- In this post, we will revisit most popular blue-chip stock portfolios using Python fintech libraries.

- Our objective is to optimize currently available quant trading and investing solutions for private DIY self-traders. Our trading approach consists of the following 4 steps:

- Step 1: Examine the AAPL trading signals and support/resistance regression lines.

- Step 2: Compare AAPL vs MSFT in terms of returns, volatility, covariance, and correlations.

- Step 3: Compare MA 10-20-30, daily returns, pair plots, correlations, Monte Carlo simulations, and Sharpe ratios of AAPL, AMZN, MSFT, and TSLA stocks.

- Step 4: Perform the SPY stock price analysis and FB Prophet forecast.

Let’s dive into the details below.

Table of Contents

- AAPL Trading Signals Verified

- AAPL/MSFT Risk vs ROI Analysis

- Popular 4-Stock Portfolio

- Monte-Carlo Predictions

- SPY Return/Volatility

- SPY Prophet Forecast

- Summary

- References

- Explore More

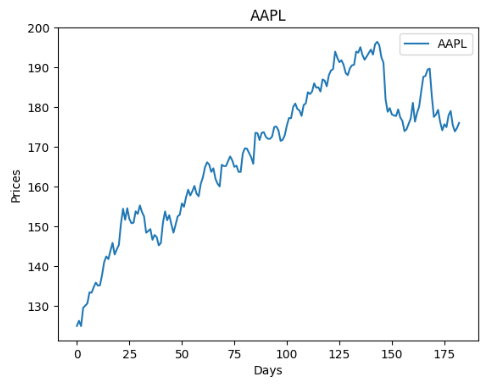

AAPL Trading Signals Verified

Let’s set the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

Let’s import the key libraries and define the following functions

import numpy as np

import pandas as pd

from math import sqrt

import matplotlib.pyplot as plt

import pandas_datareader as web

from scipy.signal import savgol_filter

from sklearn.linear_model import LinearRegression

from pandas_datareader import data as pdr

import yfinance as yfin

yfin.pdr_override()

def pythag(pt1, pt2):

a_sq = (pt2[0] - pt1[0]) ** 2

b_sq = (pt2[1] - pt1[1]) ** 2

return sqrt(a_sq + b_sq)

def regression_ceof(pts):

X = np.array([pt[0] for pt in pts]).reshape(-1, 1)

y = np.array([pt[1] for pt in pts])

model = LinearRegression()

model.fit(X, y)

return model.coef_[0], model.intercept_

def local_min_max(pts):

local_min = []

local_max = []

prev_pts = [(0, pts[0]), (1, pts[1])]

for i in range(1, len(pts) - 1):

append_to = ''

if pts[i-1] > pts[i] < pts[i+1]:

append_to = 'min'

elif pts[i-1] < pts[i] > pts[i+1]:

append_to = 'max'

if append_to:

if local_min or local_max:

prev_distance = pythag(prev_pts[0], prev_pts[1]) * 0.5

curr_distance = pythag(prev_pts[1], (i, pts[i]))

if curr_distance >= prev_distance:

prev_pts[0] = prev_pts[1]

prev_pts[1] = (i, pts[i])

if append_to == 'min':

local_min.append((i, pts[i]))

else:

local_max.append((i, pts[i]))

else:

prev_pts[0] = prev_pts[1]

prev_pts[1] = (i, pts[i])

if append_to == 'min':

local_min.append((i, pts[i]))

else:

local_max.append((i, pts[i]))

return local_min, local_max

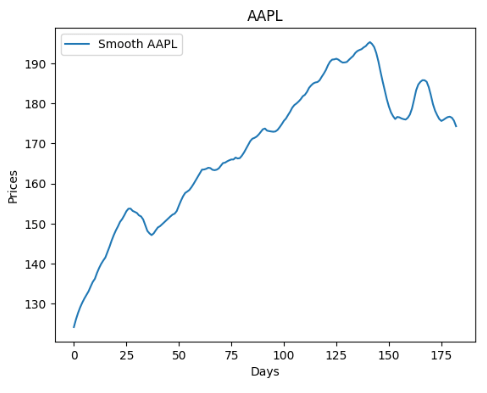

Let’s look at the smoothed version if the above plot

month_diff = series.shape[0] // 30

if month_diff == 0:

month_diff = 1

month_diff

6

smooth = int(2 * month_diff + 3)

smooth

15

pts = savgol_filter(series, smooth, 3)

plt.title(symbol)

plt.xlabel('Days')

plt.ylabel('Prices')

plt.plot(pts, label=f'Smooth {symbol}')

plt.legend()

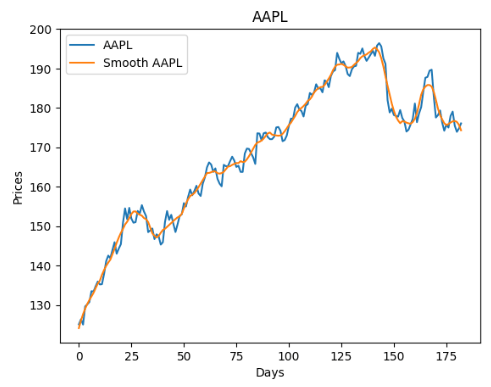

Let’s combine these two curves into the single joint plot

plt.title(symbol)

plt.xlabel('Days')

plt.ylabel('Prices')

plt.plot(series, label=symbol)

plt.plot(pts, label=f'Smooth {symbol}')

plt.legend()

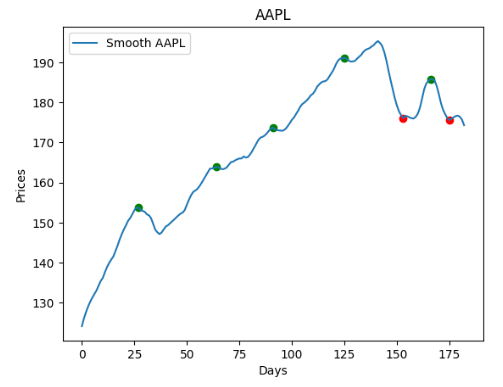

Let’s generate the trading signals using the smoothed price curve

local_min, local_max = local_min_max(pts)

plt.title(symbol)

plt.xlabel('Days')

plt.ylabel('Prices')

plt.plot(pts, label=f'Smooth {symbol}')

for pt in local_min:

plt.scatter(pt[0], pt[1], c='r')

for pt in local_max:

plt.scatter(pt[0], pt[1], c='g')

plt.legend()

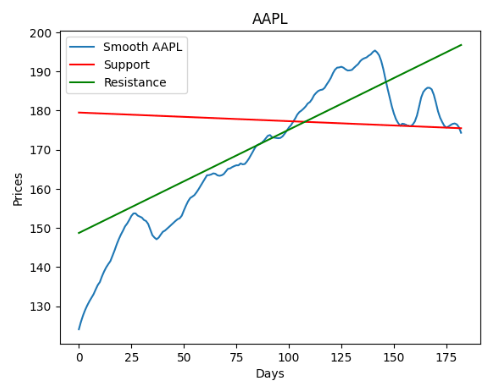

Let’s calculate the local support and resistance lines using the regression_ceof function

local_min_slope, local_min_int = regression_ceof(local_min)

local_max_slope, local_max_int = regression_ceof(local_max)

support = (local_min_slope * np.array(series.index)) + local_min_int

resistance = (local_max_slope * np.array(series.index)) + local_max_int

plt.title(symbol)

plt.xlabel('Days')

plt.ylabel('Prices')

plt.plot(pts, label=f'Smooth {symbol}')

plt.plot(support, label='Support', c='r')

plt.plot(resistance, label='Resistance', c='g')

plt.legend()

plt.title(symbol)

plt.xlabel('Days')

plt.ylabel('Prices')

plt.plot(series, label=symbol)

plt.plot(support, label='Support', c='r')

plt.plot(resistance, label='Resistance', c='g')

plt.legend()

Let’s plot the AAPL Simple Moving Average (SMA) to verify the 5-year MA crossover strategy

# import modules

from datetime import datetime

import yfinance as yf

import matplotlib.pyplot as plt

# initialize parameters

start_date = datetime(2017, 1, 1)

end_date = datetime(2023, 9, 26)

# get the data

df = yf.download('AAPL', start = start_date,

end = end_date)

import matplotlib

from pylab import rcParams

matplotlib.rcParams.update({'font.size': 18})

rcParams['figure.figsize'] = 15, 6

simple_ma = df["Close"].rolling(window=100).mean()

plt.figure(figsize=(14,8))

simple_ma.plot(label="Simple Moving Average")

df["Close"].plot(label="Closing Price")

plt.xticks(rotation=0)

plt.title("Moving Average of Closing Price", size=22)

plt.legend()

plt.show(

AAPL/MSFT Risk vs ROI Analysis

Following the quant trading diversification approach, we will show how a trader can reduce the volatility of the portfolio’s returns by choosing just 2 tech stocks such as AAPL and MSFT.

# Import libraries

import pandas as pd

import numpy as np

import yfinance as yf

import statsmodels.api as sm

from statsmodels.regression.rolling import RollingOLS

import matplotlib.pyplot as plt

import plotly.express as px

import plotly.graph_objects as go

from IPython.display import clear_output

#Download data

startdate='2023-01-01'

enddate='2023-09-26'

tickers = ['AAPL', 'MSFT']

price = yf.download(tickers, startdate, enddate)['Close']

price.tail()

[*********************100%***********************] 2 of 2 completed

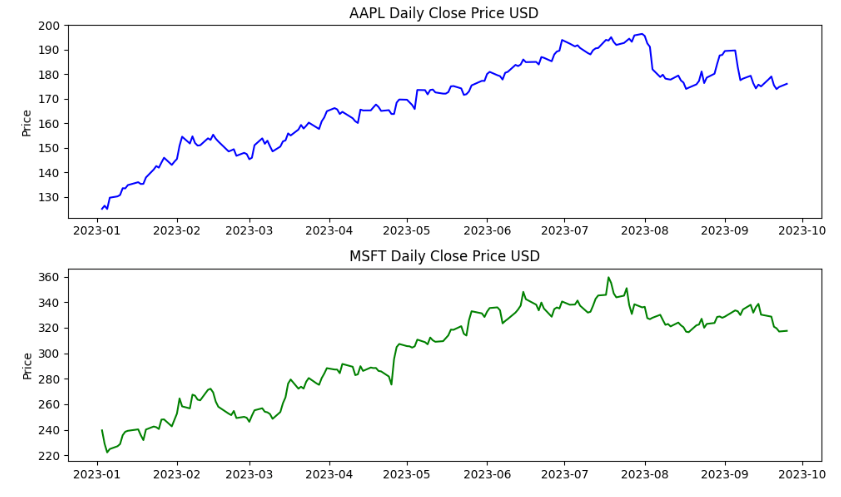

We can plot these two stocks as follows

# AAPL plot

plt.figure(figsize=(10,6))

plt.subplot(2, 1, 1)

plt.plot(price.AAPL, color='b')

plt.ylabel('Price')

plt.title('AAPL Daily Close Price USD')

# MSFT plot

plt.subplot(2, 1, 2)

plt.plot(price.MSFT, color='g')

plt.ylabel('Price')

plt.title('MSFT Daily Close Price USD')

# Use plt.tight_layout() to improve the spacing between subplots

plt.tight_layout()

plt.show()

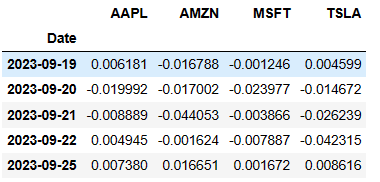

We can calculate their daily returns

returns = price.pct_change().dropna()

print(returns.tail())

AAPL MSFT

Date

2023-09-19 0.006181 -0.001246

2023-09-20 -0.019992 -0.023977

2023-09-21 -0.008889 -0.003866

2023-09-22 0.004945 -0.007887

2023-09-25 0.007380 0.001672

AAPL MSFT

count 182.000000 182.000000

mean 0.001970 0.001689

std 0.013394 0.016852

min -0.048020 -0.043743

25% -0.006398 -0.008414

50% 0.001838 0.000901

75% 0.009300 0.011763

max 0.046927 0.072435

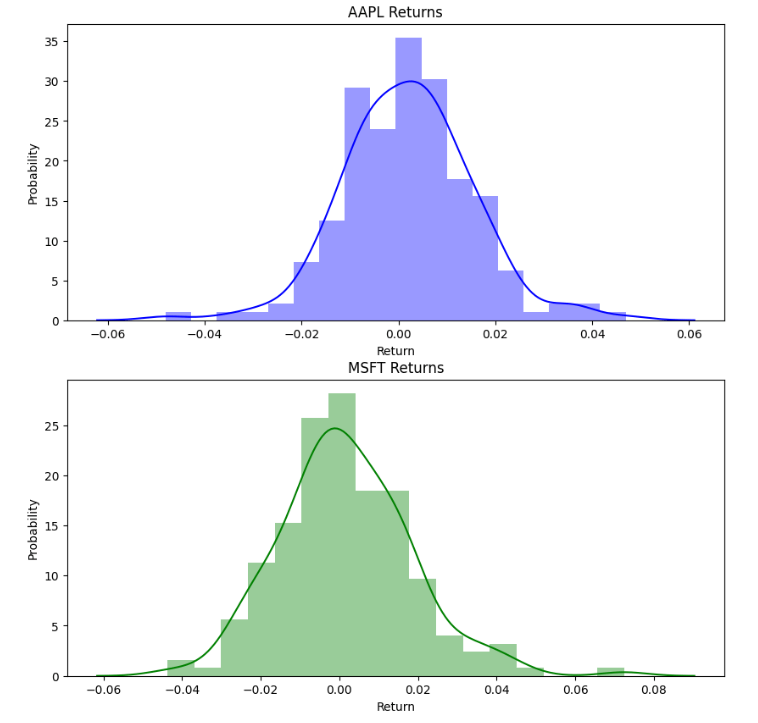

We can plot histograms or probabilities of their daily returns

import seaborn as sns

fig = plt.figure(figsize=(10,10))

# AAPL plot

plt.subplot(2, 1, 1)

sns.distplot(returns.AAPL, color='b');

plt.xlabel('Return')

plt.ylabel('Probability')

plt.title('AAPL Returns')

# MSFT plot

plt.subplot(2, 1, 2)

sns.distplot(returns.MSFT, color='g')

plt.xlabel('Return')

plt.ylabel('Probability')

plt.title('MSFT Returns')

plt.show()

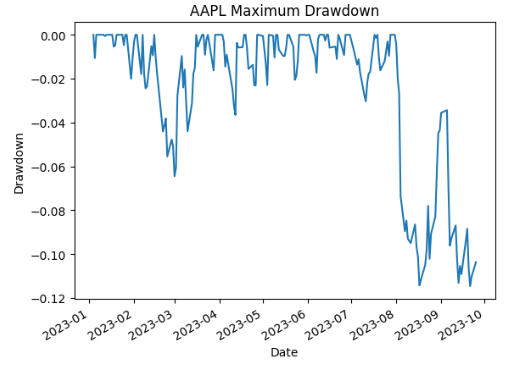

It is very interesting to compare Maximum Drawdown of these 2 stocks

wealth_index = (1+returns['AAPL']).cumprod()

previous_peaks_MSFT = wealth_index.cummax()

drawdowns_MSFT = (wealth_index - previous_peaks_MSFT)/previous_peaks_MSFT

drawdowns_MSFT.plot.line()

plt.ylabel('Drawdown')

plt.title('AAPL Maximum Drawdown')

drawdowns_MSFT.min(), drawdowns_MSFT.idxmin()

wealth_index = (1+returns['MSFT']).cumprod()

previous_peaks_MSFT = wealth_index.cummax()

drawdowns_MSFT = (wealth_index - previous_peaks_MSFT)/previous_peaks_MSFT

drawdowns_MSFT.plot.line()

plt.ylabel('Drawdown')

plt.title('MSFT Maximum Drawdown')

drawdowns_MSFT.min(), drawdowns_MSFT.idxmin()

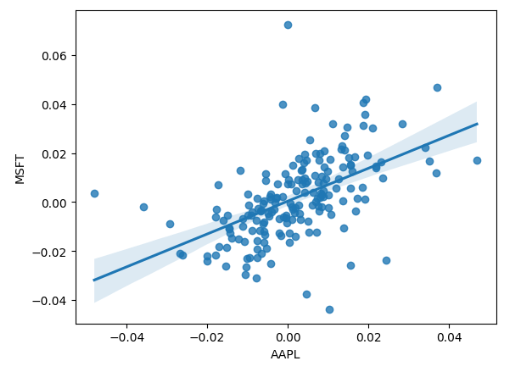

It is worthwhile to look at correlations of their returns

corr = returns[['AAPL', 'MSFT']].corr()

print(corr)

sns.scatterplot(x="AAPL", y="MSFT", data=returns)

sns.regplot(x="AAPL", y="MSFT", data=returns)

AAPL MSFT

AAPL 1.000000 0.532946

MSFT 0.532946 1.000000

Then we can calculate their compounded growth and covariance

n_days = returns.shape[0]

compounded_growth = (1+returns).prod()

n_periods = returns.shape[0]

ann_returns = compounded_growth**(252/n_days)-1

ann_returns

AAPL 0.605810

MSFT 0.477083

dtype: float64

cov = returns.cov()

cov

AAPL MSFT

AAPL 0.000179 0.000120

MSFT 0.000120 0.000284

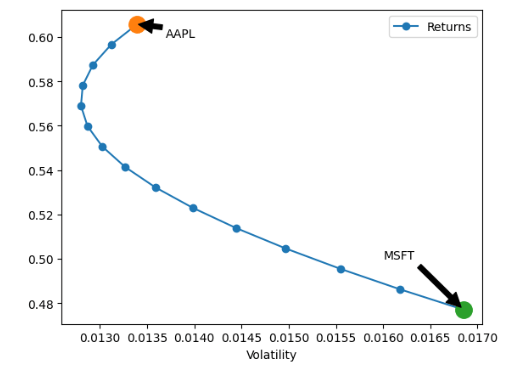

Let’s turn our attention to the efficient frontier of our 2 assets. In doing so, we need to calculate the portfolio return-volatility

# Calculate the portfolio return

def portfolio_return(w, r):

return w.T @ r

# Calculate the portfolio volatility return

def portfolio_vol(w, covmat):

return (w.T @ covmat @ w)**0.5

We are now ready to plot the efficient frontier curve

#Plot the efficient frontier of two assets

ax=plt.figure(figsize=(14,6))

n_points = 15

weights = [np.array([w, 1-w]) for w in np.linspace(0, 1, n_points)]

def plot_ef2(n_points, returns, cov):

weights = [np.array([w, 1-w]) for w in np.linspace(0, 1, n_points)]

rets = [portfolio_return(w, ann_returns) for w in weights]

vols = [portfolio_vol(w, cov) for w in weights]

ef = pd.DataFrame({

"Returns": rets,

"Volatility": vols

})

return ef.plot.line(x="Volatility", y="Returns", style="o-")

ax = plot_ef2(n_points, ann_returns, cov)

ax.plot([0.013394], [0.605810], 'o',markersize=14)

ax.annotate('AAPL', xy=(0.013394, 0.605810), xytext=(0.0137, 0.60),

arrowprops=dict(facecolor='black', shrink=0.05))

ax.plot([0.016852], [0.477083], 'o',markersize=14)

ax.annotate('MSFT', xy=(0.016852, 0.477083), xytext=(0.016, 0.5),

arrowprops=dict(facecolor='black', shrink=0.05))

Popular 4-Stock Portfolio

Our current objectives are as follows:

- Build moving average of selected stocks

- Determine correlations between stock returns

- Create and validate an optimal stock portfolio

- Predict the future behavior of selected stocks

#Import

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from pandas_datareader import data

from datetime import datetime

# Setting the begining and ending

today = datetime.now()

year_ago = datetime(today.year-1, today.month, today.day)

# Four company for data extraction

company_list = ['AAPL', 'TSLA', 'MSFT', 'AMZN']

Reading input stock data:

for company in company_list:

globals()[company] = pdr.get_data_yahoo(company, year_ago, today)

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

[*********************100%***********************] 1 of 1 completed

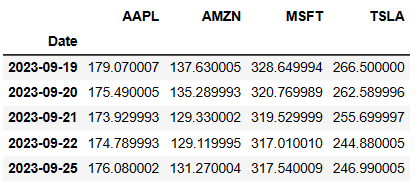

price = yf.download(company_list, startdate, enddate)['Close']

price.tail()

[*********************100%***********************] 4 of 4 completed

Let’s calculate MA 10-20-30

MA_days = [10, 20, 30]

for ma in MA_days:

ma_str = "MA AAPL {}".format(ma)

price[ma_str] = price.AAPL.rolling(ma).mean()

ma_str = "MA AMZN {}".format(ma)

price[ma_str] = price.AMZN.rolling(ma).mean()

ma_str = "MA MSFT {}".format(ma)

price[ma_str] = price.MSFT.rolling(ma).mean()

ma_str = "MA TSLA {}".format(ma)

price[ma_str] = price.TSLA.rolling(ma).mean()

price.tail()

AAPL AMZN MSFT TSLA MA AAPL 10 MA AMZN 10 MA MSFT 10 MA TSLA 10 MA AAPL 20 MA AMZN 20 MA MSFT 20 MA TSLA 20 MA AAPL 30 MA AMZN 30 MA MSFT 30 MA TSLA 30

Date

2023-09-19 179.070007 137.630005 328.649994 266.500000 177.631001 140.334001 332.945999 264.648001 180.4320 137.736501 329.637001 254.881998 179.340000 137.489334 326.883334 248.060999

2023-09-20 175.490005 135.289993 320.769989 262.589996 176.889001 140.327000 331.734998 265.715001 180.3450 137.788500 329.552501 256.351998 179.196334 137.334334 326.707334 248.490666

2023-09-21 173.929993 129.330002 319.529999 255.699997 176.526001 139.475000 330.696997 266.136000 179.9855 137.479000 329.179001 257.293998 179.054333 137.050334 326.617334 248.940999

2023-09-22 174.789993 129.119995 317.010010 244.880005 176.187001 138.564000 328.970999 265.774001 179.9060 137.343000 329.031001 258.035999 178.948333 136.735667 326.420001 248.925666

2023-09-25 176.080002 131.270004 317.540009 246.990005 175.859001 137.381000 326.931000 263.115002 179.7795 137.243501 328.759001 258.455999 178.891334 136.497667 326.304335 249.070333

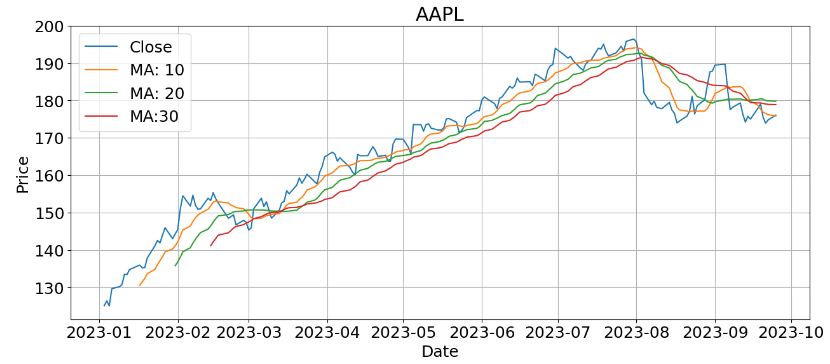

- AAPL MA 10-20-30:

import matplotlib

plt.figure(figsize=(15, 6))

matplotlib.rcParams.update({'font.size': 18})

plt.plot(price['AAPL'])

plt.plot(price['MA AAPL 10'])

plt.plot(price['MA AAPL 20'])

plt.plot(price['MA AAPL 30'])

plt.title('AAPL')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend(('Close','MA: 10', 'MA: 20', 'MA:30'))

plt.grid()

plt.show()

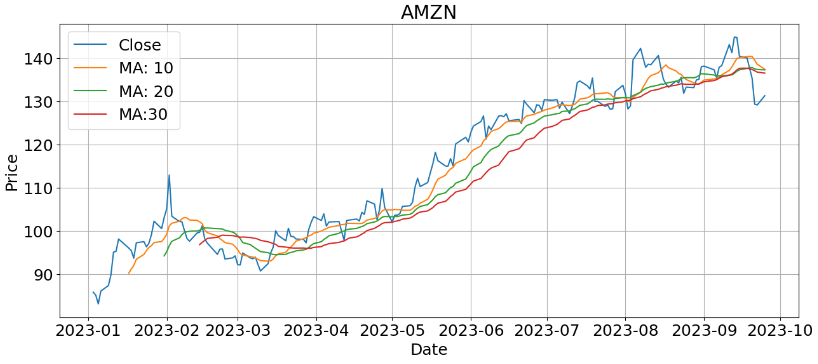

- AMZN MA 10-20-30:

plt.figure(figsize=(15, 6))

matplotlib.rcParams.update({'font.size': 18})

plt.plot(price['AMZN'])

plt.plot(price['MA AMZN 10'])

plt.plot(price['MA AMZN 20'])

plt.plot(price['MA AMZN 30'])

plt.title('AMZN')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend(('Close','MA: 10', 'MA: 20', 'MA:30'))

plt.grid()

plt.show()

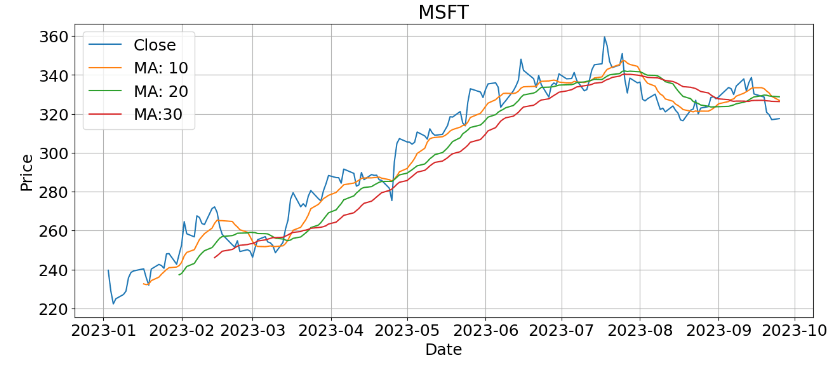

- MSFT MA 10-20-30:

plt.figure(figsize=(15, 6))

matplotlib.rcParams.update({'font.size': 18})

plt.plot(price['MSFT'])

plt.plot(price['MA MSFT 10'])

plt.plot(price['MA MSFT 20'])

plt.plot(price['MA MSFT 30'])

plt.title('MSFT')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend(('Close','MA: 10', 'MA: 20', 'MA:30'))

plt.grid()

plt.show()

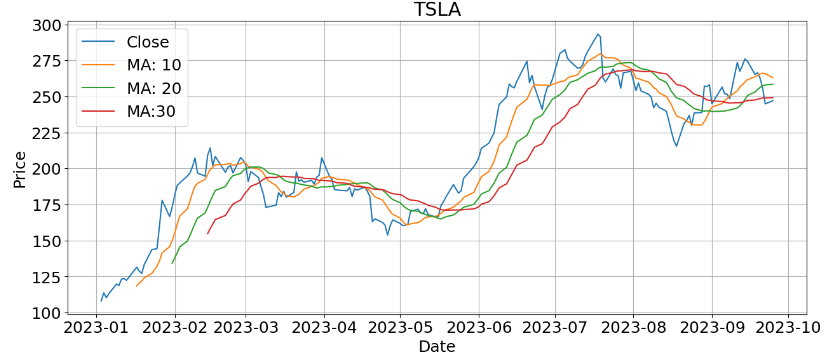

- TSLA MA 10-20-30:

plt.figure(figsize=(15, 6))

matplotlib.rcParams.update({'font.size': 18})

plt.plot(price['TSLA'])

plt.plot(price['MA TSLA 10'])

plt.plot(price['MA TSLA 20'])

plt.plot(price['MA TSLA 30'])

plt.title('TSLA')

plt.xlabel('Date')

plt.ylabel('Price')

plt.legend(('Close','MA: 10', 'MA: 20', 'MA:30'))

plt.grid()

plt.show()

Let’s calculate and plot Daily Returns of our 4 stocks

price['Daily Returns AAPL'] = price['AAPL'].pct_change()

price['Daily Returns AMZN'] = price['AMZN'].pct_change()

price['Daily Returns MSFT'] = price['MSFT'].pct_change()

price['Daily Returns TSLA'] = price['TSLA'].pct_change()

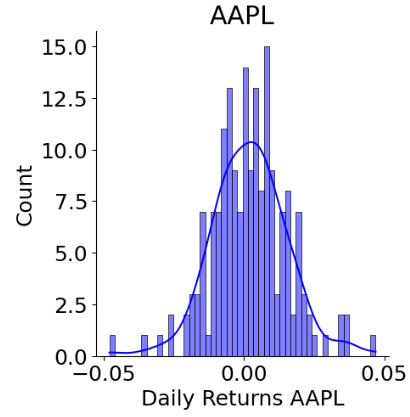

- Daily Returns AAPL

sns.displot(price['Daily Returns AAPL'].dropna(), bins=50, color='blue', kde=True)

plt.title("AAPL")

plt.show()

- Daily Returns AMZN

sns.displot(price['Daily Returns AMZN'].dropna(), bins=50, color='blue', kde=True)

plt.title("AMZN")

plt.show()

- Daily Returns MSFT

sns.displot(price['Daily Returns MSFT'].dropna(), bins=50, color='blue', kde=True)

plt.title("MSFT")

plt.show()

- Daily Returns TSLA

sns.displot(price['Daily Returns TSLA'].dropna(), bins=50, color='blue', kde=True)

plt.title("TSLA")

plt.show()

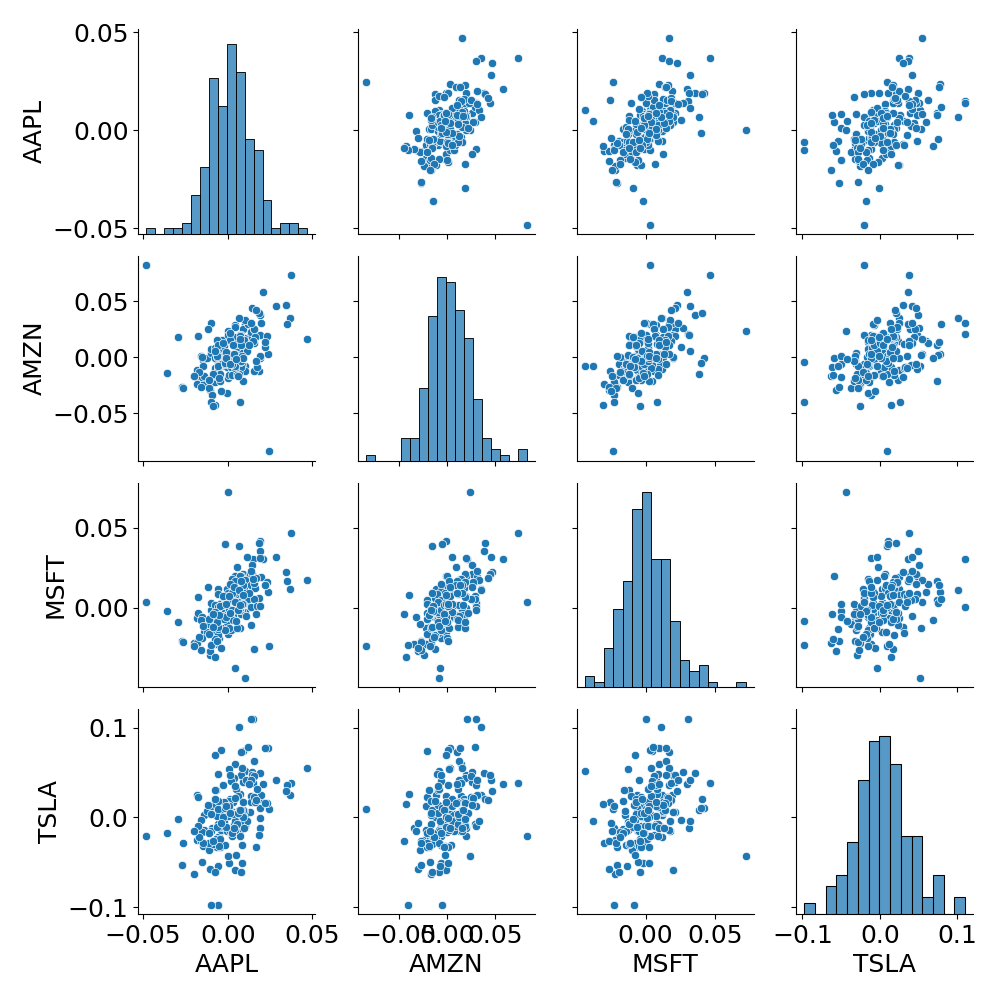

Let’s prepare the above returns for the stock correlation analysis

stock_returns = pd.DataFrame()

stock_returns['AAPL']=price['Daily Returns AAPL'].dropna()

stock_returns['AMZN']=price['Daily Returns AMZN'].dropna()

stock_returns['MSFT']=price['Daily Returns MSFT'].dropna()

stock_returns['TSLA']=price['Daily Returns TSLA'].dropna()

stock_returns.tail()

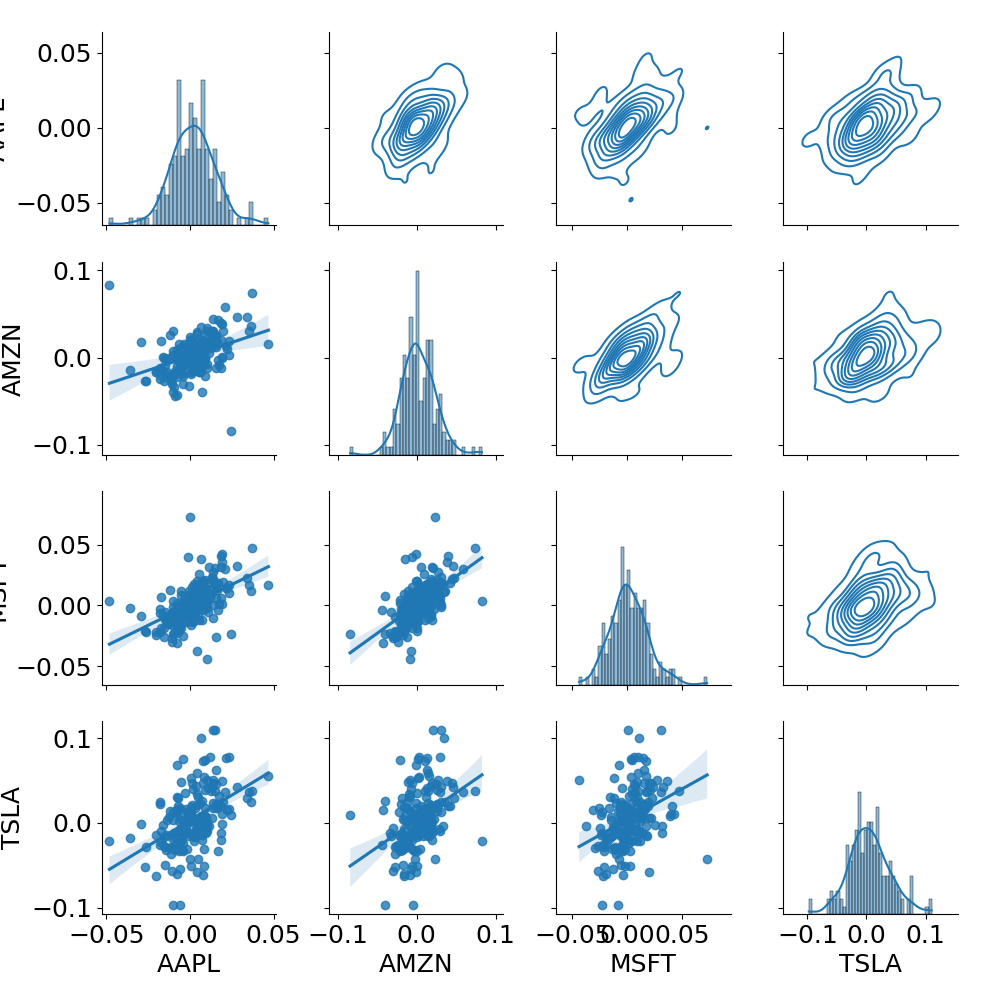

- Pair plot

sns.pairplot(stock_returns)

plt.savefig('pairplot_tech.png')

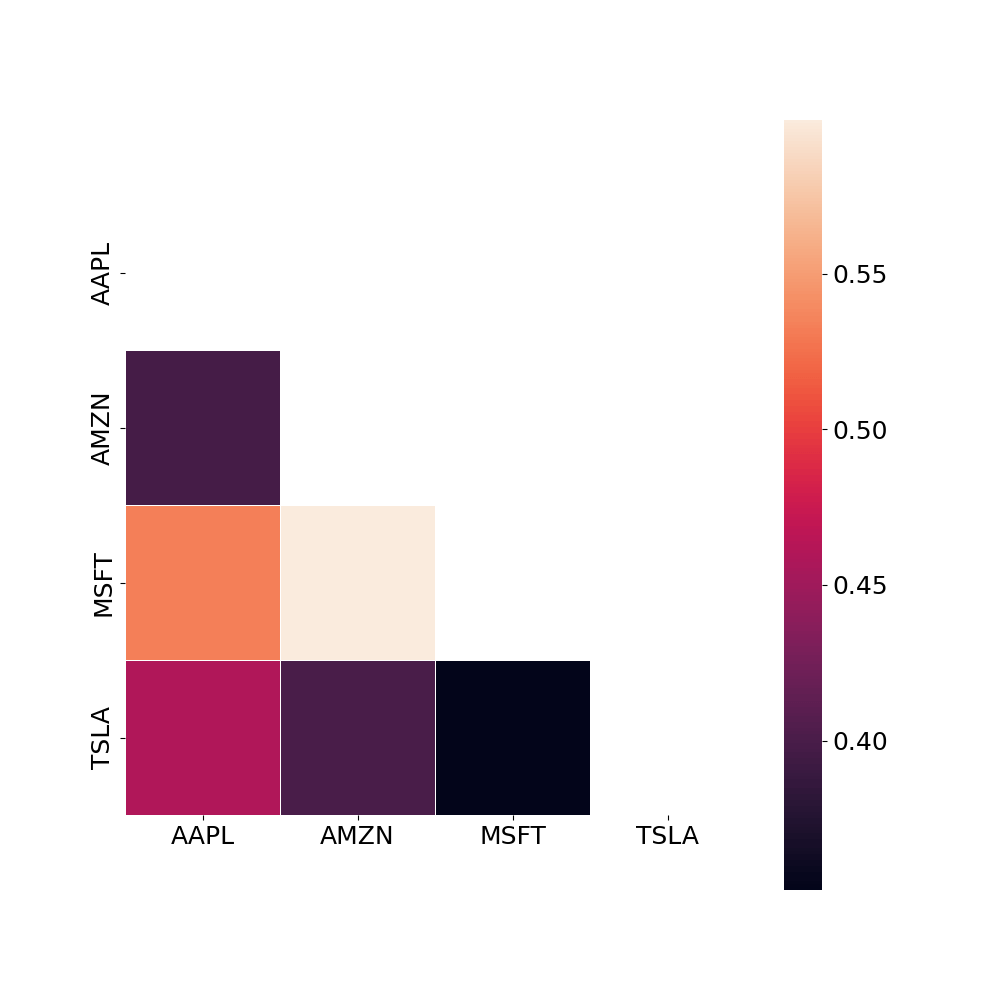

- Correlation matrix

# Build correlation matrix

corr = stock_returns.corr()

mask = np.triu(np.ones_like(corr, dtype=bool))

plt.figure(figsize=(10, 10))

sns.heatmap(corr, mask=mask, square=True, linewidths=.5, annot=True)

#plt.show()

plt.savefig('corrmatrix_tech.png')

- Joint plot

def draw_jointplot(data):

grid = sns.PairGrid(data.dropna())

grid.map_diag(sns.histplot, bins=40, kde=True)

grid.map_lower(sns.regplot)

grid.map_upper(sns.kdeplot)

draw_jointplot(stock_returns)

plt.savefig('stockreturns_tech.png')

Here, Row 1: AAPL, Row 2: AMZN, Row 3: MSFT, Row 4: TSLA.

Let’s calculate the mean returns and covariance of our stocks

mean_income = stock_returns.mean() # Mean income for each stock

cov_returns = stock_returns.cov() # Covariation

count = len(stock_returns.columns)

print(mean_income, cov_returns, sep='\n')

AAPL 0.001970

AMZN 0.002569

MSFT 0.001689

TSLA 0.005150

dtype: float64

AAPL AMZN MSFT TSLA

AAPL 0.000179 0.000115 0.000120 0.000215

AMZN 0.000115 0.000467 0.000218 0.000301

MSFT 0.000120 0.000218 0.000284 0.000207

TSLA 0.000215 0.000301 0.000207 0.001217

Let’s find the maximum Sharpe ratio of our portfolio by generating random shares while plotting the efficient frontier curve as an envelope

# Function, that generate random shares

def randomPortfolio():

share = np.exp(np.random.randn(count))

share = share / share.sum()

return share

def IncomePortfolio(Rand):

return np.matmul(mean_income.values, Rand)

def RiskPortfolio(Rand):

return np.sqrt(np.matmul(np.matmul(Rand, cov_returns.values), Rand))

combinations = 4000

risk = np.zeros(combinations)

income = np.zeros(combinations)

portfolio = np.zeros((combinations, count))

# Function, which create new combinations of shares

for i in range(combinations):

rand = randomPortfolio()

portfolio[i, :] = rand

risk[i] = RiskPortfolio(rand)

income[i] = IncomePortfolio(rand)

plt.figure(figsize=(15, 8))

plt.scatter(risk * 100, income * 100, c="b", marker="o",s=20)

plt.xlabel("Risk")

plt.ylabel("Income")

plt.title("Portfolios")

MaxSharpRatio = np.argmax(income / risk)

plt.scatter([risk[MaxSharpRatio] * 100], [income[MaxSharpRatio] * 100], s=140,c="r", marker="o", label="Max Sharp ratio")

plt.legend()

#plt.show()

plt.savefig('efficiencycurve_portfolios.png')

Finally, we can compare the maximum Sharpe ratios of our stocks

best_port = portfolio[MaxSharpRatio]

for i in range(len(company_list)):

print("{} : {}".format(company_list[i], best_port[i]))

AAPL : 0.5737824378783145

TSLA : 0.1887338094255849

MSFT : 0.033839219286878226

AMZN : 0.2036445334092224

Monte-Carlo Predictions

We will consider the 1Y forecast with the mean and STD values

days = 365

dt = 1 / days

stock_returns.dropna(inplace=True)

mu = stock_returns.mean()

sigma = stock_returns.std()

We need the following function

def monte_carlo(start_price, days, mu, sigma):

price = np.zeros(days)

price[0] = start_price

shock = np.zeros(days)

drift = np.zeros(days)

for x in range(1, days):

shock[x] = np.random.normal(loc=mu * dt, scale=sigma*np.sqrt(dt))

drift[x] = mu * dt

price[x] = price[x-1] + (price[x-1] * (drift[x] + shock[x]))

return price

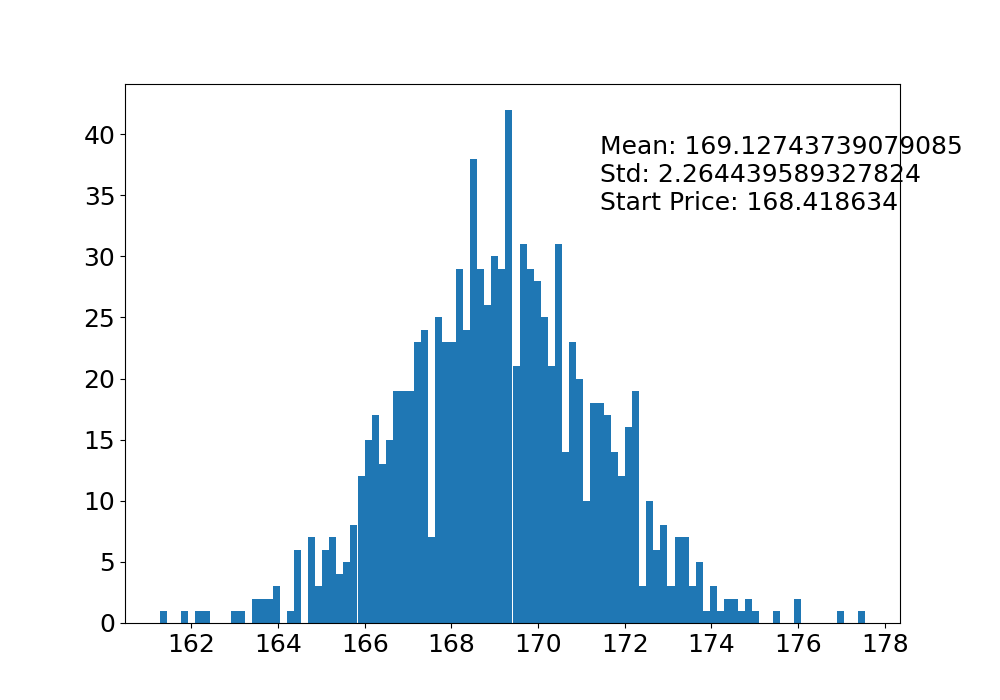

- AAPL

price['AAPL'].describe()

count 183.000000

mean 168.418634

std 17.755754

min 125.019997

25% 153.840004

50% 172.690002

75% 180.955002

max 196.449997

Name: AAPL, dtype: float64

start_price = 168.418634

sim = np.zeros(1000)

plt.figure(figsize=(15, 8))

for i in range(1000):

result = monte_carlo(start_price, days, mu['AAPL'], sigma['AAPL'])

sim[i] = result[days - 1]

plt.plot(result)

plt.xlabel('Days')

plt.ylabel('Price')

plt.title('Monte Carlo Analysis for AAPL')

plt.savefig('monte_aapl.png')

plt.figure(figsize=(10, 7))

plt.hist(sim, bins=100)

plt.figtext(0.6, 0.7, "Mean: {} \nStd: {} \nStart Price: {}".format(sim.mean(), sim.std(), start_price))

#plt.show()

plt.savefig('montehist_aapl.png')

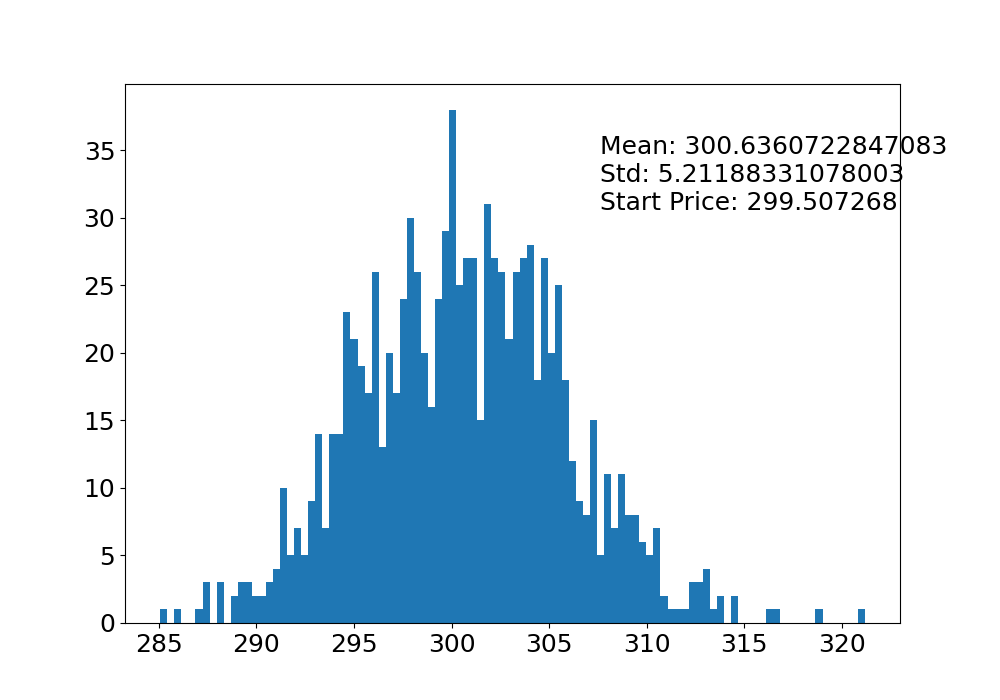

- MSFT

price['MSFT'].describe()

count 183.000000

mean 299.507268

std 36.373372

min 222.309998

25% 267.145004

50% 311.739990

75% 330.964996

max 359.489990

Name: MSFT, dtype: float64

start_price = 299.507268

sim = np.zeros(1000)

plt.figure(figsize=(15, 8))

for i in range(1000):

result = monte_carlo(start_price, days, mu['MSFT'], sigma['MSFT'])

sim[i] = result[days - 1]

plt.plot(result)

plt.xlabel('Days')

plt.ylabel('Price')

plt.title('Monte Carlo Analysis for MSFT')

plt.savefig('monte_msft.png')

plt.figure(figsize=(10, 7))

plt.hist(sim, bins=100)

plt.figtext(0.6, 0.7, "Mean: {} \nStd: {} \nStart Price: {}".format(sim.mean(), sim.std(), start_price))

#plt.show()

plt.savefig('montehist_msft.png')

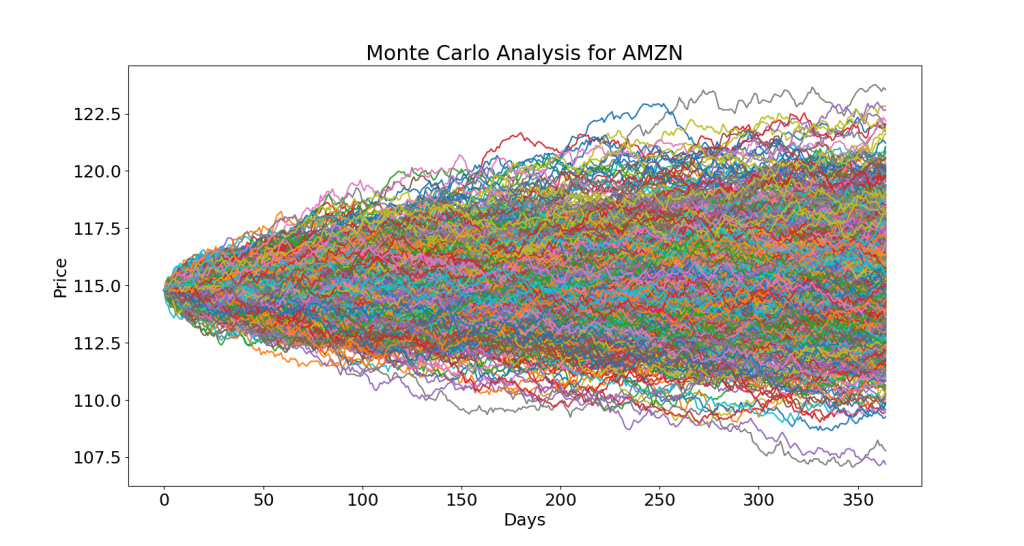

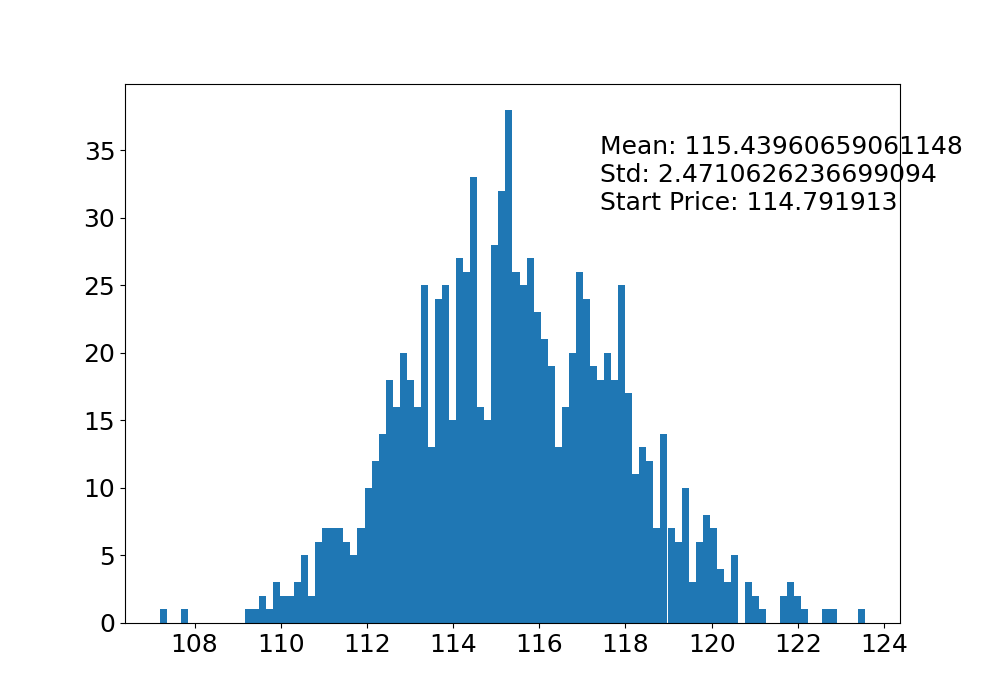

- AMZN

price['AMZN'].describe()

count 183.000000

mean 114.791913

std 17.026834

min 83.120003

25% 99.380001

50% 112.910004

75% 130.184998

max 144.850006

Name: AMZN, dtype: float64

start_price = 114.791913

sim = np.zeros(1000)

plt.figure(figsize=(15, 8))

for i in range(1000):

result = monte_carlo(start_price, days, mu['AMZN'], sigma['AMZN'])

sim[i] = result[days - 1]

plt.plot(result)

plt.xlabel('Days')

plt.ylabel('Price')

plt.title('Monte Carlo Analysis for AMZN')

plt.savefig('monte_amzn.png')

plt.figure(figsize=(10, 7))

plt.hist(sim, bins=100)

plt.figtext(0.6, 0.7, "Mean: {} \nStd: {} \nStart Price: {}".format(sim.mean(), sim.std(), start_price))

#plt.show()

plt.savefig('montehist_amzn.png')

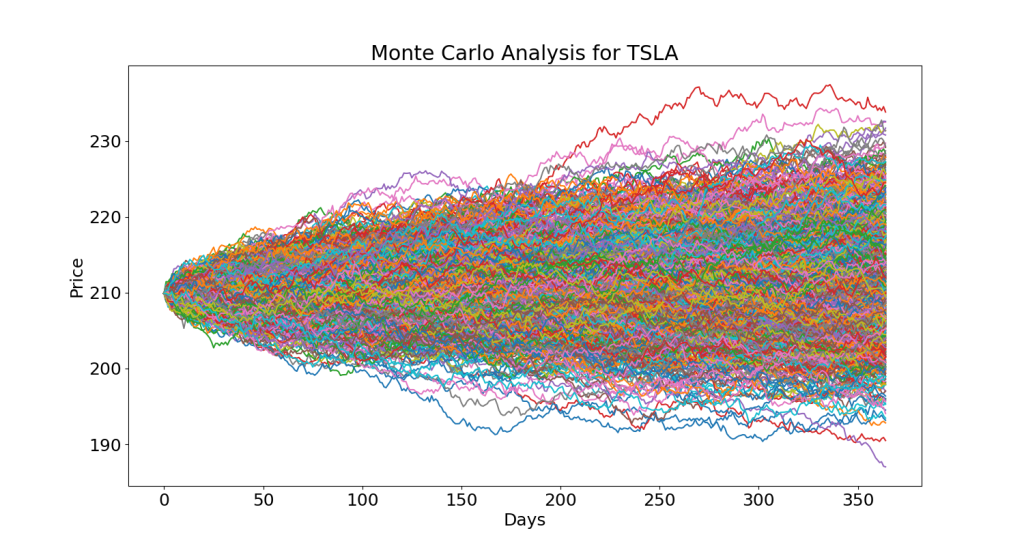

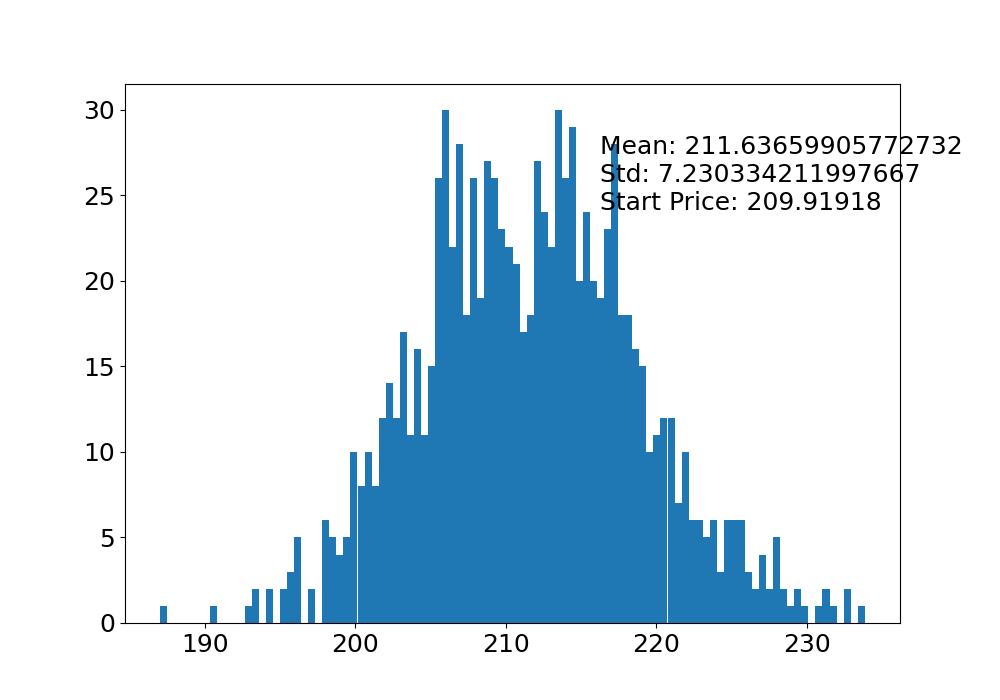

- TSLA

price['TSLA'].describe()

count 183.000000

mean 209.919180

std 45.605744

min 108.099998

25% 180.294998

50% 201.289993

75% 254.904999

max 293.339996

Name: TSLA, dtype: float64

plt.figure(figsize=(10, 7))

plt.hist(sim, bins=100)

plt.figtext(0.6, 0.7, "Mean: {} \nStd: {} \nStart Price: {}".format(sim.mean(), sim.std(), start_price))

#plt.show()

plt.savefig('montehist_tsla.png')

SPY Return/Volatility

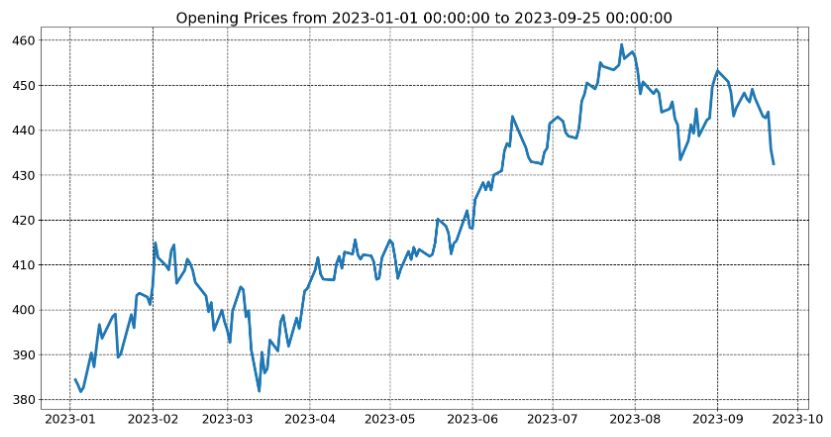

Let’s look at the SPY index in 2023

# import modules

from datetime import datetime

import yfinance as yf

import matplotlib.pyplot as plt

# initialize parameters

start_date = datetime(2023, 1, 1)

end_date = datetime(2023, 9, 25)

# get the data

data = yf.download('SPY', start = start_date,

end = end_date)

# display

plt.figure(figsize = (20,10))

plt.title('Opening Prices from {} to {}'.format(start_date,

end_date))

plt.plot(data['Open'],lw=4)

plt.grid(color='k', linestyle='--', linewidth=1)

plt.show()

Let’s calculate the average annual SPY return and volatility

nifty=data.copy()

nifty_returns=(nifty['Close']/nifty['Open'])-1

volatility= np.std(nifty_returns)

trading_days=len(nifty_returns)

mean=nifty_returns.mean()

print('Annual Average SPY return',mean)

print('Annual volatility',volatility*np.sqrt(trading_days))

print('Number of trading days',trading_days)

Annual Average SPY return 0.0006876400629725226

Annual volatility 0.09887050147370505

Number of trading days 182

The SPY daily returns are given by

daily_returns=np.random.normal(mean/trading_days,volatility,trading_days)+1

index_returns=[10980]

for x in daily_returns:

index_returns.append(index_returns[-1]*x)

plt.plot(daily_returns)

plt.show()

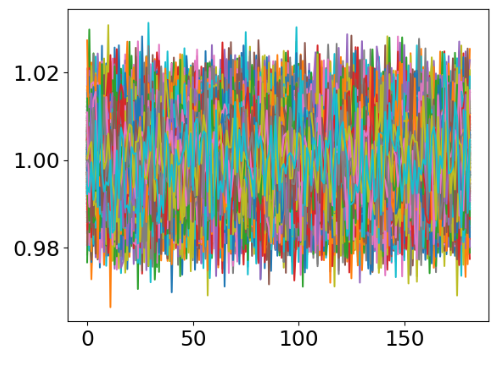

The corresponding 1000 random simulations of daily returns are

for i in range(1000):

daily_returns=np.random.normal(mean/trading_days,volatility,trading_days)+1

index_returns=[10980]

for x in daily_returns:

index_returns.append(index_returns[-1]*x)

plt.plot(daily_returns)

plt.show()

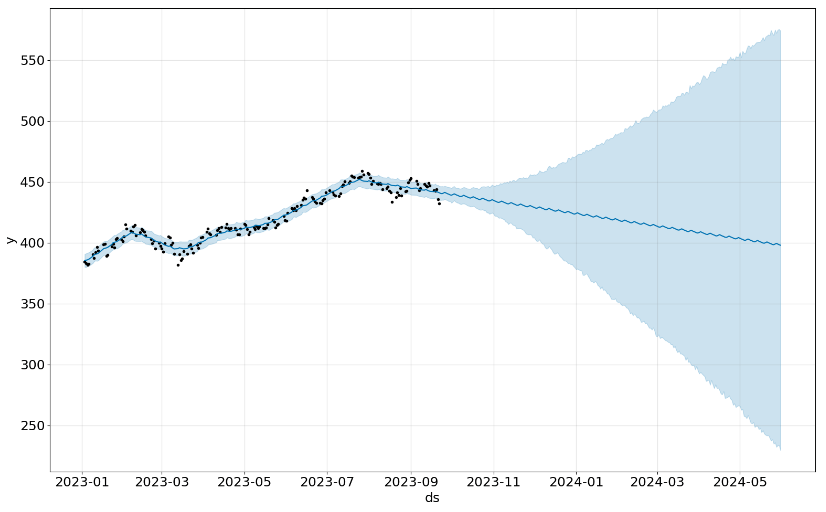

SPY Prophet Forecast

Let’s prepare the SPY stock data for the FB Prophet forecast

nifty.reset_index(inplace=True)

nifty['Date']= pd.to_datetime(nifty['Date'])

nifty.rename(columns={'Date':'ds','Open':'y'},inplace=True)

The forecast model is expressed as

from prophet import Prophet

model=Prophet()

model.fit(nifty)

predict_df=model.make_future_dataframe(periods=252)

predict_df.tail()

ds

429 2024-05-27

430 2024-05-28

431 2024-05-29

432 2024-05-30

433 2024-05-31

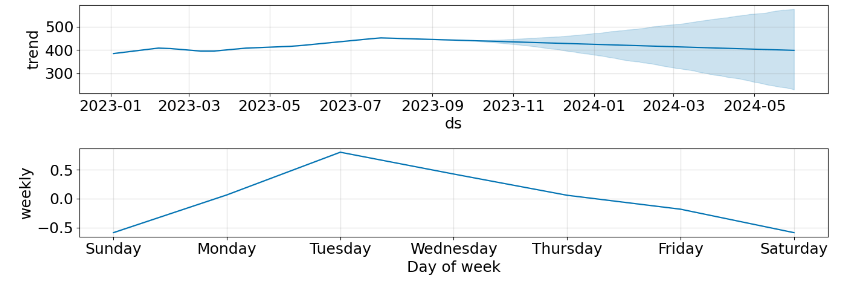

Let’s plot the forecast and its components

forecast=model.predict(predict_df)

fig1=model.plot(forecast)

plt.xticks(fontsize = 15)

fig2=model.plot_components(forecast,figsize=(14,5))

Summary

- In this post, we have shown how to compute stock volatility in Python and the different measures of risk-adjusted returns based on it.

- While we continue to rank SPY as a long-term hold position, we focused our discussion on rather short-term trading strategies to see how top blue-chip stocks have now again gained positive momentum.

- The AAPL example has explained how quant traders can use various SMA and MA crossovers to identify buy and sell signals. These signals have been verified using regression support and resistance lines.

- The AAPL-MSFT example has illustrated the value of an efficient frontier graph, maximum drawdown curves, correlations of returns, covariance metrics, and the compounded growth.

- The 4-stock portfolio example has demonstrated the importance of comparing and integrating popular trading indicators, correlation plots, and Monte Carlo simulations.

- Finally, we have analyzed the SPY index in terms of volatility and average returns using both historical data and the Prophet forecast model.

- Results produced by this software have been verified by comparison to a number of well known 3rd party trading platforms such as Macroaxis, TradingView, Barchart, etc.

References

- GitHub Rep

- Volatility And Measures Of Risk-Adjusted Return With Python

- Buy and Sell Signals with the Simple Moving Average Crossover

- Scalable Time-Series Forecasting with Spark and Prophet

- How to Download historical stock prices in Python ?

- Monte Carlo Methods

- Predicting Nifty using Monte Carlo, fbprophet

Explore More

- Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

- Risk-Aware Strategies for DCA Investors

- Joint Analysis of Bitcoin, Gold and Crude Oil Prices with Optimized Risk/Return in 2023

- Towards Max(ROI/Risk) Trading

- DJI Market State Analysis using the Cruz Fitting Algorithm

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- A TradeSanta’s Quick Guide to Best Swing Trading Indicators

- Stock Portfolio Risk/Return Optimization

- Risk/Return QC via Portfolio Optimization – Current Positions of The Dividend Breeder

- Portfolio Optimization Risk/Return QC – Positions of Humble Div vs Dividend Glenn

- The Qullamaggie’s TSLA Breakouts for Swing Traders

- The Qullamaggie’s OXY Swing Breakouts

- Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

- Quant Trading using Monte Carlo Predictions and 62 AI-Assisted Trading Technical Indicators (TTI)

- Are Blue-Chips Perfect for This Bear Market?

- Track All Markets with TradingView

- S&P 500 Algorithmic Trading with FBProphet

- Stock Forecasting with FBProphet

- Predicting Trend Reversal in Algorithmic Trading using Stochastic Oscillator in Python

- Inflation-Resistant Stocks to Buy

- ML/AI Regression for Stock Prediction – AAPL Use Case

- Macroaxis Wealth Optimization

- Investment Risk Management Study

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly

Leave a comment