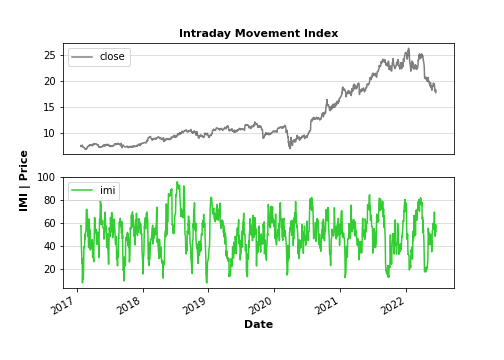

Let’s look at the Intraday Momentum Index (IMI) – a technical indicator that combines aspects of candlestick analysis with the relative strength index (RSI) in order to generate overbought or oversold signals. The intraday indicator was developed by market technician Tushar Chande to aid investors with their trading decisions.

from tti.indicators import IntradayMovementIndex

idmi_indicator = IntradayMovementIndex(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, idmi_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, idmi_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, idmi_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

idmi_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

idmi_indicator.getTiGraph().savefig(‘../TTI/example_idmi.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

idmi_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_idmi.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [58.6614]

Most recent Technical Indicator value: [52.5]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 61.885001 -18.33

2022-06-13 hold none 17.85 61.885001 -17.85

2022-06-14 hold none 18.24 61.885001 -18.24

2022-06-15 hold none 18.290001 61.885001 -18.290001

2022-06-16 hold none 17.67 61.885001 -17.67

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 9.934999 -8.395001

2022-06-13 9.934999 -7.915001

2022-06-14 9.934999 -8.305001

2022-06-15 9.934999 -8.355002

2022-06-16 9.934999 -7.735001

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 37, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 33, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 61.89, 'last_open_long_positions': 1, 'last_open_short_positions': 2, 'last_portfolio_value': -17.67, 'last_earnings': 9.93, 'final_balance': -7.74}

Graph for the executed trading signal simulation, saved.

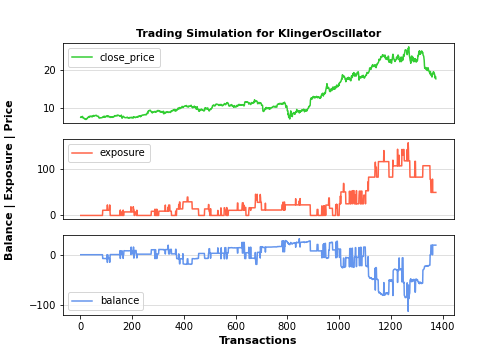

Let’s look at the Klinger oscillator (KO) – a financial tool that was designed by Stephen Klinger in 1977 to predict long-term trends in money flow while also detecting short-term fluctuations. In addition, it predicts price reversals in a financial market by extensively comparing volume to price:

from tti.indicators import KlingerOscillator

klo_indicator = KlingerOscillator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, klo_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, klo_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, klo_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

klo_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

klo_indicator.getTiGraph().savefig(‘../TTI/example_klo.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

klo_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_klo.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [12512248.6986]

Most recent Technical Indicator value: [7423476.0864]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 49.249999 0.0

2022-06-13 hold none 17.85 49.249999 0.0

2022-06-14 hold none 18.24 49.249999 0.0

2022-06-15 hold none 18.290001 49.249999 0.0

2022-06-16 hold none 17.67 49.249999 0.0

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 18.905005 18.905005

2022-06-13 18.905005 18.905005

2022-06-14 18.905005 18.905005

2022-06-15 18.905005 18.905005

2022-06-16 18.905005 18.905005

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 59, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 60, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 49.25, 'last_open_long_positions': 1, 'last_open_short_positions': 1, 'last_portfolio_value': 0.0, 'last_earnings': 18.91, 'final_balance': 18.91}

Graph for the executed trading signal simulation, saved.

Let’s look at the Linear Regression (LREG) Indicator that plots the ending value of a Linear Regression Line for a specified number of bars; showing, statistically, where the price is expected to be. For example, a 20 period Linear Regression Indicator will equal the ending value of a Linear Regression line that covers 20 bars.

from tti.indicators import LinearRegressionIndicator

lreg_indicator = LinearRegressionIndicator(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, lreg_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, lreg_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, lreg_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

lreg_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

lreg_indicator.getTiGraph().savefig(‘../TTI/example_lreg.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

lreg_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_lreg.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [18.438] Most recent Technical Indicator value: [18.0806] Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 117.055 -36.66

2022-06-13 hold none 17.85 117.055 -35.700001

2022-06-14 hold none 18.24 117.055 -36.48

2022-06-15 hold none 18.290001 117.055 -36.580002

2022-06-16 hold none 17.67 117.055 -35.34

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 55.309997 18.649997

2022-06-13 55.309997 19.609996

2022-06-14 55.309997 18.829997

2022-06-15 55.309997 18.729995

2022-06-16 55.309997 19.969996

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 169, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 169, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 117.05, 'last_open_long_positions': 2, 'last_open_short_positions': 4, 'last_portfolio_value': -35.34, 'last_earnings': 55.31, 'final_balance': 19.97}

Graph for the executed trading signal simulation, saved.

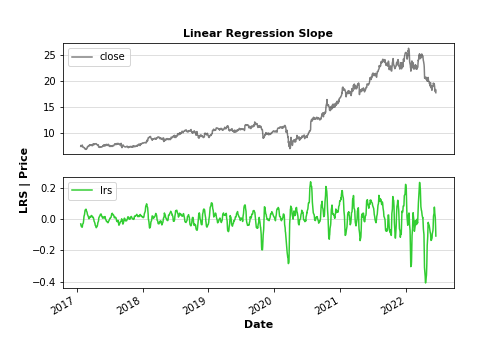

It is useful to consider the Linear Regression Slope Indicator – a centered oscillator type of indicator which is similar to momentum indicators. The momentum is positive when the Slope is above 0 and negative when it is below 0. We can use this indicator to measure the strength or weakness and direction of the momentum.

from tti.indicators import LinearRegressionSlope

slop_indicator = LinearRegressionSlope(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, slop_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, slop_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, slop_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

slop_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

slop_indicator.getTiGraph().savefig(‘../TTI/example_slop.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

slop_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_slop.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [-0.0622]

Most recent Technical Indicator value: [-0.1086]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 50.594999 -18.33

2022-06-13 hold none 17.85 50.594999 -17.85

2022-06-14 buy long 18.24 68.834999 0.0

2022-06-15 hold none 18.290001 50.594999 -18.290001

2022-06-16 hold none 17.67 50.594999 -17.67

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 16.434991 -1.895009

2022-06-13 16.434991 -1.415009

2022-06-14 16.434991 16.434991

2022-06-15 16.484993 -1.805008

2022-06-16 16.484993 -1.185008

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 52, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 52, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 50.59, 'last_open_long_positions': 1, 'last_open_short_positions': 2, 'last_portfolio_value': -17.67, 'last_earnings': 16.48, 'final_balance': -1.19}

Graph for the executed trading signal simulation, saved.

Let’s look at the market facilitation index (MFI) – an indicator that measures the strength or weakness behind movements of the price of an asset.

The MFI indicator can help you decide when a price trend is strong enough to justify trading it, when a new trend may be about to start and when to avoid entering trades altogether.

It does this by looking at changes in the size of price moves and whether the trading volume is rising or falling.

from tti.indicators import MarketFacilitationIndex

mfi_indicator = MarketFacilitationIndex(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, mfi_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, mfi_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, mfi_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

mfi_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

mfi_indicator.getTiGraph().savefig(‘../TTI/example_mfi.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

mfi_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_mfi.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [2.6e-08]

Most recent Technical Indicator value: [3.27e-08]

Technical Indicator signal: ('sell', 1)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 sell short 7.565 11.3475 -7.565

2017-01-05 buy long 7.51 7.51 7.51

2017-01-06 sell short 7.41 18.625 0.0

2017-01-09 sell short 7.48 29.845 -7.48

... ... ... ... ... ...

2022-06-10 buy long 18.33 892.622498 -274.949999

2022-06-13 buy long 17.85 910.472498 -249.900005

2022-06-14 buy long 18.24 910.862498 -255.359997

2022-06-15 buy long 18.290001 910.912499 -256.060013

2022-06-16 sell short 17.67 910.657499 -247.380001

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 -7.565

2017-01-05 0.055 7.565

2017-01-06 0.055 0.055

2017-01-09 0.055 -7.425

... ... ...

2022-06-10 209.124999 -65.825

2022-06-13 209.124999 -40.775007

2022-06-14 209.514998 -45.844999

2022-06-15 209.564999 -46.495014

2022-06-16 209.734999 -37.645002

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 686, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 683, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 910.66, 'last_open_long_positions': 16, 'last_open_short_positions': 30, 'last_portfolio_value': -247.38, 'last_earnings': 209.73, 'final_balance': -37.65}

Graph for the executed trading signal simulation, saved.

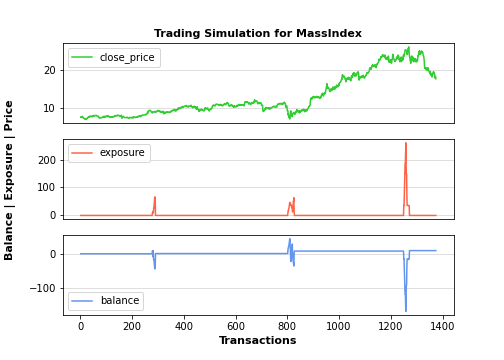

Let’s look at the mass index (MI) – an indicator, developed by Donald Dorsey, used in technical analysis to predict trend reversals. It is based on the notion that there is a tendency for reversal when the price range widens, and therefore compares previous trading ranges (highs minus lows).

from tti.indicators import MassIndex

mind_indicator = MassIndex(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, mind_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, mind_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, mind_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

mind_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

mind_indicator.getTiGraph().savefig(‘../TTI/example_mind.png’)

print(‘\nGraph for the calculated fo indicator data, saved.’)

Execute simulation based on trading signals

simulation_data, simulation_statistics, simulation_graph = \

mind_indicator.getTiSimulation(

close_values=df[[‘close’]], max_exposure=None,

short_exposure_factor=1.5)

print(‘\nSimulation Data:\n’, simulation_data)

print(‘\nSimulation Statistics:\n’, simulation_statistics)

Save the Graph for the executed trading signal simulation

simulation_graph.savefig(‘../TTI/simulation_mind.png’)

print(‘\nGraph for the executed trading signal simulation, saved.’)

Technical Indicator value at 2022-06-15: [24.0192]

Most recent Technical Indicator value: [23.9409]

Technical Indicator signal: ('hold', 0)

Graph for the calculated fo indicator data, saved.

Simulation Data:

signal open_trading_action stock_value exposure portfolio_value \

Date

2017-01-03 hold none 7.37 0.0 0.0

2017-01-04 hold none 7.565 0.0 0.0

2017-01-05 hold none 7.51 0.0 0.0

2017-01-06 hold none 7.41 0.0 0.0

2017-01-09 hold none 7.48 0.0 0.0

... ... ... ... ... ...

2022-06-10 hold none 18.33 0.0 0.0

2022-06-13 hold none 17.85 0.0 0.0

2022-06-14 hold none 18.24 0.0 0.0

2022-06-15 hold none 18.290001 0.0 0.0

2022-06-16 hold none 17.67 0.0 0.0

earnings balance

Date

2017-01-03 0.0 0.0

2017-01-04 0.0 0.0

2017-01-05 0.0 0.0

2017-01-06 0.0 0.0

2017-01-09 0.0 0.0

... ... ...

2022-06-10 9.335 9.335

2022-06-13 9.335 9.335

2022-06-14 9.335 9.335

2022-06-15 9.335 9.335

2022-06-16 9.335 9.335

[1374 rows x 7 columns]

Simulation Statistics:

{'number_of_trading_days': 1374, 'number_of_buy_signals': 16, 'number_of_ignored_buy_signals': 0, 'number_of_sell_signals': 27, 'number_of_ignored_sell_signals': 0, 'last_stock_value': 17.67, 'last_exposure': 0.0, 'last_open_long_positions': 0, 'last_open_short_positions': 0, 'last_portfolio_value': 0.0, 'last_earnings': 9.34, 'final_balance': 9.34}

Graph for the executed trading signal simulation, saved.

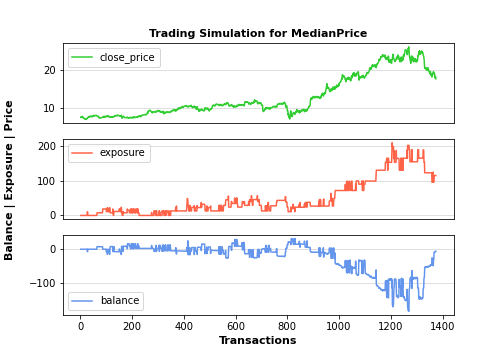

Let’s look at the Median Price (MP) indicator. MP is simply the midpoint of each day’s price. The Typical Price and Weighted Close are similar indicators. The MP indicator provides a simple, single-line chart of the day’s “average price.” This average price is useful when you want a simpler view of prices.

from tti.indicators import MedianPrice

medp_indicator = MedianPrice(input_data=df)

Get indicator’s value for a specific date

print(‘\nTechnical Indicator value at 2022-06-15:’, medp_indicator.getTiValue(‘2022-06-15’))

Get the most recent indicator’s value

print(‘\nMost recent Technical Indicator value:’, medp_indicator.getTiValue())

Get signal from indicator

print(‘\nTechnical Indicator signal:’, medp_indicator.getTiSignal())

Show the Graph for the calculated Technical Indicator

medp_indicator.getTiGraph().show()

Save the Graph for the calculated Technical Indicator

medp_indicator.getTiGraph().savefig(‘C:/Users/adrou/OneDrive/Documents/TTI/example_medp.png’)