Featured Photo by Ella Olsson on Pexels

Inspired by the recent TSA e-commerce use-case, this article is a beginner-friendly guide to help you understand and evaluate ARIMA-based time-series forecasting models such as SARIMA and SARIMAX.

Objective: To understand the basic concepts of ARIMA, SARIMA and SARIMAX in terms of Time Series Forecasting QC.

Application: We will focus on an QC-optimized SARIMA(X) model in order to forecast the e-commerce sales of a food delivery company based in Helsinki, Finland.

Insights: We will assume that delivery companies get its revenue from two main sources:

- Up to 30% cut from every order.

- Delivery fees.

The first revenue stream depends upon the order volume and the value of each order. The second revenue is linked to multiple sources such as delivery distance, order size, order value, day of the week, etc.

Concepts:

- ACF, PACF

- Seasonal Decomposition

- Stationarity of time-series

- ADF & KPSS Tests

- Hyper-Parameter Optimization (HPO)

- SARIMA/SARIMAX: Model QC Comparisons

- Evaluation Metrics: AIC, BIC, MSE, SSE, and RMSE

Table of Contents:

- Libraries

- Input Data

- Feature Engineering

- Temporal Patterns

- ADF & KPSS Tests

- ACF & PACF

- SARIMA Model

- SARIMAX Model

- Model Comparison

- Summary

- Explore More

- Embed Socials

- Infographic

You can go through the below articles for more details on ARIMA-related topics:

- Complete Guide To SARIMAX in Python for Time Series Modeling

- Time Series Forecasting with SARIMAX

- Time Series Forecasting with ARIMA , SARIMA and SARIMAX

- ARIMA SARIMA SARIMAX For Beginners

Libraries

Let’s set the working directory YOURPATH

import os

os.chdir(‘YOURPATH’)

os. getcwd()

and import the following libraries

import itertools

import warnings

from datetime import datetime, timedelta

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from pandas.plotting import lag_plot

import seaborn as sns

%matplotlib inline

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.stattools import adfuller, kpss

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.statespace.sarimax import SARIMAX

from statsmodels.tools.sm_exceptions import ConvergenceWarning

Input Data

Let’s load the input dataset

source_df = pd.read_csv(‘orders.csv’)

df = source_df.copy()

df.tail(5)

df.shape

(18706, 13)

df[‘TIMESTAMP’] = pd.to_datetime(df[‘TIMESTAMP’])

df.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 18706 entries, 0 to 18705 Data columns (total 13 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 TIMESTAMP 18706 non-null datetime64[ns] 1 ACTUAL_DELIVERY_MINUTES - ESTIMATED_DELIVERY_MINUTES 18706 non-null int64 2 ITEM_COUNT 18706 non-null int64 3 USER_LAT 18706 non-null float64 4 USER_LONG 18706 non-null float64 5 VENUE_LAT 18706 non-null float64 6 VENUE_LONG 18706 non-null float64 7 ESTIMATED_DELIVERY_MINUTES 18706 non-null int64 8 ACTUAL_DELIVERY_MINUTES 18706 non-null int64 9 CLOUD_COVERAGE 18429 non-null float64 10 TEMPERATURE 18429 non-null float64 11 WIND_SPEED 18429 non-null float64 12 PRECIPITATION 18706 non-null float64 dtypes: datetime64[ns](1), float64(8), int64(4) memory usage: 1.9 MB

df.describe().T

We can see that there are no extreme deviations between mean and median values of each column. This suggests that we can expect little skewness in the distributions.

Let’s look at the spatial content of our input data

plt.scatter(df[‘USER_LAT’],df[‘USER_LONG’],c=df[‘ACTUAL_DELIVERY_MINUTES’])

plt.colorbar()

plt.title(“ACTUAL_DELIVERY_MINUTES”)

plt.xlabel(“USER_LAT”)

plt.ylabel(“USER_LONG”)

plt.savefig(‘inputdeliverymin.png’)

plt.scatter(df[‘VENUE_LAT’],df[‘VENUE_LONG’],c=df[‘ITEM_COUNT’])

plt.colorbar()

plt.title(“ITEM_COUNT”)

plt.xlabel(“VENUE_LAT”)

plt.ylabel(“VENUE_LONG”)

plt.savefig(‘inputvenueitemcount.png’)

Feature Engineering

Let’s plot the sns Pearson correlation heatmap

def correlation_check(df: pd.DataFrame) -> None:

“””

Plots a Pearson Correlation Heatmap.

—

Args:

df (pd.DataFrame): dataframe to plot

Returns: None

"""

# Pretty Name

df.rename(columns={"ACTUAL_DELIVERY_MINUTES - ESTIMATED_DELIVERY_MINUTES": "ACTUAL-ESTIMATED"},

inplace=True)

# Figure

fig, ax = plt.subplots(figsize=(16,12), facecolor='w')

correlations_df = df.corr(method='pearson', min_periods=1)

sns.heatmap(correlations_df, cmap="Oranges", annot=True, linewidth=.1)

# Labels

ax.set_title("Pearson Correlation Heatmap", fontsize=15, pad=10)

ax.set_facecolor(color='white')

correlation_check(df)

plt.savefig(‘salesheatmap.png’)

We can also check feature correlations via the sns pairplot

sns.pairplot(data=df)

plt.savefig(‘salespairplot.png’)

As with the heatmap, the pair-plot didn’t reveal any underlying, strong relationship between the variables. Exceptions:

- ACTUAL_DELIVERY_MINUTES – ESTIMATED_DELIVERY_MINUTES is strongly correlated with ACTUAL_DELIVERY_MINUTES and ESTIMATED_DELIVERY_MINUTES.

- There are correlations between spatial coordinates.

Temporal Patterns

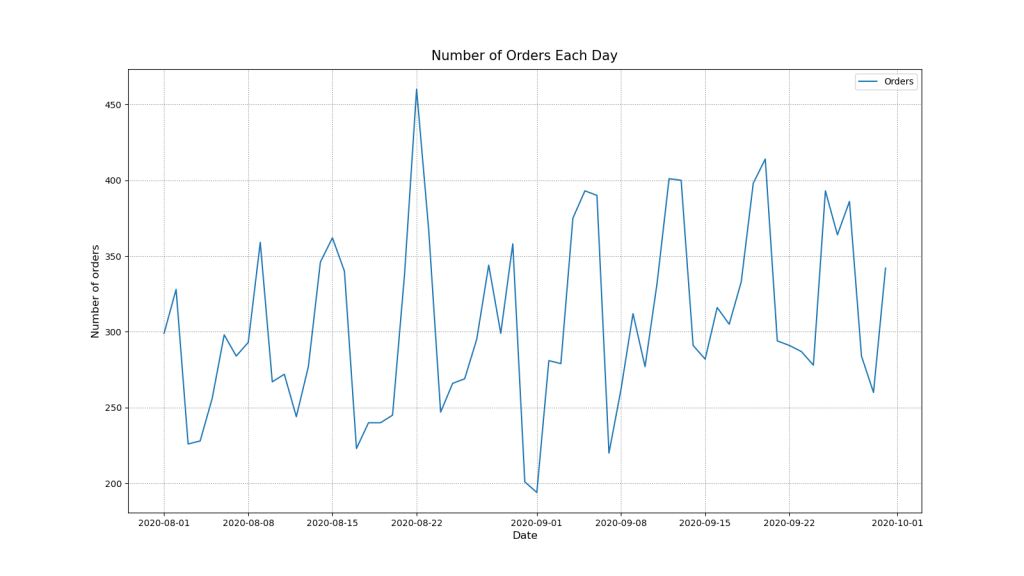

Let’s create a new DataFrame with daily frequency and number of orders

daily_df = df.groupby(pd.Grouper(key=’TIMESTAMP’, freq=’D’)).size().reset_index(name=’ORDERS’)

daily_df.set_index(‘TIMESTAMP’, inplace=True)

daily_df.index.freq = ‘D’ # To keep pandas inference in check!

print(daily_df.head())

print(daily_df.describe())

RDERS

TIMESTAMP

2020-08-01 299

2020-08-02 328

2020-08-03 226

2020-08-04 228

2020-08-05 256

ORDERS

count 61.000000

mean 306.655738

std 58.949381

min 194.000000

25% 267.000000

50% 294.000000

75% 346.000000

max 460.000000

Let’s plot the number of orders per day

def orders_per_day(df: pd.DataFrame) -> None:

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

ax.plot(df.index, df['ORDERS'])

# Labels

ax.set_title("Number of Orders Each Day", fontsize=15, pad=10)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

# Grid & Legend

plt.grid(linestyle=":", color='grey')

plt.legend(["Orders"])

plt.savefig('salesnumberofdays.png')

orders_per_day(daily_df)

plt.savefig(‘salesnumberoforders.png’)

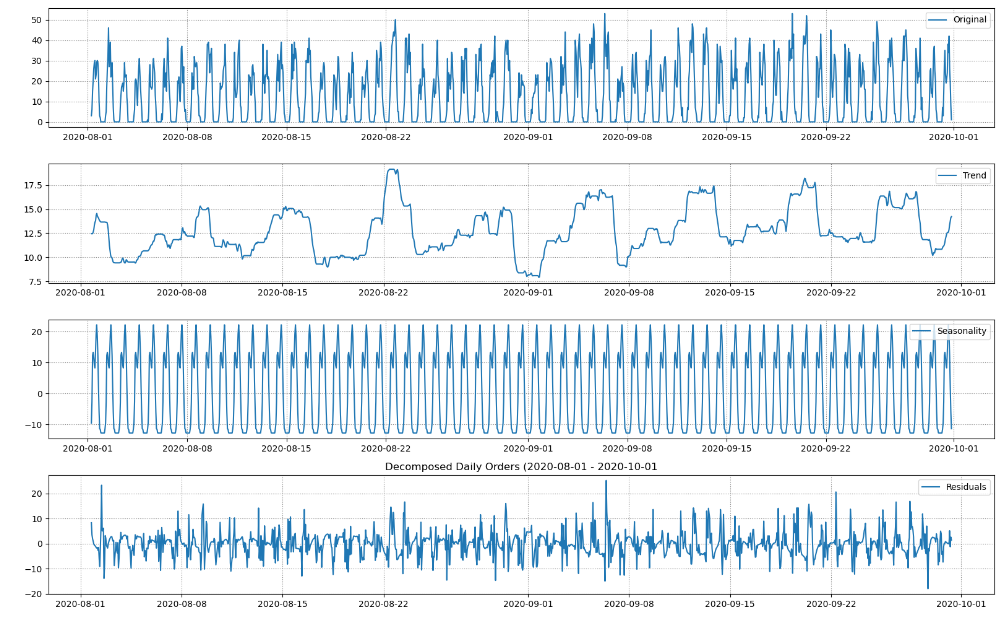

Let’s check the series for trends and seasonality

def decompose_series(df: pd.DataFrame) -> None:

# Decomposition

decomposition = seasonal_decompose(df)

trend = decomposition.trend

seasonal = decomposition.seasonal

residual = decomposition.resid

#Figure

fig, (ax1,ax2,ax3,ax4) = plt.subplots(4,1, figsize=(16,10), facecolor='w')

ax1.plot(df, label='Original')

ax2.plot(trend, label='Trend')

ax3.plot(seasonal,label='Seasonality')

ax4.plot(residual, label='Residuals')

# Legend

ax1.legend(loc='upper right')

ax2.legend(loc='upper right')

ax3.legend(loc='upper right')

ax4.legend(loc='upper right')

ax1.grid(linestyle=":", color='grey')

ax2.grid(linestyle=":", color='grey')

ax3.grid(linestyle=":", color='grey')

ax4.grid(linestyle=":", color='grey')

plt.title('Decomposed Daily Orders (2020-08-01 - 2020-10-01')

plt.tight_layout()

plt.savefig('salesdecomposeseries.png')

decompose_series(daily_df)

- Trend: There is a general rising trend for the given time period. However, it is not constant. Number of orders decreases around 9th of september but then recovers resulting in an approx. 7% overall increase for the observed time period.

- Seasonality: There are clear weekly seasonal patterns. Number of orders is low in the beginning of the week and grows towards the weekend.

- Residuals: No observable patterns left in the residuals.

Let’s plot a heatmap with days of the week and hours of the day vs the number of orders

def orders_weekdays_hours(dataframe: pd.DataFrame) -> None:

# Data

df = dataframe.copy(deep=False)

# Reshaping data for the plot

df["hour"] = pd.DatetimeIndex(df['TIMESTAMP']).hour

df["weekday"] = pd.DatetimeIndex(df['TIMESTAMP']).weekday

daily_activity = df.groupby(by=['weekday','hour']).count()['TIMESTAMP'].unstack()

# Figure Object

fig, ax = plt.subplots(figsize=(10,10), facecolor='w')

yticklabels = ["Mon", "Tue","Wed", "Thu", "Fri", "Sat", "Sun"]

sns.heatmap(daily_activity, robust=True, cmap="Oranges", yticklabels=yticklabels)

# Labeling

ax.set_title("Ordering Patterns", fontsize=15, pad=10)

ax.set_xlabel("Hours of the day (Hours)", fontsize=12, x=.5)

ax.set_ylabel("Day of the week", fontsize=12, y=.5)

plt.savefig('salesorderingpatterns.png')

orders_weekdays_hours(df)

- Each day seems to have two peaks in number of orders.

- Hottest ordering times are slightly different for workdays and weekends.

- During the workdays number of orders peaks at 8am and 16pm with decrease in orders during the lunchtime.

- The weekends exhibit a similar behavior but higher overall number of orders and with different peaks at 10-11am and 15-16pm.

Let’s creating a new DataFrame with hourly frequency number of orders

hourly_df = df.groupby(pd.Grouper(key=’TIMESTAMP’, freq=’1h’)).size().reset_index(name=’ORDERS’)

hourly_df.set_index(‘TIMESTAMP’, inplace=True)

hourly_df.index.freq = ‘H’

print(hourly_df, hourly_df.describe())

ORDERS TIMESTAMP 2020-08-01 06:00:00 3 2020-08-01 07:00:00 6 2020-08-01 08:00:00 15 2020-08-01 09:00:00 20 2020-08-01 10:00:00 26 ... ... 2020-09-30 16:00:00 42 2020-09-30 17:00:00 26 2020-09-30 18:00:00 19 2020-09-30 19:00:00 8 2020-09-30 20:00:00 1 [1455 rows x 1 columns] ORDERS count 1455.000000 mean 12.856357 std 13.733086 min 0.000000 25% 0.000000 50% 8.000000 75% 24.000000 max 53.000000

Let’s plot the number of orders per hour

def orders_per_hour(df: pd.DataFrame, start: datetime, end: datetime ) -> None:

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

ax.plot(df.index, df['ORDERS'])

# Labels

ax.set_title(f"Number of Orders Each Hour ({start.date()} - {end.date()})", fontsize=15, pad=10)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

# Axis Limit

ax.set_xlim([start, end])

# Legend & Grid

plt.grid(linestyle=":", color='grey')

plt.legend(["Orders"])

plt.savefig('salesnumberofeachhours.png')

start = datetime(2020, 8, 1)

end = datetime(2020, 8, 15)

orders_per_hour(hourly_df, start, end)

Let’s decompose these time series

decompose_series(hourly_df)

- Trend: There doesn’t seem to be definite upwards or downwards trend. Recall from the daily plot that there is a trend.

- Seasonality: There is very strong daily seasonal pattern. Recall from the daily plot that there is also a weekly seasonality.

- Residuals: No observable patterns left in the residuals.

Let’s plot rolling mean and STD with window=48

def plot_rolling_mean_and_std(dataframe: pd.DataFrame, window: int) -> None:

df = dataframe.copy()

# Get Things Rolling

roll_mean = df.rolling(window=window).mean()

roll_std = df.rolling(window=window).std()

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

ax.plot(df, label='Original')

ax.plot(roll_mean, label='Rolling Mean')

ax.plot(roll_std, label='Rolling STD')

# Legend & Grid

ax.legend(loc='upper right')

plt.grid(linestyle=":", color='grey')

plt.savefig('salesrollingmean.png')

plot_rolling_mean_and_std(hourly_df, window=48)

- We can see that the mean and the variance of the time series are time-variant.

- Mean and variance seem to follow weekly seasons.

ADF & KPSS Tests

Let’s perform the Augmented Dickey Fuller (ADF) Test:

– The null hypothesis for this test is that there is a unit root.

– The alternate hypothesis is that there is no unit root in the series.

def perform_adf_test(df: pd.DataFrame) -> None:

adf_stat, p_value, n_lags, n_observ, crit_vals, icbest = adfuller(df)

print('\nAugmented Dickey Fuller Test')

print('---'*15)

print('ADF Statistic: %f' % adf_stat)

print('p-value: %f' % p_value)

print(f'Number of lags used: {n_lags}')

print(f'Number of observations used: {n_observ}')

print(f'T values corresponding to adfuller test:')

for key, value in crit_vals.items():

print(key, value)

We also perform the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test for stationarity:

– The null hypothesis for the test is that the data is stationary.

– The alternate hypothesis for the test is that the data is not stationary.

def perform_kpss_test(df: pd.DataFrame) -> None:

kpss_stat, p_value, n_lags, crit_vals = kpss(df, nlags='auto', store=False)

print('\nKwiatkowski-Phillips-Schmidt-Shin test')

print('---'*15)

print('KPSS Statistic: %f' % kpss_stat)

print('p-value: %f' % p_value)

print(f'Number of lags used: {n_lags}')

print(f'Critical values of KPSS test:')

for key, value in crit_vals.items():

print(key, value)

Let’s call these two functions

perform_adf_test(hourly_df)

perform_kpss_test(hourly_df)

Augmented Dickey Fuller Test --------------------------------------------- ADF Statistic: -3.464712 p-value: 0.008941 Number of lags used: 24 Number of observations used: 1430 T values corresponding to adfuller test: 1% -3.434931172941245 5% -2.8635632730206857 10% -2.567847177857108 Kwiatkowski-Phillips-Schmidt-Shin test --------------------------------------------- KPSS Statistic: 0.396855 p-value: 0.078511 Number of lags used: 20 Critical values of KPSS test: 10% 0.347 5% 0.463 2.5% 0.574 1% 0.739

- Since ADF Statistic -3.46 < -3.43 and p-value: 0.0089 < 0.05 we can reject the N0 hypothesis in the favor of NA. According to the ADF test, our time series have no unit root.

- Since KPSS Statistic 0.396 < 0.463 and 0.078 > 0.05 we fail to reject the N0 hypothesis. According to the KPSS test, our time series are trend-stationary.

This is consistent with our observation that rolling mean and STD follow a weekly trend.

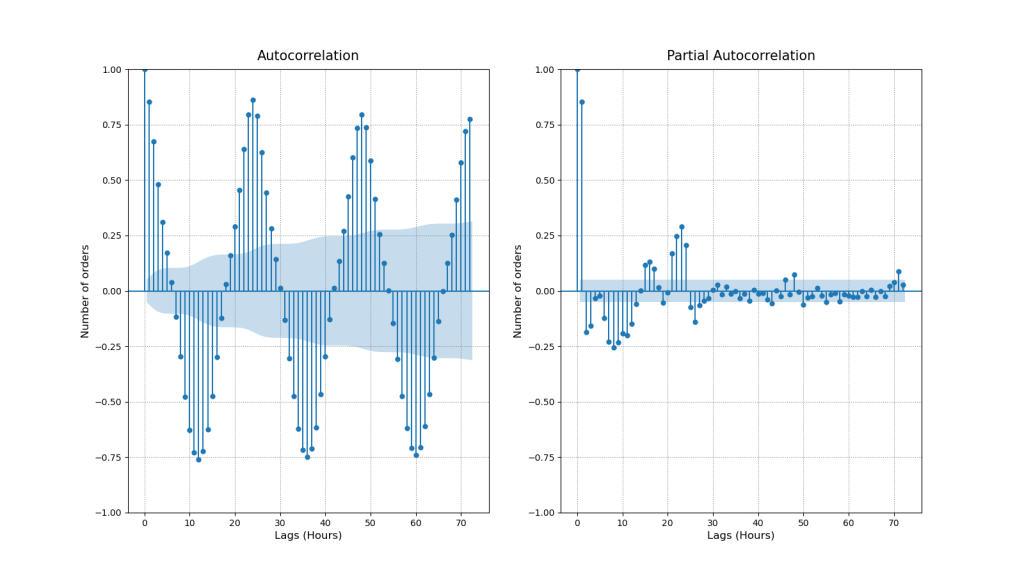

ACF & PACF

Let’s invoke ACF and PACF to identify the lags that have high correlations

def plot_acf_pacf(df: pd.DataFrame, acf_lags: int, pacf_lags: int) -> None:

# Figure

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(16,9), facecolor='w')

# ACF & PACF

plot_acf(df['ORDERS'], ax=ax1, lags=acf_lags)

plot_pacf(df['ORDERS'], ax=ax2, lags=pacf_lags, method='ywm')

# Labels

ax1.set_title("Autocorrelation", fontsize=15, pad=10)

ax1.set_ylabel("Number of orders", fontsize=12)

ax1.set_xlabel("Lags (Hours)", fontsize=12)

ax2.set_title("Partial Autocorrelation", fontsize=15, pad=10)

ax2.set_ylabel("Number of orders", fontsize=12)

ax2.set_xlabel("Lags (Hours)", fontsize=12)

# Legend & Grid

ax1.grid(linestyle=":", color='grey')

ax2.grid(linestyle=":", color='grey')

plt.savefig('salesautocorrelation.png')

plot_acf_pacf(hourly_df, acf_lags=72, pacf_lags= 72)

- ACF

- As we already knew our series are seasonal and our ACF plot confirms this pattern. If we plot more lags we will also observe that significance of the lags is gradually declining.

- First significant lag is lag 1. The number of daily orders raises/decreases gradually from hour to hour. Hence the orders during the previous hour might tell us something about orders during the current hour.

- Next important lags are 12 and 24. These are deterministic seasonal patterns connected with day/night cycles. 12 hour lag is negatively correlated because when at 8:00 am number of orders starts to increase at 20:00 pm the number of orders is already decreasing. However, 24 hour lag shows that number of orders made today at 16:00 pm might tell us about the number of orders to be made tomorrow at 16:00 pm.

- PACF

- We can see that lag 1 and 24 have the highest correlations. This means that seasons 24 hours apart are directly inter-correlated regardless of what is happening in between.

We can take a detailed look at the above Lags of interest

def lag_plots(df: pd.DataFrame) -> None:

# Figure

fig, (ax1, ax2, ax3) = plt.subplots(1, 3, figsize=(16,9), facecolor='w')

# Lags

lag_plot(df['ORDERS'], lag=1, ax=ax1, c='#187bcd')

lag_plot(df['ORDERS'], lag=12, ax=ax2, c='grey')

lag_plot(df['ORDERS'], lag=24, ax=ax3, c='#187bcd')

# Labels

ax1.set_title("y(t+1)", fontsize=15, pad=10)

ax2.set_title("y(t+12)", fontsize=15, pad=10)

ax3.set_title("y(t+24)", fontsize=15, pad=10)

# Legend & Grid

ax1.grid(linestyle=":", color='grey')

ax2.grid(linestyle=":", color='grey')

ax3.grid(linestyle=":", color='grey')

lag_plots(hourly_df)

Lags 1, 12, and 24 follow the ACF correlation trends: both high positive linear correlations (Lags 1 and 24) and a strongly negative non-linear correlation (Lag 12) are confirmed.

SARIMA Model

The SARIMA model is specified as follows

(p,d,q) x (P,D,Q)s

where

- Trend Elements are:

- p: Autoregressive order

- d: Difference order

- q: Moving average order

- Seasonal Elements are:

- P: Seasonal autoregressive order.

- D: Seasonal difference order. D=1 would calculate a first order seasonal difference

- Q: Seasonal moving average order. Q=1 would use a first order errors in the model

- s Single seasonal period

We will use the Box–Jenkins method for SARIMA parameter tuning.

Let’s split the input dataframe into train/test sets as 75% / 15%.

def train_test_split(df: pd.DataFrame, train_set, test_set):

train_set = df[df.index <= train_end]

test_set = df[df.index > train_end]

return train_set, test_set

warnings.simplefilter(‘ignore’, ConvergenceWarning)

train_end = datetime(2020,9,15)

test_end = datetime(2020,9,30)

train_df, test_df = train_test_split(hourly_df, train_end, test_end)

Let's set the hyper-parameters p, d, q = 1, 1, 1 P, D, Q = 2, 1, 1 s = 24 and fit the SARIMA model

sarima_model = SARIMAX(train_df, order=(p, d, q), seasonal_order=(P, D, Q, s))

sarima_model_fit = sarima_model.fit(disp=0)

print(sarima_model_fit.summary())

SARIMAX Results

==========================================================================================

Dep. Variable: ORDERS No. Observations: 1075

Model: SARIMAX(1, 1, 1)x(2, 1, 1, 24) Log Likelihood -3158.989

Date: Sat, 14 Jan 2023 AIC 6329.979

Time: 11:21:55 BIC 6359.718

Sample: 08-01-2020 HQIC 6341.255

- 09-15-2020

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.3729 0.027 13.720 0.000 0.320 0.426

ma.L1 -0.9415 0.012 -75.980 0.000 -0.966 -0.917

ar.S.L24 0.1375 0.024 5.666 0.000 0.090 0.185

ar.S.L48 -0.1325 0.025 -5.272 0.000 -0.182 -0.083

ma.S.L24 -0.9997 2.136 -0.468 0.640 -5.186 3.187

sigma2 21.9775 46.728 0.470 0.638 -69.607 113.562

===================================================================================

Ljung-Box (L1) (Q): 0.64 Jarque-Bera (JB): 317.47

Prob(Q): 0.42 Prob(JB): 0.00

Heteroskedasticity (H): 1.27 Skew: 0.46

Prob(H) (two-sided): 0.03 Kurtosis: 5.53

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Let’s plot the SARIMA diagnostics

sarima_model_fit.plot_diagnostics(figsize=(16, 9))

plt.savefig(‘salesarimaxdiagplot.png’)

- The standardize residual plot: The residuals over time don’t display any obvious patterns. They appear as white noise.

- The Normal Q-Q-plot: Shows that the ordered distribution of residuals follows the linear trend of the samples taken from a standard normal distribution with N(0, 1). However, the slight curving indicates that our distribution has heavier tails.

- Histogram and estimated density plot: The KDE follows the N(0,1) line however with noticeable differences. As mentioned before our distribution has heavier tails.

- The Correlogram plot: Shows that the time series residuals have low correlation with lagged versions of itself. Meaning there are no patterns left to extract in the residuals.

Let’s compare the test data vs SARIMA predictions

pred_start_date = test_df.index[0]

pred_end_date = test_df.index[-1]

sarima_predictions = sarima_model_fit.predict(start=pred_start_date, end=pred_end_date)

sarima_residuals = test_df[‘ORDERS’] – sarima_predictions

def plot_test_predictions(test_df: pd.DataFrame, predictions) -> None:

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

ax.plot(test_df, label='Testing Set')

ax.plot(predictions, label='Forecast')

# Labels

ax.set_title("Test vs Predictions", fontsize=15, pad=10)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

# Legend & Grid

ax.grid(linestyle=":", color='grey')

ax.legend()

plt.savefig('salesarimaxtestpredictions.png')

plot_test_predictions(test_df, sarima_predictions)

Let’s get the SARIMA evaluation data

sarima_aic = sarima_model_fit.aic

sarima_bic = sarima_model_fit.bic

sarima_mean_squared_error = sarima_model_fit.mse

sarima_sum_squared_error=sarima_model_fit.sse

sarima_root_mean_squared_error = np.sqrt(np.mean(sarima_residuals**2))

print(f’Akaike information criterion | AIC: {sarima_aic}’)

print(f’Bayesian information criterion | BIC: {sarima_bic}’)

print(f’Mean Squared Error | MSE: {sarima_mean_squared_error}’)

print(f’Sum Squared Error | SSE: {sarima_sum_squared_error}’)

print(f’Root Mean Squared Error | RMSE: {sarima_root_mean_squared_error}’)

Akaike information criterion | AIC: 6329.978772260314 Bayesian information criterion | BIC: 6359.718044919224 Mean Squared Error | MSE: 23.867974361783705 Sum Squared Error | SSE: 25658.072438917483 Root Mean Squared Error | RMSE: 5.6716207290283

Let’s perform the SARIMA forecast of hourly orders

Forecast Window

days = 24

hours = days * 24

sarima_forecast = sarima_model_fit.forecast(hours)

sarima_forecast_series = pd.Series(sarima_forecast, index=sarima_forecast.index)

Since negative orders are not possible, we can trim them

sarima_forecast_series[sarima_forecast_series < 0] = 0

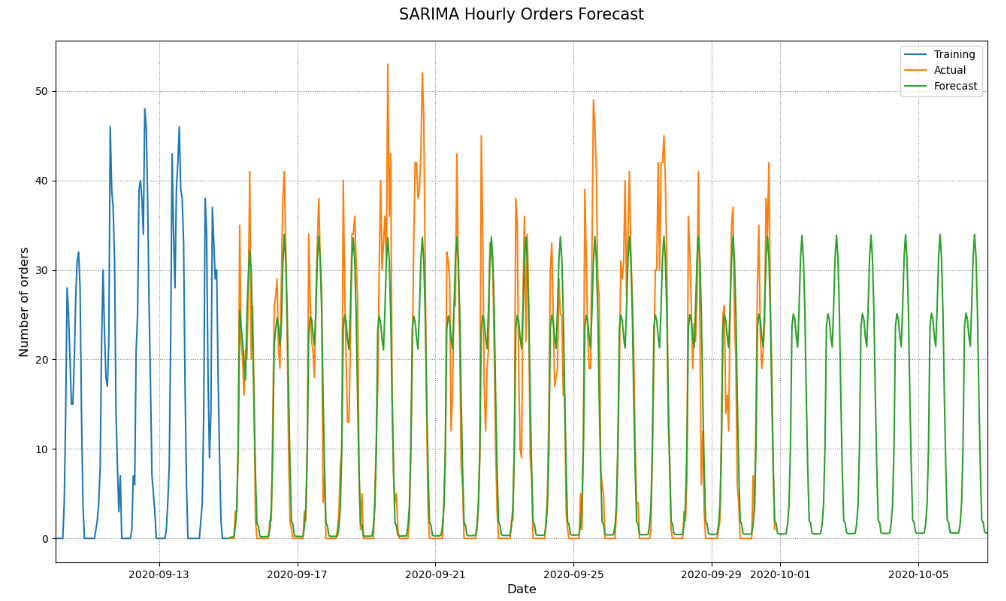

Let’s plot the test, train and forecast values

def plot_sarima_forecast(train_df: pd.DataFrame, test_df: pd.DataFrame, fc_series: pd.Series) -> None:

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

# Plot Train, Test and Forecast.

ax.plot(train_df['ORDERS'], label='Training')

ax.plot(test_df['ORDERS'], label='Actual')

ax.plot(fc_series, label='Forecast')

# Labels

ax.set_title("SARIMA Hourly Orders Forecast", fontsize=15, pad=20)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

xmin = datetime(2020, 9, 10)

xmax = datetime(2020, 10, 7)

ax = plt.gca()

ax.set_xlim([xmin, xmax])

# Legend & Grid

ax.grid(linestyle=":", color='grey')

ax.legend()

plt.savefig('salesarimahorlyforecast.png')

plot_sarima_forecast(train_df, test_df, sarima_forecast_series)

- Our SARIMA model predicts the overall hourly ordering patterns pretty well. It captures the two daily peaks and the lunchtime valley between them.

- However, it fails to predict weekly patterns. Every day in our forecast seem to be the same. If this model was sent to production we would be able to predict the number of orders every hour but that prediction would be based on the assumption that the number of orders is the same every day.

- While this model doesn’t have a great long term predictive power it can serve as a solid baseline for our next models.

SARIMAX Model

Let’s prepare the data

hour_weekday_df = hourly_df.copy()

hour_weekday_df[‘weekday_exog’] = hour_weekday_df.index.weekday

print(hour_weekday_df.head(10))

ORDERS weekday_exog TIMESTAMP 2020-08-01 06:00:00 3 5 2020-08-01 07:00:00 6 5 2020-08-01 08:00:00 15 5 2020-08-01 09:00:00 20 5 2020-08-01 10:00:00 26 5 2020-08-01 11:00:00 29 5 2020-08-01 12:00:00 30 5 2020-08-01 13:00:00 21 5 2020-08-01 14:00:00 23 5 2020-08-01 15:00:00 29 5

weekday_exog = hour_weekday_df[(hour_weekday_df != 0).all(1)]

weekday_exog = weekday_exog.groupby(weekday_exog.index.weekday)[‘ORDERS’].mean()

print(weekday_exog.head(7))

TIMESTAMP 1 17.386364 2 18.591241 3 18.628099 4 19.891304 5 21.939597 6 25.715385 Name: ORDERS, dtype: float64

weekday_exog = {key: (weekday_exog[key] / weekday_exog[1]) for key in weekday_exog.keys()}

print(weekday_exog)

{1: 1.0, 2: 1.0693001288106483, 3: 1.0714200831847889, 4: 1.144075021312873, 5: 1.2618853357897968, 6: 1.4790548014077425}

hour_weekday_df.replace({“weekday_exog”: weekday_exog})

1455 rows × 2 columns

Let’s perform a grid search for the SARIMAX HPO

p = range(1, 3)

d = range(1, 2)

q = range(1, 3)

s = 24

pdq = list(itertools.product(p, d, q))

seasonal_pdq = [(x[0], x[1], x[2], s) for x in pdq]

def grid_search_sarimax(train_set: pd.DataFrame) -> None:

# Supress UserWarnings

warnings.simplefilter('ignore', category=UserWarning)

# Grid Search

for order in pdq:

for seasonal_order in seasonal_pdq:

model = SARIMAX(train_set['ORDERS'],

order=order,

seasonal_order=seasonal_order,

exog=train_set['weekday_exog']

)

results = model.fit(disp=0)

print(f'ARIMA{order}x{seasonal_order} -> AIC: {results.aic}, BIC:{results.bic}, MSE: {results.mse}')

train_end = datetime(2020,9,15)

test_end = datetime(2020,9,30)

train_df, test_df = train_test_split(hour_weekday_df, train_end, test_end)

Set Hyper-Parameters

p, d, q = 1, 1, 2

P, D, Q = 2, 1, 2

s = 24

exog = train_df[‘weekday_exog’]

Fit SARIMAX

sarimax_model = SARIMAX(train_df[‘ORDERS’],

order=(p, d, q),

seasonal_order=(P, D, Q, s),

exog=exog)

sarimax_model_fit = sarimax_model.fit(disp=0)

Print the summary report

print(sarimax_model_fit.summary())

SARIMAX Results

==========================================================================================

Dep. Variable: ORDERS No. Observations: 1075

Model: SARIMAX(1, 1, 2)x(2, 1, 2, 24) Log Likelihood -3118.452

Date: Sat, 14 Jan 2023 AIC 6254.904

Time: 11:29:13 BIC 6299.513

Sample: 08-01-2020 HQIC 6271.818

- 09-15-2020

Covariance Type: opg

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

weekday_exog 0.8400 0.138 6.074 0.000 0.569 1.111

ar.L1 0.4934 0.063 7.777 0.000 0.369 0.618

ma.L1 -1.1571 0.080 -14.553 0.000 -1.313 -1.001

ma.L2 0.1576 0.070 2.261 0.024 0.021 0.294

ar.S.L24 0.8878 0.052 17.064 0.000 0.786 0.990

ar.S.L48 -0.2623 0.024 -10.922 0.000 -0.309 -0.215

ma.S.L24 -1.7497 0.052 -33.831 0.000 -1.851 -1.648

ma.S.L48 0.7717 0.051 15.081 0.000 0.671 0.872

sigma2 20.6048 0.887 23.226 0.000 18.866 22.344

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 339.16

Prob(Q): 0.98 Prob(JB): 0.00

Heteroskedasticity (H): 1.34 Skew: 0.54

Prob(H) (two-sided): 0.01 Kurtosis: 5.57

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Let’s plot the SARIMAX diagnostics

sarimax_model_fit.plot_diagnostics(figsize=(16, 9))

plt.savefig(‘salesarimaxmodelfit.png’)

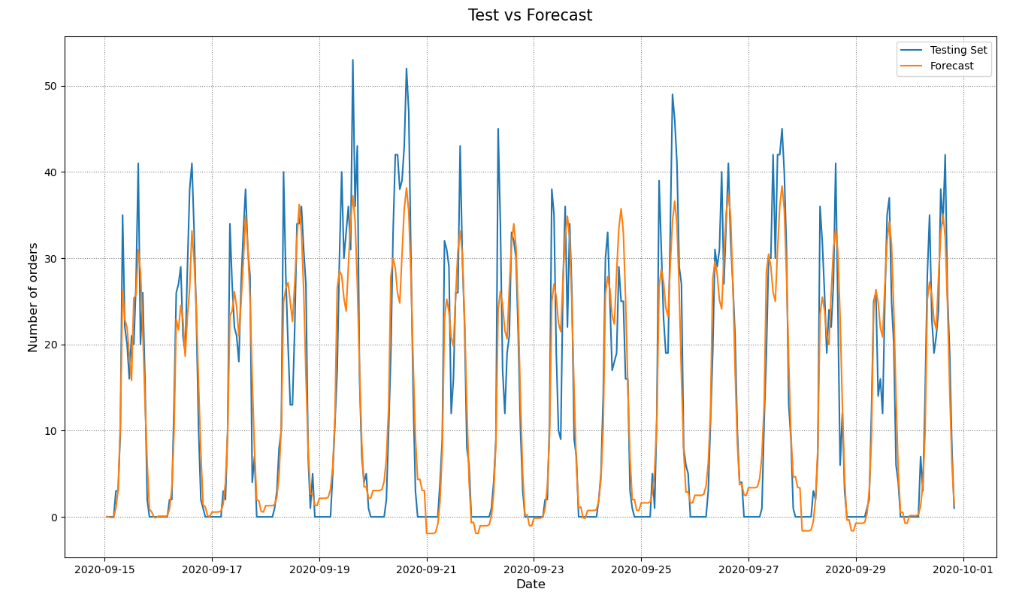

Let’s plot the predictions

pred_start_date = test_df.index[0]

pred_end_date = test_df.index[-1]

exog = test_df[‘weekday_exog’]

predictions = sarimax_model_fit.predict(start=pred_start_date, end=pred_end_date, exog=exog)

residuals = test_df[‘ORDERS’] – predictions

def plot_sarimax_test(test_set: pd.DataFrame, predictions: pd.Series) -> None:

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

ax.plot(test_set['ORDERS'], label='Testing Set')

ax.plot(predictions, label='Forecast')

# Labels

ax.set_title("Test vs Forecast", fontsize=15, pad=15)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

# Legend & Grid

ax.grid(linestyle=":", color='grey')

ax.legend()

plt.savefig('salessarimaxtestforecastplot.png')

plot_sarimax_test(test_df, predictions)

Let’s get the SARIMAX evaluation data

sarimax_aic = sarimax_model_fit.aic

sarimax_bic = sarimax_model_fit.bic

sarimax_mean_squared_error = sarimax_model_fit.mse

sarimax_sum_squared_error=sarimax_model_fit.sse

sarimax_root_mean_squared_error = np.sqrt(np.mean(residuals**2))

print(f’Akaike information criterion | AIC: {sarimax_aic}’)

print(f’Bayesian information criterion | BIC: {sarimax_bic}’)

print(f’Mean Squared Error | MSE: {sarimax_mean_squared_error}’)

print(f’Sum Squared Error | SSE: {sarimax_sum_squared_error}’)

print(f’Root Mean Squared Error | RMSE: {sarimax_root_mean_squared_error}’)

Akaike information criterion | AIC: 6254.90400948669 Bayesian information criterion | BIC: 6299.512918475054 Mean Squared Error | MSE: 22.10675398176249 Sum Squared Error | SSE: 23764.760530394677 Root Mean Squared Error | RMSE: 5.132961570576301

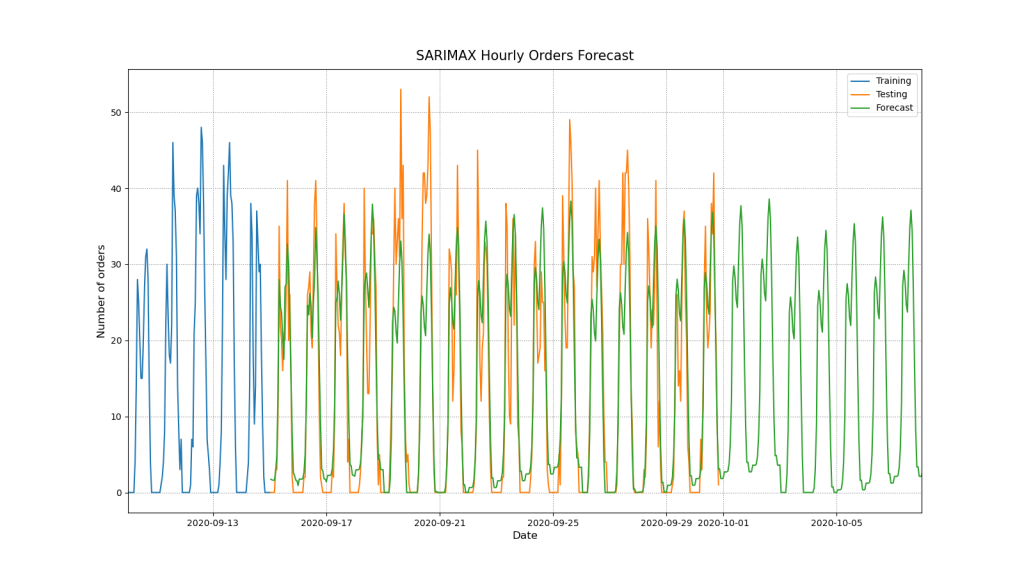

Let’s plot the train, test, and predicted values

Forecast Window

days = 24

hours = (days * 24)+1

exog = pd.date_range(start=’2020-10-01′, end=’2020-10-25′, freq=’1H’)

fc = sarimax_model_fit.forecast(hours, exog=exog.weekday)

fc_series = pd.Series(fc, index=fc.index)

Since negative orders are not possible we can trim them.

fc_series[fc_series < 0] = 0

def plot_sarimax_forecast(train_df: pd.DataFrame, test_df: pd.DataFrame, fc_series: pd.Series) -> None:

# Figure

fig, ax = plt.subplots(figsize=(16,9), facecolor='w')

# Plot Train, Test and Forecast.

ax.plot(train_df['ORDERS'], label='Training')

ax.plot(test_df['ORDERS'], label='Testing')

ax.plot(fc_series, label='Forecast')

# Labels

ax.set_title("SARIMAX Hourly Orders Forecast", fontsize=15, pad=10)

ax.set_ylabel("Number of orders", fontsize=12)

ax.set_xlabel("Date", fontsize=12)

# Axis Limits

xmin = datetime(2020, 9, 10)

xmax = datetime(2020, 10, 8)

ax = plt.gca()

ax.set_xlim([xmin, xmax])

# Legend & Grid

ax.grid(linestyle=":", color='grey')

ax.legend()

plt.savefig('salesarimaxhourlyordersforecast.png')

plot_sarimax_forecast(train_df, test_df, fc_series)

Model Comparison

Let’s compare the two models

model_comparison = pd.DataFrame({‘Model’:[‘SARIMA(1, 1, 1)(2, 1, 1)24′,’SARIMAX(1, 1, 2)(2, 1, 2)24’],

‘AIC’:[sarima_aic, sarimax_aic],

‘BIC’:[sarima_bic, sarimax_bic],

‘MSE’: [sarima_mean_squared_error, sarimax_mean_squared_error],

‘SSE’: [sarima_sum_squared_error, sarimax_sum_squared_error],

‘RMSE’: [sarima_root_mean_squared_error, sarimax_root_mean_squared_error]})

model_comparison.head()

Summary

- SARIMAX performs better than SARIMA in terms of AIC, BIC, MSE, SSE, and RMSE

- There is a general rising trend for the given time period.

- ADF Statistic -3.46 < -3.43 and p-value: 0.0089 < 0.05, so we can reject the null hypophysis N0 in favour of NA, i.e. our series have no unit root.

- Since KPSS Statistic 0.396 < 0.463 and 0.078 > 0.05 we fail to reject the null hypothesis N0, and so our series are trend-stationary.

- ACF confirmed deterministic seasonal patterns connected with day/night cycles.

- PACF shows that lag 1 and 24 have the highest correlation. This means that seasons 24 hours apart are directly correlated regardless of what is happening in between.

- SARIMAX: Log Likelihood -3118.452,

- Ljung-Box (L1) (Q): 0.00

- Prob(Q): 0.98

- Prob(H) (two-sided): 0.01

- Heteroskedasticity (H): 1.34

- Jarque-Bera (JB): 339.23

- Skew: 0.54

- Kurtosis: 5.57

- SARIMA:

- Log Likelihood -3158.989

- Ljung-Box (L1) (Q): 0.64

- Heteroskedasticity (H): 1.27

- Prob(H) (two-sided): 0.03

- Jarque-Bera (JB): 317.41

- Skew: 0.46

- Kurtosis: 5.53

- The log-likelihood value of a regression model is a way to measure the goodness of fit for a model. The higher the value of the log-likelihood, the better a model fits a dataset. In our case, Log Likelihood SARIMA < Log Likelihood SARIMAX.

- Heteroscedasticity is what you have in your data when the conditional variance in your data is not constant. In our case, Heteroskedasticity SARIMAX > Heteroskedasticity SARIMA.

- The Jarque-Bera test is a goodness-of-fit test that determines whether or not sample data have skewness/kurtosis that matches a normal distribution. The test statistic of the Jarque-Bera (JB) test is always a positive number and if it’s far from zero, it indicates that the sample data do not have a normal distribution. In our case, JB SARIMAX > JB SARIMA.

- A two-tailed test, in statistics, is a method in which the critical area of a distribution is two-sided and tests whether a sample is greater than or less than a certain range of values. In our case, Prob(H) (two-sided) SARIMA > Prob(H) (two-sided) SARIMAX.

- Ljung-Box (L1) (Q) SARIMAX << Ljung-Box (L1) (Q) SARIMA. Essentially, it is a test of lack of fit: if the autocorrelations of the residuals are very small, we say that the model doesn’t show ‘significant lack of fit’.

- The Normal Q-Q-plots shows that the ordered distribution of residuals follows the linear trend for both models. However, the slight curving indicates that our distribution has heavier tails.

- Histogram and estimated density plot: The KDE follows the N(0,1) line with slight differences.

- SARIMA: Model succeeded in capturing the underlying hourly ordering patterns with limited accuracy. However, it failed to capture patterns related to days of the week.

- SARIMAX: Model did a better job! It improved the accuracy of the previous model. However, its accuracy is still limited. This model captured the two daily spikes but not when these spikes crossed the mark of 40 orders. Additionally the model predicts orders during the night hours that are very unlikely to occur. It seems that the model would benefit from another exog variable that would apply hourly weights for each hour of the day.

Explore More

Stock Forecasting with FBProphet

S&P 500 Algorithmic Trading with FBProphet

E-Commerce Cohort Analysis in Python

E-Commerce Data Science Use-Case

E-Commerce ML/AI Classification

- Simple E-Commerce Sales BI Analytics

- Brazilian E-Commerce Showcase

- A K-means Cluster Cohort E-Commerce

Embed Socials

Infographic

How do we calculate HQIC information criteria for time series data when we fit SARIMA model?

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

DonateDonate monthlyDonate yearly