In this post, we extend the earlier study by applying FBProphet to Algorithmic Trading using S&P 500 stock for test purposes.

Contents:

The Facebook’s Prophet library is an open-source library designed for automated forecasts for univariate time series datasets such as stock prices. The objective of this test case example is to use Prophet assisted forecasting and algorithmic trading in Python. The data we will be using is the historical daily S&P 500 adjusted close price available in Yahoo Finance.

Importing Libraries

Let’s set the working directory

import os

os.chdir(‘YourPath’) # Set working directory

and import the following libraries

import pandas as pd

import numpy as np

from fbprophet import Prophet

import matplotlib.pyplot as plt

from functools import reduce

%matplotlib inline

import warnings

warnings.filterwarnings(‘ignore’)

plt.style.use(‘seaborn-deep’)

pd.options.display.float_format = “{:,.2f}”.format

Data Preparation

Let’s read the input csv file

stock_price = pd.read_csv(‘^GSPC.csv’,parse_dates=[‘Date’])

stock_price.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 1005 entries, 0 to 1004 Data columns (total 7 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Date 1005 non-null datetime64[ns] 1 Open 1005 non-null float64 2 High 1005 non-null float64 3 Low 1005 non-null float64 4 Close 1005 non-null float64 5 Adj Close 1005 non-null float64 6 Volume 1005 non-null int64 dtypes: datetime64[ns](1), float64(5), int64(1) memory usage: 55.1 KB

Let’s check the statistics

stock_price.describe()

Let’s change the column names

stock_price = stock_price[[‘Date’,’Adj Close’]]

stock_price.columns = [‘ds’, ‘y’]

stock_price.tail(10)

Let’s plot the time-series

Prophet Forecast

Let’s call Prophet() and fit the above stock data by calling the method fit

model = Prophet()

model.fit(stock_price)

and use make_future_dataframe for forecasting

future = model.make_future_dataframe(100, freq=’d’)

future_boolean = future[‘ds’].map(lambda x : True if x.weekday() in range(0, 5) else False)

future = future[future_boolean]

future.tail()

followed by

forecast = model.predict(future)

forecast.tail()

Let’s plot the result

model.plot(forecast);

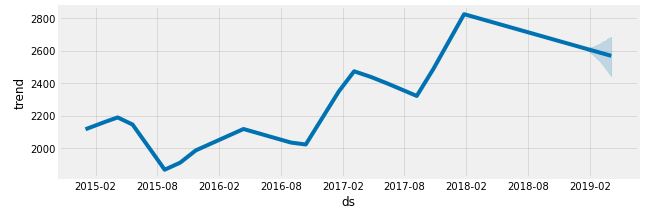

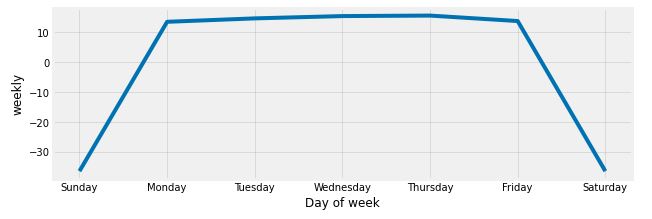

and all components

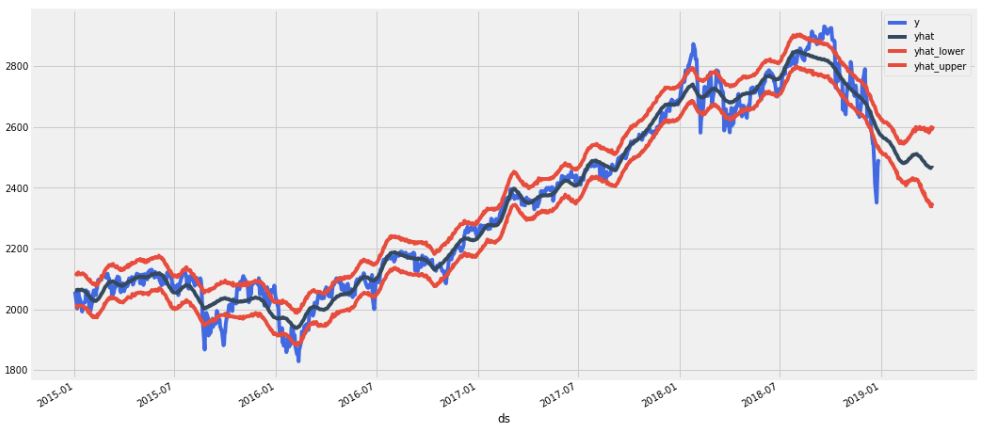

Let’s combine actual data and predictions with lower/upper limits into a single plot

stock_price_forecast = forecast[[‘ds’, ‘yhat’, ‘yhat_lower’, ‘yhat_upper’]]

df = pd.merge(stock_price, stock_price_forecast, on=’ds’, how=’right’)

df.set_index(‘ds’).plot(figsize=(16,8), color=[‘royalblue’, “#34495e”, “#e74c3c”, “#e74c3c”], grid=True);

Forecast Simulations

Let’s see how the above simulations and forecast can be used in trading scenario testing.

stock_price[‘dayname’] = stock_price[‘ds’].dt.day_name()

stock_price[‘month’] = stock_price[‘ds’].dt.month

stock_price[‘year’] = stock_price[‘ds’].dt.year

stock_price[‘month/year’] = stock_price[‘month’].map(str) + ‘/’ + stock_price[‘year’].map(str)

stock_price = pd.merge(stock_price,

stock_price[‘month/year’].drop_duplicates().reset_index(drop=True).reset_index(),

on=’month/year’,

how=’left’)

stock_price = stock_price.rename(columns={‘index’:’month/year_index’})

stock_price.tail()

Let’s run the loop over each unique month/year in the stock price while fitting the Prophet model and then applying a monthly forecast

loop_list = stock_price[‘month/year’].unique().tolist()

max_num = len(loop_list) – 1

forecast_frames = []

for num, item in enumerate(loop_list):

if num == max_num:

pass

else:

df = stock_price.set_index('ds')[

stock_price[stock_price['month/year'] == loop_list[0]]['ds'].min():\

stock_price[stock_price['month/year'] == item]['ds'].max()]

df = df.reset_index()[['ds', 'y']]

model = Prophet()

model.fit(df)

future = stock_price[stock_price['month/year_index'] == (num + 1)][['ds']]

forecast = model.predict(future)

forecast_frames.append(forecast)

INFO:fbprophet:Disabling yearly seasonality. Run prophet with yearly_seasonality=True to override this.

stock_price_forecast = reduce(lambda top, bottom: pd.concat([top, bottom], sort=False), forecast_frames)

stock_price_forecast = stock_price_forecast[[‘ds’, ‘yhat’, ‘yhat_lower’, ‘yhat_upper’]]

stock_price_forecast.to_csv(‘stock_price_forecast.csv’, index=False)

stock_price_forecast = pd.read_csv(‘stock_price_forecast.csv’, parse_dates=[‘ds’])

Let’s merge our data and plot the result

df = pd.merge(stock_price[[‘ds’,’y’, ‘month/year_index’]], stock_price_forecast, on=’ds’)

df[‘Percent Change’] = df[‘y’].pct_change()

df.set_index(‘ds’)[[‘y’, ‘yhat’, ‘yhat_lower’, ‘yhat_upper’]].plot(figsize=(16,8), color=[‘royalblue’, “#34495e”, “#e74c3c”, “#e74c3c”], grid=True)

df.head()

Trading Algorithm

Let’s test the following 4 initial trading algorithms/scenarios:

- Hold: Our bench mark. This is a buy and hold strategy. Meaning we buy the stock and hold it until the end time period.

- Prophet: This strategy is to sell when our forecast indicates a down trend and buy back in when it indicates an upward trend.

- Prophet Thresh: This strategy is to sell only when the stock price fall below our yhat_lower boundary.

- Seasonality: This strategy is to exit the market in August and re-enter in October. This was based on the seasonality chart, as shown above.

These algorithms are as follows

df[‘Hold’] = (df[‘Percent Change’] + 1).cumprod()

df[‘Prophet’] = ((df[‘yhat’].shift(-1) > df[‘yhat’]).shift(1) * (df[‘Percent Change’]) + 1).cumprod()

df[‘Prophet Thresh’] = ((df[‘y’] > df[‘yhat_lower’]).shift(1)* (df[‘Percent Change’]) + 1).cumprod()

df[‘Seasonality’] = ((~df[‘ds’].dt.month.isin([8,9])).shift(1) * (df[‘Percent Change’]) + 1).cumprod()

(df.dropna().set_index(‘ds’)[[‘Hold’, ‘Prophet’, ‘Prophet Thresh’,’Seasonality’]] * 1000).plot(figsize=(16,8), grid=True)

print(f”Hold = {df[‘Hold’].iloc[-1]1000:,.0f}”) print(f”Prophet = {df[‘Prophet’].iloc[-1]1000:,.0f}”)

print(f”Prophet Thresh = {df[‘Prophet Thresh’].iloc[-1]1000:,.0f}”) print(f”Seasonality = {df[‘Seasonality’].iloc[-1]1000:,.0f}”)

Hold = 1,230 Prophet = 1,126 Prophet Thresh = 1,176 Seasonality = 1,269

This is what we get by simulating an initial investment of $1,000. As we can see, the Seasonality and Hold scenarios yield the best outcome.

Summary

- It appears that Prophet works best with time-series data that have strong seasonal effects and several seasons of historical data. It handles outliers well. This observation does support previous studies.

- This project is a real-world realiability test of the serverless investing algorithm based on the AWS Lambda and Facebook Prophet as ML model. The performance efficiency and cost savings are beyond the scope of this study.

Leave a comment